Table of Contents

- Foreword

- The Development of Smart Water Markets Using Blockchain Technology (Aditya K. Kaushik)

- Civilian Drones: Privacy Challenges and Potential Resolution (Ananth Padmanabhan)

- The Privacy Negotiators: The Need for U.S. Tech Companies to Mediate Agreements on Government Access to Data in India (Madhulika Srikumar)

- Governing Data: Non-Discrimination and Non-Domination in Decision-Making (Joshua Simons)

- Open Transit Data in India (Richard Abisla)

- Blockchain Regulation in the United States: Evaluating the overall approach to virtual asset regulation (Tanvi Ratna)

- Improving India’s Parliamentary Voting and Recordkeeping (Pranesh Prakash)

- India and the United States: The Time Has Come to Collaborate on Commercial Drones (Sylvia Mishra)

- Civic Futures 2.0: The Gamification of Civic Engagement in Cities (Subhodeep Jash)

- Key Differences Between the U.S. Social Security System and India’s Aadhaar System (Kaliya Young)

Blockchain Regulation in the United States: Evaluating the overall approach to virtual asset regulation (Tanvi Ratna)

Tanvi Ratna is a policy analyst and engineer, managing blockchain projects with a leading global consulting firm, based in India. She helped design the blockchain policy framework of the Government of Karnataka, home to India's Silicon Valley, and helps advise the central government in India on blockchain regulation. Her research focuses on designing effective regulatory frameworks for blockchain.

Introduction

Blockchain technology and cryptocurrencies have received more hype and regulatory attention than perhaps any other emerging technology in recent times. There are both private blockchains, where access to the network is permissioned, and public blockchains, where access is open. Public blockchains are powered by virtual currencies or cryptocurrencies. They are different from Distributed Ledger Technology (DLT), in that they have a consensus layer powered by cryptography, and the whole system sustains itself with an incentive structure, which is the cryptocurrency. Blockchain, for the purposes of this paper, primarily refers to public blockchains unless otherwise specified, as the bulk of the regulatory and policy focus has been around public blockchains.

Blockchain offers a highly compelling case of futuristic regulation and the ability of governments to cope with rapid technological developments for the following reasons:

- Technology with in-built economic model: Public blockchains are different from other technological innovations so far, in the sense that they are more than just a technology, but also more than just a currency or financial instrument. Blockchains are networks with an unorthodox peer-to-peer economic model. This makes it difficult to define a policy precedent or approach.

- Multi-faceted and global instrument: Cryptocurrencies can behave as a currency or equity, they are global by nature, and cut across the fields of technology, finance, and business. Traditionally, all these aspects of economic behavior are regulated in silos.

- Paradigm shift for society and business models: Because of their networked and peer-to-peer nature, blockchains can reorganize existing silos in systems and processes, and have far reaching effects on existing social, business and governance structures.

Blockchain is an interesting test of how governments cope with emerging paradigms, as it is a challenge to traditional mindsets and systems across the board. As phrased in a recent report by Don Tapscott, the challenge is to create a regulatory environment that “simultaneously protects investors and consumers, sustains innovation, grows the economy, and cultivates a new kind of society.”1

This study is a brief survey of regulatory actions and capacity building efforts undertaken by different agencies of the U.S. federal government towards cryptocurrencies and blockchain technology, and some perspectives from the ecosystem and state government levels. The aim of this study is to assess the overall government strategy being adopted towards this technology in the United States.

The Overall Approach to Blockchain Regulation in the United States

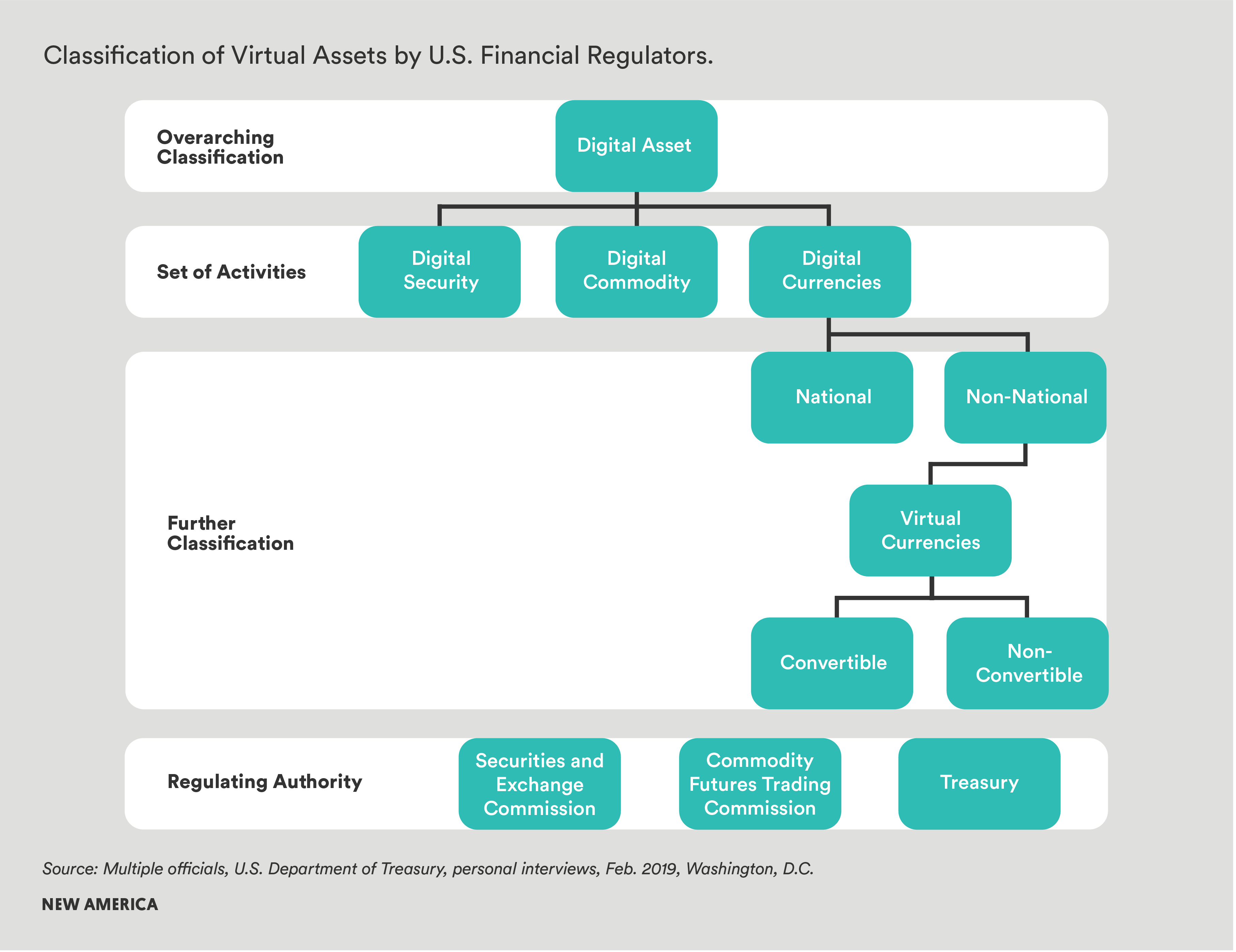

The definition of cryptocurrencies is still an evolving debate in the United States, with many calls for over-arching definitions and clarifications. Even at the time of publication of this paper, a taxonomy act had been introduced in the U.S. Congress to address this precise issue.2 The government, at least at the level of federal financial regulators, applies the following system of classification towards cryptocurrencies, or their preferred moniker the “digital asset.”

Figure 1: Classification of Virtual Assets by U.S. Financial Regulators

Source: Multiple officials, U.S. Department of Treasury, personal interviews, Feb. 2019, Washington, D.C.

There are many other agencies involved, outside of the three major regulators, even at the federal level. These include the U.S. Congress, which has a Blockchain Caucus; criminal enforcement agencies such as the FBI, Department of Justice, and Homeland Security; and a host of inter-departmental task forces.

For the purpose of this study, we explore in some detail the actions of the three major regulators who are the main drivers of activity, as well as some perspectives from the ecosystem and state government levels.

Activity by Major Federal Regulators

Securities and Exchange Commission (SEC)

The SEC has been one of the two most active agencies on cryptocurrency regulation in the United States; the other being the Commodity Futures Trading Commission (CFTC), which will be discussed later. The SEC is not one of the first agencies to begin regulating but it became more active with the growth of Initial Coin Offerings (ICOs) and security issue related activity in the blockchain ecosystem around 2016. The SEC views (some) virtual assets as securities, and recently issued guidance to that effect.

Regulatory Action: From 2014 to 2017, the SEC was cautious of cryptocurrencies. From 2013 to 2014, the agency issued investor alerts on Ponzi schemes and fraudulent activities in virtual currencies.3 The focus was on investor education and fraud prevention.

The DAO hack of 2016 4 was a major turning point in shifting the attention of the SEC towards the classification of cryptocurrencies into securities and non-securities. In 2017, the SEC issued an in-depth investigative report definitively classifying the DAO as a security.5 This spurred intense deliberation globally on security vs. utility tokens, and different countries such as Switzerland, Singapore, South Korea issued classification frameworks.

ICOs proliferated in 2017-2018 and the cryptocurrency market reached some of its highest valuations by the end of 2017. In the wake of concerns about scams and an unregulated ICO market, the SEC undertook heavy enforcement action in Feb 2018. Over 80 firms that had undertaken ICO offerings were subpoenaed.6

In 2018-20119 the explorations of asset classes deepened with the submission of proposals to launch a Bitcoin exchange traded fund (ETF) to boost institutional investment. The SEC rejected nine of these proposals. Some major decisions on new submissions are expected in 2019.7

On April 3, 2019 the SEC released its most definitive guidance to date, providing a framework for identifying whether a token was an investment contract or not.8 The SEC has now set a precedent of issuing “no-action letters” to startups after studying their business models. The no action letter lays out conditions to be met and serves as an assurance of no action by the SEC against the startup, for the actions it has disclosed in its application. The SEC issued its first “no-action letter” after 11 months of deliberation and discussion with the Florida-based startup, TurnKey Jet, Inc. after examining it through the Howey Test, 9 and deciding that their token offering was not a security, but closer to crypto-based store credit.

Capacity Development: The first in-depth activity by the SEC on blockchain was the DAO investigation in 2016, and they have been steadily increasing their capacity on the subject ever since. In January 2018, Hester Peirce, a leading champion of blockchain technology, was appointed as one of the five Commissioners of the SEC.10 The agency already had active working groups looking at the technology, such as the distributed ledger working group.

In June 2018, a new senior advisory position was created at the SEC to coordinate efforts across all SEC divisions and offices regarding the application of U.S. securities laws to emerging digital asset technologies and innovations, including initial coin offerings and cryptocurrencies. Valerie Szczepanik was appointed to this role.11

Similar to the model of LabCFTC,12 in October 2018 the SEC set up a dedicated team, called the Strategic Hub for Innovation and Financial Technology (Fintech Finhub), with a sizeable staff to serve as the focal point for tracking and interacting with fintech issues and innovators.13 The Finhub is also in the process of hiring a crypto securities lawyer at the time of this writing.14

Commodity Futures Trading Commission (CFTC)

The CFTC has been one of the two most active federal agencies in the regulation of cryptocurrencies. It is also widely considered to be the most supportive of the innovation.

Virtual currencies have been determined to be commodities by the CFTC under the Commodity Exchange Act. While its regulatory oversight authority over commodity cash markets is limited, it maintains general anti-fraud and manipulation enforcement authority over virtual currency cash markets as a commodity in interstate commerce.15

Regulatory Action: The CFTC adopts and advocates for a “light touch” approach towards cryptocurrencies. It refrained from issuing any directives or taking any enforcement action until late 2018.

During peaking bitcoin prices, ICOs, and an SEC crackdown, the CFTC also undertook enforcement actions from early 2018. It issued a first full ban for fraudulent trading activity to the company CabbageTech in August 2018, and issued the arrest of a cryptocurrency trader for fraud in November 2018.16

Capacity Building: The CFTC has been quick to embrace the incoming changes brought about by a host of emerging technologies, including blockchain and machine learning, and focuses on staying on top of developments and innovating its own processes.17

In 2017, they pioneered a forward-looking regulatory model with the launch of LabCFTC, a focal point to make the CFTC more accessible to fintech innovators and serve as a platform to inform the Commission's understanding of new technologies. The lab aims to promote responsible FinTech innovation to improve the quality, resiliency, and competitiveness of U.S. markets, and to accelerate CFTC engagement with fintech and regtech solutions.

The lab has grown to a six-member core team with law and technology backgrounds and serves as an internal platform and think tank for the CFTC. It is structured in a hub and spoke model, with staff from operating divisions who serve as subject matter experts. LabCFTC has an open door policy and pursues active engagement with the startup and stakeholder community including through hosting office hours in cities across the U.S. It also has international partnerships with governments in the United Kingdom, Australia, and Singapore.18

In 2017, the Agency launched a podcast series, the first of its kind for a government regulator, to educate consumers and bring in wider perspectives from government, private sector, and civil society on a range of topics, including FinTech. Over five podcasts, four consumer advisories, and two primers were released by the CFTC LabCFTC, and the Office of Customer Education and Outreach on the topics of cryptocurrencies and smart contracts between 2017 and 2018.19 The lab recently issued a Request for Information on Ether in order to help inform the Agency on aspects of crypto-asset markets and mechanics. 20

The U.S. Department of the Treasury

The U.S. Department of the Treasury and its associated agencies play a host of important roles in setting the direction and coordination on digital asset regulation.

The U.S. Treasury has been looking into cryptocurrencies through its own divisions, the most visible of which have been three of its specialized agencies: the Internal Revenue Service (IRS), Financial Crimes Enforcement Network (FinCEN), and the Office of Foreign Assets Control (OFAC). The Treasury and their agencies look at virtual assets in their role as a currency, though as an exception, the IRS define them as property for tax purposes.

Financial Crimes Enforcement Network (FinCEN) and Office of Foreign Assets Control (OFAC)

One of the most active areas of guidance and enforcement by the Treasury has been around anti-money laundering (AML), know your customer (KYC), and Counter Terrorism Financing and Sanctions.

With a mandate to safeguard the U.S. financial system from illicit use and combat money laundering, the FinCEN was one of the first regulators to become active on cryptocurrencies in the United States. As early as 2013, the FinCEN issued guidance that virtual currency exchangers and administrators would be considered money transmission businesses (MSBs).21 In a letter to Congress in 2018, FinCEN reiterated that stance with clarifications regarding who would be required to comply.22

As a result, virtual currency exchangers and administrators are required to register with the FinCEN, comply with existing AML/KYC requirements, and the Bank Secrecy Act (BSA), including suspicious activity reports (SARs) and currency transaction reports (CTRs).

As of 2018, there are approximately 100 virtual currency exchangers and administrators that have registered as MSBs with FinCEN.23 FinCEN has examined one third of these MSBs and has brought several enforcement actions.

In 2018, FinCEN and OFAC both released guidance on virtual currencies compliance with sanctions on Iran.24 OFAC added a set of blacklisted digital currency addresses to their Specially Designated Nationals And Blocked Persons (SDN) list.

Internal Revenue Service (IRS)

In 2014, the IRS issued Notice 2014-21 in the form of FAQs to describe how existing tax principles would apply to transactions using virtual currencies.25 In this notice, the IRS stated that virtual currencies would be treated as property for federal tax purposes and provided some information on taxation for some activities such as mining, self-employment, contracting, and third party settlement. However, the technology has matured significantly since then, leaving many questions still unanswered. There have been an increasing number of calls from the community, from lawyers,26 and even from Congress27 for the IRS to issue updated information and clearer guidelines.

Capacity Building: There are two aspects of capacity building in the Treasury: one, at the level of coordination of overall financial regulation; and two, in terms of internal capacity.

At a high level, the Treasury Secretary has the authority to convene all financial regulators. Through the Financial Stability Oversight Council (FSOC), a working group on digital assets was convened in 2017. It was comprised of several regulators, including the SEC, CFTC, the Consumer Financial Protection Board (CFPB), the Federal Reserve, the Office of the Comptroller of the Currency (OCC). After 18 months of deliberation over new technologies, including blockchain, the FSOC came out with a seminal report on recommendations for FinTech in general, which included aspects such as the streamlining of state and federal money transmission laws and experimentation with regulatory sandboxes.28 In recent remarks, a senior official also said the Treasury supported the idea of a federal charter for streamlining regulation.29

The Treasury leads the FSOC digital asset working group and the Treasury and FinCEN participate in a host of inter-agency working groups such as the FBI-led Virtual Currency Emerging Threats Working Group, the FDIC-led Cyber Fraud Working Group, and the Terrorist Financing and Financial Crimes-led Treasury Cyber Working Group.30 These groups provide a consistent platform for capacity building and exchange amongst U.S. financial regulators on blockchain and virtual assets.

Unlike the other agencies, the FinCEN does not have a public-facing focal point of contact for the blockchain community. It does, however, have a network of dedicated officers for virtual currency in its relevant offices and bureaus, such as the Office of Terrorist Financing and Financial Crimes.

In terms of internal capacity building, a unique tool developed by the Treasury is the FinCEN Networking Bulletin that was launched in March 2013. The bulletin provides a more granular explanation of virtual currency movement to law enforcement, and assists them in following the money as it funnels between virtual currency channels and the U.S. financial system.31

Among other things, the bulletin addresses the role of traditional banks, money transmitters, and exchangers that come into play as intermediaries by enabling users to fund the purchase of virtual currencies and exchange virtual currencies for other types of currency. It also highlights known records processes associated with virtual currencies and the potential value these records may offer to investigative officials.

More recently, the bulletin has been expanded from only U.S. financial regulators to include some international partners as well. The bulletin has a crowd-sourcing feature and asks the readers to provide ongoing feedback on what they are learning through their investigations.

This bulletin has helped the FinCEN create a forum to quickly learn of new developments. Furthermore,based on this information, the FinCEN has issued several analytical products of a tactical nature to inform law enforcement operations.

Perspectives of Other Stakeholders

State Governments

State governments within the United States have their own jurisdiction over money transmission and enforcing financial laws, as well as in designing corporate licensing and registration and other incentives to attract startups and investment in their state. New York was the pioneering state in starting these experiments in 2014, and since then several states have come out with their own bills and frameworks.

In 2014, the New York Department of Financial Services created the ‘BitLicense’, a business license for virtual currency activities applying to activities involving New York State or its residents. It included regulation around money transmission, custody, exchange services, and other aspects.32 Although New York had a first mover advantage and followed a thorough consultation process,33 the eventual regulation was seen as onerous34and not well suited to the needs of the startup community.35 Since then, several states have developed bills and legislation to incentivize blockchain startups, including Arizona, Delaware, Nevada, Massachusetts, Washington, and others.36 The most comprehensive and innovative reform to date has, interestingly, come from the state of Wyoming.

In early 2019, Wyoming passed a monumental 13 bills to provide one of the most comprehensive legal frameworks for blockchain startups in the United States.37 Unique protections granted under this legal framework are direct property rights for individual owners of digital assets, a state chartered depository to provide banking services to blockchain startups, a series LLC corporate structure, qualified digital asset custodians, and a regulatory sandbox.38 This framework is the most comprehensive till date in the United States.

Startups and Ecosystem Perspective

The blockchain developer and start-up ecosystems in the United States have faced stark consequences in terms of federal regulations and have their own perspective on how legislation should be created. The significant drop in token prices starting in 2018 led to a period of contraction in the industry (termed “Crypto Winter”) that was, in part, attributed to regulatory crackdowns. The author undertook a series of interviews with blockchain startups and venture capital funds in tech hubs on the West Coast to gauge the impact that regulatory action was having on start-up growth in the space. This revealed a number of key points of concern.

- Investment has slowed down considerably for crypto-based blockchain projects based in the United States: Multiple startups spoke of capital becoming very difficult to secure for crypto-based blockchain projects in the United States. While funding does come in for private blockchain startups, and in trading activity, large scale investment into public blockchain protocols has slowed considerably. Regulatory action has slowed both retail and institutional funding into public blockchain projects, and also impeded the flow of private money. Some startups with innovative products were almost on the verge of shutting down because they were unable to find funding. Many budding startups spoken with in the Seattle area had shut down over the last year because of funding shortages.39

- Public blockchain firms tend to adopt foreign domiciles: Some venture funds commented that even if they wanted to invest in public blockchain startups and have them based in the United States, the lawyers would advise strongly against domicile in the U.S.40 Multiple startups commented that it was a “no-brainer” for them to domicile their crypto-based startups outside of the U.S., which they saw as “unfriendly to cryptocurrencies.”41 A strong sentiment amongst both startups and funds interviewed was that they believed the U.S. government viewed cryptocurrencies negatively and did not support or understand the transformative potential of public blockchains.42

- The regulatory landscape is too confusing for startups: Almost all the startups interviewed found the proliferation of regulators confusing to navigate and said that under current guidelines, they were never sure of when they were under threat of enforcement action. Many startups had taken the initiative of reaching out to their Congressperson and spending significant sums on hiring lawyers. However, they were quickly overwhelmed by jurisdictional confusion between who was setting guidelines and policy standards and who was responsible for enforcement. Practitioners and product developers said that despite best efforts, they were left without a clear understanding of how to legally secure themselves according to continuously emerging guidance measures. As a result, the preference was to domicile their start-up in another country with simpler rules.

- Enterprise experiments are becoming larger: Juxtaposed against a shrinking public blockchain start-up scene were also comments of “Big Tech” experiments in blockchain growing larger and more ambitious. There were multiple mentions of Facebook’s upcoming blockchain product, of the IBM and Walmart’s blockchain project, and Microsoft and other Big Tech firms’ experiments gathering scale and momentum. Some concluded that enterprises would outpace disruptive platforms such as Bitcoin and Ethereum in blockchain adoption, which was in some ways inimical to the disruption of blockchains to monopolistic power.43

Overall Conclusions on the U.S. Approach

The U.S. federal government’s approach has been almost entirely regulatory-led. Legislation and policy are absent from federal government action on virtual assets so far. As a quick note, the Congressional Blockchain Caucus has a small number of members, and although they have introduced three bills, it is unlikely that these will pass anytime soon without wider support in Congress.

An overall assessment of the federal regulatory approach so far highlights the following concerns:

The U.S. federal approach is highly fragmented

The most obvious aspect of the federal approach is the highly fragmented nature of regulatory action. In the absence of directives by Congress or the White House, regulators have taken the lead in government action in the sector. This has created the risk of patchwork regulation due to a highly proliferated financial regulatory system. To their credit, as seen in this paper, federal agencies have put in place many mechanisms for coordination. However, as also seen, this approach has created a lot of confusion and uncertainty on the ground for startups and investors, and has led to the U.S. being seen as an unfriendly destination for crypto-based startups. The model of regulation-by-enforcement, rather than a light touch approach, has deepened this perception and created a clamor for clear rules and guidance before harsh enforcement.

The U.S. federal regulatory approach is missing the paradigm-shifting nature of the technology

Financial regulators have taken a risk-based approach that is technology-neutral. As a result, virtual assets, in their examination by the federal government, have been reduced to their financial functions. This is unfortunate, because blockchain technology powered by cryptocurrencies has transformative implications, not just as a currency or payment medium, but as a business model, as a capital formation model, and as a new protocol for transactions that form the basis of the economy and can impact institutional power and social structures.

There is no agency in the federal government that is looking at blockchain technology as a whole. ICOs, for example, have been reduced to whether or not they are security offerings, but no examination has been done of the model with regard to capital formation laws. No examination has been done of banking laws for blockchain business models at a federal level.

Federal regulators have not undertaken any new rule-making on the issue. This is exacerbated by the lack of federal legislative or executive action. The overall approach of the government has been to extend the application of laws, in many cases from the 1960s, to regulate innovations in the space. This can work in the short term; however, this is increasingly getting entrenched as the federal approach. It started with the FinCEN extending the application of MSB laws in 2013 and continues with the latest SEC guidance furthering the application of the Howey Test in 2019.

It is understandable that since blockchain technology is not used on a major scale yet, federal regulators need not engage in a lengthy and expensive rule making process. However, there are also no signals that such thinking is underway. The internet boom taught us that technology may take time to develop, but it proliferates and gets too big to ignore very fast. The world still faces regulatory challenges from the internet revolution, for example, by not thinking ahead around the use of data in business models. However, these technologies are now too big and deeply embedded in the social fabric to be changed drastically. It would be irresponsible to make similar mistakes with blockchain, as many are referring to it as the second internet.

The U.S. federal regulatory approach is possibly entrenching intermediaries and existing power structures

U.S. regulators, to their credit, have been vocal and careful about wanting to regulate abnormal activity without hampering innovation. However, perhaps unintentionally, regulatory action so far has had the effect of entrenching existing power structures and business models, rather than supporting innovation. This has happened on two fronts.

The first front is entrenched money flows. Blockchain startups had developed an innovative fundraising and user acquisition model with Initial Coin Offerings (ICOs). However, this needed a new regulatory framework, in the absence of which fraudulent activity proliferated. Some countries chose to regulate this by using a sandbox approach. However, the United States undertook a regulation-by-enforcement route, with no clear legal guidelines to hold ICOs. While this did stop fraudulent activity, it also stopped a lot of legitimate activity by scaring away investors and startups, who chose to domicile elsewhere. SEC released its guidelines for ICOs only in February 2019, a year after the wave of enforcement, by which time several other countries had come out with ICO frameworks and startups had relocated. The other effect this had was to reinforce the existing fundraising structures of private, venture capital and institutional money, many of whom were themselves getting disrupted by the ICO model, which had created an alternative avenue of fundraising. It also limited public offerings to traditional listing rules which are notorious in the difficulty they create for startups to list. After the JOBS Act and Section D,44 the ICO model was a second alternative to startup funding that should have received greater attention as an innovation that needed to be fenced in by appropriate rules rather than stopped completely by enforcement.

The second front is entrenched advantage for enterprise and large tech firms. Regulatory action against cryptocurrencies has created a preference for private or enterprise blockchain activity. Prescient industry watchers have already pointed out that true disruption is in public blockchains, that siloed private blockchain experiments would not sustain in the long term and would eventually have to move into a semblance of inter-operable public blockchains. The shift to enterprise blockchain has been to the benefit of existing industry leaders in enterprise solutions, and also spurred Big Tech giants such as Facebook, Amazon, and Microsoft to develop blockchain solutions. This is not a bad development, but juxtaposed with a slowdown of funds for public blockchain startup projects, it also implies that we might see further consolidation of Big Tech over a technology that could have disrupted them.

The U.S. regulatory approach is creating opportunities for regulatory arbitrage globally

The U.S. regulatory approach has been seen by many in the ecosystem as onerous, confusing, and unsupportive, and there is unlikely to be a clear directive from Congress or the White House soon to move towards a single window or more coordinated approach. These conditions have created a ripe environment for global regulatory arbitrage as a lever to attract and retain talented startups and shape the way forward in blockchain technology. Several countries such as Singapore, Malta, and Switzerland have taken a lead in creating sandboxes and other incentives to attract startups and investors, and now have thriving blockchain ecosystems. The timeline for this technology to mature is not too long, and it is likely that mature and scalable solutions will emerge in about five years.45 Unless the regulatory paradigm changes significantly in the United States, other geographies will take a lead in this technology.

Conclusion

The United States’ approach to the regulation of virtual assets has been highly fragmented. Due to the proliferation of federal financial regulators, and the lack of policy oversight, different regulatory agencies have taken the initiative. While from a regulators perspective, this approach is understandable as they are carrying out their respective economic mandates, blockchain is a multi-faceted technology, where financial regulation has direct implications on technological development and business models. Blockchain startups could have served as a disruptor to the centralized influence of large firms in technology and finance. However, the current regulatory framework is not supportive of this disruption, as discussed before.

The United States’ approach to the regulation of virtual assets has been highly fragmented.

The patchwork and regulation-by-enforcement nature of government action is confusing for startups and has deterred U.S. investment into the public blockchain space. Most startups that were working in the public blockchain space have relocated to other countries, and many that stayed are facing funding shortages. This has created a large opportunity for regulatory arbitrage globally, and countries such as Singapore, Switzerland and Malta have made themselves leaders in the space very quickly with progressive regulation and robust startup ecosystems.

There are positive aspects of increased capacity building and inter-agency coordination among federal regulators in the United States. States are also developing innovative frameworks. However, virtual assets remain borderless global assets. Regulating them effectively, while harnessing their innovative potential, will require coordinated action at the national level in terms of both regulations and incentives. However, the White House and Congress remain loosely engaged in the process, and such coordination might not materialize soon.

While America remains a leading player in the technology, competition is increasing globally. In the absence of a holistic policy and regulatory approach, the United States might not fully harness its potential in the long run.

Citations

- Don Tapscott, “2018 Regulation Roundtable: Addressing the Regulatory Challenges of Disruptive Innovation,” Summary of 10 May 2018 Proceedings held at KPMG Toronto, Blockchain Research Institute, Aug. 8 2018.

- Warren Davidson, R-OH, "Text – H.R.7356 – 115th Congress (2017-2018): Token Taxonomy Act." Congress.gov. December 20, 2018, accessed April 14, 2019, source.

- U.S. Securities and Exchange Commission, “Ponzi Schemes Using Virtual Currencies,” July 23, 2017, source

- The DAO is one example of a Decentralized Autonomous Organization, which is a term used to describe a “virtual” organization embodied in computer code and executed on a distributed ledger or blockchain.

- U.S. Securities and Exchange Commission, “Report of Investigation Pursuant to Section 21(a) of the Securities Exchange Act of 1934: The DAO,” July 25, 2017, source

- Lester Coleman, "SEC Subpoenas 80 Cryptocurrency Firms," CCN, March 04, 2018, accessed May 16, 2019. source.

- Nikhilesh De, "SEC Again Delays Decision on Bitwise Bitcoin ETF Approval," CoinDesk, May 15, 2019. accessed May 16, 2019, source.

- U.S. Securities and Exchange Commission, Fintech Finhub, "Framework for “Investment Contract” Analysis of Digital Assets," April 3, 2019, accessed April 14, 2019, source.

- The Howey Test is the standard methodology, put in place by the U.S. Supreme Court to determine whether a transaction is an example of an "investment contract,” i.e., a security. It derives from a 1946 case, SEC v. W.J. Howey Co., a lawsuit involving the Howey Company of Florida. In the context of blockchain tokens, the Howey test can be expressed as three independent elements: (1) An investment of money, (2) in a common enterprise, (3) with an expectation of profits predominantly from the efforts of others.

- "A New Commissioner at America's Main Securities Regulator Causes a Buzz," The Economist, Nov. 08, 2018, accessed April 14, 2019, source.

- Stan Higgins, "The SEC Just Appointed Its First-Ever Crypto Czar," CoinDesk, June 04, 2018, accessed April 14, 2019, source.

- Detailed in the next section, LabCFTC is a pioneering regulatory model in dealing with fintech innovations

- Stephan O'Neal, “SEC Launches FinHub to Communicate With Industry, But What Does It Have to Say?" Cointelegraph, Feb. 13, 2019, accessed April 14, 2019, source.

- Yogita Khatri, "The SEC Wants to Hire a 'Crypto Securities' Advisor," CoinDesk, April 01, 2019, accessed April 14, 2019, source.

- Commodity Futures Trading Commission, “An Introduction to Virtual Currency,” 2017, source.

- Khatri, Yogita, "CabbageTech CEO Indicted in New York for Defrauding Crypto Investors," CoinDesk, March 27, 2019, accessed April 14, 2019, source.

- Chris Giancarlo, "CFTC Chairman Chris Giancarlo,” DC Blockchain Summit 2019, Georgetown University, Washington, D.C., March 6, 2019.

- Daniel Gorfine (Director, LabCFTC), personal interview, Washington, D.C., April 2019.

- Daniel Gorfine, "Podcasts." Commodity Futures Trading Commission, accessed April 14, 2019. source.

- Commodity Futures Trading Commission, "Request for Input on Crypto-asset Mechanics and Markets." December 11, 2018, accessed May 12, 2019, source.

- United States Financial Crimes Enforcement Network, Department of Treasury, Guidance: Application of FinCEN’s Regulations to Persons Administering, Exchanging, or Using Virtual Currencies, FIN-2013-G001, March 18, 2013, source.

- Peter Van Valkenburgh, "FinCEN Raises Major Licensing Problem for ICOs in New Letter to Congress," Coin Center, March 6, 2018, accessed May 12, 2019, source.

- Timothy Spangler and Robert J. Rhatigan. "FinCEN Warns That Virtual Currency Activities Are Subject to Anti-Money Laundering Obligations," Lexology, April 03, 2018, accessed April 14, 2019, source.

- FinCEN, "Advisory on the Iranian Regime’s Illicit and Malign Activities and Attempts to Exploit the Financial System," FIN-2018-A006, October 11, 2018, accessed April 14, 2019, source Advisory FINAL 508.pdf.

- Internal Revenue Service, "Notice 2014-21," March 2014, accessed April 14, 2019, source.

- "Tax Treatment of Cryptocurrency Hard Forks for Taxable Year 2017," American Bar Association to Internal Revenue Service, March 19, 2017, Washington, D.C.

- "IRS Treatment of Virtual Currencies," U.S. House of Representatives Committee on Ways and Means to Internal Revenue Service, Sept. 19, 2018, Washington, D.C. source.

- Steven T. Mnuchin and Craig S. Phillips, “A Financial System That Creates Economic Opportunities Nonbank Financials, Fintech, and Innovation,” U.S. Department of the Treasury, July 2018. source.

- Craig S. Phillips "Fireside Chat with Counselor Craig Phillips, U.S. Dept. of the Treasury," Speech at the D.C. Blockchain Summit 2019, Georgetown University, Washington, D.C., March 6, 2019.

- Statement of Jennifer Shasky Calvery, Director, Financial Crimes Enforcement Network, United States Department of the Treasury (2013) (testimony of Jennifer Shasky Calvery).source.

- Ibid.

- "Virtual Currency Business (BitLicense)," New York Department of Financial Services, 2015. source.

- Patrick Murck, (Partner, Cooley LLP), personal interview, March 2019.

- Marco Santori and Maria Vullo, "Legal Tender? The Regulation of Cryptocurrencies," June 7, 2018, accessed April 14, 2019, source.

- Anonymous New York venture capitalist in blockchain, personal interview, March 2019.

- Gage Lathrop and Dale Werts, "Blockchain and Cryptocurrency: State Law Roundup," JD Supra, July 10, 2018, accessed April 14, 2019, source.

- Long, Caitlin, "What Do Wyoming's 13 New Blockchain Laws Mean?" Forbes, April 08, 2019, accessed April 14, 2019, source.

- Caitlin Long (Co-Founder, Wyoming Blockchain Coalition), personal interview, Feb. 2019.

- Multiple start-up founders and business strategy leads (anonymous), personal interview, April 2019, Seattle.

- Greg Heuss (Managing Partner, Counterpoint Ventures), personal interview, April 2019, Seattle, Washington.

- Multiple start-ups (anonymous), interview by the author, April 2019, Los Angeles and San Francisco, California.

- David Otto (Founder and Managing Partner, Martin Davis PLLC), personal interview, April 2019, Seattle, Washington.

- Multiple start-ups and Venture Capitalists (anonymous), interview by the author, April 2019, Los Angeles and San Francisco, California.

- The SEC, as well as the securities laws it enforces, have come under bipartisan criticism from academics, entrepreneurs, investors, and members of Congress for creating red tape that makes it difficult both for entrepreneurs to raise capital in the public markets and for investors to find wealth-building opportunities. This concern prompted Congress to pass regulatory relief overwhelmingly in the Jumpstart Our Business Start-ups (JOBS) Act, which was signed by President Obama in 2012. In 2018, the U.S. House of Representatives passed a bill allowing further relief, the Jobs and Investor Confidence Act. The JOBS Act eased some burdens on entrepreneurs by exempting small and “emerging growth” companies from some of the costly burdens of securities laws like the Sarbanes-Oxley Act of 2002 and the Dodd-Frank Act 2010.For further reference: John Berlau, "Cryptocurrency and the SEC's Limitless Power Grab," Competitive Enterprise Institute, April 11, 2019, accessed April 14, 2019, source.

- Multiple venture capitalists, interviewed by author, Feb./Apr. 2019, New York, Seattle, San Francisco.