The Subprime PLUS Loan Crisis How Dozens of Universities Steer Low-Income Families to Debt They Can’t Afford

Table of Contents

Abstract

A New America report identifies 41 universities that appear to be steering low-income families to Parent PLUS loan debt they cannot afford, at the same time that they are providing large tuition discounts to wealthier students. The list includes 23 selective private universities and 18 public flagship and research institutions, nearly half of which are in the South.

Collectively, these 41 universities, many of whom work closely with private, for-profit enrollment management consultants, spent $2.4 billion of their own financial aid dollars on students who lacked financial need in 2023, according to the latest data available. Nearly $2 out of every $5 these schools spent on institutional aid that year went to non-needy students—those whom the federal government deems able to afford college without financial aid. Meanwhile, more than 32,000 families of Pell Grant recipients who had either graduated or left these schools in the recent past were stuck with PLUS loans they took out to pay for their children to attend these institutions. These families carried a median Parent PLUS loan debt load of nearly $30,000 each. For many of these families, the amount they owed came close to or exceeded their yearly earnings.

A potential subprime PLUS loan crisis is looming. It’s hard to see how encouraging low-income families to take on debt that they probably can’t repay will end in anything but disaster, unless the government takes decisive action to contain and undo the damage.

Updated on March 18, 2026: This report has been updated to correct the percent of University of Connecticut freshmen receiving non-need-based aid from 88 percent to 20 percent.

Acknowledgments

We would like to thank the Joyce Foundation for its generous support of this work. The views expressed in this report are those of its author and do not necessarily represent the views of the Joyce Foundation or its officers or employees. The author would like to thank Rachel Fishman and Sabrina Detlef for their keen editing skills. He would also like to thank Katherine Portnoy, Amanda Dean, and Natalya Brill for their communications, production, and data visualization support.

Downloads

Introduction

Public flagship and research universities in the South are thriving, setting enrollment records year after year. National publications marvel at their success recruiting students from around the country, particularly at a time when higher education as a whole seems to be in such dire straits. And journalists and pundits twist themselves into knots trying to explain the appeal of the schools to suburban college applicants from Northern states. Are these students flocking to these schools to enjoy the sun, tailgate parties, and winning football? Or are they, as Fox News would have it, leaving in droves to escape woke politics?1

In reality, there is a much simpler reason. Many of these universities are spending tens of millions of dollars each year—and, in the case of the University of Alabama, $185 million annually—to reel in affluent students from around the country.2 In other words, these schools are offering the best deals to well-to-do students and their families who are shopping around. Take Caroline Ward, who in 2017 was one of more than 200 freshmen from Illinois to receive full-tuition scholarships from the University of Alabama. “Students are looking for those scholarships, and they’re going to take them wherever they could get them,” Ward told the Chicago Tribune at the time.3

This sounds like a win-win, right? The universities are spending a lot of money to get the applicants they want, and these students are getting a great deal. What’s not to like?

There is, however, another side to this story, and it is one that has not received nearly enough attention. While the universities are wooing wealthy students, many of them are pushing the families of low- and lower-middle-income students into economic peril by pressuring them to take on heavy debt loads they are unlikely to be able to repay.

At issue is the fact that these universities, working with high-priced enrollment management consultants, are engaging in financial aid leveraging or financial aid optimization, in which analysts determine the precise price points at which these institutions can enroll different groups of students without spending a dollar more than is necessary. At selective colleges, both private and public, the largest discounts go to the most desirable students, typically the highest-achieving applicants, who can help the schools rise up the U.S. News & World Report rankings, and the wealthiest, who, even with the tuition break, can boost the institutions’ bottom line. While lower-income students will often receive some aid, those dollars won’t come anywhere close to meeting their financial need, which means that these students’ families are left with little choice but to borrow federal Parent PLUS loans to cover the funding gaps.

The Parent PLUS loan program was never intended for this purpose. Congress created the program in 1980 to help middle- and upper-middle-income families afford to send their children to expensive private colleges. For low-income families with few assets, taking on PLUS loans is extremely risky. Unlike federal student loans, which are strictly limited to $5,500 to $7,500 per year for dependent students (those under the age of 24), PLUS loans, for much of their history, have allowed parents to borrow up to the full cost of attendance, which includes not only tuition and fees but living expenses as well, regardless of their income.

Parent PLUS debt, like federal student loans, generally can’t be discharged in bankruptcy, and the loans are subject to the government’s extraordinary debt collection powers, including wage garnishment and partial offsets of defaulted borrowers’ Social Security benefits and income tax refunds. As a result, failure to repay these loans can lead to financial disaster, particularly for older Americans with few resources.4

To be fair, many selective colleges use financial-aid leveraging strategies for only a subset of their students. And those colleges that remain committed to meeting the full financial need of their students may use the additional revenue they generate from recruiting affluent students to boost need-based aid at their institutions.

However, the country’s largest enrollment management firms aggressively market financial aid leveraging or optimization products that are designed to help colleges use all of their aid to pursue the most desirable prospective students and increase their bottom lines. As EAB, the giant enrollment management consulting company, states in its marketing materials, “Our Financial Aid Optimization program ensures that every dollar you commit to aid is used to further your enrollment and net tuition revenue goals.”5

One way for a college to use financial aid to increase its “net tuition revenue goals” is to provide discounts to a larger number of wealthy students, who, even with the rebates, will ultimately pay more than less advantaged students and have families who may be willing to make substantial donations to the institution. But another way is to steer low-income students’ families to Parent PLUS loans. After all, Parent PLUS loans are easy credit colleges can offer families to cover funding gaps. The loans are readily available, so long as potential borrowers do not have bad credit. And because there are no consequences for the schools if borrowers can’t repay the debt, college officials don’t have to worry about how hazardous these loans may be for students’ families. As a 2019 Urban Institute report stated, the PLUS loan program is “a no-strings-attached revenue source for colleges and universities, with the risk shared only by parents and the government,” which loses the money if borrowers default.6

There have long been rumors that colleges were pushing low-income families to borrow PLUS loans. In October 2021, The Wall Street Journal confirmed these suspicions in a front-page exposé entitled “How Baylor Steered Lower-Income Parents to Debt They Couldn’t Afford.”7 The newspaper revealed that Baylor had been pressing low-income families to take out “no limit” Parent PLUS loans and then used the proceeds to help pay for the institution’s efforts “to transform itself from a regionally known Baptist college into a national brand.” The article cited U.S. Department of Education data showing that these cash-strapped families borrowed a median debt load of nearly $44,000, more than many of them earned in a year.8

According to The Wall Street Journal, Baylor’s inability or unwillingness to adequately support low-income students over the previous decade had not discouraged university recruiters from seeking them out. If anything, they recruited these students even more aggressively. Between 2010 and 2015, recipients of Pell Grants, the federal government’s primary source of funding for low-income students, made up between 20 and 25 percent of the student body annually. A former recruiter complained that she had been tasked with “visiting poor neighborhoods in Texas to sell prospective students on a college they couldn’t afford.”9

Confronted by The Wall Street Journal reporters, Linda Livingstone, Baylor’s president, acknowledged that her predecessors had acted irresponsibly by enrolling “students who really couldn’t afford Baylor.” She pledged to do better. “My heart goes out to families that are in that situation,” she told the newspaper. “We are working very, very hard to ensure that we don’t see that so much going forward.”10

While Livingstone’s sympathy provides cold comfort for families who were encouraged to take on this debt, she has taken steps to make Baylor more affordable for low-income students. Under the new Baylor Benefit Scholarship program, the university waives tuition and fees for students from families with annual incomes of $50,000 or less.11 University officials say the program is paying off, as the retention rates for Pell Grant recipients at the university has shot up.12 Still, the program does not cover room and board and other living expenses, so the jury is still out on how helpful it will be. And Baylor continues to be one of the most aggressive schools in providing non-need-based discounts to affluent students.

The Wall Street Journal reporters made clear that Baylor was not alone in pushing low-income families to take out Parent PLUS loans. In fact, the article led off by stating, “Some of the wealthiest U.S. colleges are steering parents into no-limit federal loans to cover rising tuition, leaving many poor and middle-class families with debt they can’t repay.”13 The journalists examined Parent PLUS loan borrowing at the wealthiest private universities in the country—those with endowments of $1 billion or more. They wrote that in addition to Baylor, about a half-dozen other of the most-wealthy schools, including Syracuse University, Texas Christian University, and the University of Miami, seemed to be steering low-income families to PLUS loans because they had “relatively low Parent PLUS repayment rates and high numbers of borrowers from low-income backgrounds.”14

Last year, I wrote a paper, entitled A Case of Predatory Inclusion at Baylor University, which revisited The Wall Street Journal article and provided updates on what has happened at Baylor since.15 The paper argued that the financial aid leveraging strategies that enrollment management firms like EAB and Ruffalo Noel Levitz market to universities push their clients to engage in a process of predatory inclusion. Predatory inclusion is when a marginalized group is given access to a service, good, or opportunity, but the conditions of access jeopardize the benefits.16

Universities that leverage financial aid and saddle low-income families with tens of thousands of dollars of debt they are unlikely to be able to repay are engaging in predatory inclusion. Yes, these universities are providing higher education access but at the potential cost of financial ruin for students’ families. That’s too high a price to pay, particularly given the wealth and power of these institutions.

For this paper, I wanted to identify universities, besides Baylor, that appear to be the most aggressive in leveraging their financial aid and pushing low-income families to borrow PLUS loans they cannot afford. Because there are affluent schools with lower endowments that leverage the bulk of their aid, this paper includes private colleges with endowments of $500 million or more.

Even more significantly, this paper includes public universities as well. In the face of state disinvestment and the lure of moving up the U.S. News rankings, many public universities have embraced the enrollment management strategies of their private college counterparts. At the urging of consultants, these once-low-cost schools, which for decades served as a gateway to the middle class, are increasingly employing their aid to lure affluent out-of-state students with good grades and standardized test scores to their campuses so that they can increase both their revenue and their rankings.17

In order to identify the schools that are most aggressive in leveraging their financial aid, I examined more than 20 years of institutional financial aid data for each of these institutions.18 I also looked at the average-net-price-by-income data that colleges have reported annually to the U.S. Department of Education’s Integrated Postsecondary Education Data System (IPEDS) since 2008 to examine the funding gaps with which these schools are leaving their lowest-income students.19

This paper identifies 41 universities that appear to be aggressively leveraging their aid and pushing low- and lower-middle-income students to borrow Parent PLUS loans. The list includes 23 selective private universities and 18 public flagship and research institutions, nearly half of which are in the South.

Collectively, these 41 universities spent $2.4 billion of their own financial aid dollars on students who lacked financial need in 2023, the latest data available. Nearly $2 out of every $5 these schools spent on institutional aid that year went to non-needy students—those whom the federal government deems able to afford college without financial aid.20 Meanwhile, more than 32,000 families of Pell Grant recipients who had either graduated or left these 41 schools in the recent past were stuck with PLUS loans they took out to pay for their children to attend these institutions. These families carried a median Parent PLUS loan debt load of nearly $30,000 each.21 For many of these families, the amount they owed came close to or exceeded their yearly earnings.

In 2023, the 41 universities collectively:

- provided more than a quarter of freshmen a median amount of non-need-based “merit” aid of nearly $15,000 each;

- met, on average, just 74 percent of the financial need of their freshmen student aid recipients; and

- charged freshmen from families with annual incomes of $30,000 or less an average net price of $18,000, after all grant and scholarship aid was awarded. At the private universities, these first-year students and their families were left on the hook for about $24,000, and at the public ones, they had to come up with more than $14,000.

Like Baylor, the 41 universities on the list have higher aspirations. None more so than the University of Alabama, which has spent over $2 billion of its own money in current dollars on non-need-based aid since 2003, the year the institution declared its intention to become a national university. This paper shows how the University of Alabama has been on a remarkably similar path as Baylor over the past two decades and has put low- and lower-middle-income families in financial jeopardy. Meanwhile, its aggressive approach has forced other public universities, particularly in the South, to respond in kind.

This paper also shows that some of the private universities on the list have used enrollment management strategies, such as financial aid leveraging, since the 1980s and 1990s to transform themselves from commuter schools to nationally prominent universities. Schools like George Washington University produced the blueprint that schools like Baylor and the University of Alabama have followed to try and raise their stature.

We will not know the full fallout from these Parent PLUS loan steering practices for a while, because students and their parents did not have to make payments on their loans during the COVID pandemic, and the Biden administration did not collect on defaulted student loans. President Trump resumed student and parent loan collections and then paused them once again. Nevertheless, there is expected to be a tsunami of student and parent loan defaults over the coming year.

Worried that the lack of loan limits in the Parent PLUS loan program have given colleges carte blanche to raise sticker prices as high as they want and have encouraged overborrowing, the Republican-led Congress approved legislation in July that introduced borrowing caps into the program. Starting on July 1, 2026, families will be able to take out Parent PLUS loans up to only $20,000 per year per student, and $65,000 overall for that individual while in college. While the policy is well-intentioned, it is unlikely to be anything but minimally helpful for low-income families who cannot afford to take on any Parent PLUS loans. As a recent Brookings Institution paper argued, the new loan limits will continue “leaving financially vulnerable families exposed to unmanageable debt burdens.”22

To make matters worse, the legislation removed the ability of parents to consolidate their PLUS loans and pay the debt back as a percentage of their income through the Income-Contingent Repayment Program. This was the one safety net available in the Parent PLUS loan program for financially distressed borrowers.

Substantial changes need to be made to the Parent PLUS loan program. Chief among them would be adding an “ability to pay measure” that would prevent parents from borrowing over their means. And colleges should have skin in the game, so that they are held accountable if large numbers of their former students’ parents are unable to repay their loans. But fixing the Parent PLUS loan program is not enough. The problems outlined in this report won’t be solved until policymakers recognize that what’s happened at these 41 universities isn’t an accident and isn’t inevitable. Loading low-income families with Parent PLUS loans is part of the deliberate financial aid leveraging strategies that the country’s largest enrollment management firms have been selling colleges. Policymakers must put the brakes on financial aid leveraging and hold these firms and their clients to account for the damage they have done to low- and lower-middle-income families who simply wanted to give their children the same opportunities that more affluent families take for granted.

But even more fundamentally, it is time for policymakers to address the real affordability crisis in higher education for the vast majority of Americans, instead of standing by as selective public and private colleges and universities fight over and cater to the students who already have every advantage in the world.

Citations

- Joshua Nelson, “High School Seniors from the North Flock to Southern Universities: Report,” Fox News, October 6, 2024, source.

- Data on the University of Alabama’s yearly spending on non-need-based aid, which has been adjusted for inflation, comes from an annual survey that the college guidebook publisher Peterson’s conducts of colleges and universities. New America licensed data from Peterson’s “Undergraduate Financial Aid and Undergraduate Databases” 2024.

- Dawn Rhodes, “Growing Brain Drain: University of Alabama’s Gain in Drawing in Illinois Students Is a Loss for Illinois,” Chicago Tribune, April 6, 2018, source.

- For more on the dangers that student and Parent PLUS loan default poses for older Americans, see CFPB Office for Older Americans and Office of Students and Young Consumers, “Social Security Offsets and Defaulted Student Loans,” Consumer Financial Protection Bureau website, January 8, 2025, source.

- EAB, “Solutions: Financial Aid Optimization,” source.

- Sandy Baum, Kristin Blagg, and Rachel Fishman, Reshaping Parent PLUS Loans: Recommendations for Reforming the Parent PLUS Program (Urban Institute, April 2019), 4, source.

- Tawnell D. Hobbs and Andrea Fuller, “How Baylor Steered Lower-Income Parents to Debt They Couldn’t Afford,” Wall Street Journal, October 14, 2021, source.

- Hobbs and Fuller, “How Baylor Steered Lower-Income Parents,” source.

- Hobbs and Fuller, “How Baylor Steered Lower-Income Parents,” source.

- Hobbs and Fuller, “How Baylor Steered Lower-Income Parents,” source.

- Baylor University, “Baylor Benefit Scholarship,” source.

- Wesley Null (Baylor University vice-provost for undergraduate education and institutional effectiveness), in discussions with the author, April 2025.

- Hobbs and Fuller, “How Baylor Steered Lower-Income Parents,” source.

- Hobbs and Fuller, “How Baylor Steered Lower-Income Parents,” source.

- Stephen Burd, A Case of Predatory Inclusion at Baylor University: How the Baptist University Steered Low-Income Families to Hazardous Debt as It Sought National Prominence (New America, June 2025), source.

- For more on the concept of predatory inclusion, see Louise Seamster and Raphaël Charron-Chénier, “Predatory Inclusion and Education Debt: Rethinking the Racial Wealth Gap,” Social Currents, 4, no. 3 (2017): 200, doi: 10.1177/2329496516686620.

- Ozan Jaquette, State University No More: Out-of-State Enrollment and The Growing Exclusion of High-Achieving, Low-Income Students at Public Flagship Universities (Jack Kent Cooke Foundation, May 2017), source.

- Data on the 41 universities’ spending on institutional aid over the last 20 years comes from an annual survey that the college guidebook publisher Peterson’s conducts of colleges and universities. New America licensed data from Peterson’s “Undergraduate Financial Aid and Undergraduate Databases,” 2024.

- Colleges report the average net-price-by-income data annually to IPEDS, which displays the school-by-school data on its College Navigator site.

- Data on the 41 universities’ spending on non-need-based aid in 2023 comes from an annual survey that the college guidebook publisher Peterson’s conducts of colleges and universities. New America licensed data from Peterson’s “Undergraduate Financial Aid and Undergraduate Databases” 2024.

- The PLUS loan borrowing data are produced for rolling two-year pooled cohorts for the U.S. Department of Education’s College Scorecard. In this case, the cohort consists of PLUS loan borrowers who are the families of Pell Grant recipients who graduated or withdrew from the school in 2019–20 and 2020–21.

- Arnav Dharmagadda and Sarah Turner, Capping the Wrong Program: Why Parent PLUS Loan Limits May Miss the Mark (Brookings, 2025), 2, source.

Making the List

Until the start of this decade, it was not possible to detect whether specific colleges and universities were pressuring low-income families to take out Parent PLUS loans. That’s because there were no school-by-school data available indicating which parents were borrowing PLUS loans to send their children to those institutions.

We did know, however, that many colleges downplay the risks that low-income families can expect when they borrow PLUS loans. A significant share of colleges engage in the deceptive act of packaging PLUS loans in the financial aid offers they make to prospective students, often in the exact amount of their funding gaps.1 As ProPublica and The Chronicle of Higher Education wrote in a joint 2012 article on Parent PLUS loans, “That can make it look like a family won’t have to pay anything at all for college, at least until they read the fine print.”2 In addition, many schools omit key details about PLUS loans in their award letters, keeping students and their families in the dark about the potential hazards of using them. Borrowers often have buyer’s remorse and complain that their children’s colleges kept them in the dark.3

There have also been alarming trends in the national data available on Parent PLUS loan borrowing. In 2018, New America’s Rachel Fishman released an eye-opening report showing that low-income families—and particularly those of color—were increasingly taking out Parent PLUS loans.4 Fishman explained how discriminatory federal housing and lending policies had prevented most Black families from building wealth, forcing them to be more reliant on debt financing for college than white families. “Given the enormous collection powers of the federal government, the Parent PLUS loan program is becoming predatory for Black PLUS borrowers who are more likely to be low-income and low-wealth, and who will likely to struggle to repay,” she wrote.5

Other reports show that these problems are getting only worse. A 2022 paper from Georgetown University Law School’s Center on Poverty and Inequality found that the share of students whose families annually earned under $30,000 and borrowed PLUS loans grew from fewer than one in 10 in 2008 to one in five in 2018. The increase was sharpest for low-income Black students. The share of Black students whose families had annual incomes of less than $30,000 and borrowed PLUS loans “nearly tripled,” from 18 percent to a shocking 44 percent.6

The picture became clearer in January 2021, when the U.S. Department of Education added institution-by-institution PLUS loan borrowing and repayment data to its College Scorecard, an online consumer tool for college applicants and their families. With the changes, the Scorecard revealed the number of Parent PLUS Loan borrowers at each college or university whose children graduated or had left the institution in recent years. The Scorecard also broke down the data to show how many of those borrowers were the parents of Pell recipients. In addition, the Scorecard disclosed the median amount of Parent PLUS loan debt these low- and lower-middle-income families took out.

To compile the list of 41 public and private universities highlighted in this report, I analyzed the College Scorecard data, and I included only those schools at which the families of Pell Grant recipients made up at least one-third of PLUS loan borrowers and borrowed a median amount of $15,000 or more. Collectively, at the 41 schools, 45 percent of the borrowers were the parents of Pell recipients, and they borrowed a median amount of $29,102.

Because I was looking for universities that are big players in enrollment management, I examined more than 20 years of institutional financial aid data at more than 300 selective colleges and universities. These data are included in an annual survey that the college guidebook publisher Peterson’s conducts of colleges and universities. Colleges report these data in their Common Data Sets, and Peterson’s aggregates them for subscribers. I also examined the average net-price-by-income data that colleges have reported annually to the Department of Education’s Integrated Postsecondary Education Data System (IPEDS) since 2008. These data indicate the funding gaps that low-income students and their families face at these institutions. To be included on the list, the universities had to have charged the lowest-income families an average net price of $12,000 or more, after all grant and scholarship aid was awarded. To see all of the data that I took into consideration when determining that these 41 universities should be on the list, see the appendix.

Here’s how the 41 schools measure up in terms of how much they spend on institutional aid, meet financial need, and charge the lowest-income families:

- Amount of non-need-based aid: The median amount of non-need-based aid the 41 universities awarded in 2023 was about $50 million.

- Share of freshmen receiving non-need-based aid and median amount of non-need-based aid award they received: At the 41 institutions, the median share of freshmen receiving non-need-based aid was 28 percent and they received a median amount of nearly $15,000 each.

- Percentage of financial need met: The median share of financial need that the 41 universities met of their freshmen financial recipients was just 74 percent.

- Average net price the lowest-income freshmen pay: After all grants and scholarships were considered, these universities charged freshmen from families with annual incomes of $30,000 or less a median average net price of about $18,000.

Some readers may take comfort that this report identifies only 41 universities that appear to be steering low-income families to PLUS loans as part of their financial aid leveraging efforts. However, the list does not aim to identify all colleges that are pushing low-income families to borrow PLUS loans. This list, for example, does not include historically Black colleges and universities (HBCUs), which are heavily reliant on PLUS loans to help their students’ parents pay for college. These institutions have been historically underfunded and, compared to the universities on this list, have much less money to devote to financial aid. The omission of HBCUs is not meant to excuse these schools for burdening their students’ families with risky loans. But they are not pushing their students’ parents to borrow PLUS loans to try to rise to the top of the U.S. News rankings.

The list also does not include art schools, which tend to be the country’s most expensive colleges because they require students to buy expensive tools and supplies.7 While these institutions are highly competitive, they are niche, and not representative of higher education as a whole.

And I was conservative in compiling the list, including only universities that appear to be leveraging a great deal of their aid. It is likely that a lengthier investigation would reveal other schools that put low-income students’ families in financial jeopardy as well.

Citations

- For more on the deceptive practice of Parent PLUS loan packaging, see Stephen Burd, Rachel Fishman, Laura Keane, and Julie Habbert et al., Decoding the Cost of College: The Case for Transparent Financial Aid Award Letters (New America and uAspire, June 2018), source; and U.S. Government Accountability Office, Financial Aid Offers: Action Needed to Improve Information on College Costs and Financial Aid, GAO-23-104708 (GAO, 2022), source.

- Marian Wang, Becky Supiano, and Andrea Fuller, “Student Loans, Backed by the Government, Crush Many Families,” ProPublica and The Chronicle of Higher Education, October 7, 2012, source.

- Wang, et al., “Student Loans, Backed by the Government, Crush Many Families,” source.

- Rachel Fishman, The Wealth Gap PLUS Debt: How Federal Loans Exacerbate Inequality for Black Families (New America, May 2018), source.

- Fishman, The Wealth Gap PLUS Debt, source.

- Casey Goldvale, et al., Unrepayable Debt: How Economic, Racial, and Geographic Inequality Shape the Distribution of Parent PLUS Loans (Georgetown Center on Poverty and Inequality, September 2022), 6–9, source.

- Catherine Rampell, “The Most Expensive Colleges in the Country Are Art Schools, Not Ivies,” Washington Post, March 28, 2014, source.

Private Universities

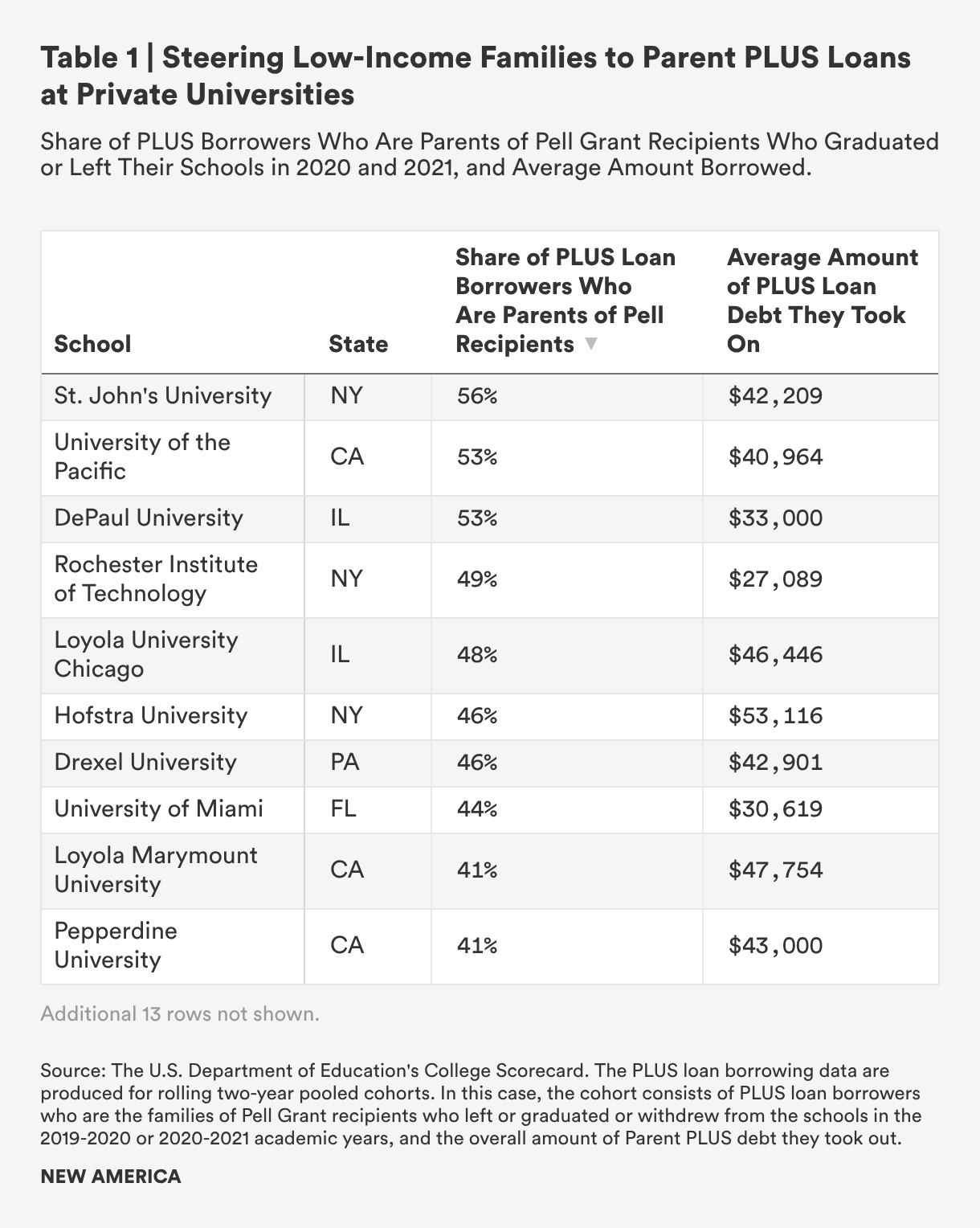

More than 26,000 families who had children who either graduated or left these 23 private universities in 2020 and 2021 borrowed PLUS loans to help pay for college. Nearly 12,000 of them, or 44 percent, were the families of Pell recipients. They borrowed a median debt load of nearly $40,000. Table 1 shows the school-by-school numbers:

Here’s how the 23 private universities stack up in terms of how much they spend on institutional aid, meet financial need, and charge the lowest-income families:

Private University Profile

- Amount of non-need-based aid: The median amount of non-need-based aid the 23 private universities awarded in 2023 was about $61 million. The three schools that gave out the most were St. John’s University, $218 million; Drexel University, $100 million; and Texas Christian University, $98 million.

- Share of freshmen receiving non-need-based aid and median amount of non-need-based aid award they received: At the 23 private universities, the median share of freshmen receiving non-need-based aid was 27 percent and they received about $22,000 each. The three schools that awarded aid to the largest share of non-needy freshmen were the University of Miami, 62 percent (an average of $23,000 each); Loyola Marymount University, 56 percent (an average of $11,000 each); and University of Denver, 54 percent (an average of $22,000 each).

- Percentage of financial need met: The median share of financial need that the 23 private universities met of their freshmen financial recipients was 85 percent. The schools that met the lowest share of financial need were Quinnipiac University, 66 percent; Hofstra University, 71 percent; and Loyola Marymount University, 71 percent.

- The average net price the lowest income freshmen pay: After all grants and scholarships were considered, these 23 private universities charged freshmen from families with annual incomes of $30,000 or less an average net price of nearly $24,000. The schools that charged the lowest-income students the most were Pepperdine University, $36,000; Quinnipiac University, $31,000; and Fordham University, $31,000.

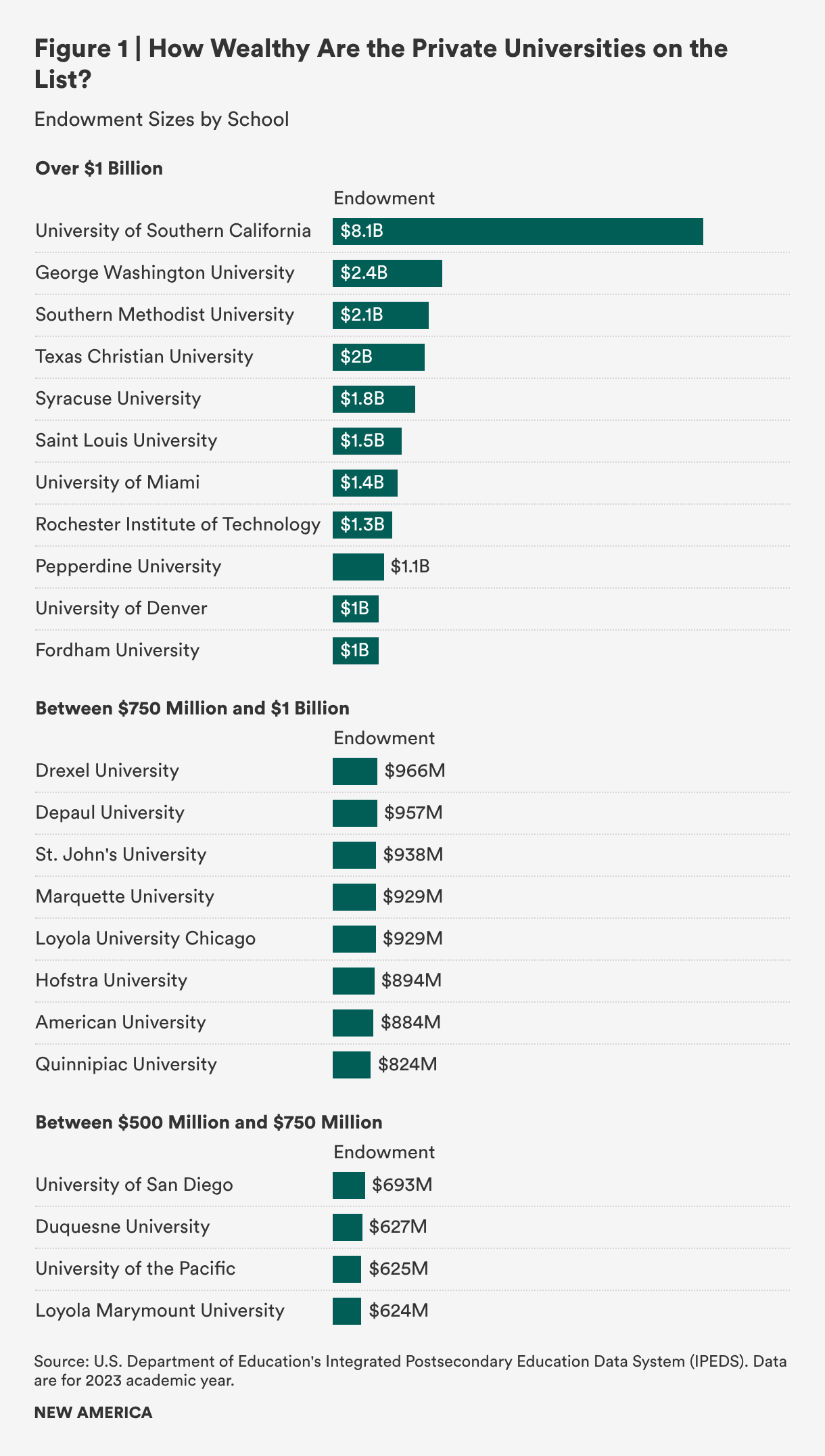

As Figure 1 shows, all the private universities on the list have endowments of $500 million or more. Eleven are among the wealthiest universities in the country, with endowments over $1 billion. Of the remaining 12, 8 have endowments between $750 million and $1 billion, and the remaining ones exceeding $500 million. These schools generally do not engage in financial aid leveraging to keep their doors open or to fill seats. They are doing so to rise in the rankings, increase their revenues, and compete against their rivals.

Over half the private universities on the list have religious affiliations: Nine of the schools are Catholic and four are Protestant. Of the Catholic schools, five are Jesuit institutions. As the journalist and author Neil Swidey wrote in my book Lifting the Veil on Enrollment Management shows, Jesuit schools like Saint Louis University were among the first to become more analytical in their use of data comparing colleges’ success in enrolling students and strategic in their use of financial aid.1 Catholic colleges have at times wrestled with the tension between their historic missions to provide an affordable education to low-income students and the desire to raise their academic profile and compete for higher-achieving students.2

Like Baylor, the Protestant universities on the list have engaged in financial aid leveraging aggressively not only to raise their academic profile but to compete with one another to be considered the top Christian university in the country, the Protestant version of Notre Dame University. For example, the online site Niche in 2025 named Texas Christian University the country’s top Christian college—besting Southern Methodist University, which won the honor the year before. Like Baylor, these schools are leaving the families of Pell recipients with loads of Parent PLUS loan debt many of them are unlikely to be able to repay.

This list also contains some bigger-name, non-sectarian universities—such as The George Washington University, the University of Miami, and the University of Southern California—that have used enrollment management and financial aid leveraging to climb up the rankings and become national institutions. They have followed similar paths as they have sought to rise up the pecking order.

Here’s the story of one of those universities, and another that is trying to follow in its footsteps.

The George Washington University

For most of its history, which goes back to 1821, The George Washington (GW) University was an affordable commuter school that served a diverse group of working adults seeking credentials that would help them advance in their careers—a much different clientele than its tonier neighbor, Georgetown University, enrolled.

That all changed with the arrival of the university’s new president, Stephen Joel Trachtenberg, in 1988. Trachtenberg, the former president of the University of Hartford, immediately set an ambitious course for GW: to be a destination of choice for affluent students who did not make the cut at the nation’s most selective colleges. To accomplish this, he applied lessons he had learned as a senior administrator at Boston University in the 1970s under the tutelage of John Silber, who helped transform BU from a commuter school into a major research university.3 Trachtenberg took those lessons and wrote a blueprint that countless other universities—both public and private—have followed to raise their stature.

Trachtenberg’s goal was to make GW more appealing to an upscale crowd. To carry out that mission, he turned what had been a relatively low-cost institution into one of the most expensive colleges in the country. He believed the higher the price, the more alluring the school would be to the top-end students and families he sought. In a 2015 New York Times article entitled “How to Raise a University’s Profile: Pricing and Packaging,” New America’s Kevin Carey wrote, “Trachtenberg convinced people that George Washington was worth a lot more money by charging a lot more money.”4

And he went on a building spree to provide the kind of amenities that wealthier students crave, such as state-of-the art dormitories and a fancy student union that won the American Institutes of Architects’ highest award. For Trachtenberg, the constant construction on campus signaled the dynamism of the university. “Mr. Trachtenberg understood the centrality of the university as a physical place. New structures were a visceral sign of progress,” Carey wrote. “They told visitors, donors, and civic leaders that the institution was, like beams and scaffolding rising from the earth, ascending.”5

And Trachtenberg opened up the university’s financial aid coffers for the sole purpose of “buying talent,” as he told The Atlantic.6 He operated under the philosophy “that students were more interested in attending a $40,000 school with a $20,000 discount than they were in attending a $20,000 school,” the magazine reported in a profile of Trachtenberg entitled “Meet the High Priest of Runaway College Inflation.”7

Although it has been many years since Trachtenberg retired as president of George Washington University, the school is still “buying talent.” In 2023, 29 percent of GW freshmen received non-need-based aid, averaging over $23,000 each. At the same time, the university charged the lowest-income students an average net price of more than $21,000.

According to the Education Department’s College Scorecard data, 722 families with children who either graduated or left GW in 2020 and 2021 borrowed PLUS loans to help pay for college. Of those, 261, or 36 percent, were the families of Pell recipients. They carried a median debt load of $26,000.

Trachtenberg’s vision of making GW into a popular destination for affluent students who did not make it into the nation’s most selective colleges has panned out. But the changes were made on the backs of the low- and lower-middle-income students who had once been the lifeblood of the university.

St. John’s University

It may be surprising to learn that the selective college that has awarded the most non-need-based aid in each of the past 15 years is St. John’s University in Queens, New York, which is still considered a commuter campus. The university, which spent $218 million on non-need-based aid in 2023, primarily serves students from New York City’s five boroughs and Long Island.

St. John’s leaders, however, have long had higher aspirations for the university, which have been fueled by the school’s athletic prowess. The school sports 17 NCAA Division 1 teams, none more famous than the men’s basketball team. The Red Storm, now coached by the infamous Rick Patino, has appeared in 31 NCAA tournaments (including in 2025).

St. John’s president, Rev. Donald J. Harrington, started to make those aspirations a reality in 1999, by breaking ground on its residence village, which housed the school’s first five dormitories.8 Speaking to The New York Times in 2001, Harrington said that the new dorms were just a start: “We see ourselves as being a national university.”9

Father Harrington followed GW’s blueprint closely—jacking up tuition, going on a building spree, and, of course, buying higher-achieving students from outside the boroughs. While the vast majority of students still commute to the school, St. John’s has built a large residential presence. Last year, 2,500 students lived in residential facilities on or near campus, and they came from 45 states and 106 countries.10

St. John’s traditional low- and lower-middle-income clientele have paid a high price for these changes. In 2023, the university charged freshmen from families with annual incomes of $30,000 or less an average net price of nearly $23,500, leaving their parents with little choice but to borrow PLUS loans.

According to the Education Department’s College Scorecard data, 3,068 families who had children who either graduated or left St. John’s in 2020 and 2021 borrowed PLUS loans to help pay for college. Of those, 1,707, or 56 percent, were the families of Pell recipients, and they assumed a median debt load of more than $42,000.

St. John’s use of the Parent PLUS loan program has helped fuel its transformation. Today, the families of former St. John’s students carry about $633 million in outstanding Parent PLUS loan debt, third among all selective colleges in the country, public or private.

Harrington stepped down as president of St. John’s in 2013, in the midst of a financial scandal at the university. But he made clear that his aspirations for the school remained sky-high. “St. John’s has been transformed and stands today a truly world-class global university,” he wrote to the universities’ trustees at the time.11

Citations

- Neil Swidey, “Reign and Ruin: The Rise of Enrollment Management and the U.S. News College Rankings,” in Lifting the Veil on Enrollment Management: How a Powerful Industry is Limiting Social Mobility in American Higher Education, ed. Stephen J. Burd (Harvard Education Press, 2024),15–19.

- For more on the tensions some Catholic colleges have experienced regarding their competing enrollment priorities, see Becky Supiano, “Catholic Colleges Work to Maintain Access as Their Profiles Rise,” Chronicle of Higher Education, October 4, 2009, source.

- Kevin Carey, “How to Raise a University’s Profile: Pricing and Packaging,” New York Times, February 6, 2015, source.

- Carey, “How to Raise a University’s Profile,” source.

- Carey, “How to Raise a University’s Profile,” source.

- Julia Edwards, “Meet the High Priest of Runaway College Inflation (He Regrets Nothing),” The Atlantic, September 2012, source.

- Edwards, “Meet the High Priest of Runaway College Inflation,” source.

- St. John’s University, “Twenty Years Ago: Residence Halls Usher in a New Era for St. John’s,” August 30, 2019, source.

- Samuel Weiss, “St. John’s Works to Shake Its Commuter School Image,” New York Times, May 2, 2001, source.

- St. John’s University, “Fast Facts: Fall 2024,” source.

- Wendy Ruderman, “Amid Pending Investigation, President of St. John’s Says He Will Retire,” New York Times, May 3, 2013, source.

Public Universities

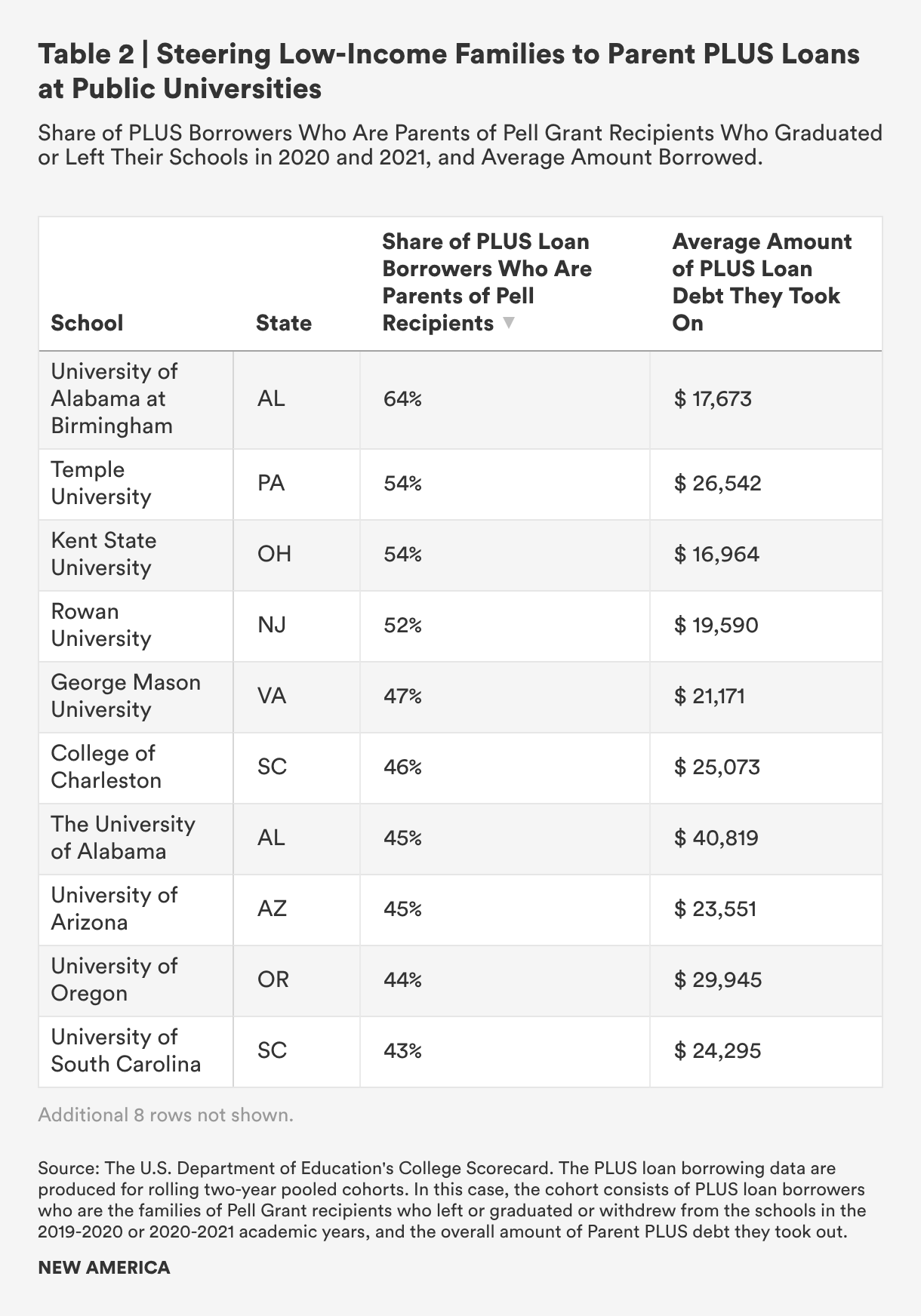

About 46,000 families who had children who either graduated or left the 18 public flagship and research universities on the list in 2020 and 2021 borrowed PLUS loans to help pay for college. Nearly 21,000 of them, or 46 percent, were the families of Pell recipients. They carried a median debt load of more than $21,000. Table 2 gives the school-by-school numbers:

Here’s how the 18 public universities stack up in terms of how much they spend on institutional aid, meet financial need, and charge the lowest-income families:

Public University Profile

- Amount of non-need-based aid: The median amount of non-need-based aid the 18 public universities awarded in 2023 was about $36 million. The schools that gave out the most were the University of Alabama, $185 million; the University of Arizona, $152 million; and Auburn University, $66 million.

- Share of freshmen receiving non-need-based aid and median amount of non-need-based aid award they received: At the 18 public universities, the median share of freshmen receiving non-need-based aid was 29 percent and they received a median amount of about $7,500 each. The two schools that awarded aid to the largest share of non-needy freshmen were the University of Arizona, 46 percent (an average of $14,000 each); and the University of South Carolina, 42 percent (an average of $7,000 each).

- Percentage of financial need met: The median share of financial need that the 18 public universities met of their freshmen was just 61 percent. The schools that met the least need were the University of Cincinnati, 46 percent; the University of Oregon, 47 percent; and Clemson University, 48 percent.

- Average net price the lowest-income freshmen pay: After all grants and scholarships were considered, these 18 public universities charged freshmen from families with annual incomes of $30,000 or less an average net price of more than $14,000 in 2023. The schools that charged the lowest-income students the most were Temple University, $23,000; the University of Alabama, $19,000; and Auburn, $16,000.

As I reported in Lifting the Veil on Enrollment Management, state disinvestment and institutional status-seeking have worked hand in hand over the last two decades to encourage public universities to adopt the enrollment management strategies of private colleges.1 With the help of enrollment management consultants, many public universities have hiked up their prices and provided tuition discounts and merit scholarships to lure affluent out-of-state students with good grades and standardized test scores to their campuses to increase their revenue and climb up the rankings. The allure of these students is obvious: Even with discounts they pay more than in-state students. Competition for these students is stiff, so these universities are willing to pay more for them.

But public universities’ use of financial aid leveraging is not just about the money. They are also seeking greater prestige. Schools like the University of Alabama and Clemson University became fixated on climbing the U.S. News national rankings, where public research universities compete fiercely with private ones for top spots.2

To be sure, many public universities haven’t embraced enrollment management and don’t leverage their institutional financial aid in this way. But these schools tend to be located in the declining number of states that have kept their public universities affordable, such as California, Florida, New York, North Carolina, and Washington. None of the public universities on the list hail from those states.

Two-thirds of the public universities on the list are from the Midwest and the South, the regions of the country where schools have embraced enrollment management the most. Competition among the public flagship and research universities in the Midwestern states is intense. In addition, Midwestern universities are in states where the number of high school graduates is shrinking so they use their financial aid strategically to shop for students around the country.

There is no similar shortage of students in the South. The Southern public universities on the list embraced enrollment management to make up for severe state budget cuts, to better compete with one another, and to build national brands. The University of Alabama’s aggressive efforts to become a nationally renowned institution forced other public flagship and research universities in the region to respond. Most of the Southern public universities on the list followed Alabama’s lead. One, which was led by a fierce advocate for public higher education, initially resisted. The next section focuses on the transformation of the University of Alabama, and how it affected two other Southern public research universities.

University of Alabama

For much of its history, Alabama’s flagship university was committed to providing a low-cost education to the white citizens of the state (the first Black students were not admitted until 1963 and only were able to enter the university under the protection of the National Guard). In turn, the vast majority of the university’s funding came from the state. But in the 1990s, the state’s commitment wavered. Starting in 1995, Republican Governor Fob James reduced state funding for higher education in order to steer more money to Alabama’s struggling elementary and secondary schools. This policy led to a substantial reduction in the share of the state budget devoted to financing higher education.3

The university went through multiple rounds of cost cutting. Morale suffered as the university began reducing and eliminating academic departments. Meanwhile routine maintenance around campus was delayed, as some buildings and facilities fell into disrepair.

University leaders realized that they needed to forge a new path, largely independent of the state, to save it from stagnation.

In 2003, the University of Alabama’s board of trustees chose Robert E. Witt, the former business school dean at the University of Texas at Austin and president of the University of Texas at Arlington, to be its new president. The trustees asked him to make the institution into a national brand that could compete with research universities around the country. Hitting the ground running, Witt laid down a challenge to the admissions office: “Recruit top student scholars with the same fervor as top athletic prospects, and look beyond the state’s borders to find them,” according to a paper that several university officials wrote for the journal of the American Association of Collegiate Registrars and Admissions Officers in 2010.4

Witt’s plan, which also called for expanding the university’s enrollment from 19,000 to 28,000 over a 10-year period, energized the admissions staff.5 The ambitious plan promised to change the trajectory of the institution. But it also risked leaving the school’s traditional constituencies behind.

For Witt, recruiting top students from “beyond the state’s borders” was the key to his plan, as out-of-state students paid as much as three times more than in-state ones. To carry out this mission, the University of Alabama set up full-time regional recruiters in nearby states, including Florida, Georgia, and Texas, and eventually spread them nationwide. Just which out-of-state students the University of Alabama’s enrollment management team, then led by Roger Thompson, was targeting soon became clear. In a 2005 article in The Atlantic, Mathew Quirk wrote of a presentation that Thompson and his colleagues delivered at an admissions conference that year:

Two members of the University of Alabama’s enrollment management team demonstrated how, in their campaign for out-of-state prospects, they overlaid income data from the U.S. Census on maps of high schools to target wealthy students…After the presentation, I sat down with Roger Thompson and asked him how he approached recruiting at rich private secondary schools. “Oh, if you’re in enrollment management, these schools are fantastic!” he said. “There are some kids there that we’ll buy. The National Merit kids, they’re going to get a full ride. But if you’re sitting at a private high school in Florida, where they pay twenty grand to go, we don’t even bring financial aid material. What’s the point? You don’t even need to talk about cost.”6

Witt and Thompson knew that enrolling much larger numbers of wealthy students would bring in more revenue the university could use to help pay for its costly transformation and increase the chances of getting lucrative donations.

But how did the University of Alabama lure more well-to-do students to Tuscaloosa? It followed the same blueprint that Trachtenberg used to help transform George Washington University. These tactics included four key moves.

A. Jacking Up Tuition

Soon after arriving in Tuscaloosa, Witt concluded that the University of Alabama was not expensive enough. As a result, he began to raise tuition by $1,000 a year. “Our thinking was, if we begin to notice a softening in applications, acceptances and/or matriculation, we’ll know that we need to start backing off a little,” he told Josh Mitchell, The Wall Street Journal reporter who wrote the 2021 book The Debt Trap, which includes a chapter focusing on the University of Alabama’s quest for prominence.7 Instead of dropping off, applications increased, and the cost of attendance continued to rise. Ten years after Witt introduced his plan, the University of Alabama had doubled its tuition and fees for both in-state and out-of-state students.8

It may seem counterintuitive that a university would attract more students by raising its prices. But upscale students and families tend to equate low costs with low quality. Generally, affluent students would rather go to an overpriced college than a bargain one. George Washington University, for example, reached the height of its popularity when it was the most expensive university in the country.

Bringing in more students and charging more helped the universities pay for their plans to upgrade their campuses.

B. Going on a Building Spree

When Witt started his presidency at the University of Alabama, he inherited a backlog of maintenance projects. But that was just the start. According to The New York Times, the university put up 64 new buildings during the decade Witt served as president, including 10 new luxury dorms and a cutting-edge recreation center.9 The Washington Post reported in 2016 that the University of Alabama’s building spree included “an opening or renovation every 90 days.”10

Like Trachtenberg before him, Witt understood that that the near-constant construction sent a message to the wealthy students and families he was trying to attract that the university was on the rise. Witt also wouldn’t spare any expense to make sure that the campus was as attractive as possible. As Mitchell wrote in The Debt Trap, he looked at “The Happiest Place on Earth” as a guide for the university’s landscaping. Mitchell wrote, “Research indicated that many families decide whether to apply to a school within 20 minutes of arriving on its campus. First impressions were everything. Witt concluded the grounds had to be pristine. To lead the grounds crew, he hired a retired Air Force colonel, who went to Disney World to study how the theme park managed its grounds.”11

C. Making Money off Student Aid

While raising prices and upgrading the campus made the University of Alabama more attractive to the affluent students and families it was courting, the institution was able to clinch the deal only once it overhauled its financial aid policies so that it could woo these students. To do so, the university turned to the top enrollment management firm at the time, Noel Levitz (which Baylor was working with at this same time).

When the University of Alabama hired Noel Levitz, enrollment management was still largely the province of private colleges. For generations, public universities had been generally accessible for students and did not award much of their own financial aid. For its part, the University of Alabama awarded less than $10 million of institutional aid in 2003. A decade later, the university spent $85 million on non-need-based aid alone, more than any other selective public university at the time. By 2023, the university’s non-need-aid budget was up to $185 million, second only to Arizona State University, which enrolls far more students than Alabama.

Aid to non-needy students fueled the University of Alabama’s enormous growth, with its enrollment nearly doubling over the last two decades. Out-of-state students flooded into the institution and now substantially outnumber in-state ones. With recruiters, armed with generous scholarships, spread throughout the country, the university has succeeded in luring high-achieving students who may never have considered moving to the Deep South for college.

In 2017, the Chicago Tribune was shocked to learn that more than 1,600 Illinois students were attending the flagship campus in Tuscaloosa, up from 150 a decade before.12 “And Alabama isn’t just taking any students; many are among Illinois’ brightest,” the newspaper reported. “More than 700 Illinoisans from 193 cities made the president’s and dean’s lists at Alabama, earning at least a 3.5 GPA for fall 2017.” According to the newspaper, these students “are meeting one another in classes, clubs and sororities, and through campus group chats.”13

But the University of Alabama recruiters were not only looking for top scholars who would cost them full tuition scholarships. They were also seeking full-pay students who could be swayed to study in Tuscaloosa with only a relatively small discount. In 2019, researchers from the University of California at Los Angeles and the University of Arizona looked closely at the out-of-state high school visits University of Alabama recruiters had made two years earlier. Their study found that “these visits focused on schools in affluent communities, with visited schools having a much higher percent of white students than nonvisited schools.”14 In addition, the researchers discovered that the university had “made 935 visits to out-of-state private high schools, more than double the total number of in-state recruiting visits.”15

The researchers—Ozan Jaquette and Crystal Han in California and Karina Salazar in Arizona—also showed just how lucrative Witt’s mandate “to look beyond the state’s borders” had been for the University of Alabama. They found that n 2002–03, the university enrolled just 626 out-of-state freshmen, and it had net tuition revenue of $105 million. Six years later, the number of freshmen from other states had grown to 1,895, and net tuition revenue increased to $225 million. By 2017–2018, the university enrolled a whopping 5,001 out-of-state freshmen and raked in $493 million in net tuition revenue, according to an Inside Higher Ed article about the researchers’ work.16

While its efforts to gain greater national prominence paid great dividends to the University of Alabama, its transformation was made largely on the backs of its former constituencies, who benefitted little from the university’s generosity with tuition discounts and scholarships to non-needy students.

D. Pushing PLUS Loans

In examining the allegations of Parent PLUS loan steering at the University of Alabama, it is critical to examine the period between 2010 and 2016, when the school pushed financial aid leveraging into a much higher gear. In these years, the university accelerated its use of non-need-based aid to get the students it desired, while slamming the brakes on meeting the financial need of its student aid recipients.

The University of Alabama put its out-of-state student recruiting strategy into overdrive after suffering even more severe state budget cuts as a result of the financial crisis and economic recession that devastated the country at the end of the aughts. From 2010 to 2016, the university tripled its spending on non-need-based aid, from $45 million to $146 million, the highest amount spent by any public university at the time.

But while the University of Alabama lured more affluent students to its campus, it also ratcheted up its recruiting of low-income students, just as Baylor had done during this time period. The University of Alabama increased the share of Pell Grant recipients in its student body from 17 percent in 2009 to 21 percent a year later. They made up at least a fifth of the class for the next five years.

Normally college access advocates would applaud a school for enrolling so many low-income students. However, it is important to remember that under the financial aid leveraging programs that enrollment management firms market to colleges, institutional aid is not used to meet financial need. In fact, covering low-income students’ financial need is considered inefficient and wasteful. The aim, after all, is for universities to reel in the students they most desire, without spending a dollar more than is necessary.

At the University of Alabama, the average amount of financial need that the school met of its student aid recipients did in fact drop substantially in the years after it started working with Noel Levitz. In the decade after Witt had introduced his plan, the average share of need that the University of Alabama met plummeted, from 73 to 53 percent.17

With the university meeting substantially less of their financial need, low- and lower-middle-income students were left with larger and larger funding gaps. Students from families making $30,000 or less paid an average net price of about $22,000, equal to three-quarters of their parents’ yearly income.18 As a result of the university’s embrace of financial aid leveraging, these families were left with little choice but to take out PLUS loans if they wanted to send their children to the school.

Indeed, PLUS loan borrowing soared at the University of Alabama during this period. Between 2010 and 2016, the number of families borrowing Parent PLUS loans to send their children there grew by 60 percent, to 3,402, and the amount they borrowed doubled, to $96 million. (Back in 2002, before the university embraced financial aid leveraging, only 595 families borrowed, and their total was lower, the equivalent of $8.5 million in 2025 dollars.) Today, nearly 13,000 families of former University of Alabama students owe about $723 million in outstanding Parent PLUS loan debt, the second biggest total among all colleges in the country, public or private.19

The University of Alabama, like Baylor, relied heavily on Parent PLUS loans to help fuel its ambitions. But, as Mitchell writes in The Debt Trap, this strategy left many victims in its wake: “Alabama had become the fastest-growing public university in America. It also represented the avarice and indulgence that define today’s universities. It was in the thick of a construction and hiring boom—intended to improve the quality of education and the student experience. The school achieved that goal,” he wrote, “but it was financed on the backs of students and their parents, who turned to federal student loans, with no assessment of the borrowers’ ability to repay their mountainous debt.”20

But just how much harm these institutions caused did not start to become clear until the U.S. Department of Education started publishing institution-by-institution Parent PLUS loan data in its College Scorecard in January 2021.

It is eye-opening to see just how close the University of Alabama’s data in the Education Department’s College Scorecard is to Baylor’s. In its exposé of Baylor, The Wall Street Journal cited College Scorecard data showing that 47 percent of PLUS loan borrowers with kids who graduated or withdrew from Baylor in 2018 and 2019 were the parents of Pell Grant recipients.21 They incurred a median of $43,500 in PLUS debt while their children were in college. At the University of Alabama, 45 percent of PLUS loan borrowers with children who graduated or withdrew from the school in 2020 and 2021 were the parents of Pell Grant recipients. They borrowed a median of $40,819 in Parent PLUS debt while their children were in college.22 Because of its size, however, the University of Alabama has put many more low-income families into financial jeopardy than Baylor did.

Like Baylor, the University of Alabama has recently created a scholarship program for low-income students to help cover their tuition and fees. Under the Alabama Advantage Scholarship, Pell Grant recipients can receive up to $5,000 to cover any remaining in-state tuition, after all other grants and scholarships are awarded.23 Unlike Baylor, however, University of Alabama officials have never acknowledged any fault for their policies. The University of Alabama’s lack of contrition is frustrating to parents who are buried in PLUS loan debt and see no end in sight.

Take Grindl Weldon, a single mom and teacher from a rural part of Northern Alabama. According to The Hechinger Report, Weldon, with the help of federal student aid, was able to pay tuition for her daughter Caitlin to attend the University of Alabama. However, she needed help to cover room and board, so she borrowed $25,000 in PLUS loans. “I knew I was getting myself into debt, but what were my choices?” she said. “I felt like her future was at stake. What would any mama do?”24

Weldon already had $25,000 of her own student debt. When she found that her combined monthly payments would grow to over $500, she said she almost collapsed. She does not think she will ever be able to pay off her debt. She hopes other low- and lower-middle-income PLUS loan borrowers will come forward to tell their stories. “Maybe if more people knew they weren’t the only ones, something would change,” she said. “That’s what I am hoping.”25

Auburn University

Perhaps no school felt more of an impact from what was happening at the University of Alabama than Auburn University, its closest competitor.

In the 1990s, Auburn was the hot public university in Alabama, the school of choice for many of the state’s top students. But at the turn of the century, the university became mired in controversy and mismanagement. The board of trustees fired a popular president and replaced him with a series of interim leaders. Soon afterward, the university’s accreditor put the school on probation because of concerns about how the board was operating.26 Then allegations of academic fraud involving the football team roiled the campus.27 “This was about as dysfunctional a university as anywhere in America,” Wayne Flint, a retired history professor, said at the time.28

To add insult to injury, Auburn’s chief rival was on the rise. The University of Alabama’s success in attracting nonresident students with good grades and test scores helped raise its stature, making it more attractive to the state’s best students. An outside consulting company warned Auburn officials in 2006 that “the U of A’s aggressive recruitment of high academic achievers could reduce AU’s share of strong in-state students and damage AU’s reputation.”29

Enter Jay Gogue, the former president of New Mexico State University and the University of Houston, who became Auburn’s president in 2007. Borrowing a page from the blueprint that Robert E. Witt was following at the University of Alabama, Gogue directed the university’s admissions staff to more aggressively pursue “high-performing students” and use non-need-based “merit” aid to get them. “There’s going to be a lot of emphasis to raise private money to support scholarships,” Gogue said at the time.30

Before Gogue’s arrival, Auburn had not been a player in the merit-aid arms race or engaged in financial aid leveraging. In fact, in 2006, the university spent less than $100,000 on non-need-based aid. “Alabama’s done great with scholarships,” Wayne Alderman, Auburn’s then-dean of enrollment services, told the Tuscaloosa News in 2008. “Auburn traditionally has not put much money into scholarships but some of that is, we’ve always been able to attract a pretty good student body. Still, we have to be more competitive with scholarships.”31

Gogue agreed that Auburn had to become more competitive. In his first year, Auburn spent about $13 million on non-need-based aid. That expenditure allowed the university to provide discounts, averaging about $6,000 each, to 11 percent of freshmen who lacked financial need. Within four years, the university had tripled its non-need-aid budget to $38 million, allowing it to provide an average discount of $7,500 to about one-quarter of its non-needy freshmen. In 2023, the university awarded $66 million to non-needy students, with one-third of freshmen receiving an average discount of more than $9,000.

Increased competition from the University of Alabama pushed Auburn to engage in financial aid leveraging. But it has taken a more modest and focused approach than its rival in Tuscaloosa. While Auburn has sought to increase its academic profile and enroll more high-achieving students from out of state, more than half of the student body continues to come from Alabama.

Auburn’s goal has been to be nationally “recognized for its academic excellence and exceptional student experience” while “maintaining its position as Alabama’s highest-ranked university,” according to university officials.32 The University of Alabama’s rise threatened Auburn’s standing. Between 2007 and 2015, the University of Alabama bested its rival in the U.S. News rankings in all but one year.33 But Auburn fought back, and a change in the rankings methodology in 2018 that sought to reward colleges for their record in graduating Pell Grant recipients sent the University of Alabama into a tailspin from which it has not recovered.34 In the 2025 U.S. News rankings, the University of Alabama not only trails Auburn but also its own branch campus in Birmingham.35

For its part, Auburn is among the country’s least socioeconomically diverse public universities. In the first five years of Gogue’s presidency, the share of Pell Grant recipients in the student body grew from 13 percent in 2009 to 18 percent in 2010 and 2011. That was the high watermark. Today, they make up only 12 percent of students. Meanwhile, the share of Black students at Auburn has plummeted, from 8 percent of the student body in 2010 to just 4 percent in 2023, even before the Supreme Court outlawed the use of affirmative action in college admissions. While the overall student population has grown by nearly 7,000 over that period, the university enrolls almost 500 fewer Black students annually than it did in 2010.

“A lot of the times, I’ll look at my roll sheet and we’ll have more students from Chicago, Boston, or Boulder, Colorado, than we’ll have from the local communities around us,” Keith Hébert, a public history professor at Auburn, told Inside Higher Ed in 2020. “Some of that is we’re trying to become a robust research university. But there are talented African American students in our region that we don’t seem to be putting effort into recruiting.”36

But, truthfully, many low- and lower-middle-income students are likely better off not going to Auburn. Since 2008, the school has charged freshmen from families with annual incomes of $30,000 or less an average net price of about $19,000. With funding gaps that large, these families have had little choice but to borrow PLUS loans to send their children the school.

According to the Education Department’s College Scorecard data, nearly 1,700 families who had children who either graduated or left Auburn in 2020 and 2021 borrowed PLUS loans to help pay for college. Of those, 662, or 40 percent, were the families of Pell recipients. They took out a median debt load of more than $41,000, nearly $500 more than their counterparts at the University of Alabama.37

The competition between Auburn and the University of Alabama to be the state’s highest ranked university has come at a very high cost for low- and lower-middle-income students in the state. By leveraging nearly all of their financial aid to attract affluent students, these institutions have become prohibitively expensive for everyone else. In other words, the status wars have served no greater public purpose and have left many of the families of the universities’ least privileged students in financial distress.

Louisiana State University

While Auburn and other Southern public universities followed in the footsteps of the University of Alabama, Louisiana State University resisted that path—at least at first.

In 2013, Louisiana State University’s Board of Supervisors chose a crusader for public higher education to be the next president of the LSU System and chancellor of its flagship campus. F. King Alexander came to Louisiana State after seven years as the president of California State University at Long Beach, one of the most racially and socioeconomically diverse colleges in the country. There, Alexander had seen the power of public colleges and universities to transform lives and increase social mobility.

Alexander is a firm believer in “the ideology that higher education is a public good that benefits society as well as the individual,” as The Washington Monthly reported in a 2015 profile entitled “Can This Man Save the Public University?”38 Alexander had no interest in following the University of Alabama’s example. “Universities need to quit worrying about U.S. News and prestige and start worrying about their mission,” he told The Hechinger Report in 2019. “I’ve got way too many of my colleagues that are chasing things that mean nothing. They end up reducing opportunities that they are supposed to be providing for their state.”39

Alexander’s willingness to fight for what he believed in was sorely tested at Louisiana State. Year after year, he went to battle with Governor Bobby Jindal over proposals to slash higher education spending. Jindal, then a darling of conservative Republicans and an aspiring GOP presidential candidate, repeatedly proposed slashing higher education spending to close massive state budget deficits, which started after he signed into law the largest tax cuts in the state’s history. Between 2012 and 2019, per-student funding at Louisiana’s public colleges and universities dropped by almost 38 percent, the largest reduction of any state but Arizona. As a result, the average tuition and fees at the state’s four-year public universities nearly doubled.40 As bad as that was, it may have been far worse had Alexander not fought so hard.

Alexander believed that it was essential for state university leaders to stay in the arena and go to battle for public higher education and the opportunities these institutions provide low- and lower-middle-income students and students of color. But he recognized that it was becoming a lonely fight, as other public university leaders in the South were looking to embrace enrollment management and financial aid leveraging. “Unfortunately, I’ve got a lot of my colleagues who are more apt to just throw in the towel and say, ‘Yeah, the states are getting out, we just have to be more creative,’” he told The Chronicle of Higher Education during a budget battle in 2015.41

Alexander’s main priority was to open Louisiana State’s doors wider to students who had been historically excluded. Instead of sending his admissions officers around the country to seek out wealthy white suburban students wherever they could find them, he directed them to find Black, Hispanic, and rural students within the state who could thrive at the flagship.42

Before he could achieve his goal, Alexander needed to change the academic criteria required to be admitted to the institution. When he arrived at Louisiana State, applicants were judged by two numbers, their GPA and ACT scores. Anyone who did not score at least a 22 on the ACT would be rejected.43

Alexander felt that the policy was discriminatory because students of color and many rural students do not have the preparatory advantages of more wealthy students and generally do not score as well as more affluent white students on standardized tests. He hired a new chief enrollment officer, Jose Aviles, to help him transition the university to holistic admissions, so that the school could get a more complete picture of its applicants. “We deepened what we understand as merit, who deserves the opportunity to participate,” Aviles recounted to The Hechinger Report in 2019. “If you’re just selecting students on board scores, those things alone are not enough to determine whether a student can be successful on your campus or not. Resilience or grit, students who are going to get up every day no matter how many times they are knocked down, you can look for that.”44 Alexander and Aviles also sent recruiters into every county (aka parish) in the state and increased scholarship opportunities.

These efforts paid off. In his last five years at Louisiana State, Alexander said, the university increased its enrollment of Black students by 63 percent and Hispanic students by 92 percent.45 During this period, he noted, LSU also saw increases in the graduation rates of Black, Hispanic, veteran, and first-generation students.46 Alexander believed that these policies were not only morally right, but fiscally imperative, because the population of traditional white students is shrinking, while minority populations are growing. “If we don’t pay attention to demographic trends, many of our institutions are going to be left out in the cold for decades,” he told The Hechinger Report.47

But Alexander’s efforts ran into fierce opposition from older Louisiana State alumni and parents of private high school students in Baton Rouge and New Orleans, as well as some board members and state officials. Critics accused Alexander of “dumbing down” the university, and he received a threatening private message warning him to “stop darkening our LSU.”48 Meanwhile, reports that Democratic presidential candidate Hillary Clinton had considered Alexander for a spot in her cabinet, as education secretary, did not win Alexander many friends in the conservative state of Louisiana.49

All of these fights took their toll, and the president and chancellor’s opponents had their knives out. In 2019, Alexander announced that he was stepping down and moving to the seemingly friendlier terrain of Oregon State University.50 Reporting on Alexander’s impending departure, LSU’s student newspaper noted that the chancellor “came into power as an outsider, without the support of Jindal,” and his “outsider status never evaded him.”51