Part III: The PLUS Loan “Fix”

Given the massive evidence of state-sponsored discrimination and resulting wealth disparities, all leading to low-income Black households being disproportionately burdened by Parent PLUS loans, what did Congress and the federal government do? It did essentially nothing. And so the problem continues to grow.

In 2013–14, when the Education Department revisited the Parent PLUS regulations, the adverse credit history check was one of the issues different stakeholders, including colleges and universities, student groups, and consumer advocates, tried to fix. Though the Department did not have the legal standing to revert completely to the pre-2011 credit standard, it came up with a middle-ground solution that instituted a de minimus amount to the check. In this case, total debts with adverse conditions such as 90-day delinquency must be over $2,085 (pegged to inflation in 2015). This resulted in an overall slightly weakened regulation compared with what had been the standard.

This compromise was hardly satisfying to those involved. On the one side, HBCUs had already experienced huge losses of revenue and students. On the other, consumer advocates remained concerned that low-income parents were still being offered loans when they had no ability to repay them, with powerful governmental collection tactics, such as garnishing Social Security and seizing tax refunds, looming in the background.

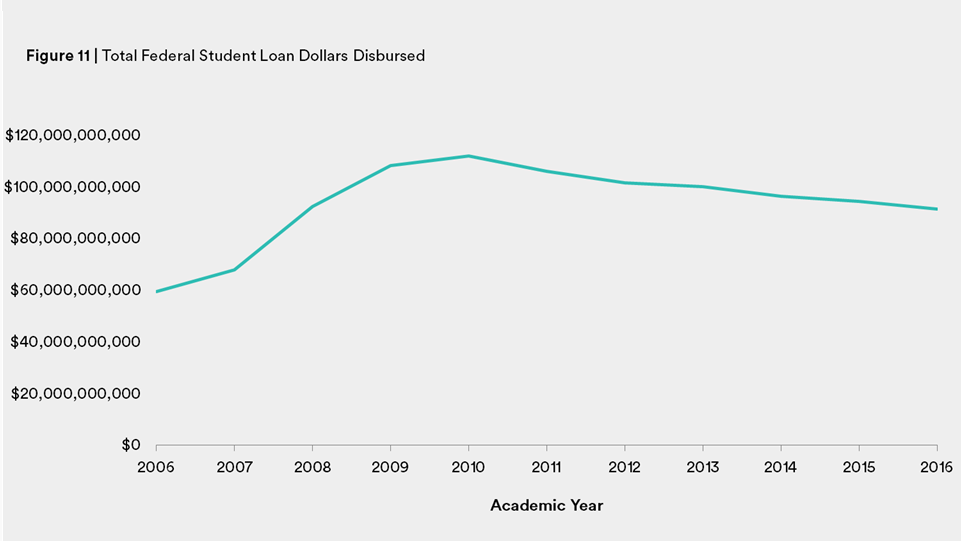

Despite these significant issues, Parent PLUS loan borrowing has increased even while all other federal student loans have been decreasing, except for Graduate PLUS loans. According to Education Department disbursement and recipient data, over the past decade there has been enormous fluctuation and growth in the federal student loan program.1 In academic year 2006–07, $59.6 billion in federal education loans were disbursed (See Figure 11). This includes subsidized, unsubsidized, Parent PLUS, and Grad PLUS loans. The disbursements hit an all-time high at $111.9 billion in 2010–11, which was both the height of the Great Recession and, for largely demographic reasons, the year when student enrollments peaked. As the economy recovered and enrollment declined, total yearly loan disbursements have fallen every year. In the most recent year of available data, academic year 2016–17, the total was $91.3 billion.

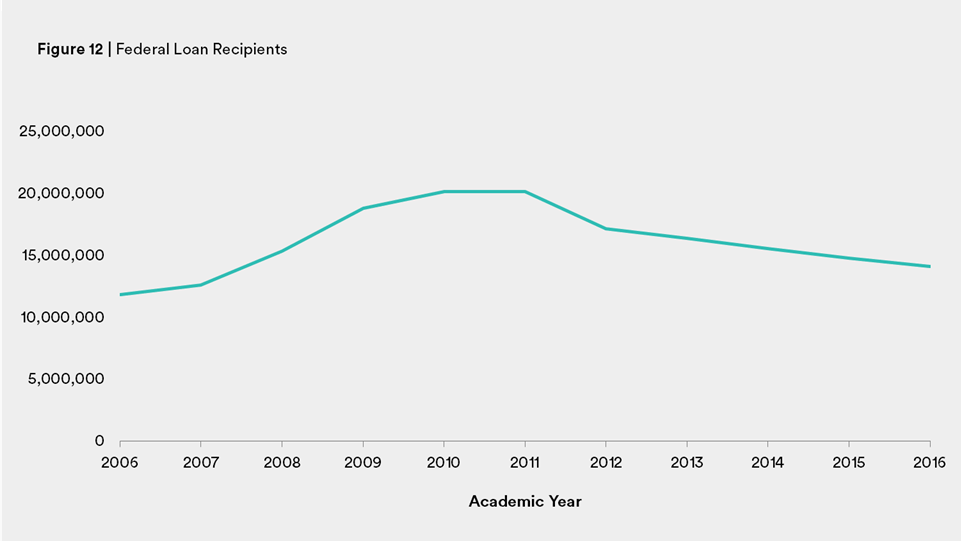

In terms of loan recipients, the pattern has been similar. In 2006–07, there were 11.8 million federal education loan recipients (See Figure 12). Recipients peaked during 2011–12, at 20.1 million borrowers. In 2016–17, that number fell to 14.1 million recipients.

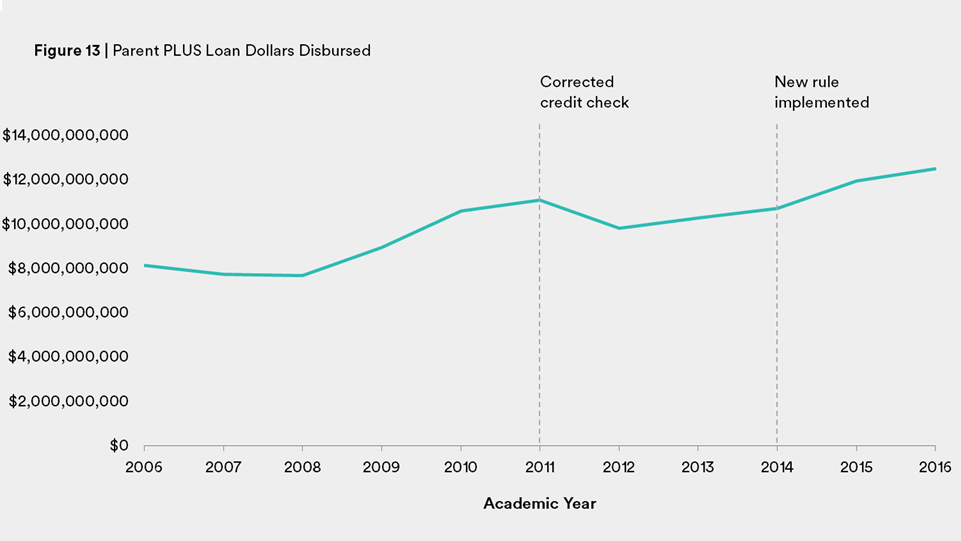

Yet during the same period, Parent PLUS loans have grown in terms of yearly disbursals. In 2006–07, $11.1 billion in Parent PLUS loans were disbursed (See Figure 13). After the Department made the credit change, the disbursal fell to $9.8 billion in 2012–13. But once the new rule was implemented in 2014–15, the yearly disbursals recovered. Last year, Parent PLUS loans experienced their highest yearly disbursement yet, $12.4 billion.

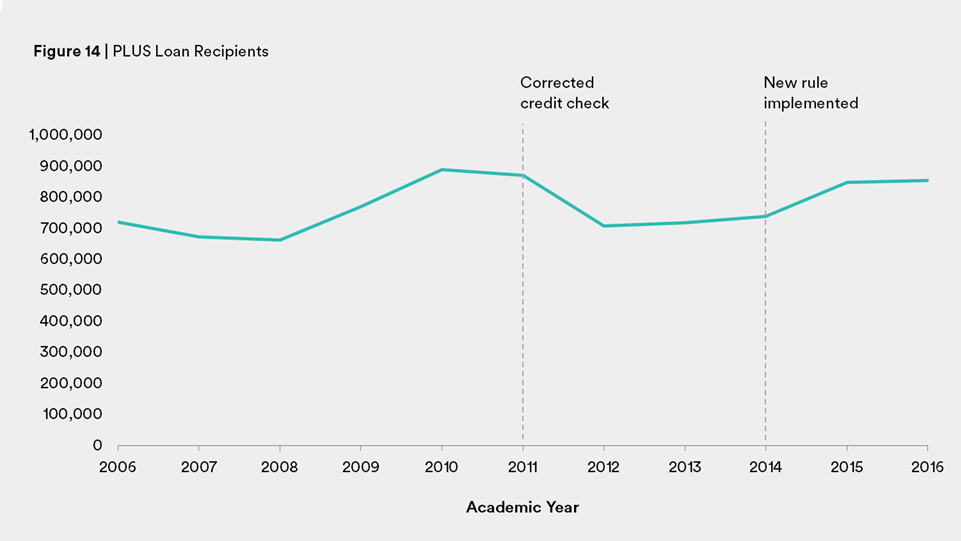

The number of Parent PLUS recipients has followed a similar pattern to that of all student loans, though the decline in recipients has not been as steep. In 2006–07, there were approximately 720,000 Parent PLUS recipients (See Figure 14). In the lead up to the credit check change in 2011–12, there were about 870,000 recipients. One year later, after the Department changed the credit check, there was a decline to approximately 707,000 recipients. Since the new credit check regulation has been implemented, the number of recipients has largely recovered and stands at 854,000.

Since the new check was put into place, Parent PLUS loan volume in terms of dollars has more than recovered. While there is still a slight difference in the number of recipients pre- and post-credit check, higher education enrollments have been declining slightly since the height of the recession, which may help explain the downward trend.

Citations

- All disbursement and recipient data were gathered using New America’s Higher Ed Index, which uses U.S. Department of Education Federal Student Aid data. For more information see source.