Competition

The relationship between market power, competition policy, and the problem of disinformation in our political culture is structural and indirect. The digital platform companies that aggregate and publish media content from channels across the internet have enormous influence over public discourse as de facto editors that determine the content we see. While there is some logic in applying regulations to monopolies as “one stop shops” to address immediate public harms, the long terms solution must involve a more robust competitive landscape to put market forces to work diversifying the digital media landscape. More to the point, competition policy affords opportunities to restore user control over data through portability and to provide individuals with the leverage they need to shape digital media products that do not devolve to the logic of data driven attention capture.

People are gradually losing track of the distinction between credible and questionable sources of news on the internet. “I saw it on Facebook” encapsulates the problem underlying the nation’s broken media system. Facebook, of course, is not a publisher. It is both a media company and a technology platform that distributes the publications of others, whose brands meanwhile fade into the background of the medium.

The same is true (in slightly different ways) of Google search, YouTube, Twitter, and other internet platforms that aggregate content. And although these companies cannot be considered news editors in the traditional sense, they do perform one key editing task: selecting which content their audience will see. In so doing, they choose not to select content based on a set of judgements related to the democratic role of public service journalism (i.e. out of a principled commitment to inform the public). Instead, they make selections based on what will keep the user on the platform longer, thus enabling the display of more ads and the collection of more user data.

“I saw it on Facebook” encapsulates the problem underlying the nation’s broken media system.

To be sure, this raw commercial logic was always a part of the media business, too. But on digital platforms, it has become the entire business. For modern internet platforms, gone is the notion that the media entity should cultivate a set of top stories that meet the needs of an informed citizen. The criteria for selection here are derived from algorithmic processing of the voluminous data that these companies keep about each user. From the data, they determine what users will find relevant, attractive, outrageous, provocative, or reassuring—a personalized editorial practice designed not to journalistically inform citizens, but rather to grab and hold every user’s attention. The precision and sophistication of the preference-matching grows with the improvement of the technology and the quantity of data. And the algorithm is indifferent as to whether it leads the user to towards facts and reasoned debate or towards conspiracy and nonsense.

When the attention-maximizing algorithms that serve as the editors of our political culture generate negative externalities for the public—such as filter bubbles that amplify disinformation and atomize the polity into opposed clusters—it is the role of government to act on behalf of society to reverse or contain the damage. This can happen in a variety of ways. We can make the criteria of the content selection—the aforementioned editing function—more visible to the user by stipulating that the platform’s algorithms be made transparent to the public. We can also limit the amount of data the companies may process in order to blunt the precision of those filtering algorithms and protect people from being segmented into self-reinforcing, misinformed audiences by requiring more stringent privacy policies. (We have covered these approaches in the previous two sections)

As a third option, we can promote market competition by giving people more control over their data and generating alternative ways for people to find the information they seek. The theory of change behind this potential measure is that by destabilizing the monopoly markets for digital media aggregation, curation, and distribution, we will foster new market structures that better serve public interest outcomes.

What is the starting point for new competition policy that can better reflect the changes wrought by the digital ecosystem? For years, there has been public debate about whether the major technology platforms—Google, Facebook, Amazon, and Apple, in particular—are monopolies and whether they should justifiably be broken up or regulated as utilities. The phenomenal growth, profitability, and market share enjoyed by these firms heightens the urgency of the issue.

Without question, there is tremendous concentration of wealth and market power in the technology sector. And many segments of the digital economy bear the hallmarks of a “winner-take-all” market.1 The top companies have gained dominance through a combination of data, algorithms and infrastructure that organically creates network effects and inhibits competitors. Put simply, once a network-based business reaches a certain scale, it is nearly impossible for competitors to catch up. The size of its physical infrastructure, the sophistication of its data processing algorithms (including AI and machine learning), and the quantity of data served on its infrastructure and feeding its algorithms (constantly making them smarter) constitutes an unassailable market advantage that leads inexorably to natural monopoly.2

The top companies have gained dominance through a combination of data, algorithms and infrastructure that organically creates network effects and inhibits competitors.

For example, there is simply no economically viable method for any company to match Google’s capability in the search market or Facebook’s capacity in social networking. That is not to say these companies are eternal. But it does mean that until there is a major shift in technology or consumer demand, they will dominate in the winner-take-all market. It is also worth raising the caveat that we must be mindful that a regulatory regime across a variety of issues that requires extensive resources to implement could perversely add to this market dominance—as the existing oligopoly might be the only market players able to fully comply. That said, this is not a reason to shy away from addressing the competition problem head-on; and there are ways to tier regulatory requirements to match proportional impact of different kinds of firms.

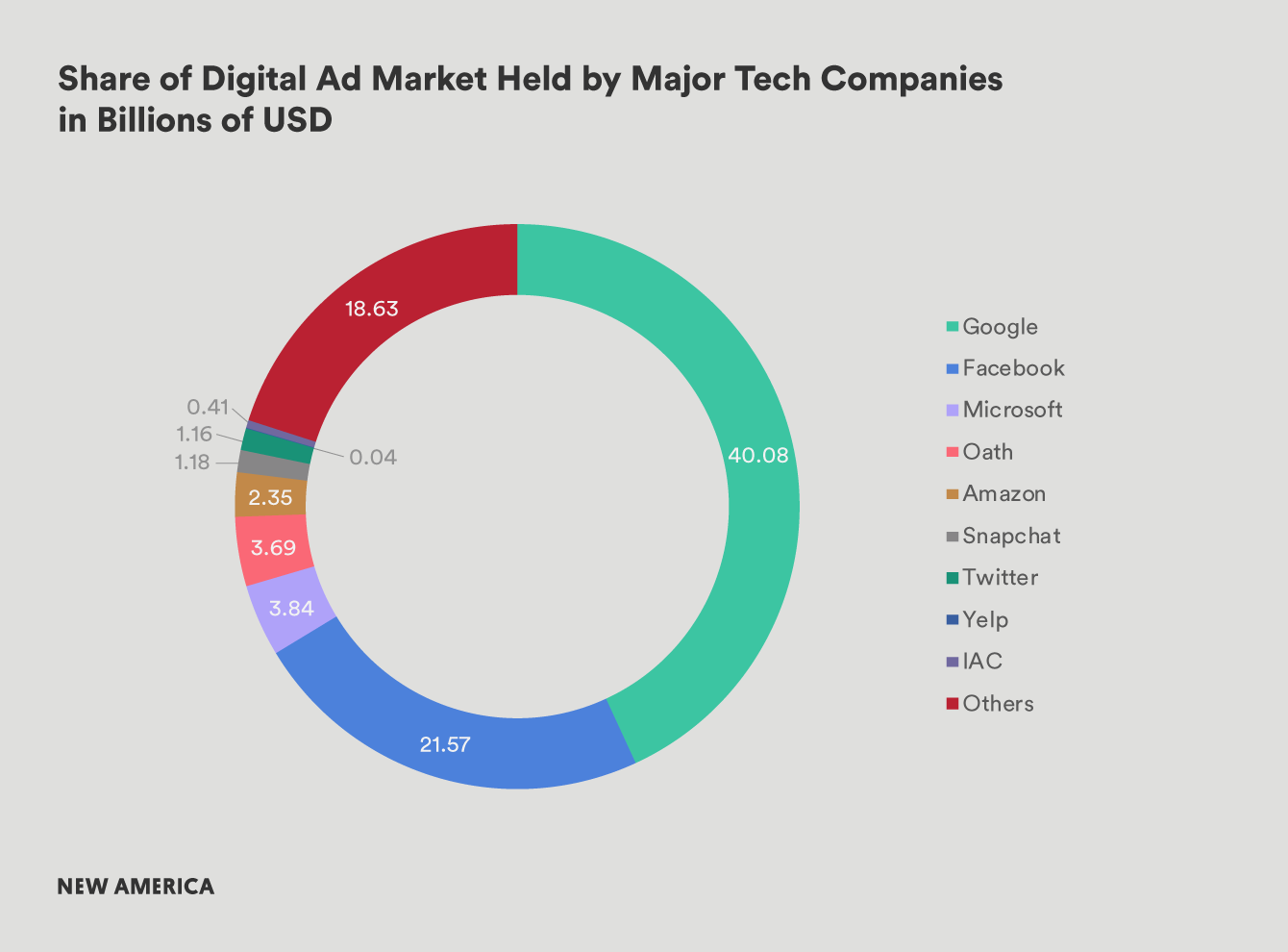

Digital policy expert Peter Swire offers a useful rubric to evaluate whether a company has achieved monopoly-scale market power.3 He offers four criteria: market share, essentiality of services, natural monopoly characteristics, and high consumer costs for exiting the market. In each of these categories, the tech platforms have met the standard. One company controls more than 91 percent of the global market in internet search,4 two companies control 73 percent of the digital advertising market,5 and one company operates the world’s two most popular internet-based, non-SMS text messaging applications.6 And to exit these markets, consumers pay a high price, particularly if they are long time users of the service.

This last point on the high cost of market exit—or switching costs, if there even exists a competitor that could offer a substitutable service—bears further consideration because it is directly related to the topic of the previous section on privacy. In these markets, most products are “free” in the sense that consumers need not pay in hard currency for access to the service. But instead, they must pay by trading their personal information for services; in other words, they pay a “privacy price.” Because there is little competition in these markets, and therefore little consumer choice, there is no option when a consumer becomes sensitive to rising privacy prices. These privacy prices are perfectly inelastic. No matter how much data Google or Facebook extract from users, no matter how that data is monetized, and no matter what level of transparency accompanies the user agreement, there is very little change in the user’s demand for the service.

The leading digital platform companies have mastered this basic microeconomic dynamic. This is why a failure to agree to the terms of service results in only one option for consumers: to not use the service at all. Following Swire’s logic, if the service is essential and the exit costs are high, then there is no choice at all. Consequently, the argument that the absence of consumer flight from the product is a market signal indicating satisfaction or indifference is an extraordinarily misleading fallacy. And placing the disinformation lens over this conundrum suggests the unsettling notion that to participate on the major internet platforms, consumers will necessarily be forced accept that political falsehoods shall be targeted at them.

No matter how much data Google or Facebook extract from users, no matter how that data is monetized, and no matter what level of transparency accompanies the user agreement, there is very little change in the user’s demand for the service.

Europeans have begun pressing the point that privacy and competition policy converge when a company with market power makes unreasonable demands for data-sharing in its terms of service. The German antitrust authority opened an investigation of Facebook’s practices last year, making precisely this case.7 Similarly, the GDPR provision that requires companies to offer meaningful, nondiscriminatory options for opting out of data sharing service agreements intends to address this reality as well.8 Indeed, one of the most high-profile lawsuits filed against the major technology companies in the wake of GDPR enforcement points to the failure of Facebook to provide meaningful alternatives to accepting all terms and conditions of use.9

Regardless of whether these companies are defined as monopolies, their market position justifies an increase in regulation and oversight to protect consumer welfare, especially on data privacy. There have to be meaningful options for privacy other than the binary choice of accepting whatever terms are offered by monopolies for essential services or exiting the market altogether, particularly given the obscure, misleading, or hard-to-find privacy options currently offered by some of the companies leading this sector.10 The policy ramifications implicate the need for both strong privacy policy enforcement as well as new forms of competition policy.

In light of this market and policy analysis, we see an urgent need to rethink competition policy as it applies to the technology sector. We believe the following measures, profiled in ascending order of ambition given current technological and political constraints, are necessary and promising opportunities for progress that demand further inquiry and examination in Washington and beyond. Most critically, we hope that these proposed measures can spark more robust discussion, research, and policy analysis.

Restrictions on Mergers and Acquisitions

There is an entire ecosystem of technology start-up companies that are built by their founders in hopes of being acquired for tidy sums by the dominant technology firms. And more visibly, the major technology firms have been overt in their strategy to acquire any competitive entrant that appears to gain market momentum (e.g. Instagram, WhatsApp, DoubleClick, YouTube, and Waze). This practice of acquiring competitors should be monitored and restricted. Looking back, it is clear that regulators should have been far more careful in assessing the potential of past mergers to result in market power and consumer harms. Any mergers that are permitted should be scrutinized and conditioned to restrict data-sharing between affiliates.11

Top 10 Acquisitions Over Past 10 Years for the 4 Major Internet Companies

Alphabet

| Company name | Price | Type | Date |

|---|---|---|---|

| Motorola Mobility | $12,500,000,000 | Device manufacturer | August 2011 |

| Nest Labs | $3,200,000,000 | Automation | January 2014 |

| DoubleClick | $3,100,000,000 | Digital advertising | April 2007 |

| YouTube | $1,650,000,000 | Video social media | October 2006 |

| HTC properties | $1,100,000,000 | Intellectual property | September 2017 |

| Waze | $966,000,000 | GPS navigation | June 2013 |

| AdMob | $750,000,000 | Digital advertising | November 2009 |

| ITA Software | $676,000,000 | Travel technology | April 2011 |

| Postini | $625,000,000 | Communications security | July 2007 |

| DeepMind Technologies | $625,000,000 | Artificial intelligence | January 2014 |

Amazon

| Company name | Price | Type | Date |

|---|---|---|---|

| Whole Foods Market | $13,700,000,000 | Supermarket chain | June 2017 |

| Zappos | $1,200,000,000 | E-commerce | July 2009 |

| Pillpack | $1,000,000,000 | E-commerce | June 2018 |

| Ring | $1,000,000,000 | Security technology | February 2018 |

| Twitch | $970,000,000 | Streaming video | August 2014 |

| Kiva Systems | $775,000,000 | Robotics | March 2012 |

| [Souq.com](http://Souq.com) | $580,000,000 | E-commerce | March 2017 |

| Quidsi | $545,000,000 | E-commerce | November 2010 |

| Elemental Technologies | $500,000,000 | Video technology | September 2015 |

| Annapurna Labs | $370,000,000 | Microelectronics | Jan-15 |

Apple

| Company name | Price | Type | Date |

|---|---|---|---|

| Beats Electronics | $3,000,000,000 | Electronics and music streaming | August 2014 |

| NeXT | $404,000,000 | Hardware and software | February 1997 |

| Anobit | $390,000,000 | Flash memory | December 2011 |

| AuthenTec | $356,000,000 | Security | July 2012 |

| PrimeSense | $345,000,000 | Scanners | November 2013 |

| P.A. Semi | $278,000,000 | Semiconductor technology | April 2008 |

| Quattro Wireless | $275,000,000 | Digital advertising | January 2010 |

| C3 Technologies | $267,000,000 | Mapping | August 2011 |

| Turi | $200,000,000 | Machine learning | July 2009 |

| Lattice Data | $200,000,000 | Artificial intelligence | May 2017 |

| Company name | Price | Type | Date |

|---|---|---|---|

| $19,000,000,000 | Mobiel messaging | February 2014 | |

| Oculus VR | $2,000,000,000 | Virtual reality | March 2014 |

| $1,000,000,000 | Social media | April 2012 | |

| LiveRail | $400m-500,000,000 | Digital monetization platform | August 2014 |

| [Face.com](http://Face.com) | $100,000,000 | Facial recognition | June 2012 |

| Atlas Solutions | <$100,000,000 | Digital advertising | February 2013 |

| Parse | $85,000,000 | Application development tools | April 2013 |

| Snaptu | $70,000,000 | Mobile application | March 2011 |

| Pebbles | $60,000,000 | Augmented reality | July 2015 |

| FriendFeed | $47,500,000 | Social networking | August 2009 |

Moreover, merger review should explicitly consider not only the concentration of horizontal market power but also the concentration of data that enables competitive advantage in multiple adjacent market segments. For example, in the case of Facebook’s acquisition of Instagram, a case can be made that these services address different markets. However, the user data they collect that informs ad-targeting decisions is firmly in the same market, and more importantly, it is the market where most of the revenues are generated.

The most effective route for a Silicon Valley firm to profile individual users is to collect as much data as possible from as many sources as possible to create a comprehensive store of data that takes advantage of inferential redundancies to affirm the individual’s behavioral preferences with greatest confidence and also eliminate any inaccuracies raised by misleading outlier activity data. If data is a source of primary value in the modern economy, then it should be a significant focus of merger review.

In addition, we would suggest an inquiry focused on the vertical integration of tracking and targeting services. The largest abuses of market power that appear to drive privacy violations, political polarization, cultural radicalization, and social fragmentation are rooted in the combination of data tracking and audience targeting within a single business. This is particularly true for companies that possess tremendous amounts of data collected through the primary service (i.e., “on-platform” collection) but generate substantial marginal value atop that by aggregating data collected outside the service and buying it from third party vendors (i.e., “off-platform” collection).

If data is a source of primary value in the modern economy, then it should be a significant focus of merger review.

To conduct this analysis and regulatory review effectively, it is likely necessary to put a value or price on personal data. It is clear that the industry makes these calculations (as do their investors) when they review an acquisition or merger proposal. Regulators must also do so in order to generate relevant standards of review. One way to test this theory would be for regulators to study mergers approved in years past that received limited scrutiny and have since resulted in apparent increases in market power. These might include Facebook-Instagram, Facebook-Whatsapp, Google-DoubleClick, and Google-YouTube. Experts can look at changes in the market post-merger to determine the effect on price, market share, and consumer choice. By applying a standard of review pegged to the concentration of value in data and aggregated consumer attention that national regulators previously missed in these cases, we may discover ways to build a generally applicable rule that better protects consumers from anticompetitive commercial behaviors for the future.

Antitrust regulators can also specifically look to apply heightened privacy and security restrictions on certain firms. For mergers and acquisitions made in particular sectors, as in the case of BIAS providers acquiring media properties or advertising technology firms, there could be tailored restrictions that treat the problem of privacy in this especially sensitive context. For instance, BIAS providers seeking to close such acquisitions could be required to abide by tailored regimes to protect consumer privacy and security like the broadband privacy rules promulgated by the Obama FCC. In a similar example, firms that participate in the digital advertising ecosystem could be required not to link any shared or acquired data with any persistent identifiers.

The underlying goal here is to make space for competitive service providers to challenge the market dominance of the large platforms by offering new products—including those that privilege truly protective consumer privacy as a feature.

Antitrust Reform

From its origins, this country has been governed with strong anti-monopoly views; as far back as 1641, the legislature of the Colony of Massachusetts decreed: “There shall be no monopolies granted or allowed among us but of such new inventions as are profitable to the country, and that for a short time.”12 The primary mode of antitrust regulation in the United States correspondingly became rooted in maintaining competition in the market, and it is the underlying theory of structural economics that significantly influenced what came to be known as the Harvard School of antitrust, which held that a market tending toward monopoly or oligopoly could result in societal harm because such concentration in the market would afford firms excessive power over other societal entities.13

In short, concentrated markets could lead to anticompetitive behavior, collusion, barriers to market entry, and consumer harm, such as raising prices, lowering quality of products and services, limiting the variety of offerings, and lowering capacity for innovation. Corporate power could also lead to predatory pricing schemes and the diminishing of competitive forces in the market more generally. The harms to the public would then include lower wages, the creation of fewer novel enterprises and innovations, and increased political clout among the monopolistic class in a way that might threaten democracy. The Harvard School’s goal was thus to premise regulation and enforcement on the structure of a market to protect competition and public welfare.

The influence of the Harvard School’s theory of antitrust, dominant for most of American history, has waned in the last few decades. In its place has risen the Chicago School of antitrust enforcement.14 It does not premise antitrust enforcement on the idea that the accumulation of market power allows the firm to engage in anticompetitive behaviors and that if it does, then the firm should be scrutinized. The new school of thought argues that enforcement should only come into consideration if a clear harm to consumer welfare can be established. In the Chicago School, that means basically only one thing: increased prices. The support for this new style of approach from all corners of the federal government, in part on the basis of Robert Bork’s well-known writings on antitrust reform,15 established it as the framework of choice for regulators throughout the 1970s and 1980s.

As many scholars have documented, this regime, still largely in place today,16 is broken.17 It creates arbitrary boundaries for regulatory jurisdiction. A firm that limits choices for consumers can be just as (or more) harmful to the consumer as another that hikes prices; both practices diminish the consumer’s value for money. To require that antitrust enforcement officials premise their decision-making primarily on whether or not consumer welfare has been harmed on the sole basis of price increases is to miss the point that a firm’s presence and activity in the market is expressed through many variables, not exclusively consumer prices, and that the consumer suffers if any of these variables works against the interest of the consumer.

And indeed, it is clear now that the United States has missed the point. The near-required premise that antitrust regulators must establish harm to consumer welfare as evidenced by price hikes has apparently failed as the national economy has undergone the influences of rapid globalization. And when we consider the case of internet platforms in particular, it becomes quite difficult to find a way to address any anticompetitive behaviors in which they engage since many of them do not charge prices for their services or undercut the alternatives.

As a result, the march to market power in the tech industry has been largely unimpeded. These firms have become so large and valuable that they resist conventional instruments of oversight. Even in cases when regulators take aggressive action against anticompetitive practices (such as tying arrangements), it does not appear to create a disciplinary impact on the market. Consider the EU’s recent announcement of a record fine against Google—$5 billion on top of last year’s $2.7 billion fine—for violating competition standards in Europe. Despite these setbacks, Alphabet’s stock price continues to rise as investors seem to shrug this off as a cost of doing business.18

It becomes difficult to find a way to address any anticompetitive behaviors in which internet platforms engage since many of them do not charge prices for their services or undercut the alternatives.

But are the leading internet brands causing consumers harm in any way? To see one of the most important and devastating examples of this harm, we need only connect back to the topic of digital disinformation and its distortion of the public sphere. For all of the reasons we have documented here (and elsewhere),19 the concentration of market power in digital advertising and information distribution has catalyzed polarization and irrationality in our political culture. But the problem is not simply about the elevation of low quality information, it is also about the decline in high quality information. To put it mildly, the public service news industry did not adapt well to the disruption of the internet, the displacement of print media as a profitable service, and the rise of platforms as aggregated distributors of digital content. With some notable exceptions (e.g. The Economist), the rising fortunes of Google and Facebook have coincided with a catastrophe for traditional news businesses.

A full account of why this happened and who bears ultimately responsibility is a beyond the scope of this essay. The point we want to make is straightforward: The accumulation of market power in the aggregation of news content in search and social media (for a zero price) together with the domination of the digital ad market (and the vast disparity of digital ad prices compared to print) has left the news industry with no path back to the profit models they enjoyed for nearly a century.

Whether we choose to read this history of the present as negative market externalities that accompanied a technological paradigm shift or the predatory pricing of digital platform monopolies, the public harm is clear as day: There are fewer journalists working today and less quality news in distribution than there once was—and as a society already in political tumult, we could not afford any decline at all. While it would not be fair to lay all of the blame on Silicon Valley’s largest firms, it would be equally foolish to ignore the role they have played in weakening the 4th Estate and the responsibility they carry to help address this public problem. Hearkening back to the Harvard School, it is the role of antitrust regulators to protect the public from both the direct and the indirect harms of concentrated market power.

The rising fortunes of Google and Facebook have coincided with a catastrophe for traditional news businesses.

What do those harms look like exactly? Traditional journalistic organizations all over the United States, including major outlets such as the Seattle Post-Intelligencer, San Francisco Chronicle, and Detroit Free Press, have all drastically reduced their services in recent years. The news hole they have vacated is not empty, it is filled with all manner of content that Facebook and Google algorithms deem to be the most relevant. But relevance is not the same as quality. Nor does it begin to replace the social contract established in the commercial news industry a century ago that sought (however imperfectly) to balance commerce with public service—a commitment from which consumers continue to benefit every time they pick up the newspaper, watch a television journalist, or visit a news website. On platforms like Facebook and Google, meanwhile, money rules over all else, expressed through the sale of aggregated attention to the end showing the consumer a relevant ad. This reality has engendered the dangerous forms of disinformation which now pervade over these platforms.

National policymakers and the public will require far more open scholarship on these matters to determine what the appropriate direction and dosage of regulatory or legislative action should be. But we must begin with a more thorough economic analysis of the current market structure in this information ecosystem. We see two areas of significant potential for competition enforcement officials as they consider the market power of internet platforms: to subject them to stricter antitrust reviews, and to apply stricter regulations on their business practices. Both sets of measures may be appropriate and necessary to adequately replace power in the hands of the individual consumer.

In regard to stricter antitrust reviews, we see great promise in empowering regulators to pursue enforcement against the industry on the basis of predatory pricing.20 While the leading internet firms’ style of predatory pricing—in offering zero-cost services or intellectual offerings at cut prices on the strength of the backing of the institutional investment community—carries a starkly different flavor from the schemes of the past in more traditional industries, it is predatory nonetheless and likely diminishes competition. And as the major platform companies offer a zero-price service, a clear externality is their indifference (and abdication of editorial responsibility) to maintaining a commitment to the veracity of the content shared on their platforms. This meanwhile contributes to an information ecosystem that is plagued by vastly decreased journalistic capacities at a time when the public requires far better access to the truth.

Scholars and critics have furthermore contested that antitrust officials can and should pursue vertical integrations of firms in the digital ecosystem.21 We agree with this perspective. As discussed above, the business model emerging amongst firms that have for the most part been thought of as internet service providers—among them Verizon, Comcast, and AT&T—is progressively gravitating toward the dissemination of new media content and digital advertising. This combination of business practices at successive regions of the value chain presents a difficult challenge to the individual consumer’s autonomy and privacy from the industry, and is one that requires further investigation, particularly in an era where the federal regulatory agencies largely lack a foothold to pursue these types of integration.

On platforms like Facebook and Google, meanwhile, money rules over all else, expressed through the sale of aggregated attention to the end showing the consumer a relevant ad.

We are similarly concerned about the accumulation and cultivation of personal data pursued by the leading internet firms as well, Facebook and Google among them. Both of these firms have sought to purchase other internet properties, thus closing horizontal mergers with brands like Waze and WhatsApp, and subsequently share consumer data collected throughout their universe of apps so as to compile behavioral profiles on individuals across their services. This carries with it certain privacy risks; consumers are often not aware that their YouTube viewing data could be shared with Waze to inform ad-targeting on the navigation service.

But perhaps even more critically, this ongoing accumulation and amalgamation of data—which is done purely for Google’s commercial purposes—places Google in a position of power; its surveillance operation, powered by Alphabet’s incredible wealth, reach and market power, can allow it to identify gaps in the market sooner than anyone else and pursue them in an anticompetitive manner. This is indeed among the concerns that were raised when Google infamously announced in 2012 that it would be reformulating its user privacy commitments into a single policy that would apply across the majority of its services.22 Intimations that Facebook was exploring data-sharing arrangements with its subsidiary WhatsApp, which have variously since been confirmed23 and may have led to the departure of WhatsApp’s founders,24 show that this sort of combination of data profiles from different services is a problem that is not restricted only to Google.

As antitrust regulators consider the case of internet firms, there is a menu of regulatory mechanisms (beyond the merger and acquisition measures discussed in the previous section) that can be pursued in contexts such as reviews of monopoly power, vertical integrations, acquisition proposals, or others to restrict the potential for harmful anticompetitive behaviors in the industry. Some of these include the following, presented here in no particular order.

- Maintain commitments to past policies, including privacy restrictions: Firms could be required to abide by all privacy policies, terms of service, and other publicly disclosed commitments to users if they wish to acquire smaller entities and broaden their reach in a horizontal market. Such a measure, if applied in the case of a merger or acquisition, can obviate situations where a firm like Google extracts data from the acquired firm like DoubleClick to further strengthen its dominance in a given market.

- Require transparency in data management practices: As we argue elsewhere, transparency is not an antidote to consumer concerns like privacy, but it is a feature that can nonetheless have great impact if influencers come to understand the inner workings of the industry. To that end, antitrust officials could require certain monopolistic, vertically integrated, or merging entities to disclose any and all data management practices to the public or to the regulatory agency. If such a requirement is difficult to impose, antitrust officials could at a minimum require that only certain data sharing arrangements taking place within the firm’s silos in particularly concerning ways be disclosed to regulatory bodies. Such conditions can enable agencies like the Antitrust Division to monitor the firm’s data practices and determine whether or not it is impeding third-party access to its platform services such as advertising networks or media properties in an anticompetitive manner.

- Assure government rights to review, investigate, and enforce: Antitrust officials can establish conditions whereby if a firm presents particularly concerning challenges to market competition, or they permit a merger or acquisition to close, they will reserve the right to review the entity’s compliance with all rules and regulations it is subject to. Additionally, officials can demand that they be afforded the right to access any relevant proprietary information and interview any key personnel should they wish to understand more about the merged firm’s business practices.

- Require support of a public media trust fund: The government could organize—and antitrust officials could require subject firms’ support of—a public media trust fund that redistributes contributions to journalistic organizations. The idea, raised by various scholars, can go a long way in restoring the strength of failing businesses that have a public interest quality to them including local journalistic outfits.

- Examine utility-style regulation to counterweight market abuses: The idea scholars have proposed that the leading internet platforms should be regulated in a manner similar to public utilities deserves serious attention. This sort of measure would require as a premise an evidentiary finding that the internet companies that should fall under such scrutiny are indeed monopolies or form a part of a tight oligopoly in particular market segments. Such a development could impart immense benefits to the modern information ecosystem if some kinds of nondiscrimination requirements were applied with circumspect rigor. Given the dominance that companies like Google and Facebook enjoy in the market for information consumption, the public may well benefit from implementation of new rules that notionally require that the platforms limit the ways they give preferential treatment to their own products and services. The EU’s challenge of Google’s promotion of its own shopping services serves as an example of the type of impact such a mode of regulation could have.

As difficult as it may be to achieve such reforms of our antitrust regime given the current political environment, pursuing this level of scrutiny to maintain sound competition policies can significantly blunt the capacity for anticompetitive behaviors in the industry, and as a result, enable and, in time, assure heightened stability and health of the electorate’s information ecosystem.

Robust Data Portability

The market for digital media is premised on gathering personal data, building detailed behavioral profiles on individuals, and extracting value by selling advertisers targeted access to those users. There are very limited consumer choices in this market and high barriers to competitive entry for alternative service providers. These circumstances offer a clear case for policies that mandate data mobility or portability. This is true for many adjacent markets in e-commerce as well. According to the logic of “winner-take-all” network effects in the data economy, we should expect to see more of this trend. In this market, consumers trade data for services (or give data in addition to money), but they reap only a marginal reward for the value of that data (e.g. more relevant ads). The lion’s share of the value from the data stays with the large data controllers. Consequently, when we consider structural solutions to the problem of data-driven filter bubbles, we are led logically to engage the question of how to distribute the value in the data economy more equitably.

The starting point here is data portability, an idea enshrined in the EU’s GDPR as well as California’s new data privacy law.25 At the minimum, consumers should be able to have a copy of all data stored about them by a service provider. But critically, we would add that consumers should have access not only to user-generated content, but to the data that is generated about them by that company (which is often more valuable than user-generated content because it is combinatorial data linked to a wide variety of tracked user behaviors and interactions with other users). This is not about data ownership; it is about how individuals can exercise rights to control their digital identities; that is, to direct and protect their own personal information and benefit from the economic value generated from it, thus affording them the capacity to shape their digital personalities in the ways they wish to shape them.

The lion’s share of the value from the data stays with the large data controllers.

This is also not solely about privacy. It is about the distribution of value in the digital and data economy. If the future marketplace is dominated by machine learning algorithms that rely on the “labor” of personal data to turn the engine of pattern recognition, knowledge generation and value creation, then it follows that individuals should be empowered to have as much control as possible over the data that matters to them, that defines their identities to other parties, and which powers these facets of the modern economy.26

Today, data portability offered by leading internet companies has extremely limited value because the data that these firms choose to make available is largely incomplete and not usefully formatted. Further, there are few if any competitors that might even try to use it, either because they do not have the capability to do so or because they do not see the economic value. Notably, there are some (perhaps counterintuitive) signs within the companies that this could change. The recent announcement of the Data Transfer Project (DTP)27 is very interesting. It is a project that brings Google, Facebook, Twitter, and Microsoft in a partnership to create a common API that permits users to move data between these service providers. So far, the project has limitations. It is in a very early stage and not yet ready for wide scale use. Exactly what data is given for transfer isn’t clear. And the way the project is described suggests the creators weren’t thinking about data portability as a hallmark feature of digital consumer behavior, but rather as an infrequent but important need to switch service providers.28 Nonetheless, the appearance of the DTP shows that a more decentralized model of data management is not impossible under the current system, and element sof it might even be embraced by the large platforms.

What we propose here goes considerably beyond what DTP imagines. If we established a general right to robust data portability, expanded the concept of API-based inter-firm data exchange in the DTP with global technical standards, and built on that idea to fundamentally restructure the market, the resultant positive change for consumers would be inordinate.

Data portability offered by leading internet companies has extremely limited value because the data that these firms choose to make available is largely incomplete and not usefully formatted

Consider the potential for competitive market entrants if users were able to move to alternative service providers carrying the full value of their data, including the analytical inferences generated about them based on that data. Consider the value (in services and compensation) that users might unlock if they could reassemble data from every company that tracks, collects or stores data about them or for them into a user-controlled data management service. Consider the rebalancing of asymmetrical market power if these data management services could act on behalf of users to engage automatically with data controllers of all kinds to ensure data usage limits are held to a pre-chosen standard rather than the defaults offered in user agreements. Consider the possibilities that might emerge if users on one platform could reach users on a competitive service through a common application programming interface. Consider how users could choose to pool data with others (of their own volition) and create collective value that might be transferred to different platforms for new services or monetized for mutual gain. There are significant technical and data privacy challenges to making this a reality—in part because some of the value of one individual’s data lies in the ways in which it is combined with another’s data—but it has enormous potential.

As a thought experiment to explore new ideas and policy proposals, we offer the provocative proposal for data portability that follows. We believe some approximation of this concept would create substantial competitive pressure in the market with myriad potential benefits. But specific to the focus of this analysis, a change in market structure of this type would act to curb the negative externalities of data markets that are driving the proliferation of disinformation. Here is how it might work.

- Define the Market: Establish a legal definition for data controllers or data brokers—commercial firms of a certain size that collect, process, and commercialize personal information as a direct or indirect part of their business.

- Establish Individual Data Rights: These rights would include full transparency about the nature and scope of personal data collected, processed, shared or sold by the data controller. It would include access to the personal data given by the individual to a data controller as well as the data generated by the data controller about the individual. It would include the right to view, delete, or revise this data. And it would permit all individuals to set the conditions for the type of data collected, the uses to which it may be put, the terms of sharing and commercialization, and the frequency of consent required. (These rights map to the standards described in the previous section.)

- Portability: All data controllers would be required to make it possible for users (upon request) to access, copy, and port their data through a simple API. The format of ported data should be standardized so that ported data can be aggregated by the individual into a digital “data wallet” that should be machine-readable so that other data collectors can process the data should the individual wish to share personal data with them.

- Data Management Service Marketplace: Because it is unreasonable to expect that all consumers will have the capacity and capability to manage all of the data that they might copy and port to their data wallets from all of the dozens of data controllers with whom they interact, it will be necessary to establish a market for Data Management Services (DMS) that have regulated standards for security, privacy and interoperability. Similar to the way robo-advisors use software to manage investment portfolios based on a set of user-defined preferences (taking on the burden of interfacing with complex financial service markets), a DMS will manage data assets for individuals. The DMS will have a set of defaults for data rights in accordance with the law and will permit users to adjust those settings to match their preferences for data sharing. The DMS will automatically interface with the complex terms of service provided by data controllers and manage opt-in/opt-out settings (or reject service altogether) in accordance with the individual’s pre-set preferences. In order to ensure that all individuals can exercise their data rights, it may be worthwhile to consider a lightweight “public option” DMS to which all citizens are automatically enrolled. Notably, such a system could also offer substantial efficiencies for streamlining and digitizing government services.

- Intermediary DMS Marketplace: On top of the public DMS system will be a secondary commercial market. This market will have access through an API to the underlying DMS service. It will permit private sector companies to offer innumerable commercial applications and services that individuals may choose in real time or through their pre-set preferences. Some will help users monetize their own data. Others may seek to group consenting users into aggregate data sets that optimize value. Others may permit easy switching between competitive service providers. Some may sell enhanced privacy protection or anonymity. The core concept is to leverage competition to put the user rather than the data controller in a position of greater control.

This imaginative scenario contains a variety of assertions and leaps of political will, policy change, technical development, market cultivation, and user acclimation. There are also some questions we purposely leave on the table for discussion regarding privacy protection, cybersecurity, and administration.

We are keenly aware that a new data management market that assembles personal data into easily accessible, decentralized packages raises serious questions about vulnerability. Yet, as blockchain scholars and various other security researchers have ably demonstrated, the decentralization of personal data from Silicon Valley to the individual need not mean it is insecure. Further, the intent here is not to present this concept as a fully developed proposal, but rather to spark a debate about competing ideas to redistribute the value of individual data more equitably in our society and in the process to generate competitive pressures that will limit the negative externalities of the current market that are weakening democracy.

We are experiencing the greatest concentration of wealth in capitalism in a century, and it is built on the value of aggregated personal data. We need bold proposals for change. And we need proposals that reduce inequalities without choking technological innovation or losing the utility of data analytics and network effects. The policy architecture presented here is a provocation to open that discussion to a wide range of possibilities. We plan to pursue this idea further in subsequent research to explore more precisely how it might work, what nascent industry efforts align with this concept, and the ways in which market forces like these could facilitate public benefit.

Citations

- Om Malik, “In Silicon Valley Now, It’s Almost Always Winner Takes All”, New Yorker, December 30, 2015.

- This summation of network effects and the so-called “winner take all” market phenomenon is common to most scholarship and commentary about the contemporary tech oligopoly. It is nicely portrayed in Patrick Barwise, “Why tech markets are winner take all,” LSE Business Review, June 16, 2018.

- Peter Swire, “Should Leading Online Tech Companies be Regulated Public Utilities”, Lawfare Blog, August 2, 2017.

- “StatCounter: Global Stats”, Statcounter, July 2018.

- Jillian D’Onfro, “Google and Facebook extend their lead in online ads, and that's reason for investors to be cautious,” CNBC, December 20, 2017.

- “Most popular global mobile messenger apps as of July 2018, based on number of monthly active users (in millions)”, Statista, 2018.

- Bundeskartelamt “Preliminary Assessment in Facebook Proceeding,” December 19, 2017.

- See, e.g. EU General Data Protection Regulation, Articles 5, 6, 7, 9, 12 & 15 as well as Recitals 63 & 64.

- See, Complaint of NOYB against Facebook, May 25, 2018.

- “Facebook and Google use 'dark patterns' around privacy settings, report says”, BBC, June 28, 2018.

- This call for deeper scrutiny of acquisitions has been treated at length by other sources, see, e.g. Tim Cowen and Phillip Blond, “‘TECHNOPOLY’ and what to do about it: Reform, Redress and Regulation”, Respublica, June 2018.

- William Letwin, Law and Economic Policy in America: The Evolution of the Sherman Antitrust Act, University of Chicago Press, 1956.

- Robert D. Atkinson and David B. Audretsch, “Economic Doctrines and Approaches to Antitrust,” Information Technology & Innovation Foundation, January 2011.

- Richard Posner, “The Chicago School of Antitrust Analysis,” University of Pennsylvania Law Review, Vol. 127, No. 4, April 1979.

- Robert Bork, The Antitrust Paradox, Free Press, 1993.

- This, for the most part, is true, though the U.S. regulatory community has variously shown an interest in other means of enforcement, including in the Federal Trade Commission’s Horizontal Merger Guidelines released in 2010.

- E.g., Lina Khan, Amazon’s Antitrust Paradox, Yale Law Journal, Vol. 126, No. 3, January 2017; Franklin Foer, World Without Mind: The Existential Threat of Big Tech, Penguin Press, 2017.

- Hayley Tsukayama, Alphabet shares soar despite hit to profit from Google’s European Union fine, The Washington Post, July 23, 2018.

- Dipayan Ghosh and Ben Scott, “Digital Deceit, The Technologies Behind Precision Propaganda on the Internet,” New America and the Shorenstein Center for Media, Politics and Public Policy, Harvard Kennedy School, January 2018.

- Nitasha Tiku, How to Curb Silicon Valley Power—Even With Weak Antitrust Laws, WIRED, January 5, 2018.

- See, e.g., “Should regulators block CVS from buying Aetna?,” The Economist, November 7, 2017; William A. Galston and Clara Hendrickson, “What the Future of U.S. Antitrust Should Look Like,” Harvard Business Review, January 9, 2018.

- Jon Brodkin, Google’s new privacy policy: what has changed and what you can do about it, Ars Technica, March 1, 2012.

- Chris Merriman, WhatsApp and Facebook are sharing user data after all and it's legal, The Inquirer, May 24, 2018.

- Nick Statt, WhatsApp co-founder Jan Koum is leaving Facebook after clashing over data privacy, The Verge, April 30, 2018.

- European Commission, “GDPR Article: 20”, Official Journal of the European Union, April 27, 2017.

- For more on this concept, see, e.g. Pedro Dominguez, The Master Algorithm.

- source

- See DTP White Paper, source. The paper recommends against federating data from multiple service providers into a Personal Information Management System (for sensible reasons of cyber-security), but this also indicates that the DTP only contemplates a portion of the concept proposed here.