Jason Delisle

Director, Federal Education Budget Project

Since President Clinton first enacted tax credits for college tuition in the late 1990s, lawmakers have expanded these policies, which now amount to over $20 billion in annual aid. While these benefits are commonly described as helping families pay for college, which usually means a two-year or four-year degree, they also apply to graduate and professional education. These students are eligible for two tuition tax benefits that undergraduates may also claim: the $2,000 Lifetime Learning Credit (the Lifetime Credit) and the $4,000 Tuition and Fees Deduction (the deduction). In this post we analyze which graduate students can claim these benefits and how much they can claim, revealing some little-known facts. Some of the key findings are:

In a report earlier this year, A New Look at Tuition Tax Benefits, we used nationally representative survey data, the quadrennial National Postsecondary Student Aid Study (NPSAS), to estimate the optimal tax benefits undergraduates were eligible to claim. In this post we report the results from the same analysis for graduate and professional students (a group we refer to as “graduate students” for simplicity) and compare them with those for undergraduate students. We use the 2011-12 school year NPSAS. A methodology section at the end of our earlier paper explains more.

Besides distinguishing between graduate and undergraduate students, our approach relies on survey data rather than data from income tax returns, in contrast to prior research. We can examine how eligibility for tax benefits is distributed among the entire graduate student population. We can also identify the characteristics of students and families who cannot claim benefits and how eligibility and benefit amounts differ based on the type of school a student attends and the degree program she pursues.

In our analysis, student income information and tax benefit eligibility rules are from the tax year prior to 2011-12, while tuition and financial aid information is from 2011-12. One limitation of this approach is that a graduate student’s income may be different before and after he enrolls, and it is the student’s earnings during the calendar year she is enrolled that will determine her tax benefit eligibility.

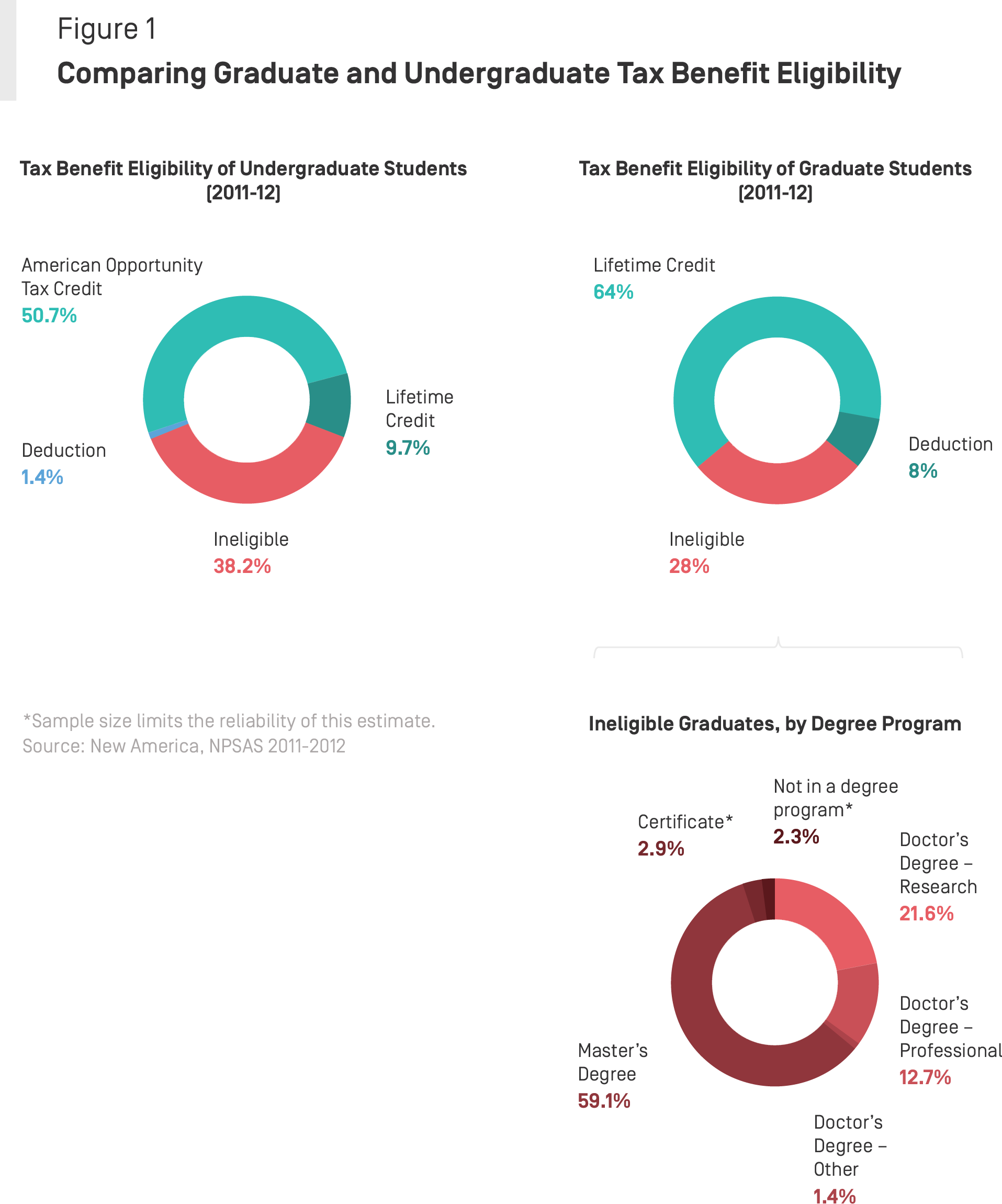

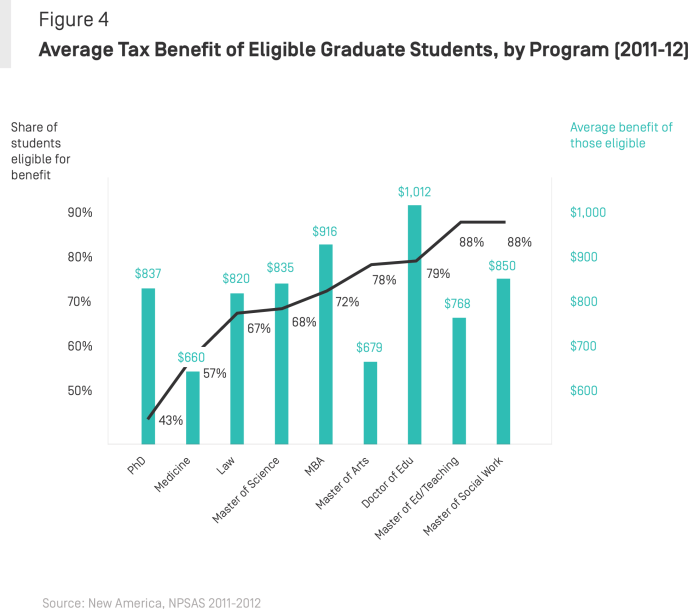

Parts of our analysis break out information on different types of graduate degrees and programs as defined in the NPSAS, including Master’s, PhD and post-Bachelor’s and post-Master’s certificates. PhD students include three categories: “PhD – Research” is a traditional doctoral student in an academic discipline; “PhD – Professional” are degrees designed for careers outside of the academe, such as medicine and law. “PhD – Other” is a small category that includes any PhD not in the other two categories. All degree and program groups shown have a sample size of at least 100, unless otherwise noted.

Lifetime Learning Tax Credit: is available to both undergraduate and graduate students. It allows filers to reduce their federal taxes up to $2,000. The credit is equal to 20 percent of the first $10,000 in tuition and fee expenses. Income limits are indexed to inflation, and are set at $51,000 or ($102,000 for married filers) for the full benefit; those earning above those amounts but less than $61,000 ($122,000) are eligible for a partial credit as the benefit is phased out. As the name implies, it is meant to facilitate “lifetime learning” by providing tax benefits to students in any year of postsecondary education.

Tuition and Fees Deduction: is available to both undergraduate and graduate students. It allows students or families to deduct up to $4,000 in tuition and fees from their incomes, reducing taxes by their marginal tax rates (e.g., 25 percent of $4,000 for those in the 25 percent tax bracket). Students and families do not need to itemize deductions to claim it. Income eligibility is capped at $65,000 ($130,000 for married filers). Above these limits a partial deduction of up to $2,000 is available for those with incomes less than $80,000 ($160,000). The benefit has been available since 2002. It has always been temporarily authorized, but extended multiple times. The last extension made the credit available through 2014; tax filers will not be able to claim the deduction in 2015 unless Congress acts to extend it.

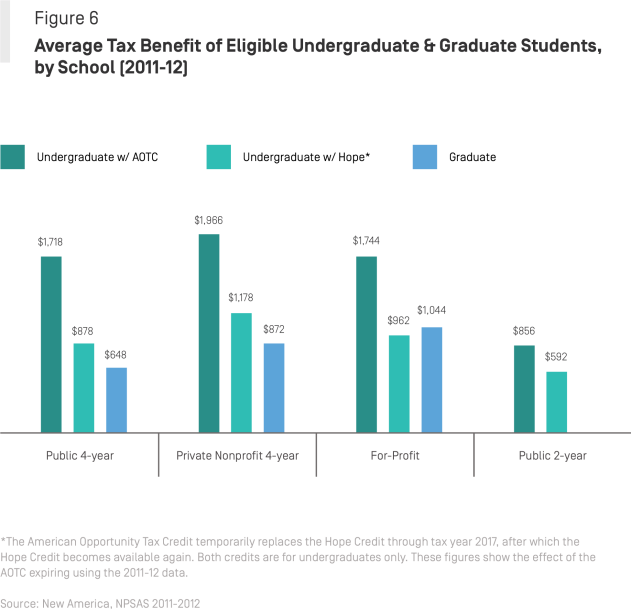

American Opportunity Tax Credit (AOTC): is the largest tax benefit but available only to undergraduates in their first four years of school who are enrolled in a degree program at least half time. These students may receive a credit up to $2,500, or 100 percent of the first $2,000 in tuition in fees and 25 percent of the next $2,000. Up to $1,000 of this credit is refundable, meaning the tax filer can claim it even if she has no tax liability to offset. Eligibility for the full AOTC is capped for single tax filers earning $80,000 ($160,000 for married filers). Those earning up to $90,000 ($180,000) can claim a partial benefit under a phase-out provision. The AOTC expires after the 2017 tax year, and the Hope Credit becomes available to undergraduates in the first two years of study. It is not refundable and is worth a maximum of $1,800.

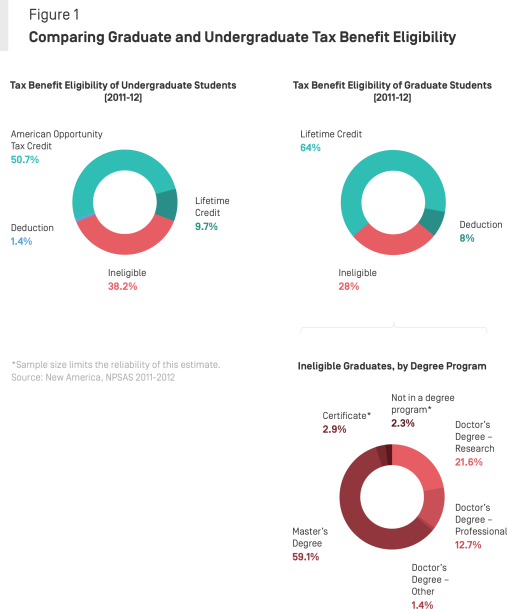

Of the total dollar value of tax benefits available to graduate students, master’s degree students as a group are eligible for the most aid. Nearly three quarters of all of the dollars available through the tax benefits can be claimed by master’s degree students. That is because they make up the bulk of graduate students (67.6 percent), but also because they are more likely to pay tuition than PhD students. About 90 percent of master’s degree students pay tuition costs compared with 69 percent of research PhD students.

This study offers the first-ever analysis of the aid graduate and professional students can claim through federal tuition tax benefits. Combined with our earlier study, A New Look at Tuition Tax Benefits, which focuses on undergraduate students, it provides a complete picture of this large source of federal student aid. Breaking out undergraduate and graduate students in our analysis has revealed some new and surprising facts about tuition tax benefits, and serves as a reminder that these two groups of students are quite different, but lawmakers and researchers tend to treat them as one when it comes to tax benefit policy.

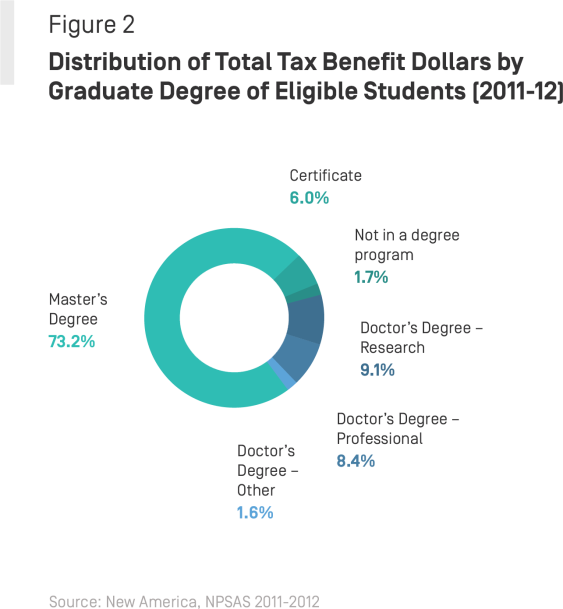

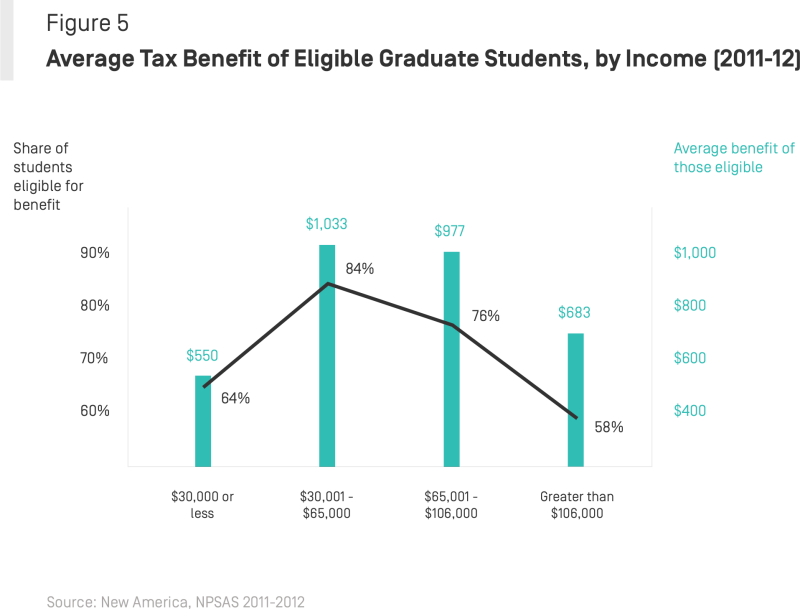

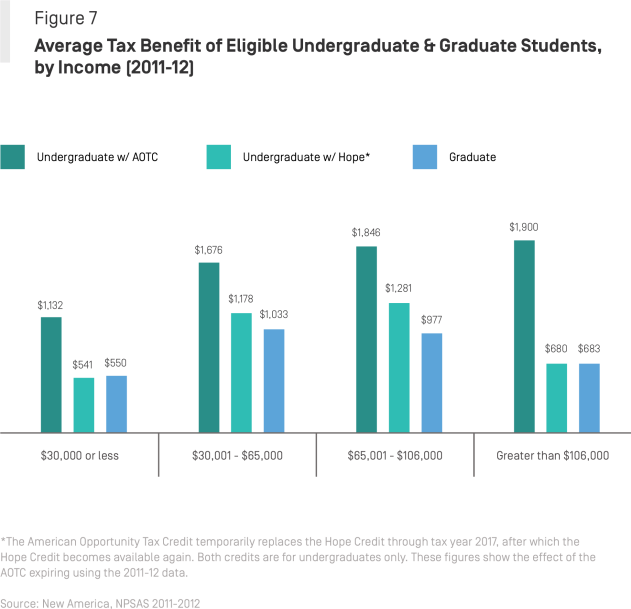

Notably, we now know that graduate students are more likely to qualify for tax benefits than are undergraduates, and without the American Opportunity Tax Credit, graduate students in the lowest and highest income groups would qualify for larger benefits on average than undergraduates in those groups.

We also discovered that graduate students who work while enrolled are more likely to benefit from the tax benefits and to qualify for larger benefits — what might be called a windfall benefit for part-time attendance. Meanwhile, full-time students have less time to work and therefore do not accrue sufficient earnings to generate the taxes needed to claim tax benefits. It turns out that qualifying for a tuition tax benefit as a graduate student is as dependent on working full-time as it is on paying tuition. That cannot be what policymakers intended.

Put another way, the largest tuition tax benefits for graduate students go to people who are fairly well-off: college graduates with full-time jobs who are pursuing even more postsecondary education. Seen in that light, one could make a good case for redirecting tax benefits for graduate school to those who are still struggling to pay for a 2-year or 4-year degree.

Director, Federal Education Budget Project