The Racialized Costs of Banking

Downloads

Overview

Recent scandals have heightened public and political attention to the financial system, making salient the flawed and racially discriminatory practices of financial services that are necessary for participating in today’s economy. Lawsuits and fines levied against large national banks allege that their discretionary practices for charging costs and fees have unfairly targeted undocumented immigrants, Native communities, and communities of color. While the practices of large national banks have captured headlines, racially discriminatory practices are likely ubiquitous across U.S. financial services and evident even in the most basic financial products at small and community “Main Street” banks.

This report discusses findings from an investigation into the racialized costs and fees associated with entry-level checking accounts from a sample of primarily small and community Main Street banks. Contradicting the wholesome stereotype of Main Street banks, balance requirements are higher and fee structures are more punishing among banks in black and Latinx communities net of controls for socioeconomic characteristics and the presence of competing financial services. There is also evidence for the role of bank employees’ discretion in shaping costs and fees. The results are even more troubling when considered alongside racial inequalities in income and wealth—not only are black and Latinx areas served by more expensive banks, but they are home to poorer residents. Given these findings, financial system regulations and strong consumer protections are necessary for guarding consumers and communities of color against being charged more for inclusion in the financial system and participation in the economy.

Key Findings

- Banks charge communities of color more for opening and maintaining basic, entry-level checking accounts. The minimum opening deposit is substantially higher in majority black neighborhoods ($80.60) and in neighborhoods without a racial majority ($97.00) than in white neighborhoods ($68.50). Opening deposit requirements are almost the same in majority Latinx ($68.60) as in white neighborhoods.

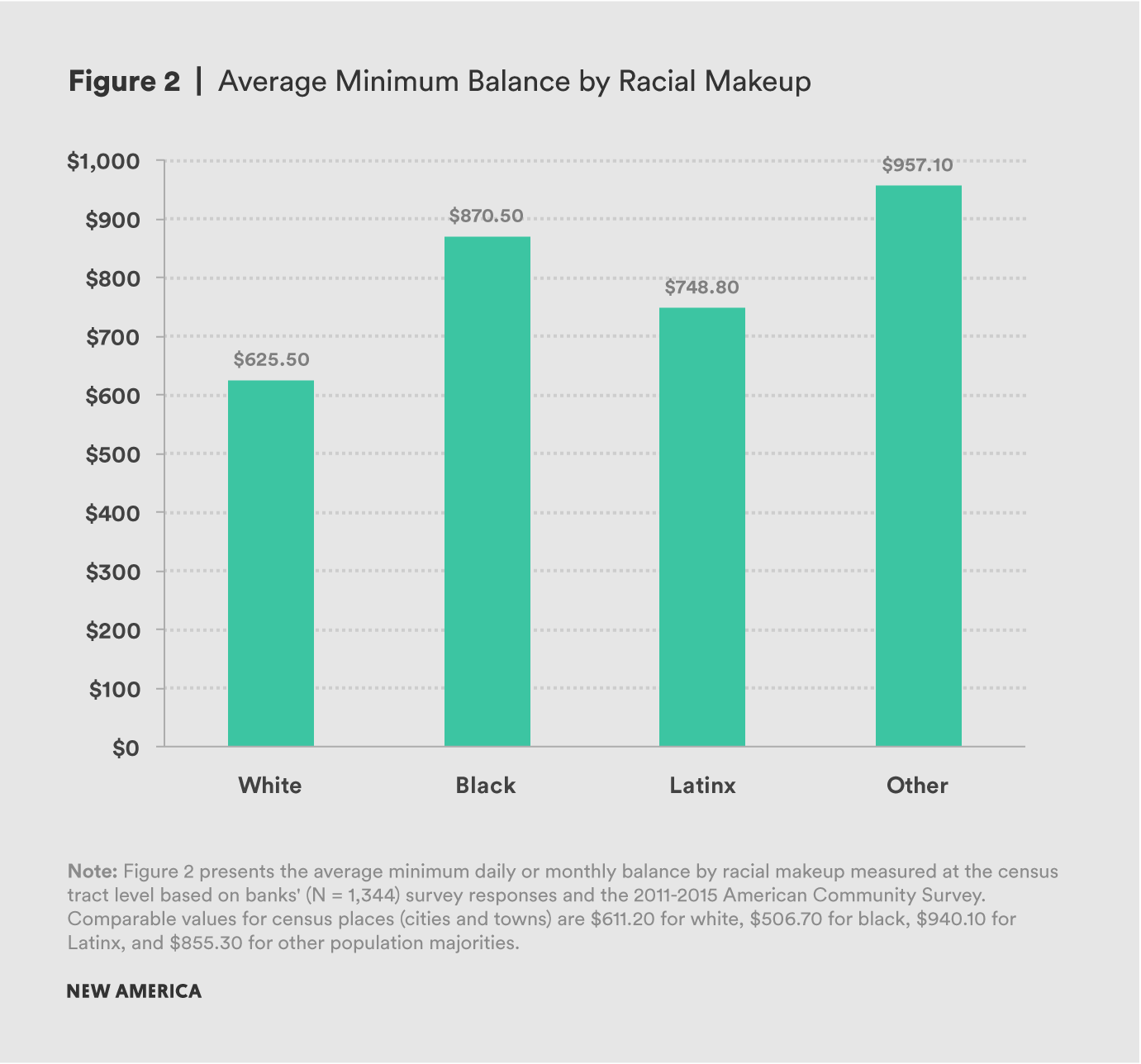

- It is cheaper to maintain a checking account opened in a white neighborhood. A minimum balance of only $625.50 is required to avoid fees in a majority white neighborhoods, compared to $748.80 in majority Latinx neighborhoods, $870.50 in majority black neighborhoods, and $957.10 in other neighborhoods.

- Discretionary banking practices amplify the racialized costs of banking, and evidence of racial bias among tellers means that checking account costs and fees depend on who consumers talk to at the bank. Tellers in places with small white populations report significantly higher overdraft fees and greater likelihoods of using credit or screening agencies than tellers in places with large white populations.

- Segregation substantially shapes the cost of banking. In total, the average checking account costs and fees are $190.09 higher for blacks, $25.53 higher for Asians, and $262.09 higher for Latinx when compared to whites.

- Banks’ costs and fees further limit the economic power of communities of color by requiring more earnings to be sequestered in checking accounts where they cannot be used. The average white American needs to deposit approximately 3 percent of a paycheck in order to open a checking account in their neighborhood and keep 28 percent of a paycheck deposited to avoid a fee or account closure. Blacks, by comparison, need to initially deposit 6 percent of a paycheck and keep 60 percent unused in their account. Comparable values for Latinx are 6 percent and 54 percent; for Asians, the values are 3 percent and 22 percent.

The Racialized Costs of Banking

Recent scandals have heightened public and political attention to the financial system, making salient the flawed and racially discriminatory practices of financial services that are necessary for participating in today’s economy.1 Large and national banks in particular have been implicated in these scandals. Civil lawsuits filed in California in 2017 allege that Wells Fargo employees targeted undocumented immigrants and Native communities to open transaction accounts and lines of credit without consumers’ knowledge and illegally charged fees on dormant accounts that consumers didn’t even know they owned.2 When consumers’ accounts exhibited signs of fraudulent activity, the bank closed the accounts instead of conducting investigations as legally required.3 Wells Fargo was fined $35 million and $100 million for these practices and, in 2018, the bank received a $1 billion fine associated with their auto insurance and mortgage lending practices.4 JPMorgan & Chase’s settlement of a $55 million lawsuit alleging racial discrimination also received widespread publicity, which evolved out of lenders’ use of discretion in varying mortgage interest rates that resulted higher rates for black and Latinx borrowers.5 6

While these banks’ practices have captured national headlines, racially discriminatory practices are not confined to large and national “Wall Street” banks and are likely ubiquitous across U.S. financial services and evident in the most basic of financial products.7 Racially discriminatory practices can also be observed within the small and community “Main Street” banks nostalgically lauded in mainstream public discourse as friendlier and more trustworthy.8 Small and community banks’ practices sometimes receive less scrutiny given their public perception, limited geographic scope, and lower share of deposits. However, relationship banking—the foundational practice of small and community banks that distinguishes them from their larger, more centralized counterparts9—may enable discriminatory practices through its reliance on discretion and contradict the wholesome stereotype of “Main Street” banks.

Relationship banking—the foundational practice of small and community banks—may enable discriminatory practices through its reliance on discretion and contradict the wholesome stereotype of “Main Street” banks.

Despite the publicity surrounding banks’ practices associated with their entry-level banking products, few investigations examine the possibility of racialized costs and fees associated with entry-level products like checking accounts. However, checking accounts are among the most widely used products and often serve as the first product obtained by a consumer—a fundamental banking product that, in many ways, serves as a gateway into the economy.10 Ninety-eight percent of consumers who use a bank have a checking account.11 Moreover, costs and fees prevent many consumers from opening and/or maintaining these accounts.12 Nearly two-thirds of consumers say their main reason for not having a checking or other bank account is because they do not have enough money, such as for affording the minimum opening deposit, minimum account balance, and maintenance fees.13 Indeed, consumers pay a cumulative average of $1,000 over 10 years for their checking accounts’ combined minimum opening deposit and balance, maintenance fees, and overdraft and insufficient funds fees.14 If banks tailor their checking accounts and the associated costs and fees to the communities they serve, and/or use discretion in charging these costs and fees, then the patterns of racial and economic segregation that characterize the American geographic landscape may shape variation in the cost of banking. In other words, banks may charge communities of color more for entrée into and participation in the economy.

This report discusses findings from novel survey data from a stratified random sample of banks that investigated the racialized costs and fees associated with entry-level checking accounts. Primarily a sample of small and community Main Street banks, a range of account characteristics are analyzed that may discourage or prevent consumers from opening accounts and heighten the possibility of their closing accounts, such as minimum opening deposit and minimum balance amounts, maintenance fees, and overdraft fees. (Readers should note that these data and analyses do not make direct comparisons between big and small and community banks. While demonstrating discriminatory practices within small and community banks, these data do not measure whether—or the extent to which—larger banks have discriminatory practices.) Balance requirements are higher and fee structures are more punishing among banks in black and Latinx communities net of controls for socioeconomic characteristics and the presence of competing financial services. There is also evidence for the role of bank employees’ discretion in shaping costs and fees. Bank tellers in predominantly non-white places are more likely to report higher overdraft fees compared to tellers in predominantly white places. These results are even more troubling when considered alongside racial inequalities in income and wealth—not only are black and Latinx areas served by more expensive banks, but they are home to poorer residents.

Racialized Patterns in Banks’ Historic and Present-Day Practices

Racialized patterns in banks’ exclusionary practices have been widely documented, including banks’ tendencies to disproportionately open and operate branches in white communities.15 For instance, black and Latinx communities are less likely to have bank branches than are communities on average, both nationally and within metropolitan areas.16 During the Great Recession, comparably-sized banks closed at higher rates in markets serving communities of color between 2009 and 2014, with some black and Latinx communities losing half their branches.17 The uneven distribution of bank branch locations exact a cost on residents of communities of color in the forms of greater travel distance and time to the nearest banking facility.18 These practices also create “banking deserts”19 in which payday lenders, check cashers, and other non-bank services thrive,20 thereby implicating banks in facilitating a market dynamic whereby the financial services environments in communities of color are dramatically different—in terms of quality and expense—from those in white communities.

Banks are implicated in facilitating a market dynamic whereby the financial services environments in communities of color are dramatically different—in terms of quality and expense—from those in white communities.

Racialized patterns are also reflected in banks’ historic and present-day practices around redlining, whereby banks extend less credit and/or higher cost credit to communities of color.21 Racialized patterns in redlining represent whether, how, and the extent to which banks invest in communities of color and reveal the ways that banks extract extra costs from communities in exchange for their investment: lending lower-quality credit at higher interest rates. This dynamic was clearly evident during the subprime lending boom when black and Latinx people and places were targeted for often-predatory subprime loans.22 Such neighborhoods also bore the brunt of the foreclosure crisis following the Great Recession23—due in no small part to racially differential treatment by lenders24—and similar practices have continued into the housing market’s recovery.25

Racialized patterns raise the concern of discrimination—especially when considering the long history of the finance industry as an active discriminator26 and contemporary examples of racial targeting,27 differential treatment,28 and disparate impact.29 In addition to the reluctance to operate in communities of color,30 another potential site of racial discrimination may be bank employees’ discretionary practices in charging costs and fees.31 Discretion by frontline employees that results in racial discrimination is well-documented in literature on police stops,32 court proceedings,33 and social service delivery.34 In the context of financial services, bank employees wield discretionary power in implementing bank policies in a racialized manner. In other words, how much a customer pays in costs and fees may depend in part on who they talk to at the bank. This pattern is reflected in analyses of data from mortgage lending lawsuits brought to the U.S. Department of Justice Civil Rights Division, which illuminated widespread discriminatory practices, including loan officers who “referred to subprime loans in minority communities as ‘ghetto loans’ and minority customers as…‘mud people.’”35

Discretion: The Foundation of Small and Community Banking

As it turns out, discretionary practices are the foundation of small and community banking. According to the FDIC, small banks hold less than $1 billion in assets and limit their services to a localized geographic scope. Adhering to the same asset holding threshold, community banks are further defined by their reliance on relationship building, local knowledge, and other unconventional data to deliver their products and services.36 In fact, Dennis Nixon, CEO of IBC Bank located in Texas and Oklahoma, penned this exact sentiment in his editorial criticizing the regulations enacted under the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act. Lamenting the regulations’ burdensome effects on small and community banks, Nixon writes, “Everyone should understand that discretion is the essence of community banking. The relationships we build in our communities that allow us to make local lending decisions are what set us apart from the larger banks…Community banks [work] with people in our communities who are not only our customers, but also our neighbors.”37

The discretionary practices that allow banks to flexibly deliver consumer-oriented products and services simultaneously create opportunities for discrimination to emerge and flourish. Sanctioned by institutional norms and deeply embedded practices that determine which consumers are worthy of handling responsible banking,38 banks and their employees make discretionary decisions that alter consumers’ engagement with and trust in financial services. As illustrated by the recent financial system scandals, banks and their employees make discretionary decisions when setting the terms of financial products and services, such as opening new accounts and lines of credit and charging interest rates on loans. In fact, when asked about banks’ official policies for charging overdraft fees on entry-level checking accounts, bank employees reveal socially-embedded biases as part of their discretionary decision-making, saying “There’s an ad-hoc policy,” “If we know it’s a mortgage payment, we might allow that,” and “Not if it’s at a casino.”39 In fact, banks involuntarily close checking accounts at significantly higher rates in counties with higher percentages of black residents in the presence of excessive overdraft fees—practices that effectively push consumers out of the financial system.40 Augmented by socially-embedded biases,41 racially discriminatory practices can emerge when banks and their employees charge consumers and communities of color more for their products and services.

The discretionary practices that allow banks to flexibly deliver consumer-oriented products and services simultaneously create opportunities for discrimination to emerge and flourish.

These practices powerfully illustrate how banks can engage in racially discriminatory practices that effectively siphon wealth out of communities of color through the very financial products and services that are considered to be tools for wealth and investment.42 Moreover, racial segregation may exacerbate discriminatory practices by creating easily identifiable, geographically organized local markets.43 Thus, the potential role of segregation in creating opportunity for animus to manifest as higher costs and fees in communities of color warrants investigation.44

Citations

- Davis, Gerald, “Managed by the Markets: How Finance Reshaped America,” Oxford University Press, 2009.

- White, Gillian, “A Lawsuit Claims Wells Fargo Targeted Undocumented Immigrants to Hit Sales Quotas.” The Atlantic, 2017. source

- Flitter, Emily and Stacy Cowley, “Wells Fargo Accused of Harming Fraud Victims by Closing Accounts,” The New York Times, 2018. source

- Levine, Matt, “Wells Fargo Pays Some More Fines,” Bloomberg View, 2018. source

- White, Gillian, “J.P. Morgan Chase’s $55 Million Discrimination Settlement” The Atlantic, 2017. source

- Glantz, Aaron and Emmanuel Martinez, “Keep Out: For People of Color, Banks are Shutting the Door to Homeownership,” 2018. source

- Clifford, Stephanie and Jessica Silver-Greenberg, “Bank tellers, with access to accounts, pose a rising security risk,” NY Times, 2016. source

- Servon, Lisa, “The Unbanking of America: How the New Middle Class Survives,” Houghton Mifflin Harcourt, 2017.

- Federal Deposit Insurance Corporation, “Community Banking Study,” Washington, DC, 2012. source

- Federal Deposit Insurance Corporation, “FDIC National Survey of Unbanked and Underbanked Households,” 2016, Washington, DC. source; Friedline, Terri, Paul Johnson, and Robert Hughes, “Toward Healthy Balance Sheets: Are Savings Accounts a Gateway to Young Adults’ Asset Diversification and Accumulation?” Federal Reserve Bank of St. Louis Review 96(4), 2014, pp. 359-389.

- Federal Deposit Insurance Corporation, “FDIC National Survey of Unbanked and Underbanked Households,” 2016, Washington, DC. source

- Federal Deposit Insurance Corporation, “FDIC National Survey of Unbanked and Underbanked Households,” 2016, Washington, DC. source

- Federal Deposit Insurance Corporation, “FDIC National Survey of Unbanked and Underbanked Households,” Washington, DC, 2016. source

- NerdWallet, “Study: Checking Fees Average Almost $1,000 Over a Decade,” n.d. source

- Celerier, Claire and Adrien Matray, “Bank Branch Supply and the Unbanked Phenomenon,” University of Zurich, 2016. source; Faber, Jacob William, “Cashing in on distress: The expansion of fringe financial institutions during the Great Recession.” Urban Affairs Review, 2017. Advance Online Publication; Toussaint-Comeau, Maude and R Newberger, “Minority-Owned Banks and their Primary Local Market Areas,” Federal Reserve Bank of Chicago, 2017.

- Despard, Mathieu and Terri Friedline, “Do metropolitan areas have equal access to banking?” Washington, DC: New America and Center on Assets, Education, and Inclusion, 2017. source

- Kashian, Russell and Robert Drago, “Minority-Owned Banks and Bank Failures After the Financial Collapse,” Economic Notes, 46(1), 2017, pp. 5-36; Toussaint-Comeau, Maude and R Newberger, “Minority-Owned Banks and their Primary Local Market Areas,” Federal Reserve Bank of Chicago, 2017.

- Jorgensen, Mimi and Randall K.Q. Akee, “Access to Capital and Credit in Native Communities: A Data Review, Digital Version,” Tucson, AZ: Native Nations Institute, 2017. source; Morgan, Donald, Maxim Pinkovskiy, and Bryan Yang, “Banking Deserts, Branch Closings, and Soft Information,” New York, NY: Federal Reserve Bank of New York, Liberty Street Economics, 2016. source

- A banking desert refers to a geographic area without bank or credit union branches. Research has measured banking deserts as census tracts that lack any of these financial services within a 10-mile radius from their centers.

- Caskey, John P., “Fringe Banking: Check Cashing Outlets, Pawnshops, and the Poor,” Russell Sage Foundation, 1994; Smith, Tony, Marvin Smith, and John Wackes, “Alternative Financial Service Providers and the Spatial Void Hypothesis,” Regional Science and Urban Economics, 38(3), 2008, pp. 205-227.

- Begley, Taylor and Amiyatosh Purnanandam, “Color and Credit: Race, Regulation, and the Quality of Financial Services,” University of Michigan Poverty Solutions, 2017. source; Cohen-Cole, Ethan, “Credit Card Redlining,” The Review of Economics and Statistics, 93(2), 2011, pp. 700-713; Rothstein, Richard, “Color of Law: A Forgotten History of How our Government Segregated America,” Liveright Publishing, 2017.

- Faber, Jacob William, “Racial Dynamics of Subprime Mortgage Lending at the Peak,” Housing Policy Debate, 23(2), 2013, pp. 328–49; Hwang, Jackelyn, Michael Hankinson, and Kreg Steven Brown, “Racial and Spatial Targeting: Segregation and Subprime Lending Within and Across Metropolitan Areas,” Social Forces, 93(3), 2015, pp. 1081-1108; Rugh, Jacob S., Len Albright, and Douglas S. Massey, “Race, Space, and Cumulative Disadvantage: A Case Study of the Subprime Lending Collapse,” Social Problems, 62(2), 2015, pp. 186-218. doi: 10.1093/socpro/spv002

- Hall, Matthew, Kyle Crowder, and Amy Spring, “Neighborhood Foreclosures, Racial/Ethnic Transitions, and Residential Segregation,” American Sociological Review, 80(3), 2015, pp. 526-549. doi: 10.1177/0003122415581334; Rugh, Jacob S., “Double Jeopardy: Why Latinos Were Hit Hardest by the US Foreclosure Crisis,” Social Forces, 93(3), 2015, pp. 1139–84.

- Chan, Sewin, Michael Gedal, Vicki Been, and Andrew Haughwout, “The Role of Neighborhood Characteristics in Mortgage Default Risk: Evidence from New York City,” Journal of Housing Economics, 22(2), 2013, pp. 100-118. doi: 10.1016/j.jhe.2013.03.003; Reid, Carolina K., Debbie Bocian, Wei Li and Roberto G. Quercia, “Revisiting the Subprime Crisis: The Dual Mortgage Market and Mortgage Defaults by Race and Ethnicity,” Journal of Urban Affairs, 39(4), 2017, pp. 469–87.

- Bhutta, Neil, Jack Popper, and Daniel R. Ringo, “The 2014 Home Mortgage Disclosure Act Data,” Federal Reserve Bulletin, 101(4), 2015, pp. 1–32; Faber, Jacob William, “Segregation and the Geography of Creditworthiness: Racial Inequality in a Recovered Mortgage Market,” Housing Policy Debate, 28(2), 2018, pp. 215-247.

- Baradaran, Mehrsa, “The Color of Money: Black Banks and the Racial Wealth Gap,” Harvard University Press, 2017.

- Massey, Douglas S., Jacob S. Rugh, Justin P. Steil, and Len Albright, “Riding the Stagecoach to Hell: A Qualitative Analysis of Racial Discrimination in Mortgage Lending,” City & Community, 15(2), 2016, pp. 118-136. doi: 10.1111/cico.12179; Rugh, Jacob S., Len Albright, and Douglas S. Massey, “Race, Space, and Cumulative Disadvantage: A Case Study of the Subprime Lending Collapse,” Social Problems, 62(2), 2015, pp. 186-218. doi: 10.1093/socpro/spv002.

- Chan, Sewin, Michael Gedal, Vicki Been, & Andrew Haughwout, “The Role of Neighborhood Characteristics in Mortgage Default Risk: Evidence from New York City,” Journal of Housing Economics, 22(2), 2013, pp. 100-118. doi: 10.1016/j.jhe.2013.03.003

- Faber, Jacob William, “Cashing in on distress: The expansion of fringe financial institutions during the Great Recession,” Urban Affairs Review, 2017. Advance Online Publication. doi: 10.1177/1078087416684037

- Baradaran, Mehrsa, “The Color of Money: Black Banks and the Racial Wealth Gap,” Harvard University Press, 2017; Rothstein, Richard, “Color of Law: A Forgotten History of How our Government Segregated America,” Liveright Publishing, 2017.

- Hanson, Andrew, Zackary Hawley, Hal Martin, and Bo Liu, “Discrimination in Mortgage Lending: Evidence from a Correspondence Experiment,” Journal of Urban Economics, 92, 2016, pp. 48-65. doi: 10.1016/j.jue.2015.12.004; Kiviat, Barbara, “The Art of Deciding with Data: Evidence from How Employers Translate Credit Reports into Hiring Decisions,” 2017, Socio-Economic Review. Advance Online Publication. doi: 10.1093/ser/mwx030; Morgan State University, “Understanding Life in Financial Deserts,” Baltimore, MD: Morgan State University, School of Community Health and Policy, Earl G. Graves School of Business and Management, 2017. source

- Epp, Charles, Steven Maynard-Moody, and Donald Haider-Markel, “Pulled Over: How Police Stops Define Race and Citizenship,” University of Chicago Press, 2014.

- Yngvesson, Barbara, “Making Law at the Doorway: The Clerk, the Court, and the Construction of Community in a New England Town,” Law & Society Review, 22(3), 1988, pp. 409-448.

- Baviskar, Siddhartha and Søren Winter, “Street-Level Bureaucrats as Individual Policymakers: The Relationship Between Attitudes and Coping Behavior Toward Vulnerable Children and Youth,” International Public Management Journal, 20(2), 2017, pp. 316-353. doi: 10.1080/10967494.2016.1235641; Zacka, Bernardo, “When the State Meets the Street: Public Service and Moral Agency,” Harvard University Press, 2017.

- Massey, Douglas S., Jacob S. Rugh, Justin P. Steil, and Len Albright, “Riding the Stagecoach to Hell: A Qualitative Analysis of Racial Discrimination in Mortgage Lending,” City & Community, 15(2), 2016, pp. 118-136. doi: 10.1111/cico.12179

- FDIC, “Community Banking Study,” Washington, DC, 2012. source

- Nixon, Dennis, “To Restore Health To Community Banks, Dodd-Frank Must Be Reformed,” Investor’s Business Daily, 2017. source

- Soss, Joseph, Richard Fording, and Sanford Schram, “The Organization of Discipline: From Performance Management to Perversity and Punishment,” Journal of Public Administration Research and Theory, 21(2 Issue Supplement), 2011, pp. i203-i232. doi:10.1093/jopart/muq09

- Friedline, Terri, Mathieu Despard, Rachael Eastlund, and Nikolaus Schuetz, “Are Banks’ Entry-Level Checking Accounts Safe and Affordable?” University of Michigan, Center on Assets, Education, and Inclusion, 2017. source

- Campbell, Dennis, F. Asís Martínez-Jerez, and Peter Tufano, “Bouncing out of the banking system: An empirical analysis of involuntary bank account closures,” Journal of Banking & Finance, 36(4), 2012, pp. 1224-1235. doi: 10.1016/j.jbankfin.2011.11.014

- Epp, Charles, Steven Maynard-Moody, and Donald Haider-Markel, “Pulled Over: How Police Stops Define Race and Citizenship,” University of Chicago Press, 2014.

- Faber, Jacob W. and Ingrid Gould Ellen, “Race and the Housing Cycle: Differences in Home Equity Trends Among Long-Term Homeowners,” Housing Policy Debate, 1482(April), 2016, pp. 1–18; Saegert, Susan, Desiree Fields, and Kimberly Libman, “Mortgage Foreclosure and Health Disparities: Serial Displacement as Asset Extraction in African American Populations,” Journal of Urban Health 88(3), 2011, pp. 390-402. doi: 10.1007/s11524-011-9584-3

- Rugh, Jacob S., Len Albright, and Douglas S. Massey, “Race, Space, and Cumulative Disadvantage: A Case Study of the Subprime Lending Collapse,” Social Problems, 62(2), 2016, pp. 186-218. doi: 10.1093/socpro/spv002; Rugh, Jacob S., and Douglas S. Massey, “Racial Segregation and the American Foreclosure Crisis,” American Sociological Review, 75(5), 2010, pp. 629-651.

- Pager, Devah and Hana Shepherd, “The Sociology of Discrimination: Racial Discrimination in Employment, Housing, Credit, and Consumer Markets,” Annual Review of Sociology, 34, 2008, pp. 181–209.

Evidence from Banks’ Entry-Level Checking Accounts

This report discusses findings from an investigation into the racialized costs of banking in entry-level checking accounts, including tests for evidence of banks’ discretionary practices in the delivery of account costs and fees. The findings are based on survey data collected from a stratified random sample of commercial banks in the United States, which asked banks about the costs and fees of entry-level checking accounts, as well as their strategies for serving consumers (e.g., whether branches operated extended hours during evenings and weekends, offered non-English language services, used ATMs, and offered online and/or mobile banking) and transaction processing (e.g., whether transactions were processed in chronological order). To analyze relationships between community racial demographics and banks’ checking account costs and fees, geocoded survey responses were combined with census tract and census place data from the 2011-2015 5-year sample of the American Community Survey (ACS), 2014 Federal Deposit Insurance Corporation (FDIC) summary of deposits, 2014 National Credit Union Administration (NCUA) call reports, and 2015 InfoGroup proprietary business listings. The results discussed here summarize key findings based on regression estimates in models with full controls, and a more detailed description of the data and methods is provided in the technical appendix.

Racial Disparities in Opening and Maintaining Accounts

Racial disparities are present in the costs and fees required to open and maintain basic, entry-level checking accounts. In other words, higher costs and fees charged by banks for these entry-level products are significantly associated with communities of color (see Figure 1). The minimum opening deposit is substantially higher in communities with majority black populations ($80.60), and in communities that are more racially diverse without a white, black, or Latinx majority ($97.00), when compared to majority white communities ($68.50). Opening deposit requirements are almost the same in majority Latinx ($68.60) as in white communities.

It is cheaper to maintain a checking account opened in a white neighborhood (see Figure 2). A minimum balance of only $625.50 is required to avoid fees or closure in a majority white tract, compared to $748.80 in majority Latinx tracts, $870.50 in majority black tracts, and $957.10 in other tracts.

The Extra Costs of Segregation

Segregation at the national level also shapes the cost of banking. In other words, in addition to the racial disparities across communities described above, white, black, Asian, or Latinx individuals can expect to pay different costs and fees based on their neighborhood-level exposure to other racial groups shaped by national patterns of segregation.1

For example, the extra costs of segregation are apparent in the maintenance fee amounts on banks’ entry-level checking accounts. The average maintenance fee amount of $2.83 varies widely by race and provides evidence of the extra costs of segregation (see Figure 3). Based on their neighborhood-level exposures to other racial groups, the average individual white person can expect to pay a maintenance fee of $6.09 while average black, Latinx, and Asian individuals pay nearly $1 more for the same fee. Despite the fact that these fees appear to be relatively small on average, the extra costs of segregation are disproportionately large. These fees add up over time, contributing to the extra costs that black, Latinx, and Asian individuals pay to maintain entry-level checking accounts.

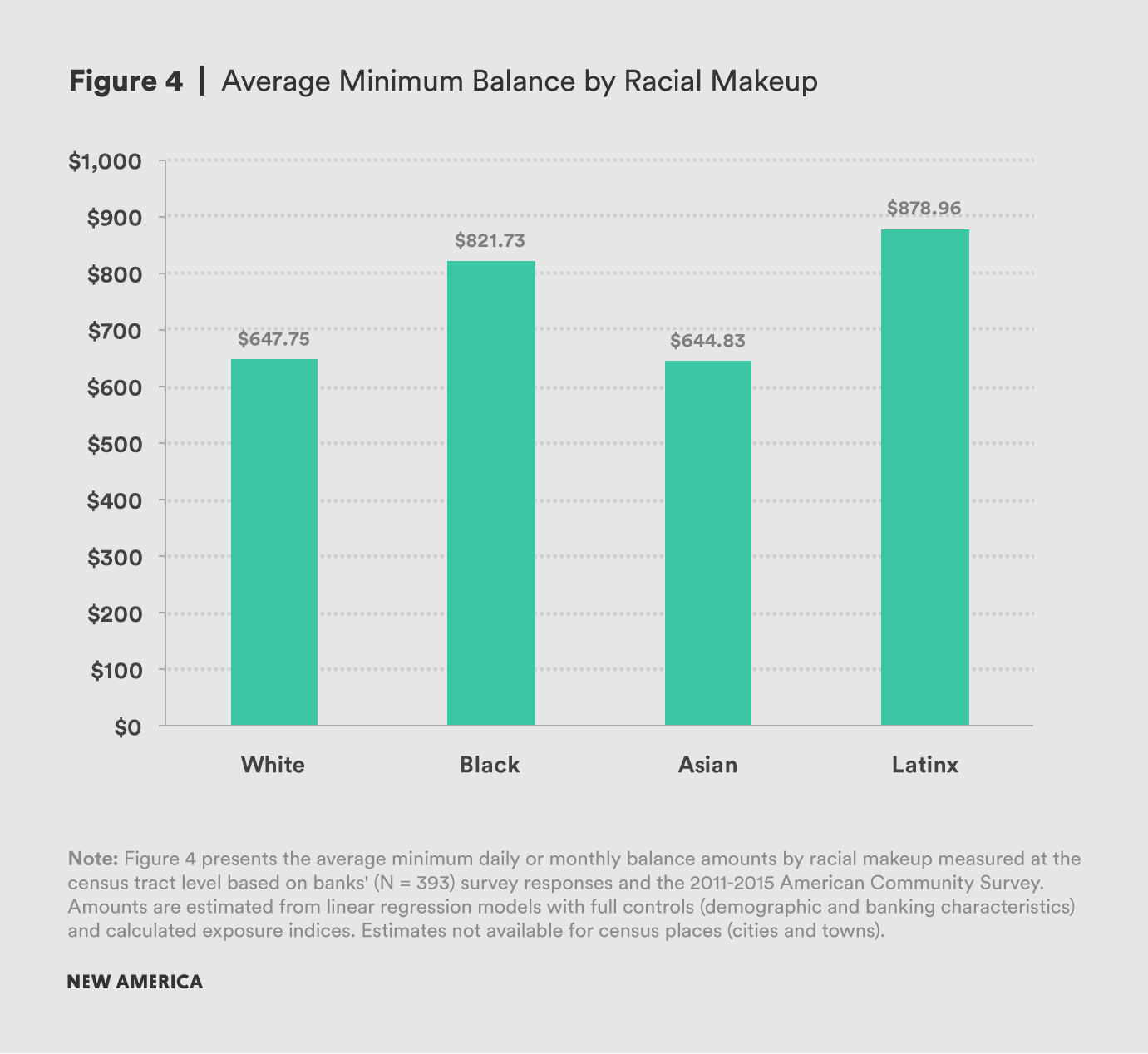

Disparities are also observed within the average minimum balance on entry-level checking accounts. While the average minimum balance is $676.55, based on average exposure to other racial groups, black and Latinx individuals can expect to maintain substantially higher minimum balance amounts (see Figure 4). The average individual white person can expect to maintain a minimum balance amount of $647.75 and the average individual Asian person can expect a balance amount of $644.83. By comparison, average black and Latinx individuals must maintain respective minimum balance amounts of $173.98 and $231.21 more than their white counterparts.

The total costs of segregation are staggering. The differences add up to hundreds of dollars after summing together all the costs and fees that average individuals can expect to pay based on their exposure to other racial groups.2 When compared to whites, the average checking account costs and fees are $190.09 higher for blacks, $25.53 higher for Asians, and $262.09 higher for Latinx.

The average individual white person can expect to maintain a minimum balance amount of $647.75, while the respective minimum balance amounts are $821.73 and $878.96 for the average Black and Latinx individuals.

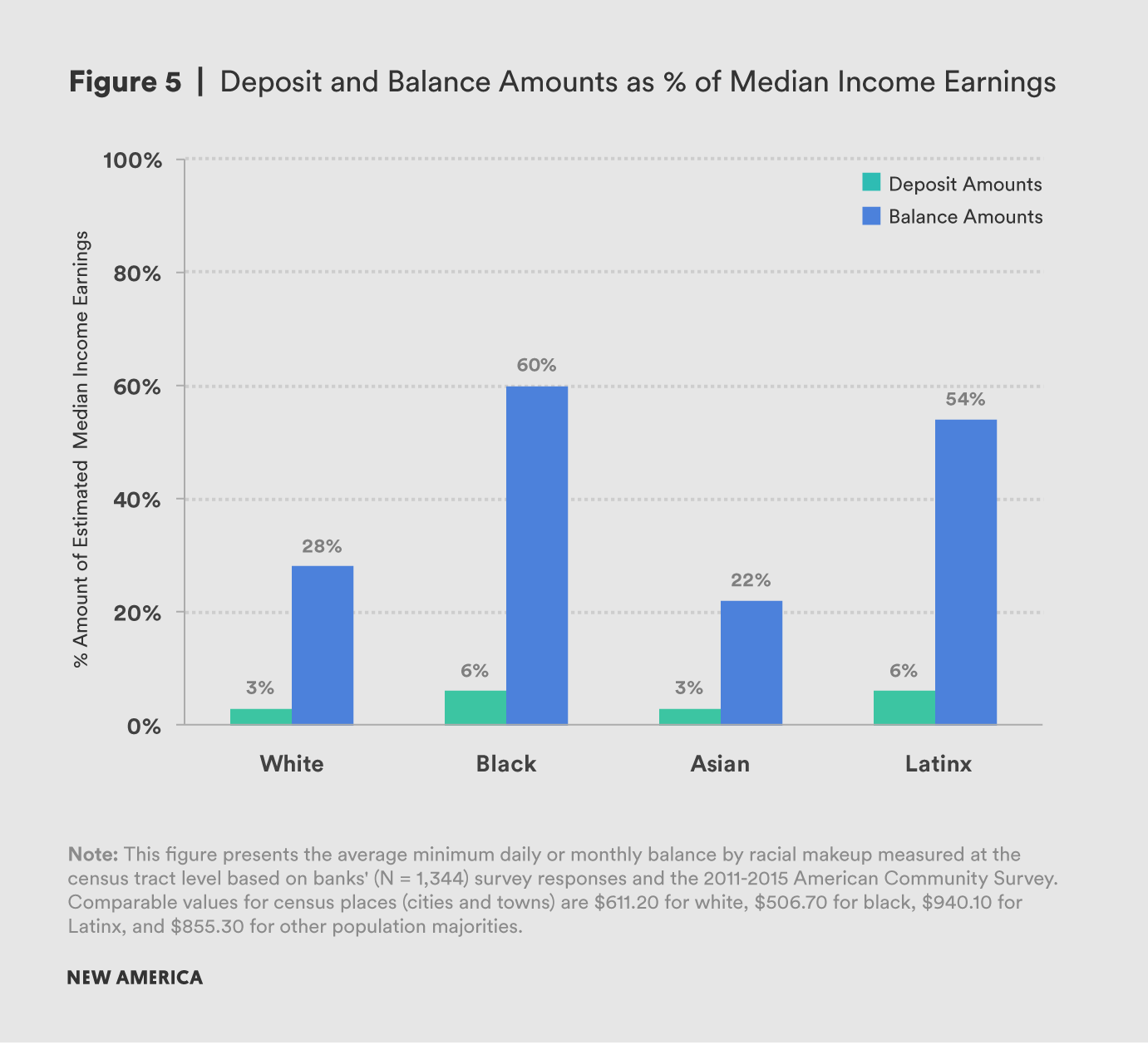

Banks’ costs and fees further limit the economic power of communities of color by requiring more earnings of black and Latinx individuals to be sequestered in checking accounts where they cannot be used (see Figure 5). For instance, based on median annual income earnings for households and assuming 26 paychecks per year, the average paycheck amounts are approximately $2,290 for whites, $1,373 for blacks, $1,640 for Latinx, and $2,856 for Asians. Based on these amounts, the average white individual needs to deposit approximately 3 percent of a paycheck in order to open a checking account in their community and keep 28 percent of a paycheck deposited to avoid a fee or account closure. For Blacks and Latinx, these amounts are more than double. Blacks need to initially deposit 6 percent of a paycheck and keep 60 percent unused in their account and the comparable values for Latinx are 6 percent and 54 percent.

Discretionary (a.k.a. Discriminatory) Banking

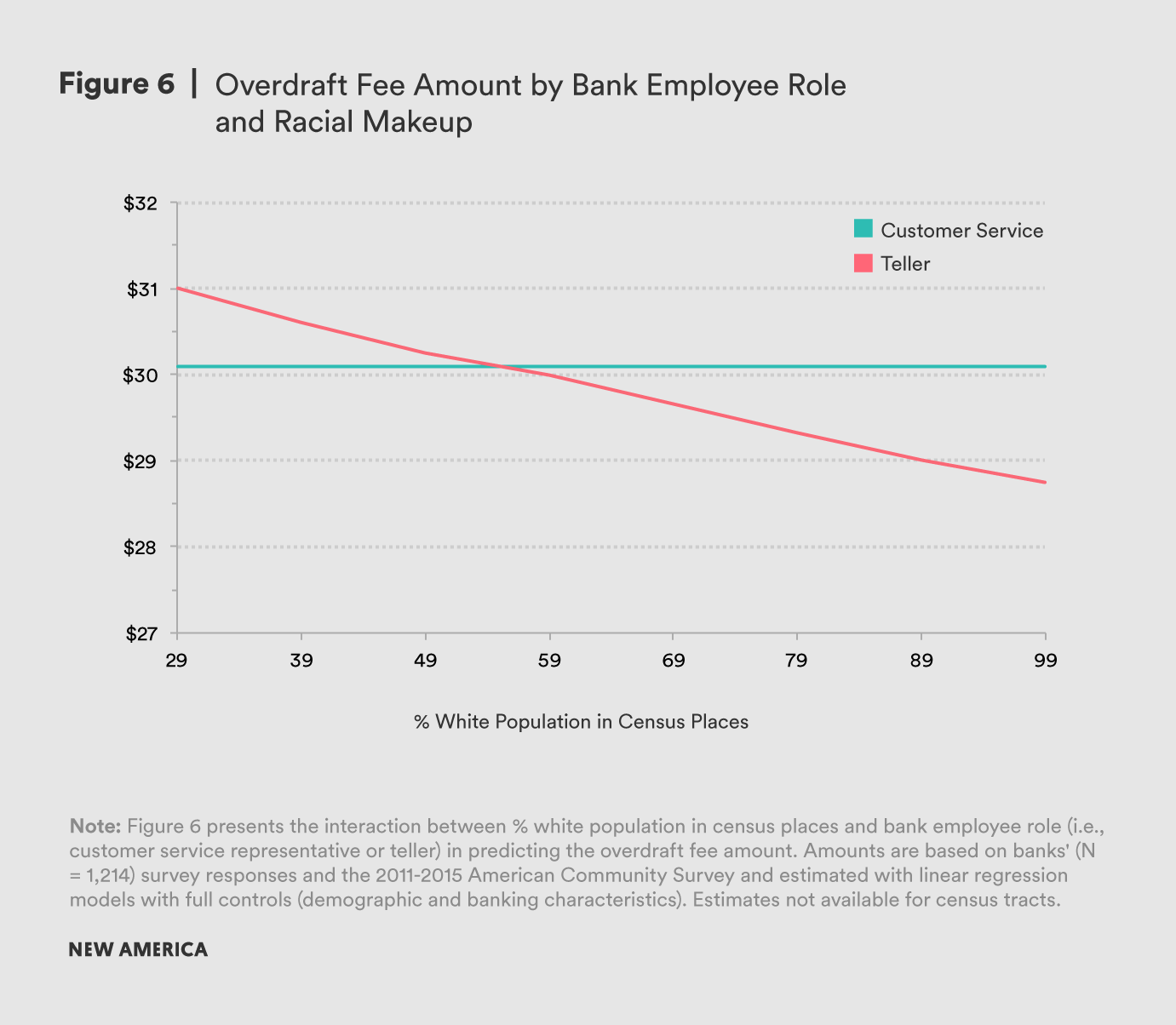

Discretionary banking practices amplify the racialized costs of banking, and evidence of racial bias among tellers suggests that checking account costs and fees depend on who consumers talk to at the bank. In particular, tellers in places with small white populations report significantly higher overdraft fees and greater likelihoods of using credit or screening agencies than tellers in places with large white populations (see Figure 6). The difference between the average overdraft fee amounts in places with the largest and smallest white populations is $2, which may seem like a small amount. However, these fees can accumulate over time and represent ways that banks may be siphoning money out of consumers of color.

Citations

- Please see the technical appendix and Reardon (2002) for more information about segregation and exposure indices. The results presented in this section are based on multivariate models with full controls.

- These costs and fees include the minimum opening balance, minimum balance, maintenance fee, and overdraft fee amounts.

What Can Be Done? Strong Financial System Regulations and Consumer Protections

Financial system regulations and strong consumer protections can guard consumers and communities of color against being charged more for inclusion in the financial system and participation in the economy. For instance, existing guidelines and standards encourage banks to voluntarily offer safe and affordable checking accounts. The FDIC’s Model Safe Accounts recommends core checking account features that include an opening deposit of $10 to $25, a monthly maintenance fee up to $3, no overdraft or insufficient funds fees, and free online and mobile banking. 1 More recently, the CFE Fund’s Bank On National Account Standards recommends an opening deposit of $25 or less, a monthly maintenance fee up to $10, no overdraft or insufficient funds fees, and free online and mobile banking. 2 However, few banks voluntarily comply with these guidelines and standards, with only 9 percent of banks having checking accounts that meet the core Bank On National Account Standards.3 Without mandatory regulations or protections, communities—and especially communities of color—may be at risk for paying higher costs and fees.

The Community Reinvestment Act (CRA) is another way of imposing mandatory regulations on banks and ensuring protections for consumers; though, the CRA emphasizes banks’ lending activity over safe and affordable checking or transaction accounts. The CRA was passed in 1977 to assess FDIC-insured financial institutions’ lending activity in low-income and economically-distressed communities and arose out of the need to redress banks’ racially discriminatory redlining practices.4 Through the CRA, FDIC-insured banks receive ratings of “substantial non-compliance” to “outstanding” that have implications for their abilities to make business decisions, and the largest banks with $1 billion or more in assets receive the most scrutiny. However, the CRA has been found to dilute the quality of lending activity while expanding its quantity.5 Moreover, banks’ CRA ratings are incongruent with current evidence of redlining and racialized patterns of entry-level checking account costs and fees,6 given that 97 percent of banks earn the highest ratings.7 Banks’ superficially high ratings may be due in part to the fact that the CRA only requires banks to report borrowers’ and communities’ income—not race.8 Thus, the CRA inadequately redresses banks’ racially discriminatory practices by conflating income and race and underestimates discriminatory practices in checking and transaction accounts by emphasizing lending.

New regulatory oversights and consumer protections were introduced in 2010 with the passage of the Dodd-Frank Wall Street Reform and Consumer Protection Act,9 which was precipitated by a financial system crisis that resulted in taxpayer-funded bank bailouts and the Great Recession.10 The Dodd-Frank Act established the Consumer Financial Protection Bureau (CFPB), a new government agency designed to protect consumers by providing regulatory oversight of the financial system and filling gaps in regulation. Since the agency’s creation, the CFPB has issued guidelines and rules to protect consumers that cover a range of activities across the financial system. These guidelines and rules have covered banks’ overdraft protections and mandatory arbitration clauses on checking and transaction accounts, payday lending, medical debt, and student loan debt.11

Financial system regulations and strong consumer protections can guard consumers and communities of color against being charged more for inclusion in the financial system and participation in the economy.

Consumers of color stand to benefit the most from the protections offered by the CFPB.12 For example, the CFPB levied millions of dollars in fines after discovering that Wells Fargo’s employees were illegally opening transaction accounts and lines of credit without consumers’ knowledge or permission in order to meet demanding sales quotas.13 Notably, bank employees admitted to targeting immigrant and Native communities.14 Consumers (disproportionately of color) whose checking accounts were opened (perhaps unknowingly) by bank employees to meet sales quotas can be charged fees when their accounts remain dormant through no fault of their own, and banks can involuntarily close these accounts altogether. This account activity can be recorded by screening agencies and become part of consumers’ financial and credit histories, further maintaining disenfranchisement in the financial system. Therefore, the CFPB’s response was necessary for protecting consumers of color against racially discriminatory practices.

While communities and consumers of color can benefit from financial system regulations and strong protections, policy is moving in the opposite direction. Recent policy changes are characterized by fewer regulations and weaker consumer protections. The House of Representatives passed the Financial CHOICE Act in 2017, and the bill awaits voting in the Senate.15 The Financial CHOICE Act removes many of the financial system regulations put into place by the Dodd-Frank Act following the financial crisis and weakens the authority of the CFPB. For instance, the Financial CHOICE Act changes the CFPB’s leadership from an independent director to a five-member commission subject to congressional oversight, eliminates the database for collecting financial system complaints directly from consumers, and exempts payday and auto title lenders from CFPB’s regulatory oversight.16 Moreover, President Trump’s 2019 budget proposes restructuring the CFPB’s funding so that it passes through Congress instead of the Federal Reserve. Such a change limits the agency’s independence from political maneuvering and partisan debates by giving policymakers direct control over the CFPB’s budget.17

As another example, bipartisan efforts in Congress recently led to the passage of S.2155 Economic Growth, Regulatory Relief, and Consumer Protection Act.18 This bill attempts to separate Main Street banks from Wall Street banks, suggesting that Main Street banks need less oversight and accountability than their Wall Street counterparts. The bill amends prior legislation to allow 25 of the largest 38 banks to avoid stricter regulatory oversight and exempts 85 percent of lenders from Home Mortgage Disclosure Act (HMDA) reporting requirements that monitor racially discriminatory lending patterns.19 However, the racialized costs of banking revealed in this report are based on a sample of mostly Main Street banks and suggest exactly the opposite. Main Street banks are not innocent: They exhibit racially discriminatory patterns and need oversight just like their Wall Street counterparts. While checking and other transaction accounts are different financial products than the lending products targeted by S.2155, the racially discriminatory patterns in the costs and fees of these Main Street banks’ most basic, entry-level checking accounts may very well exist in their lending.

Given the findings discussed in this report that are supported by a rigorous and robust research literature,20 it is not sufficient to simply encourage banks to offer safe and affordable checking accounts and discourage racially discriminatory practices. Within our capitalist and market-driven economy, regulations and strong consumer protections are clearly necessary for guarding consumers and communities of color from racially discriminatory practices and ensuring full and dignified economic participation.

Citations

- Federal Deposit Insurance Corporation, “FDIC Model Safe Accounts Pilot,” Washington, DC, 2012. source

- CFE Fund, “Bank On National Account Standards (2017-2018),” New York, 2017. source

- Friedline, Terri, Mathieu Despard, Rachael Eastlund, and Nikolaus Schuetz, “Are Banks’ Entry-Level Checking Accounts Affordable?” New America, 2017.

- Litan, Robert, Nicolas Retsinas, Eric Belsky, and Susan White Haag, “The Community Reinvestment Act after Financial Modernization: A Baseline Report,” US Department of the Treasury, 2000. source

- Begley, Taylor and Amiyatosh Purnanandam, “Color and Credit: Race, Regulation, and the Quality of Financial Services,” University of Michigan Poverty Solutions, 2017. source

- Baradaran, Mehrsa, “The Color of Money: Black Banks and the Racial Wealth Gap,” Harvard University Press, 2017; Begley, Taylor and Amiyatosh Purnanandam, “Color and Credit: Race, Regulation, and the Quality of Financial Services,” University of Michigan Poverty Solutions, 2017. source; Rothstein, Richard, “Color of Law: A Forgotten History of How our Government Segregated America,” Liveright Publishing, 2017.

- Getter, Darryl, “The Effectiveness of the Community Reinvestment Act,” Congressional Research Service, 2005. source

- Ahuja, Vedika and Jason Richardson, “State of Gentrification: Home Lending to Communities of Color in California,” The Greenlining Institute, 2017. source

- P.L. No. 111-203, “Dodd-Frank Wall Street Reform and Consumer Protection Act, 2010.” source

- Mian, Atif and Amir Sufi, “House of Debt: How They (and You) Caused the Great Recession, and How We can Prevent it from Happening Again,” University of Chicago Press, 2014.

- Consumer Financial Protection Bureau, “Recent Updates,” 2018. source

- Ficklin, Patrice, “African-American and Hispanic borrowers harmed by Provident will Receive $9 Million in Compensation,” Consumer Financial Protection Bureau, 2017. source; Dodd-Ramirez, Daniel and Patrice Ficklin, “Redlining: CFPB and DOJ Action Requires BancorpSouth Bank to Pay Millions to Harmed consumers,” Consumer Financial Protection Bureau, 2016. source; Consumer Financial Protection Bureau, “Hudson City Savings Bank to Pay $27 Million to Increase Access to Credit in Black and Hispanic Neighborhoods it Discriminated Against,” 2015. source

- Consumer Financial Protection Bureau, “Consumer Financial Protection Bureau Fines Wells Fargo $100 Million for Widespread Illegal Practice of Secretly Opening Unauthorized Accounts,” 2016. source

- White, Gillian, “A Lawsuit Claims Wells Fargo Targeted Undocumented Immigrants to Hit Sales Quotas.” The Atlantic, 2017. source; Koren, James Rufus, “Former Wells Fargo Workers say They Targeted Immigrants and Native Americans,” Los Angeles Times, 2017. source

- H.R. 10, “Financial CHOICE Act,” 115th Congress, 2017. source

- Bennett, Geoff, “House Passes Bill Aimed at Reversing Dodd-Frank Financial Regulations,” NPR, 2017. source

- Merle, Renae, “White House Budget Plan Proposes Cutting CFPB Budget, Restricting Enforcement Powers,” The Washington Post, 2018. source

- S.2155, “Economic Growth, Regulatory Relief, and Consumer Protection Act,” 115th Congress, 2018. source

- Gelzinis, Gregg, and Joe Valenti. “Fact Sheet: The Senate’s Bipartisan Dodd-Frank Rollback Bill.” Center for American Progress, 2018.

- Faber, Jacob William, “Segregation and the Geography of Creditworthiness: Racial Inequality in a Recovered Mortgage Market,” Housing Policy Debate, 28(2), 2018, pp. 215-247; Kiviat, Barbara, “The Art of Deciding with Data: Evidence from How Employers Translate Credit Reports into Hiring Decisions,” Socio-Economic Review, 2017. Advance Online Publication; Massey, Douglas S., Jacob S. Rugh, Justin P. Steil, and Len Albright, “Riding the Stagecoach to Hell: A Qualitative Analysis of Racial Discrimination in Mortgage Lending,” City & Community, 15(2), 2016, pp. 118-136.

Technical Appendix

Survey Data

The findings presented in this report come from data collected by researchers from a stratified random sample of commercial banks1 in the United States. In 2016, researchers developed, piloted, and conducted a 57-question survey to uncover variation in the costs of entry-level checking accounts. In addition to the costs and fees of entry-level checking accounts, survey questions covered topics such as banks’ strategies for serving consumers (e.g., whether branches operated extended hours during evenings and weekends, offered non-English language services, used ATMs, and offered online and/or mobile banking) and transaction processing (e.g., whether transactions were processed in chronological order). The survey was piloted and data were collected between March and December 2016 from a stratified random sample of retail banks identified from the FDIC’s list of 6,186 active banks. The FDIC’s procedures from the FDIC (2016c) Small Business Lending Survey2 were implemented to select a stratified random sample, including stratifying by banks’ asset amounts and metropolitan and non-metropolitan areas.3 Contact information for each bank’s main branch was used for survey data collection and subsequent analyses.4 The sample included 1,976 banks and 1,625 banks completed the survey. The final analytic sample included 1,344 banks with complete data on the outcome variables.

Racial Makeup and Demographic Characteristics

To analyze relationships between geographic variation in demographic characteristics and checking account costs and fees, geocoded5 survey responses were combined with data from the 2011-2015 5-year sample of the American Community Survey (ACS) (Minnesota Population Center 2011). ACS data were gathered for neighborhoods (i.e. census tracts) as well as cities and towns (i.e. census places and county subdivisions) on the following: racial makeup (i.e. percent non-Hispanic/Latinx white, non-Hispanic/Latinx black, non-Hispanic/Latinx Asian, and Hispanic/Latinx) and demographic characteristics, including percent foreign born, educational attainment (i.e. percent of adults with a college degree and percent with less than high school), poverty rate, homeownership rate, and median age.

Banking Characteristics

Controls were included to measure banks’ asset holdings and location in rural areas (i.e. variables for bank size6, asset class, and rural location of the branch), as well as the job title or role of the bank employee that responded to the survey (i.e. variables for teller, customer service, or other job [such as retail or sales representative, branch manager or bank vice president]7) and whether they held a supervisory role. The financial services environment was also measured, including the presence of other commercial banks and alternative financial services (AFS). Data from 2014 Federal Deposit Insurance Corporation (FDIC) summary of deposits, 2014 National Credit Union Administration (NCUA) call reports, and 2015 InfoGroup proprietary business listings were used to calculate the geographic density of both traditional and alternative financial services (i.e. the number of each per square mile in the census tract).

Methods

A series of regression models were estimated for each outcome of interest, and the results described in this report are based on models with full controls: racial makeup, demographic characteristics, and bank characteristics. Interaction terms were used to test for evidence of racialized discretion, such as interacting indicator variables for the survey respondent’s job title or role (i.e. teller, customer service, or other role) with racial makeup for predicting checking account costs and fees. Regression coefficients were also used to estimate how checking account costs and fees vary across the typical neighborhood-level (or place-level) racial makeup experienced by white, black, Asian, and Latinx Americans. The 2011-15 ACS data were used to calculate the white-black, white-Asian, and white-Latinx exposure indices on the census tract-level for the entire United States excluding Puerto Rico, which measure the average tract-level percent black, Asian, and Latinx among white Americans.8 These values were then multiplied by the coefficients for percent black, Asian, and Latinx in fully-controlled models and the sum was added to the product of the coefficient for each covariate and that covariate’s mean.9

Citations

- Credit unions were excluded for several reasons. Unlike banks, credit unions limit their services to members based on employer or residency requirements, and operate on a cooperative model where members are joint owners. Credit unions are also insured and regulated differently than banks. Most importantly, commercial banks are far more common and hold far more assets than credit unions.

- Federal Deposit Insurance Corporation, “FDIC Small Business Lending Survey,” Washington, DC, 2016. source

- Karyen Chu and Keith Ernst of the FDIC provided assistance with implementing random sample stratification.

- The procedure of identifying each bank by its main branch could potentially introduce bias if, for example, FDIC branch listings were all headquarter locations and headquarter locations tended to offer distinct products and services at unique prices compared to other branches, or other branches were located in racially dissimilar communities. However, the evidence indicated that racial makeup and demographic characteristics between banks’ main and other branches were strongly correlated, indicating that the racial makeup of main and other branches were similar. Moreover, results were estimated using the average racial makeup of main and other branches in order to further address this potential limitation.

- Bank addresses were geocoded to census tracts using ArcGIS 10.

- Banks were identified as being community, small, regional, or mega/large/national in size, consistent with the FDIC designations.

- There were 248 unique job titles recorded for survey respondents within the analytic sample (including spelling variations). For parsimony, titles were collapsed into tellers (56% of respondents), customer service representatives (26%), and other positions (18%).

- Massey, Douglas S. and Nancy A. Denton, “American Apartheid: Segregation and the Making of the Underclass,” Harvard University Press, 1993; Reardon, Sean, “SEG: Stata Module to Compute Multiple-Group Diversity and Segregation Indices,” EconPapers, 2002. source

- Black exposure to blacks was 45.14, exposure to Asians was 3.68, and exposure to Latinx was 14.65. Corresponding exposure indices for Asians were 8.89, 22.87, and 19.51, while they were 10.48, 5.78, and 46.35 for Latinx. Rather than calculating binary exposure measures, all four racial groups were included per Reardon (2002).

More About the Authors

Jacob Faber