Beyond Rebuilding

Abstract

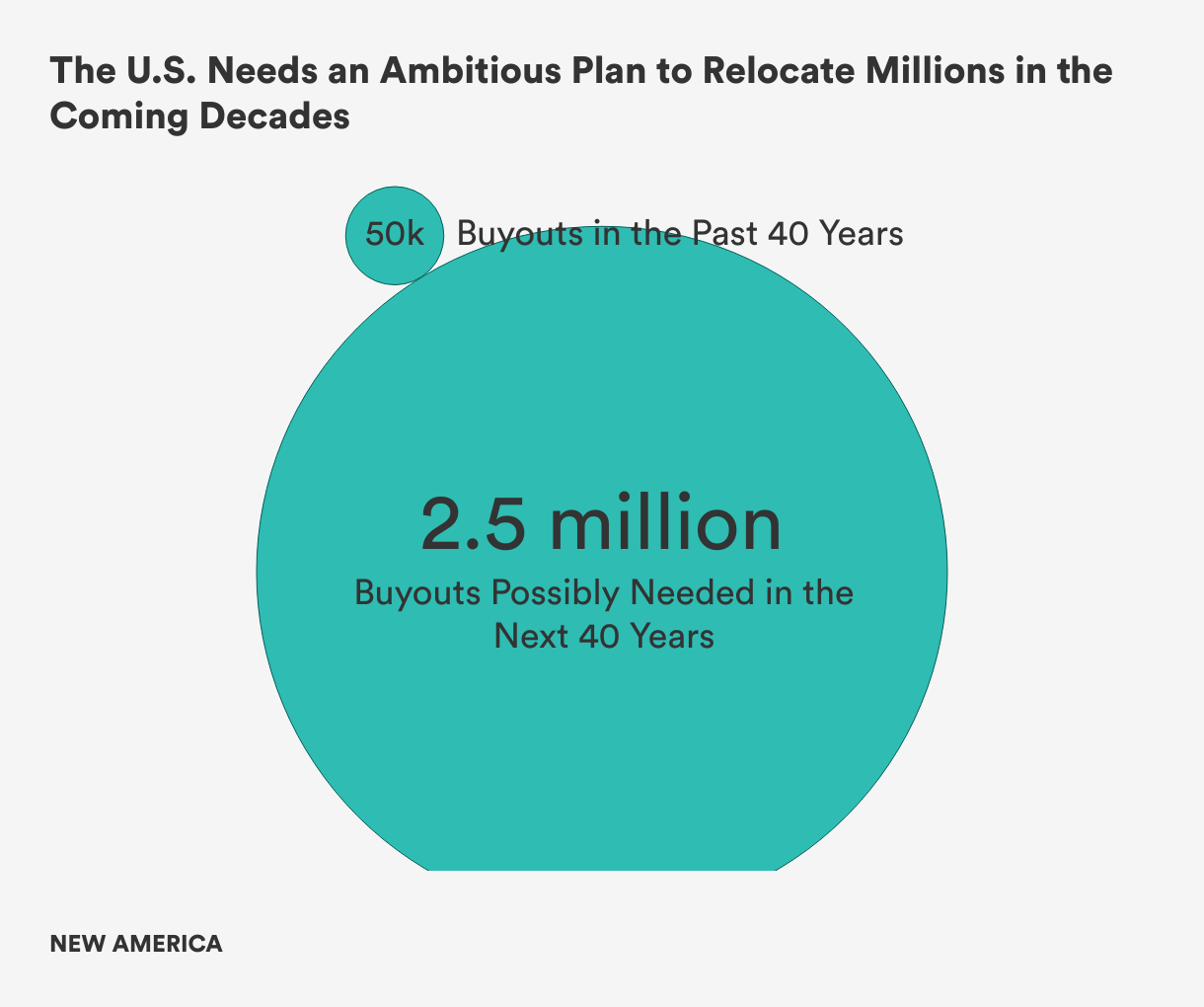

Climate impacts such as sea-level rise, extreme heat and drought, and sudden natural disasters could force over 20 million Americans to permanently leave their homes by 2100. The planned relocation of climate-vulnerable residents is known as “managed retreat,” and it is most commonly pursued through post-disaster buyouts. After a natural disaster damages or destroys a home, local governments may choose to offer homeowners the pre-disaster, fair-market value of their house to move away, rather than rebuild. Over the last 40 years, municipalities have relocated nearly 50,000 American households in this manner at a cost of $3.5 billion, typically a few homes at a time.

At this rate of buyouts, it would take thousands of years to help all at-risk American homeowners and their households move to safety. Of course, the U.S. does not have that luxury, as the ocean is already encroaching upon entire towns. Either the government must step up to more efficiently relocate such communities en masse, or property owners will eventually be forced to abandon their homes, likely at a near-total financial loss.

The U.S. needs an ambitious plan to support millions of Americans to steadily relocate in the coming decades in a way that is financially feasible, community-led, and socioeconomically equitable. The federal government, local partners, and the private sector must collaborate to (1) limit further population inflows to climate-vulnerable areas; (2) incentivize at-risk residents to move to safer ground on their own accord; and (3) proactively plan and implement buyouts at scale.

Acknowledgments

We would like to thank our FLH teammates Sabiha Zainulbhai and Jacob Kepes for their thoughtful feedback on this report. We would also like to thank our New America colleagues Kelley Gardner, Joe Wilkes, Jodi Narde, and Naomi Morduch Toubman for their help with layout and design.

Editorial disclosure: The views expressed in this report are solely those of the authors and do not reflect the views of New America, its staff, fellows, funders, or its board of directors.

Downloads

Introduction

Scientists project that sea-level rise could force over 13 million Americans to permanently leave their homes by 2100. Add wildfires, extreme heat and drought, flooding, and hurricanes, and perhaps more than 20 million Americans will need to relocate over the coming decades due to climate impacts.1

The planned relocation of climate-vulnerable residents is known as “managed retreat,” and the U.S. government most commonly pursues this strategy through post-disaster buyouts. After a natural disaster damages or destroys a home, local governments may choose to offer homeowners the pre-disaster, fair-market value of their house to move away, rather than rebuild. The federal government usually provides three-quarters of the funding, while state and local authorities administer programs and fund the balance. Over the last 40 years, municipalities have relocated nearly 50,000 American households in this manner at a cost of $3.5 billion, typically a few homes at a time.

Key Terms Defined

- Managed Retreat: The strategic and planned relocation of houses, commercial property, and infrastructure, as well as people, to a new location to reduce natural hazard risk. Managed retreat seeks to be a more proactive alternative to the forced displacement that is expected to occur as a result of sea-level rise, increasingly severe flooding and erosion, and other climate impacts.

- Buyout(s): Real estate acquisitions in which owners voluntarily sell their properties in high-risk areas and (ideally) relocate to lower-risk areas. Buyouts are mostly implemented in post-disaster contexts in the U.S., with the “buyer” being local governments, who usually receive funding from federal agencies to compensate the homeowner. The tactic is often part of a larger managed retreat strategy.

At this rate of buyouts, it would take over 4,000 years to help an estimated 5 million at-risk households move to safety.2 Of course, the U.S. does not have the luxury to incrementally relocate residents over the course of thousands of years. The ocean is already encroaching upon entire towns, from North Carolina to Louisiana and Alaska. Either the federal government must step up to more efficiently relocate such communities en masse, or property owners will eventually be forced to abandon their homes, likely at a near-total financial loss.

While small-scale relocation of climate-vulnerable households over the course of millennia is nonsensical, especially as climate impacts to housing become worse, moving millions of households all at once is similarly impossible. But steadily supporting a few hundred thousand people to relocate per year until 2100 is less daunting, particularly considering that 40 million Americans already move each year.

We need an ambitious plan to support millions of Americans to steadily relocate in a way that is financially feasible, community-led, and socioeconomically equitable. The federal government, local partners, and the private sector must collaborate over the coming decades to (1) limit further population inflows to climate-vulnerable areas; (2) incentivize at-risk residents to move to safer ground on their own accord; and (3) proactively plan and implement buyouts at scale.

Citations

- In fact, Tulane University professor Jesse Keenan estimates that 50 million Americans could move by 2050 due to climate change.

- As noted above, more than 20 million Americans may need to relocate over the coming decades due to climate change. Accounting for 2.6 persons per U.S. household and a U.S. homeownership rate of 66 percent, we estimate that approximately 5 million American households may require a future buyout. At a historical rate of roughly 1,250 buyouts per year, all future buyouts would take over 4,000 years to complete.

Rising Seas, Sinking Homes

Corrected at 4:38 p.m. on August 8, 2024: This section has been changed to correct an inaccuracy in the mention of research that predicts coastal property owners will incur $350 billion in losses between 2060 and 2079, which then balloons to $880 billion over the following 20 years, not $350 billion in annual losses by 2070 ballooning to $880 billion per year by 2090 as previously written.

Climate change poses an unprecedented threat to U.S. communities. The increasing frequency and severity of storms and flooding—exacerbated by rising sea levels—threaten lives, homes, and infrastructure. Even with global mitigation efforts to prevent future warming, the Intergovernmental Panel on Climate Change (IPCC) warns that the rate of sea-level rise is accelerating and it projects that oceans worldwide will rise by an average of one foot by 2050. Looking further ahead, sea levels could increase by nearly three feet by 2100, which could fundamentally transform current coastal landscapes.

Sea-level rise will worsen coastal flooding at all levels by 2050, according to the latest projections from the National Oceanic and Atmospheric Administration. Moderate flooding, which often damages houses and infrastructure, will likely occur 10 times more often than it does today, while the average rate of high-tide flooding will double. Major coastal storms associated with severe flooding, such as Atlantic hurricanes and landfalling atmospheric rivers on the West Coast, are expected to increase and intensify in the coming decades. Continued population growth on the coasts, and with it increased development, will leave communities more vulnerable to flood-related risk. In the absence of climate adaptation strategies, the IPCC anticipates that coastal communities globally will experience double the amount of annual flood damages by 2100.

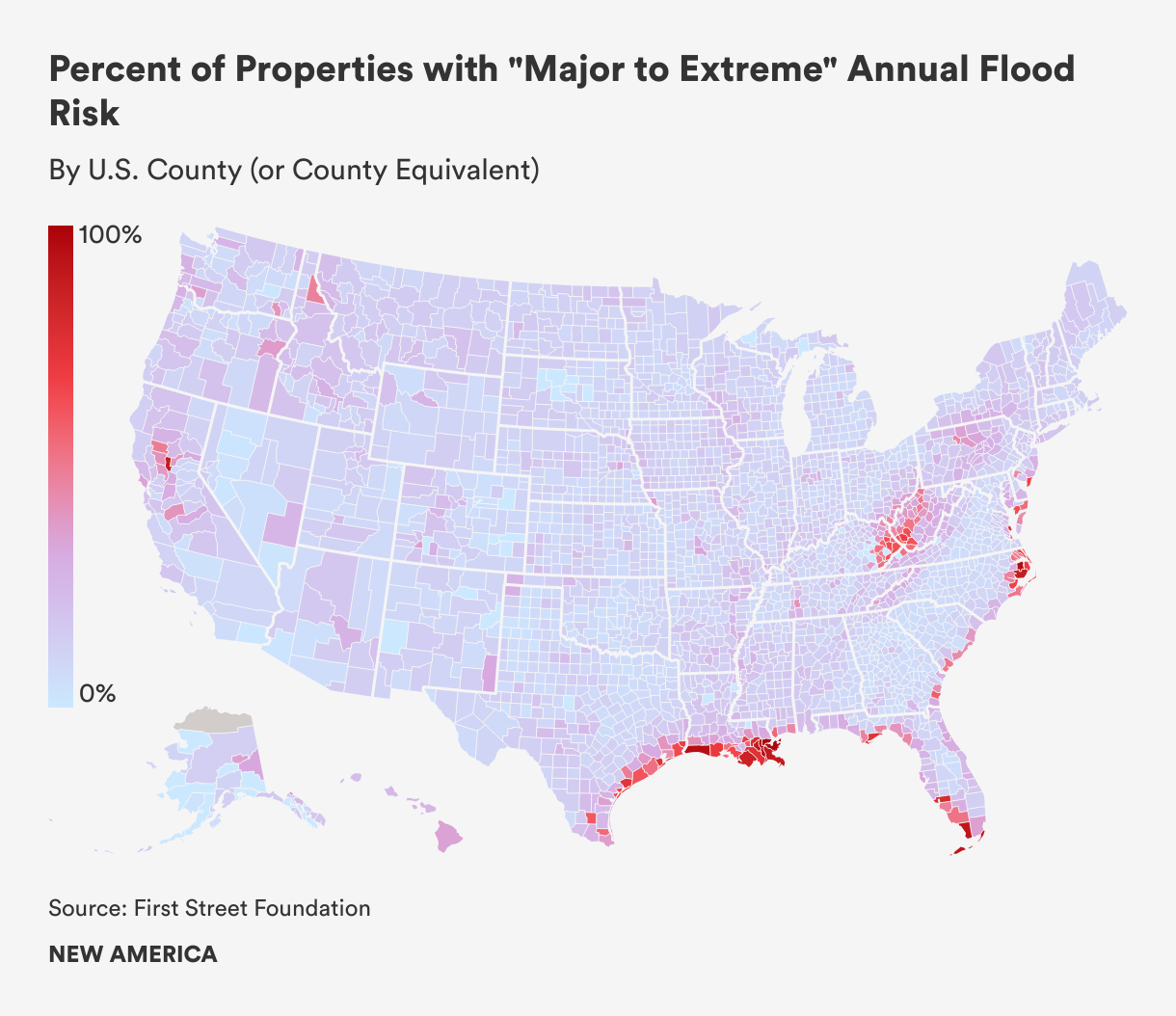

Accelerated climate impacts threaten tens of millions of homes in the U.S., notably in coastal communities. Approximately $1 trillion in real estate is at risk on the coasts and increased flooding is predicted to destroy billions of dollars of property by 2050, with the greatest impacts in the Atlantic and Gulf regions. Research from the Brooklyn-based nonprofit First Street Foundation found that flooding, the most common and costliest natural hazard, will threaten 23.5 million properties in the next 30 years. In particular, climate change will very likely compound the U.S. affordable housing crisis; peer-reviewed research projects that the number of affordable units threatened by coastal flooding will triple by 2050.

Increasingly severe climate impacts on U.S. housing security are expected to displace millions of people in the coming decades, likely causing a “ripple effect” of migration inland. The Internal Displacement Monitoring Centre found that 1.7 million Americans were displaced by natural disasters in 2020. This number is only expected to increase: Research from the University of Southern California projects that sea-level rise alone will displace 13 million people by 2100. Tulane University professor Jesse Keenan suggests that 50 million Americans could eventually move due to climate impacts more broadly. The scale of this expected displacement will reshape both coastal and inland communities socially, economically, and politically.

Climate Impacts on Vulnerable U.S. Populations

Socially and economically vulnerable populations, including minority and low-income communities, are disproportionately impacted by climate change and its associated risks to housing. These marginalized groups are more likely to live in areas exposed to climate risks, due to historic discriminatory policies such as redlining, urban renewal, and disinvestment. In large part, these policies have also led to insufficient, low-quality, or failing housing and infrastructure, all more vulnerable to climate-related damage. Renters are at even greater risk, as natural hazards threaten 40 percent of all U.S. rental housing, leaving lower-income populations with increasingly few housing options. Native Americans also face heightened risks due to near-total land dispossession historically, which has forced these communities into areas with greater climate vulnerability and fewer resources to address such threats.

Inaction within these projected scenarios would be tremendously expensive. With no climate adaptation, annual financial damage to U.S. coastal property is estimated to reach $5 trillion through 2100. Research from Industrial Economics and the University of Colorado predicts that if the government does nothing to move communities away from at-risk areas or otherwise adapt to climate change, coastal property owners will incur $350 billion in losses between 2060 and 2079, which then balloons to $880 billion over the following 20 years. In stark contrast, the study found that proactive adaptation would be 10 times less expensive.

Beyond the economic costs of inaction, there are potential social, political, and environmental consequences. Without proactive steps to reduce risk, climate change is expected to exacerbate existing social inequities as vulnerable populations, such as elderly Floridians or Native Alaskans, are least able to respond to severe hazards on their own. Poorly planned risk reduction strategies, often known as “maladaptation,” can result in financial losses, increased vulnerability, and greater distrust among residents towards government. And finally, ecosystems will suffer: During Hurricane Ian in Florida, for example, sewage pipes overflowed into waterways and gasoline leaked from submerged vehicles, polluting the coastal environment and posing threats to human health.

Managed Retreat Makes Sense, but the Current Approach Is Not Working

The current approach to managed retreat is most often implemented through post-disaster buyouts. Following a hurricane or severe flooding, for example, a local government will choose to offer homeowners the pre-disaster, fair-market value of their house to move elsewhere rather than rebuild their damaged or destroyed property. The federal government typically provides three-quarters of the funding for these buyouts—via the Federal Emergency Management Agency (FEMA) and the Department of Housing and Urban Development (HUD)—and state and local governments fund the balance and administer the programs. Over the last 40 years, municipalities have relocated nearly 50,000 American households at a cost of about $3.5 billion through buyouts, typically a few homes at a time.

Federal Flood Insurance Is Drowning

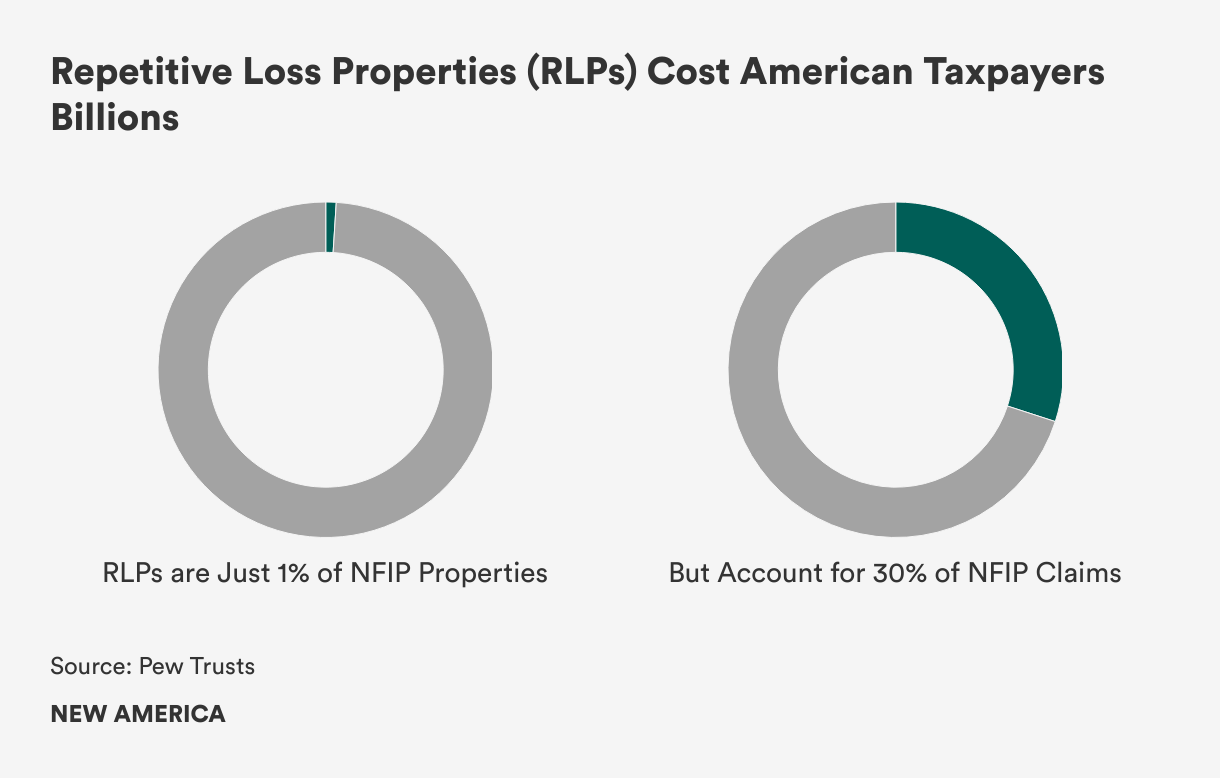

In addition to environmental benefits such as the restoration and conservation of coastal and river ecosystems,1 managed retreat makes significant economic sense. The repeated repair of damaged properties costs American taxpayers billions of dollars each year and places acute financial stress on FEMA’s National Flood Insurance Program (NFIP). Repetitive loss properties (RLPs), defined as properties that have flooded and received claims multiple times, only comprise 1 percent of NFIP properties, but have accounted for over 30 percent of all claim payments. Cumulatively, NFIP has paid more than $22 billion in insurance claims to RLPs, and the issue has only become worse: Between 2009 and 2018, the U.S. added more 64,000 RLPs as Americans continued to move into areas at risk of flooding.

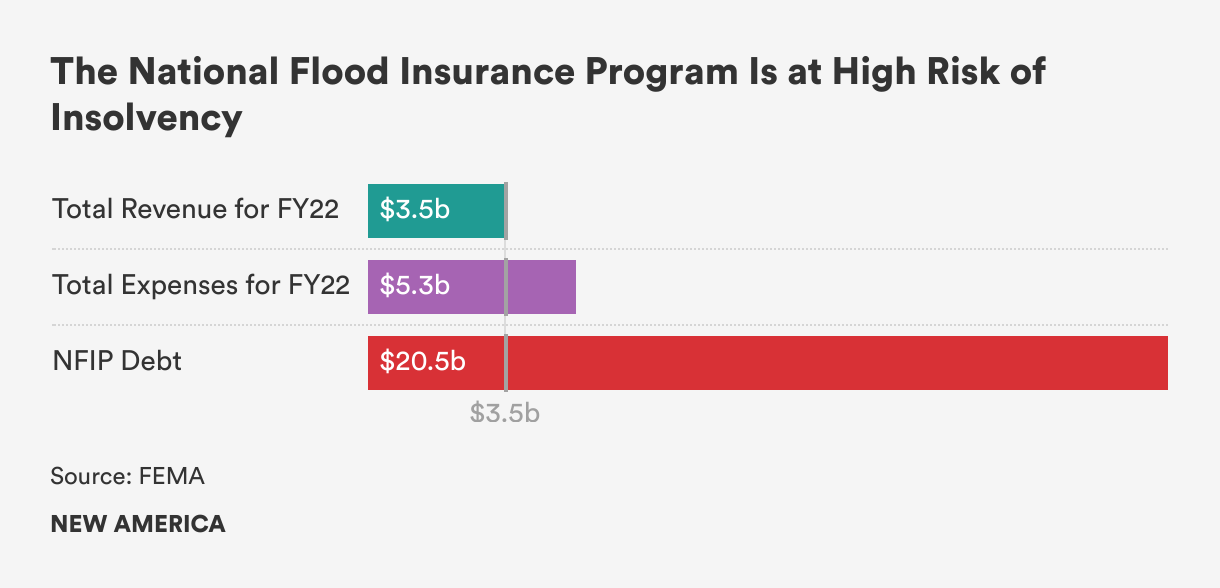

In fact, NFIP is currently at high risk of insolvency and its future is uncertain. The program is $20.5 billion in debt to the U.S. Treasury, and in fiscal year 2022 the program’s total expenses of $5.3 billion far exceeded its revenue of $3.5 billion.2 This financial situation is likely to become more severe as climate change leads to increased flooding and more frequent and stronger storms. Nationally, First Street Foundation projects that expected economic losses from flooding will rise by approximately $12 billion by 2051. It is uncertain whether Congress will continue to reauthorize an increasingly expensive flood insurance program or, alternatively, if legislators will cancel NFIP’s debt.

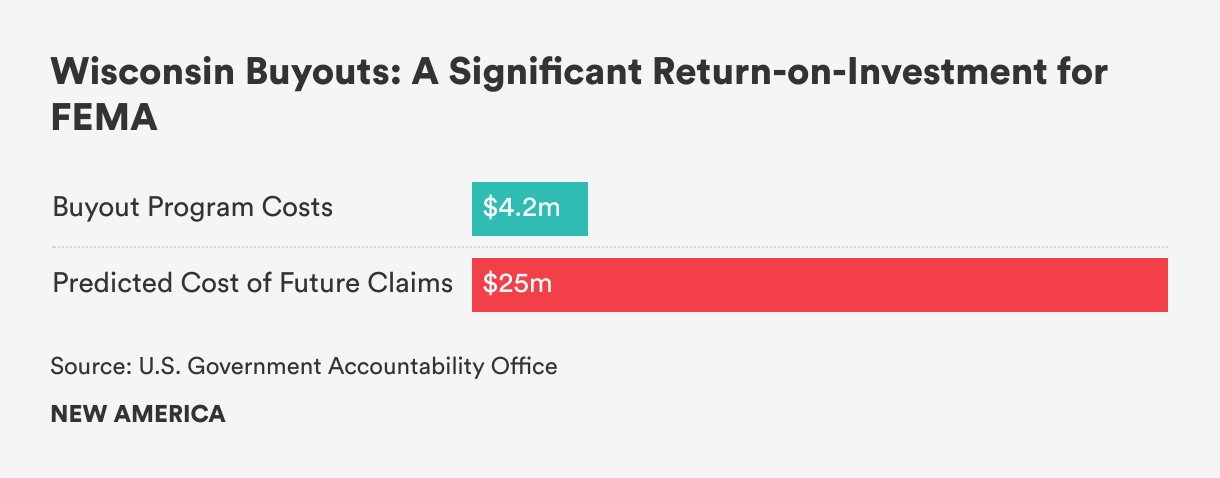

By contrast, buyouts offer a significant return-on-investment by ending the “repair loop” and lowering the costs of future disaster recovery by reducing the number of at-risk homes along the coast or in a floodplain. A 2022 study published by the U.S. Government Accountability Office, for instance, found that 89 buyouts in a Wisconsin floodplain cost FEMA $4.2 million, but helped the agency avoid $25 million in predicted future claims.

Buyouts can also lead to a number of positive social benefits if implemented through a community-centered and equitable approach. Studies show that living under the continuous threat of a natural disaster damages both mental and physical health. Relocating households out of vulnerable areas can prevent injuries and deaths associated with extreme weather events, improve health and wellbeing, and reduce or eliminate the stress and anxiety that comes in anticipation of the next disaster. In the long term, reducing climate risk improves community resilience and sustainability, which helps to ensure that future generations are more safe from climate impacts.

Building Back…Faster

Buyouts remain unpopular despite their environmental, economic, and social benefits, however. Local governments and their residents obstruct and delay these relocations for several reasons, even when it is clear that buyouts will be less expensive and less chaotic than later, post-disaster moves. For smaller municipalities, the loss of part of their tax base can pose a significant financial challenge, as the government is obliged to still provide costly public services to remaining residents. And for homeowners, the thought of moving away from their neighborhood or community can be gut-wrenching. There are ultimately few easy solutions to coax local governments to part with taxpayers or to encourage residents to leave their homes.

Procedural and structural factors related to post-disaster aid also incentivize rebuilding damaged homes. First, most buyout funding only becomes available after a federally declared natural disaster, and this money can take years to reach local coffers. Research from the Natural Resources Defense Council (NRDC) found that buyout negotiations usually take over five years to finalize. FEMA meanwhile provides flood insurance to all households in a floodplain through the NFIP, and insurance payouts arrive faster than buyout funds. As a result, many homeowners do not wait for a buyout offer and instead rebuild their houses, often multiple times, with NFIP funding. In fact, more than 30,000 severe repetitive loss properties—properties that have flooded an average of five times—are covered under NFIP. And sometimes, homeowners repair or rebuild their house multiple times before finally choosing to leave, resulting in billions of dollars in sunk costs for the U.S. government.

Second, buyouts are incredibly complicated to administer. Smaller and poorer municipalities often lack the technical expertise and staffing capacity to apply for competitive buyout programs and other grant opportunities, and then to navigate complex real estate transactions and land acquisitions if the funding is awarded. So wealthier and larger communities with better-staffed governments can more effectively plan for and fund their retreat, while marginalized or less-populated communities struggle to secure federal dollars and relocate residents, leaving many little choice but to rebuild.

Finally, previous buyout projects have consistently yielded unjust and inequitable outcomes, largely as a result of procedural and distributive justice challenges. Use of the pre-disaster, fair market value of a home to calculate the purchase offer, for example, overwhelmingly disadvantages those whose properties are low-value, undervalued, or in poorer condition—often low- to moderate-income homeowners and communities of color. Their purchase offers are significantly lower than what is necessary to acquire a house in a less flood-prone area, leaving them more susceptible to risk and displacement.

The implementation of buyouts also reveals and exacerbates stark racial disparities in the United States. An NPR analysis found that 85 percent of FEMA’s property acquisition funds have been allocated to predominantly white communities. And a comprehensive 30-year study by Rice University researchers shows that, while buyouts effectively reduce household flood risk, they often contribute to increased racial segregation residentially. These equity and justice challenges underscore an urgent need for more proactive planning and critical analysis around how buyout programs are implemented.

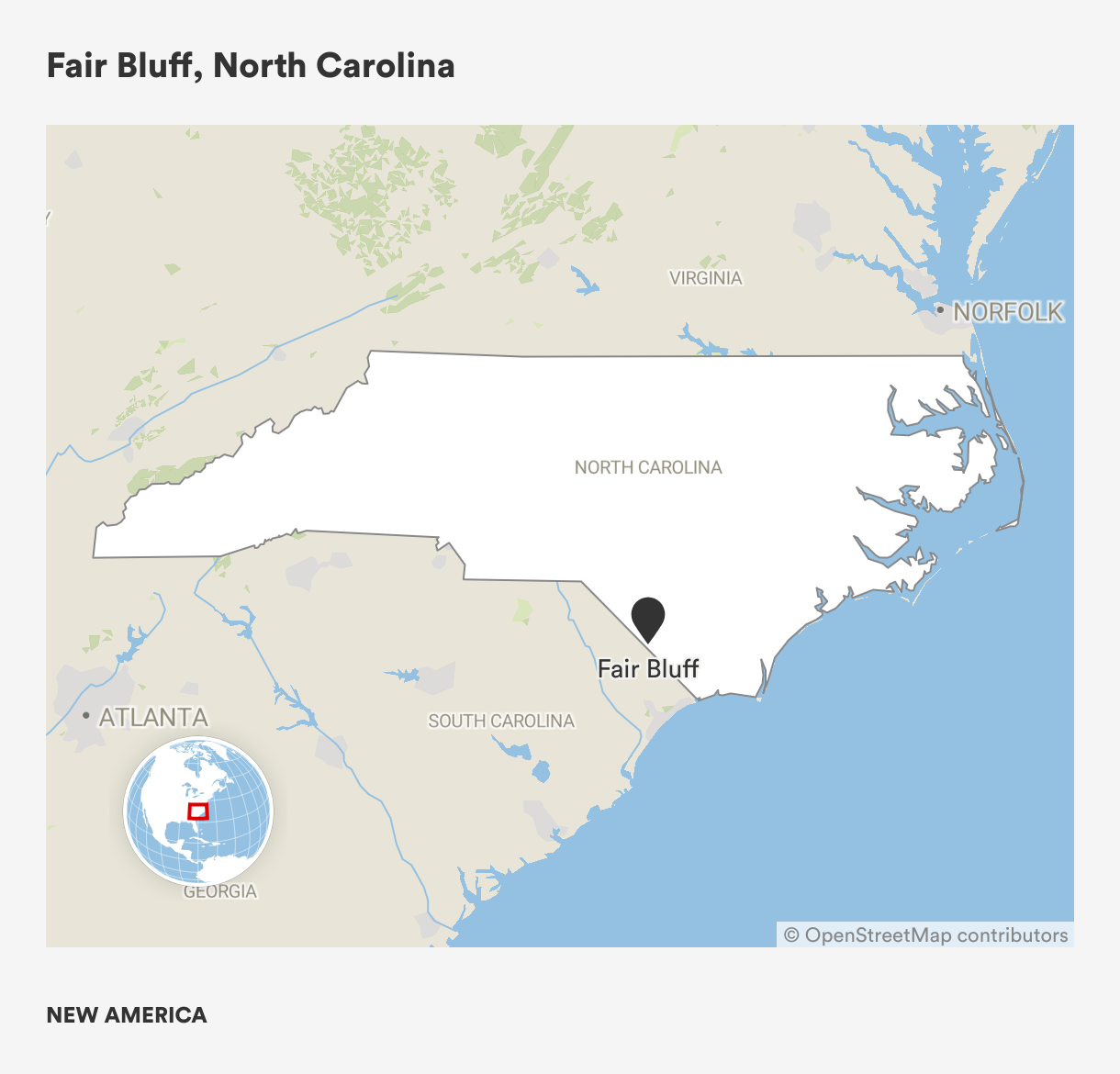

Case Study: Fair Bluff, North Carolina

Fair Bluff, a town on North Carolina’s southeast coastal plain with fewer than 1,000 residents, experienced significant damage from Hurricane Matthew in 2016 and was heavily impacted by Hurricane Florence two years later. Matthew caused widespread flooding, affecting nearly a quarter of all homes and submerging Main Street under four feet of water. Critical infrastructure was also destroyed, and nearly half the town’s population has moved away.

These severe and repeated impacts have placed tremendous strain on Fair Bluff’s financial resources and have contributed to steady population decline. This small community’s future is at risk as a result. Yet the town’s situation is not unique. Rather, it exemplifies the uncertainty faced by many small and rural communities that are grappling with worsening climate impacts.

As a small municipality with a limited tax base, Fair Bluff lacks the necessary funding and staff capacity to independently plan and implement large-scale recovery projects and must therefore rely on outside assistance. After Hurricane Matthew, for example, the State of North Carolina decided to fund three new city staff positions, and support from local universities and county government was critical in applying for and receiving federal recovery assistance.

But even as some federal agencies granted money after Hurricane Matthew to redevelop downtown, FEMA purchased 34 badly damaged properties, causing the population (and tax base) to decline further. Although buyouts are an effective strategy to reduce risk, this policy also disrupted the community’s social and economic structures, as residents typically relocated outside of Fair Bluff to neighboring towns with lower flood risks. These moves drained financial resources and created more challenges to recovery and redevelopment after the storms. Fair Bluff is struggling to both recover economically and build resilience for future disasters as a result.

Some residents have left Fair Bluffs permanently, while others remain and are committed to building a safe and vibrant community. In March 2023, FEMA approved the second phase of a project to buy out and demolish 51 commercial properties in the downtown area, which was hardest hit by Matthew, and to remediate the area into its natural condition as part of the floodplain. The goal is to utilize the area as greenspace and redevelop downtown on higher ground. However, the long-term future is still uncertain, as FEMA’s process is slow-moving and it can take multiple years to complete projects, leaving homeowners and the town in a discouraging limbo. If another storm hits, residents will face a difficult choice: attempt to rebuild yet again or leave for good.

Citations

- Dunes, wetlands, and other natural barriers further help protect communities from future storms and flooding.

- Insurance payouts account for the majority of NFIP’s expenses. Costs are also related to floodplain mapping and flood-related grants.

Our Recommendations for a Better Managed Retreat

To start, it is critical to recognize that the U.S. will not need to buy out all at-risk Americans simultaneously. Nor will all households relocate to the same receiving community. The federal government, its local partners, and the private sector should instead work steadily over the coming decades on a three-pronged approach that (1) stems population inflows to climate-vulnerable areas; (2) encourages at-risk residents to independently move to safer ground; and (3) proactively plans and implements buyouts for anyone remaining. Importantly, federal policymakers and local planners must also work to increase equity within these larger strategies.

So, how can the United States implement gradual and proactive managed retreat strategies?

This long-term planning first requires significant staffing capacity, yet research shows that most U.S. jurisdictions, particularly smaller and poorer ones, lack such resources. To that end, the federal government must adequately fund small municipalities, so in turn they can better staff planning departments, housing agencies, and other units tasked with resilience.

Recommendation #1: More federal funding for small municipalities to staff planning departments, housing agencies, and other local entities tasked with climate resilience.

Reduce Population Inflows to Climate-Vulnerable Areas

Both the federal government and municipalities should discourage, and in some cases outright restrict, people from moving into our most climate-vulnerable areas. Research from the real estate firm Redfin finds that the most at-risk parts of the U.S. are also among the fastest growing. Florida, the state at greatest risk from sea-level rise and hurricanes, was also the fastest-growing state by population percentage increase between 2021 and 2022. In large part, lower costs of living, economic growth, and warmer weather are driving population increases in climate-vulnerable areas across the Sun Belt (and any strategies to reduce these inflows must consider such factors).

Many stakeholders continue to benefit from these population increases and associated economic growth. Real estate developers profit from lucrative coastal developments, while local governments enjoy increased tax revenues. The result in many communities is a fast-growing “climate real estate bubble”: 2023 analysis by First Street Foundation and the Environmental Defense Fund suggests that U.S. properties exposed to flood risk are overvalued by between $121 billion and $237 billion. Once this bubble bursts, owners of flood-prone homes will experience a massive loss of equity and, eventually, an unsellable house. The ripple effects will threaten property values across the entire United States.

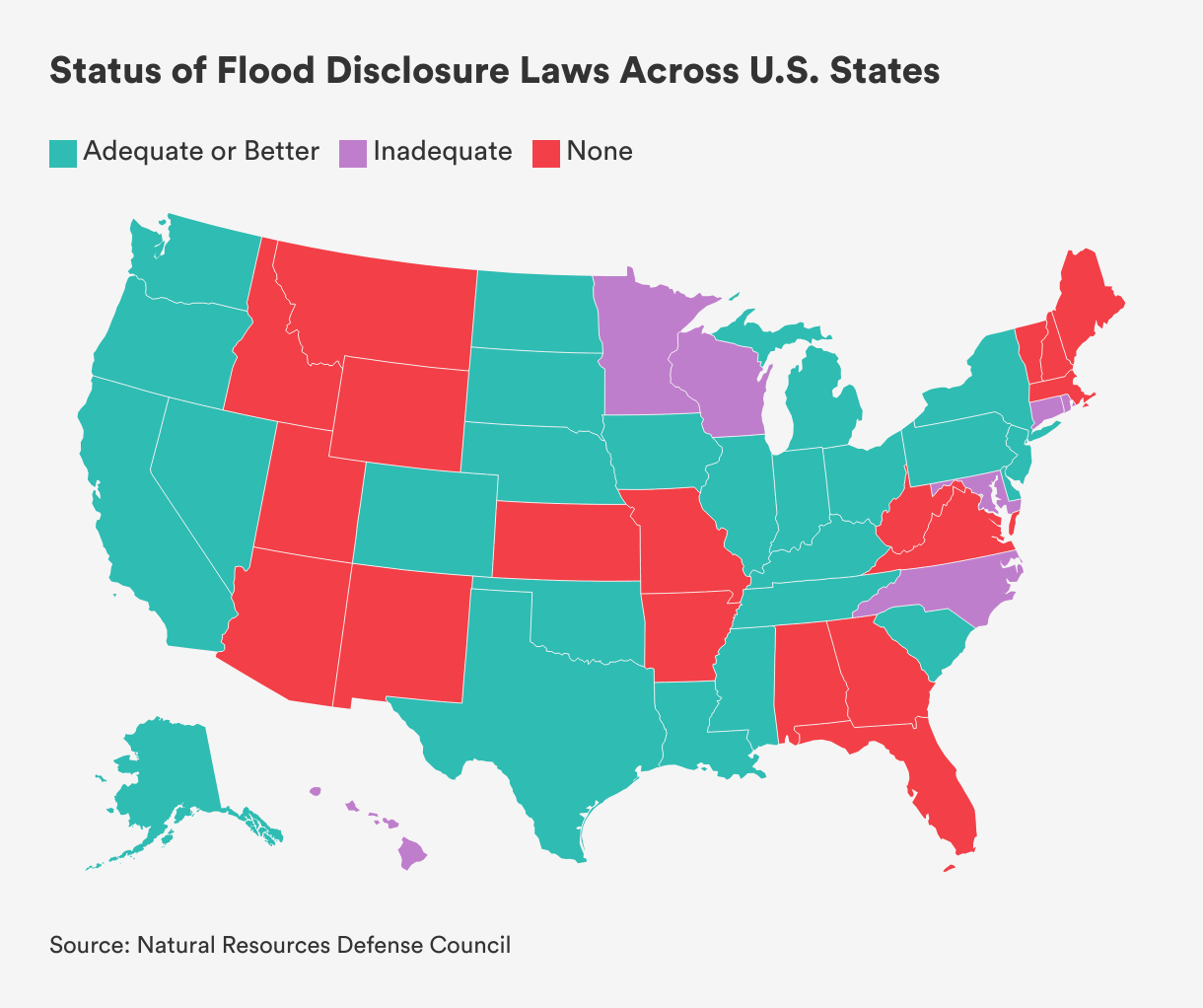

One strategy to slow these population flows is to increase the transparency surrounding climate risk to real estate. Roughly one-third of U.S. states lack disclosure laws that require sellers to inform buyers that a house is at risk of flooding or has previously flooded. Meanwhile, outdated and incomplete FEMA flood risk maps do not reflect actual risk.1 Many homeowners consequently may not understand the climate risks to their new properties.

In 2023, flood-prone New Jersey and several other states passed legislation that requires flood disclosure during real estate transactions.2 Additional states should follow suit, or the federal government should establish nationwide flood disclosure requirements, to ensure that buyers are aware of the true risks of moving into dangerous areas.

Recommendation #2: U.S. states without flood disclosure laws should pass legislation, or the federal government should enact nationwide flood disclosure requirements.

But some homeowners may tolerate (or ignore) these risks, even when they are adequately aware of them. In part, this is because FEMA offers heavily subsidized insurance to all residents in high-risk flood zones through the NFIP. Despite recent efforts to align rates with true flood risk, this insurance remains significantly discounted. The availability of NFIP creates a moral hazard, and the federal government should either stop offering the program to new construction in high-risk flood zones or further increase new policies’ rates to accurately reflect risk.

Recommendation #3: Congress must reform the National Flood Insurance Program, either by declining to offer subsidized insurance to new construction in high-risk flood zones or by further increasing rates for new policies to more correctly reflect flood risk.

Another option to slow population growth in climate-vulnerable locations is to limit or restrict new development in high-risk areas. Local governments are well-positioned to promote “climate-resilient development” through their land use management and zoning authority. Historically, racist and classist zoning policies have reinforced inequitable investment patterns and have resulted in marginalized populations’ disproportionate exposure to environmental hazards. But today, holistic, forward-looking, and innovative zoning reforms can address historic inequities, promote sustainable land use, and build community resilience to climate risks.

For example, Norfolk, Virginia, overhauled its zoning code in 2018 to include overlay zones that encourage new development at higher elevation and also place more stringent measures on development in flood-vulnerable areas. These types of policies support growth in areas of greater climate resilience, therefore directing new residents to safer ground.

Recommendation #4: Local governments should limit or restrict new development in climate-vulnerable areas through changes to land use and zoning policies.

Disincentivize Staying in At-Risk Areas, Incentivize Moving to Safer Ground

A second goal is to gradually reduce the amount of people actively residing in vulnerable areas, ultimately to lower the number of residents who will require buyouts and other post-disaster assistance in the long term. The federal government should coordinate with state and local authorities to encourage homeowners to relocate to safer areas, whether by disincentivizing their decision to stay or by making relocation more attractive.

Nationally, Congress should limit the number of times that FEMA can fund the rebuilding of homes repeatedly damaged or destroyed by climate-related disasters. Funding should instead be repurposed for buyouts and other proactive relocation measures. In fact, FEMA itself recommended removing from NFIP coverage any properties repaired four or more times. The proposal is pending Congressional approval as of fall 2023.

Homeowners are often eager to break the cycle of flooding and rebuilding, but are unable to sell their house to a new buyer. To address this challenge, qualifying and interested homeowners should be offered a “guaranteed future buyout.” First proposed by NRDC, a guaranteed future buyout option would involve a homeowner voluntarily committing to accept a buyout of their house if and when it is substantially damaged in a future disaster. The offer could be included as a benefit of NFIP coverage to ensure uptake. In the end, this type of proactive planning should substantially reduce the time to complete buyout processes and provide a sense of certainty and security for homeowners.

Recommendation #5: Congress should reform FEMA’s National Flood Insurance Program to (1) limit the number of payouts for repetitive loss properties and (2) repurpose funding to offer “guaranteed future buyouts” as part of flood insurance coverage to qualifying homeowners.

Local governments can further utilize their land use and zoning powers to implement policies that gradually vacate vulnerable areas. These innovative approaches allow municipalities and their residents to plan for relocation as climate impacts become worse, without forcing immediate moves.

Life estates, which the city of Norfolk is experimenting with, are a land use type that allows residents to live in their flood-vulnerable homes for the remainder of their life, but mandates that the house reverts to government ownership thereafter. Another strategy to incentivize development on higher ground is the use of rolling easements, which gradually move the property line away from the shoreline as sea-level rise and erosion encroach upon the land. Rolling easements allow homeowners to stay on their property in the short term, while planning for eventual retreat.

Other land use and zoning tools are available for local governments to encourage homeowners in climate-vulnerable areas to proactively move to safer ground. For instance, municipalities can use public-private land swap arrangements to advance long-term resilience goals by “swapping” private flood-prone land for property in less-vulnerable areas. The low-lying land can then be converted into wetlands or other green space, providing flood mitigation and other environmental benefits. A related, emerging zoning technique called transferred development rights (TDRs) allows a property owner to cede their development rights within one flood-prone tract and transfer these rights to another, less-risky tract. TDRs can reduce climate risk through market incentives and help shift development away from hazardous areas. And a third tool is the leaseback, in which a local government acquires a climate-vulnerable property and then leases it to the original owner, providing a flexible approach for the eventual relocation of residents. Leases could expire after a standard time period or agreements could require the lessee to vacate if a “triggering event” such as substantial flood damage occurs.

Recommendation #6: Local governments should utilize their land use and zoning powers to implement a number of innovative strategies that gradually vacate climate-vulnerable areas.

As homeowners move, intermunicipal cooperation agreements could ease a local government’s concerns around a diminishing tax base and allow neighboring communities to offer relocation options for vulnerable residents. Smaller towns often hesitate to implement buyouts for fear that dwindling tax revenue will cripple the public service delivery for those who remain. States could address this worry by widening municipal boundaries in at-risk regions or creating cost-share arrangements between outflow and inflow municipalities.

Finally, inland cities such as Buffalo, New York, and Duluth, Minnesota, have begun positioning themselves as “climate havens,“ anticipating that an inflow of residents will boost their economies and reverse post-industrial population declines. While migration to climate havens is still nascent, cities in the Northwest and Northeast could experience a 10 percent growth in population over the coming decades due to climate factors, according to one projection. This future migration will very likely constrain housing supply, raise rents and mortgages, and exacerbate housing insecurity. To mitigate these risks while encouraging climate migration, the federal government might create “climate opportunity zones,“ in which it subsidizes affordable housing and provides tax incentives for new arrivals. Regardless of any federal help, city officials must direct the necessary resources to ensure housing supply meets demand in the future.

Proactively Plan Buyouts

Third, the U.S. government and its local partners need a more proactive buyout strategy for residents who do not relocate on their own. Perhaps most importantly, Congress must decouple buyout funding from disaster declarations to allow for this approach. Most federal buyout dollars only become available after a federal disaster declaration, despite the fact that preemptive relocation is both less costly and less traumatic compared to assistance following a hurricane, flood, or wildfire.

Recommendation #7: Congress must separate the availability of federal buyout funding from federal disaster declarations to allow for more proactive relocation.

In 2022, the Bureau of Indian Affairs (within the Department of the Interior) began to experiment with proactive buyouts by granting $25 million each to two Native Alaskan communities and one Native community in Washington state to relocate to safer ground. The three villages—Newtok and Napakiak in Alaska and Taholah in Washington—are experiencing severe erosion and storm surges that threaten to destroy much of their housing and infrastructure in coming decades. Previously, these small communities were not eligible for buyouts unless impacted by a federally declared disaster, despite existential risks from rising waters. Although these initiatives are new, they offer promise for a reformed strategy.

FEMA and HUD should also fund and provide technical assistance for communities to proactively plan for eventual buyouts. Notably, this will help to address equity issues, as the most climate-vulnerable municipalities are often low-resource and struggle to presently apply for buyout funding. The process could involve locating the most at-risk homes ahead of time, engaging and educating current homeowners about their options, and completing buyout paperwork before a disaster hits. NRDC proposes that Congress authorize FEMA to finance this strategy using NFIP funds. Between 2000 and 2017, NFIP spent $46.6 billion to repair and rebuild policyholders’ homes, with repairs often costing more than the total value of the house. This federal funding could instead be used for proactive planning.

Recommendations #8 and #9: The federal government should fund and provide technical assistance for local partners to plan for future buyout scenarios. The federal government should also provide more funding to complete these proactive buyouts.

In fact, some municipalities are already planning future buyouts as part of their climate resilience and economic development strategies, with funding through local taxes and fees. Houston, Texas, the nation’s fourth largest city, encourages its residents to volunteer for buyouts before a disaster occurs. Meanwhile, the Charlotte, North Carolina, metro area funds a preemptive buyout program with fees from its stormwater utility.

Case Study: Napakiak, Alaska

Napakiak is a small, remote Native Alaskan community of 344 residents located in the Yukon-Kuskokwim Delta. The village’s existence is endangered by increasingly rapid and severe riverine erosion, as the community lives along the banks of the Kuskokwim River, the longest free-flowing river in the United States.

Napakiak’s proximity to the river has supported a subsistence lifestyle for thousands of years. But erosion at rates of 25 to 50 feet per year now threatens to destroy nearly all homes and critical infrastructure—including the village’s school and airstrip—by 2030. In response, the community developed Alaska’s first long-term Managed Retreat Plan to relocate to safer ground adjacent to the current site.

Despite Napakiak’s efforts to proactively plan a managed retreat, the community consistently struggled to access project assistance due to systemic barriers within federal programs that disadvantage marginalized groups. For example, the cost-share requirements of most programs, which is the need to match federal funding with local funding, makes it incredibly difficult for small and poor communities like Napakiak to submit an application. Additionally, buyouts were largely inaccessible to Napakiak because the U.S. Stafford Act does not recognize slow-onset disasters like erosion, making the community ineligible for FEMA disaster-based assistance. Lacking this funding, Napakiak was left vulnerable to future storms and erosion, with homes at risk of being swallowed by the river before help arrived.

In 2022, however, the Bureau of Indian Affairs (BIA) awarded Napakiak $25 million for community-led managed retreat. This funding is a first-of-its-kind federal investment to proactively implement managed retreat projects before a slow-moving disaster devastates a community.

While BIA funding is not sufficient to relocate every threatened house or all infrastructure, it will significantly expedite the retreat process.3 Napakiak’s top priority is to relocate imminently threatened structures, including 38 homes, to a new subdivision further inland. BIA funding will substantially advance development of the subdivision and relocation of threatened buildings, which could very well attract additional support from other funders.

Ultimately, this assistance will help to protect tribal sovereignty by ensuring the long-term sustainability of the community in the location they have called home for centuries.

Increase Equity in the Planning and Implementation of Buyout Projects

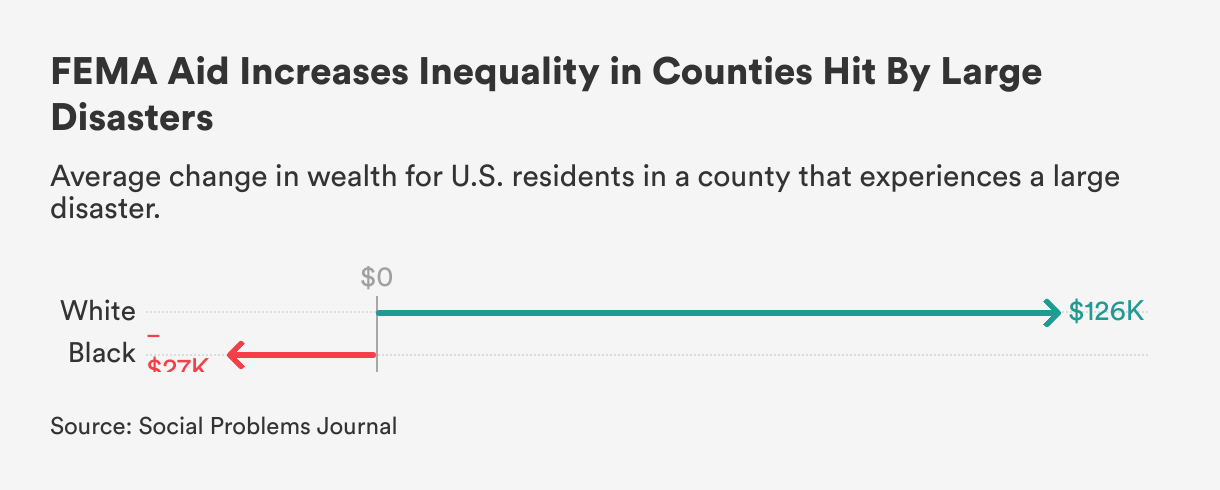

Most managed retreat projects in the U.S. do not meaningfully incorporate equity into their design and implementation. Consequently, programming can lead to inequitable and unjust outcomes, particularly for marginalized individuals and groups. In general, research shows that the more disaster-related aid an area receives from FEMA, the more inequality increases along lines of race.

As managed retreat becomes increasingly necessary amid climate change, it is essential that federal policymakers, local planners, civil society organizations, and the private sector work to deliberately incorporate equity within programs. While strategies will differ based on an area’s geographic, economic, and social characteristics, there are common practices that will help to increase equity.

To start, it is worth reiterating that small and low-resource communities continue to struggle to apply for and receive financial and technical assistance from the federal government. Research published in the peer-reviewed journal Science Advances found that counties with larger populations and higher incomes are more likely to implement buyouts.4 Analysis by Rice University similarly concluded that buyouts disproportionately benefit whiter, weather communities. Tiny, short-staffed municipalities need more assistance and resources from the federal government to grow and sustain their capacity to administer buyout programs.5

Development of managed retreat projects at the local level should prioritize the needs of socially vulnerable groups and address their unique challenges. To accomplish this goal, planners must meaningfully include affected communities in the design, planning, and implementation of buyouts. This better ensures that socially vulnerable groups’ perspectives and knowledge are valued and incorporated, leading to more equitable and effective outcomes.6 Good practices from the U.S. Environmental Protection Agency include the provision of culturally appropriate and accessible information, the facilitation of community consultations, and opportunities for residents to voice their concerns, preferences, and aspirations.

Recommendation #10: The development of managed retreat projects should center the needs of socially-vulnerable people and address their unique challenges, and also consider the long-term impacts of relocation for these groups.

An equitable managed retreat framework must also consider the long-term socioeconomic impacts of relocation and work to mitigate the disruptions experienced during the process. Strategies include assistance to both secure employment and access affordable, low-risk housing in the areas people move to after buyouts. Critically, buyout programming should start to include ongoing monitoring of equity outcomes to guide future investments.

Citations

- Of note, the 2021 Infrastructure Investment and Jobs Act allocated $600 million to FEMA to update its flood maps.

- The New Jersey statute also requires landlords to notify prospective tenants if a property is within a flood zone or has previously flooded. Only eight states have similar requirements.

- The program also aims to provide a model for other communities who may need to complete a managed retreat in the future.

- It is worth noting, however, that buyouts in such counties are in fact concentrated in areas of greater social vulnerability.

- See Recommendation #1 above.

- Of note, there were a number of successful community-led managed retreat projects prior to the mid 1990s. Since then, community-led projects are more difficult to implement as a result of a lack in funding and the challenges of interagency coordination within the U.S. government.

Conclusion

A climate housing crisis is likely unavoidable. It may first manifest as a financial meltdown, in which the insurance and mortgage industries overhaul homeowners coverage and loans, respectively, causing certain property values to plummet. Homeowners will see their equity disappear and then many could default on their mortgages and be left with insufficient funds to relocate to safer ground.

In the decades after, as the ocean swallows entire communities, the U.S. will have little choice but to relocate residents en masse. The federal government might manage this hasty retreat through eminent domain takings—the U.S. Army Corps of Engineers is currently authorized to conduct compulsory buyouts—or through mass emergency buyouts post-disaster.

These last-minute adaptation efforts would be incredibly expensive, chaotic, and traumatic. The fewer Americans that the government must relocate in this manner, however, the less costly and less hectic the process. In fact, if decision-makers are purposeful and imaginative in how they plan retreat, the strategy can socially and economically stimulate previously stagnant cities and help rectify past social and economic injustices for historically marginalized communities.

The challenge, of course, is to overcome the inertia of current approaches. The science and economics are clear. Now we just need to act.

More About the Authors

Katie Lund

Intern, Future of Land and Housing

Tim Robustelli

Senior Policy Analyst, Future of Land and Housing

Yuliya Panfil

Senior Fellow and Director, Future of Land and Housing

Issues

Programs/Projects/Initiatives

Related

Climate Change, Housing, and Homeowners Insurance in Florida: Lessons for California