Stephen Burd

Senior Writer & Editor, Higher Education

The Tuition and Fees Deduction, the most regressive of all the government’s tuition tax break programs, expired at the end of December. Champions of the program are no doubt gearing up to push Congress to revive the program once again. Lawmakers should, however, resist their pleas and instead focus on overhauling the poorly targeted, duplicative, and complex array of higher education tax benefits the government offers.

Congress created the Tuition and Fees Deduction program, which allows students and their families to subtract from their taxable income up to $4,000 a year in tuition and fees, as part of President George W. Bush’s broader tax cut legislation in 2001. Private college leaders championed the deduction, saying it would be more helpful to students attending their high-priced schools than the Hope and Lifetime Learning tax credits that the Clinton administration and Congress established in the late 1990s to make college more affordable for the middle class. Powerful lawmakers from Northeastern states, where these institutions are heavily represented, took up the cause and convinced their colleagues to include the deduction in the larger tax cut package.

At the time, some student aid advocates and experts objected to the proposal because they said that it would primarily help the highest income families eligible for the benefit – those earning between $100,000 and $160,000 annually. That’s because a tax deduction is subtracted from the amount of a family’s income that is subject to taxation. As a result, individuals in higher tax brackets would receive greater savings than those in lower brackets who paid the same tuition. In addition, low-income families who pay little or no income tax wouldn’t receive any benefit from it at all.

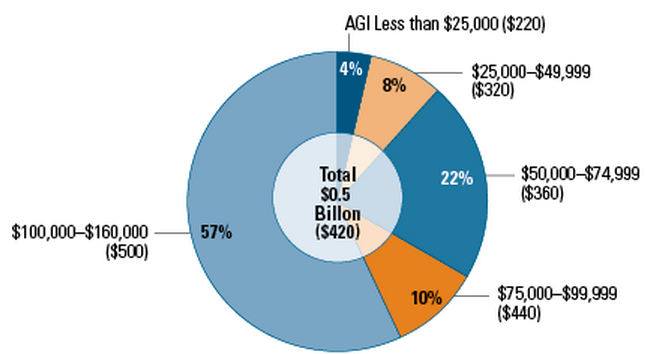

As I’ve written previously, these concerns were wholly warranted. According to the College Board, 57 percent of the $420 million in savings that filers received through the deduction in 2011 went to families making $100,000 or more. Meanwhile only 12 percent went to taxpayers making less than $50,000.

In other words, the majority of the benefits from the program went to families who, by all indications, would have sent their children to college without the help.

Besides being regressive, the deduction is also duplicative of the other tuition tax break programs that the government offers – such as the Lifetime Learning Credit, a $2,000 non-refundable tax break that is available to students who take at least one postsecondary education course; and the American Opportunity Tax Credit, a $2,500 partially-refundable tax break that is available to help cover tuition, fees, and course material expenses for the first four years of college.

The problems with the Tuition and Fees Deduction are not isolated to that program. Overall, the government’s multiple tuition tax break programs are poorly targeted, with a substantial share of the tax-based student aid going to higher-income families. And by offering multiple programs that are so similar, policymakers have made it unnecessarily difficult for students and their families to choose the option that is best for them. The Government Accountability Office found, for example, that 237,000 of 588,000 filers who claimed the tuition tax deduction in 2009 would have been better off claiming the lifetime learning tax credit instead. According to the GAO, these filers forfeited about $67 million in tax benefits as a result.

In November, the Consortium for Higher Education Tax Reform, of which New America is a member, issued a paper that set out a series of specific recommendations that would go a long way toward fixing the problems that are associated with the tuition tax break programs. The consortium’s reforms would ensure that tax-based student aid goes to low- and modest-income students who have the hardest time affording college, rather than to higher-income income individuals who are already very likely to attend college without a tax incentive. The consortium also calls for eliminating overlapping tax benefits, making it easier for families to understand and claim tax-based student aid, and deliver aid when college bills are due. And the consortium’s plan would reinvest any potential savings from these reforms into student aid.

Instead of reviving the Tuition and Fees Deduction, lawmakers should follow the consortium’s lead and reshape tax-based student aid so that it better meets our national goals of improving college access, affordability, and success.”

Senior Writer & Editor, Higher Education