Managed Retreat Makes Sense, but the Current Approach Is Not Working

The current approach to managed retreat is most often implemented through post-disaster buyouts. Following a hurricane or severe flooding, for example, a local government will choose to offer homeowners the pre-disaster, fair-market value of their house to move elsewhere rather than rebuild their damaged or destroyed property. The federal government typically provides three-quarters of the funding for these buyouts—via the Federal Emergency Management Agency (FEMA) and the Department of Housing and Urban Development (HUD)—and state and local governments fund the balance and administer the programs. Over the last 40 years, municipalities have relocated nearly 50,000 American households at a cost of about $3.5 billion through buyouts, typically a few homes at a time.

Federal Flood Insurance Is Drowning

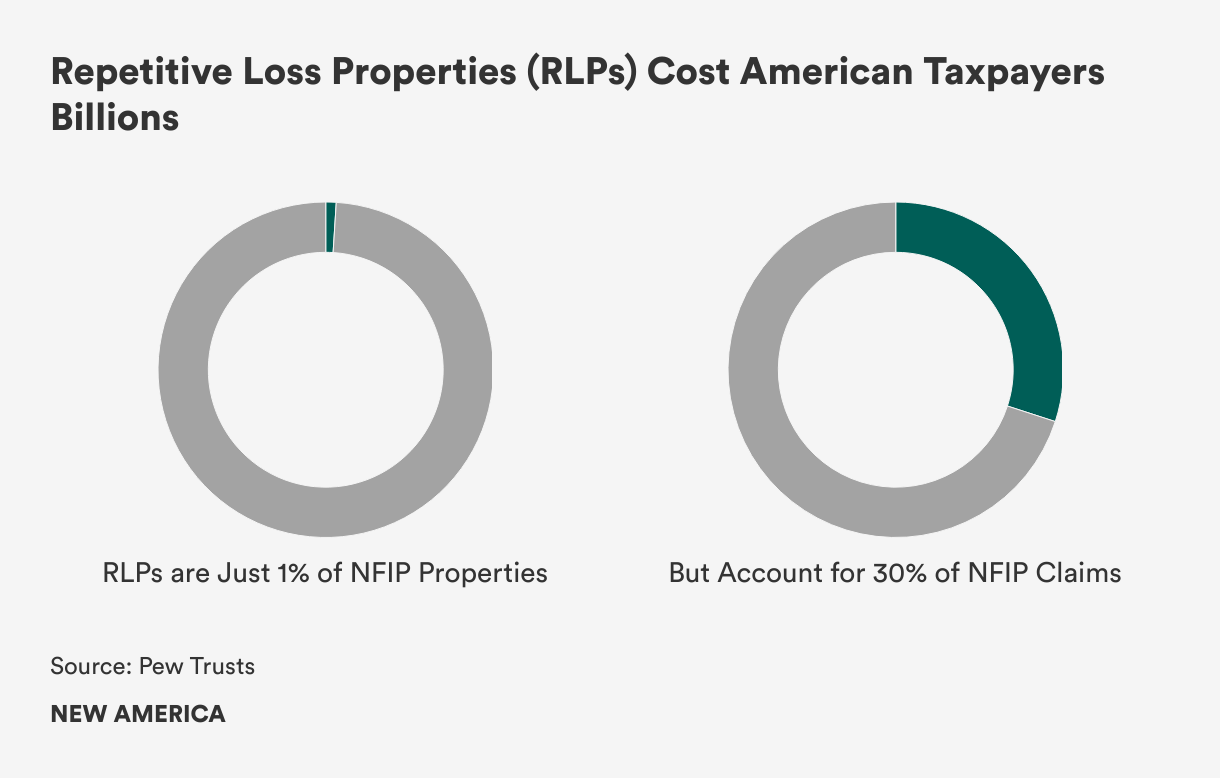

In addition to environmental benefits such as the restoration and conservation of coastal and river ecosystems,1 managed retreat makes significant economic sense. The repeated repair of damaged properties costs American taxpayers billions of dollars each year and places acute financial stress on FEMA’s National Flood Insurance Program (NFIP). Repetitive loss properties (RLPs), defined as properties that have flooded and received claims multiple times, only comprise 1 percent of NFIP properties, but have accounted for over 30 percent of all claim payments. Cumulatively, NFIP has paid more than $22 billion in insurance claims to RLPs, and the issue has only become worse: Between 2009 and 2018, the U.S. added more 64,000 RLPs as Americans continued to move into areas at risk of flooding.

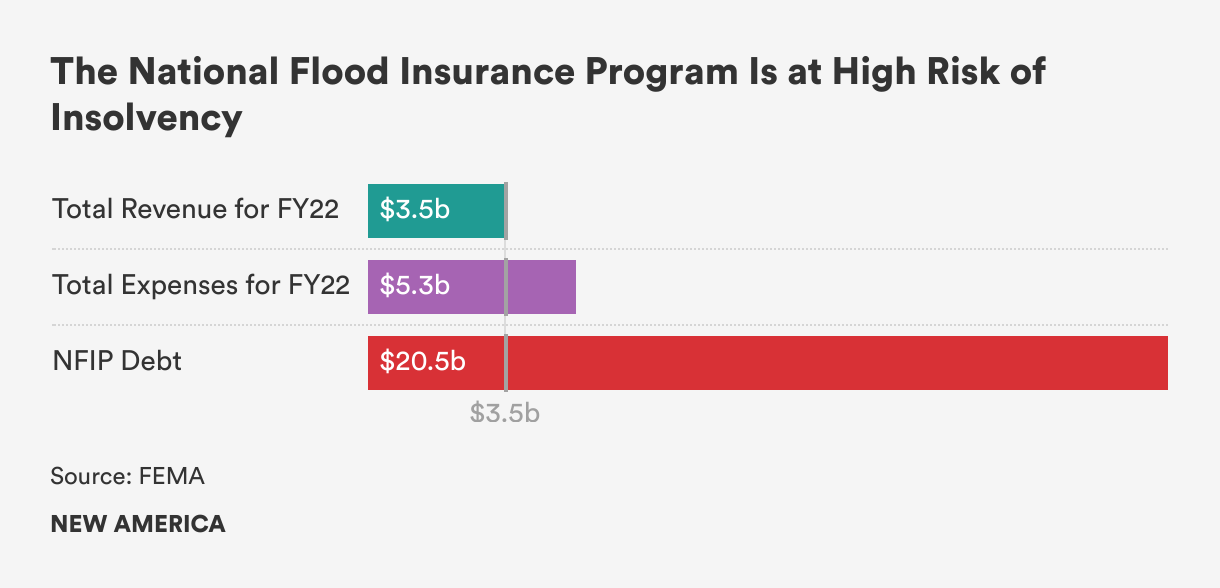

In fact, NFIP is currently at high risk of insolvency and its future is uncertain. The program is $20.5 billion in debt to the U.S. Treasury, and in fiscal year 2022 the program’s total expenses of $5.3 billion far exceeded its revenue of $3.5 billion.2 This financial situation is likely to become more severe as climate change leads to increased flooding and more frequent and stronger storms. Nationally, First Street Foundation projects that expected economic losses from flooding will rise by approximately $12 billion by 2051. It is uncertain whether Congress will continue to reauthorize an increasingly expensive flood insurance program or, alternatively, if legislators will cancel NFIP’s debt.

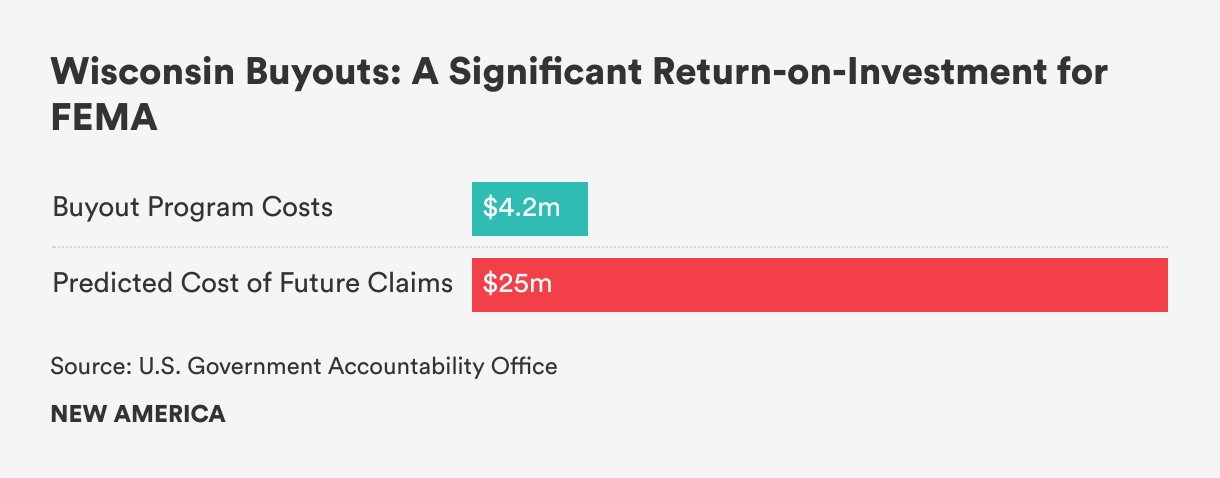

By contrast, buyouts offer a significant return-on-investment by ending the “repair loop” and lowering the costs of future disaster recovery by reducing the number of at-risk homes along the coast or in a floodplain. A 2022 study published by the U.S. Government Accountability Office, for instance, found that 89 buyouts in a Wisconsin floodplain cost FEMA $4.2 million, but helped the agency avoid $25 million in predicted future claims.

Buyouts can also lead to a number of positive social benefits if implemented through a community-centered and equitable approach. Studies show that living under the continuous threat of a natural disaster damages both mental and physical health. Relocating households out of vulnerable areas can prevent injuries and deaths associated with extreme weather events, improve health and wellbeing, and reduce or eliminate the stress and anxiety that comes in anticipation of the next disaster. In the long term, reducing climate risk improves community resilience and sustainability, which helps to ensure that future generations are more safe from climate impacts.

Building Back…Faster

Buyouts remain unpopular despite their environmental, economic, and social benefits, however. Local governments and their residents obstruct and delay these relocations for several reasons, even when it is clear that buyouts will be less expensive and less chaotic than later, post-disaster moves. For smaller municipalities, the loss of part of their tax base can pose a significant financial challenge, as the government is obliged to still provide costly public services to remaining residents. And for homeowners, the thought of moving away from their neighborhood or community can be gut-wrenching. There are ultimately few easy solutions to coax local governments to part with taxpayers or to encourage residents to leave their homes.

Procedural and structural factors related to post-disaster aid also incentivize rebuilding damaged homes. First, most buyout funding only becomes available after a federally declared natural disaster, and this money can take years to reach local coffers. Research from the Natural Resources Defense Council (NRDC) found that buyout negotiations usually take over five years to finalize. FEMA meanwhile provides flood insurance to all households in a floodplain through the NFIP, and insurance payouts arrive faster than buyout funds. As a result, many homeowners do not wait for a buyout offer and instead rebuild their houses, often multiple times, with NFIP funding. In fact, more than 30,000 severe repetitive loss properties—properties that have flooded an average of five times—are covered under NFIP. And sometimes, homeowners repair or rebuild their house multiple times before finally choosing to leave, resulting in billions of dollars in sunk costs for the U.S. government.

Second, buyouts are incredibly complicated to administer. Smaller and poorer municipalities often lack the technical expertise and staffing capacity to apply for competitive buyout programs and other grant opportunities, and then to navigate complex real estate transactions and land acquisitions if the funding is awarded. So wealthier and larger communities with better-staffed governments can more effectively plan for and fund their retreat, while marginalized or less-populated communities struggle to secure federal dollars and relocate residents, leaving many little choice but to rebuild.

Finally, previous buyout projects have consistently yielded unjust and inequitable outcomes, largely as a result of procedural and distributive justice challenges. Use of the pre-disaster, fair market value of a home to calculate the purchase offer, for example, overwhelmingly disadvantages those whose properties are low-value, undervalued, or in poorer condition—often low- to moderate-income homeowners and communities of color. Their purchase offers are significantly lower than what is necessary to acquire a house in a less flood-prone area, leaving them more susceptible to risk and displacement.

The implementation of buyouts also reveals and exacerbates stark racial disparities in the United States. An NPR analysis found that 85 percent of FEMA’s property acquisition funds have been allocated to predominantly white communities. And a comprehensive 30-year study by Rice University researchers shows that, while buyouts effectively reduce household flood risk, they often contribute to increased racial segregation residentially. These equity and justice challenges underscore an urgent need for more proactive planning and critical analysis around how buyout programs are implemented.

Case Study: Fair Bluff, North Carolina

Fair Bluff, a town on North Carolina’s southeast coastal plain with fewer than 1,000 residents, experienced significant damage from Hurricane Matthew in 2016 and was heavily impacted by Hurricane Florence two years later. Matthew caused widespread flooding, affecting nearly a quarter of all homes and submerging Main Street under four feet of water. Critical infrastructure was also destroyed, and nearly half the town’s population has moved away.

These severe and repeated impacts have placed tremendous strain on Fair Bluff’s financial resources and have contributed to steady population decline. This small community’s future is at risk as a result. Yet the town’s situation is not unique. Rather, it exemplifies the uncertainty faced by many small and rural communities that are grappling with worsening climate impacts.

As a small municipality with a limited tax base, Fair Bluff lacks the necessary funding and staff capacity to independently plan and implement large-scale recovery projects and must therefore rely on outside assistance. After Hurricane Matthew, for example, the State of North Carolina decided to fund three new city staff positions, and support from local universities and county government was critical in applying for and receiving federal recovery assistance.

But even as some federal agencies granted money after Hurricane Matthew to redevelop downtown, FEMA purchased 34 badly damaged properties, causing the population (and tax base) to decline further. Although buyouts are an effective strategy to reduce risk, this policy also disrupted the community’s social and economic structures, as residents typically relocated outside of Fair Bluff to neighboring towns with lower flood risks. These moves drained financial resources and created more challenges to recovery and redevelopment after the storms. Fair Bluff is struggling to both recover economically and build resilience for future disasters as a result.

Some residents have left Fair Bluffs permanently, while others remain and are committed to building a safe and vibrant community. In March 2023, FEMA approved the second phase of a project to buy out and demolish 51 commercial properties in the downtown area, which was hardest hit by Matthew, and to remediate the area into its natural condition as part of the floodplain. The goal is to utilize the area as greenspace and redevelop downtown on higher ground. However, the long-term future is still uncertain, as FEMA’s process is slow-moving and it can take multiple years to complete projects, leaving homeowners and the town in a discouraging limbo. If another storm hits, residents will face a difficult choice: attempt to rebuild yet again or leave for good.

Citations

- Dunes, wetlands, and other natural barriers further help protect communities from future storms and flooding.

- Insurance payouts account for the majority of NFIP’s expenses. Costs are also related to floodplain mapping and flood-related grants.