Table of Contents

Borrowing for Non-Tuition Costs and Other Factors

While family income and institutional sector are critical to understanding student borrowing decisions, there are many other factors of interest. The following section highlights variation in the share of students who borrow and how those loans are allocated across tuition and non-tuition expenses according to a student’s race and ethnicity, degree type pursued, enrollment intensity, and residency status.

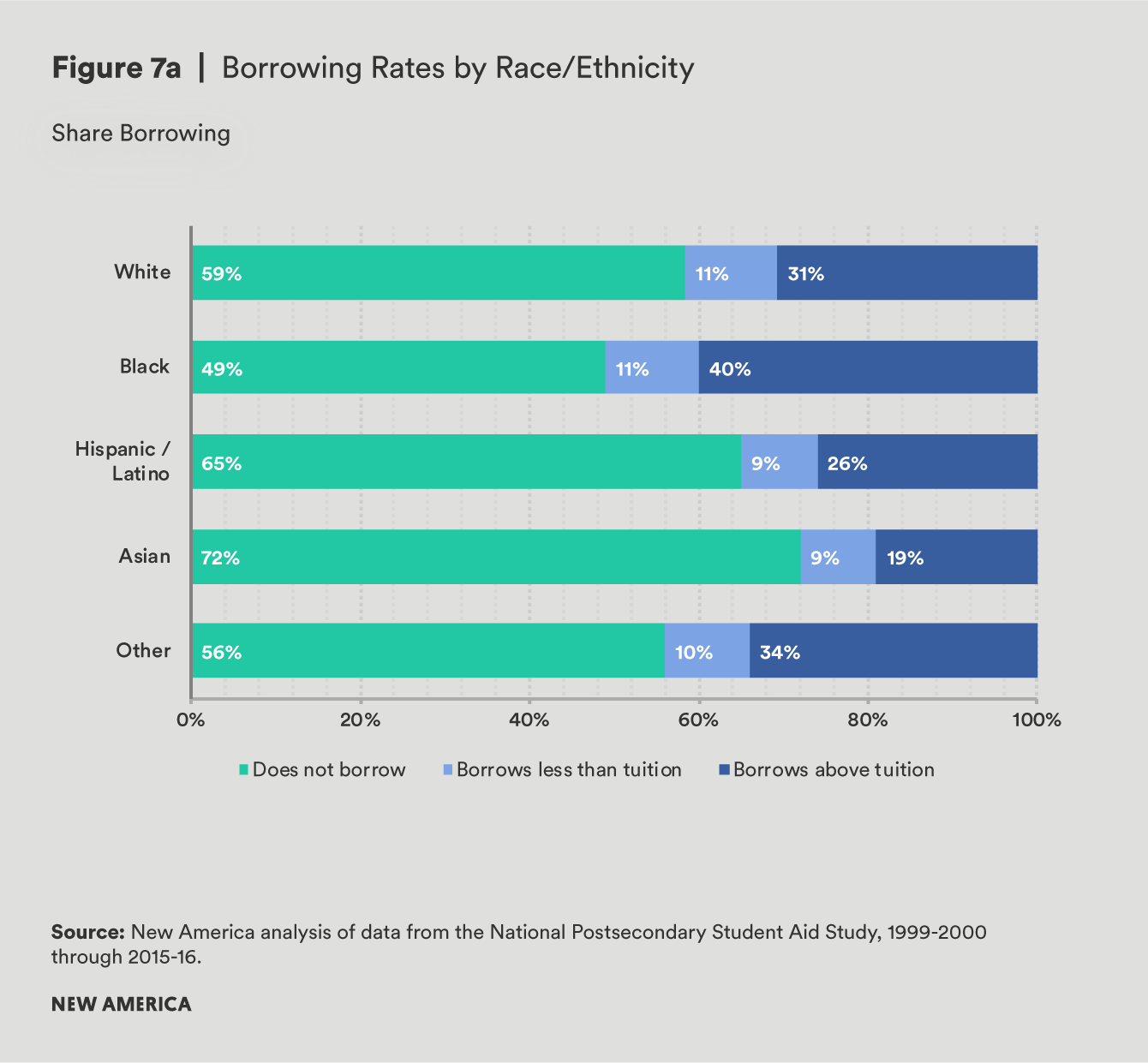

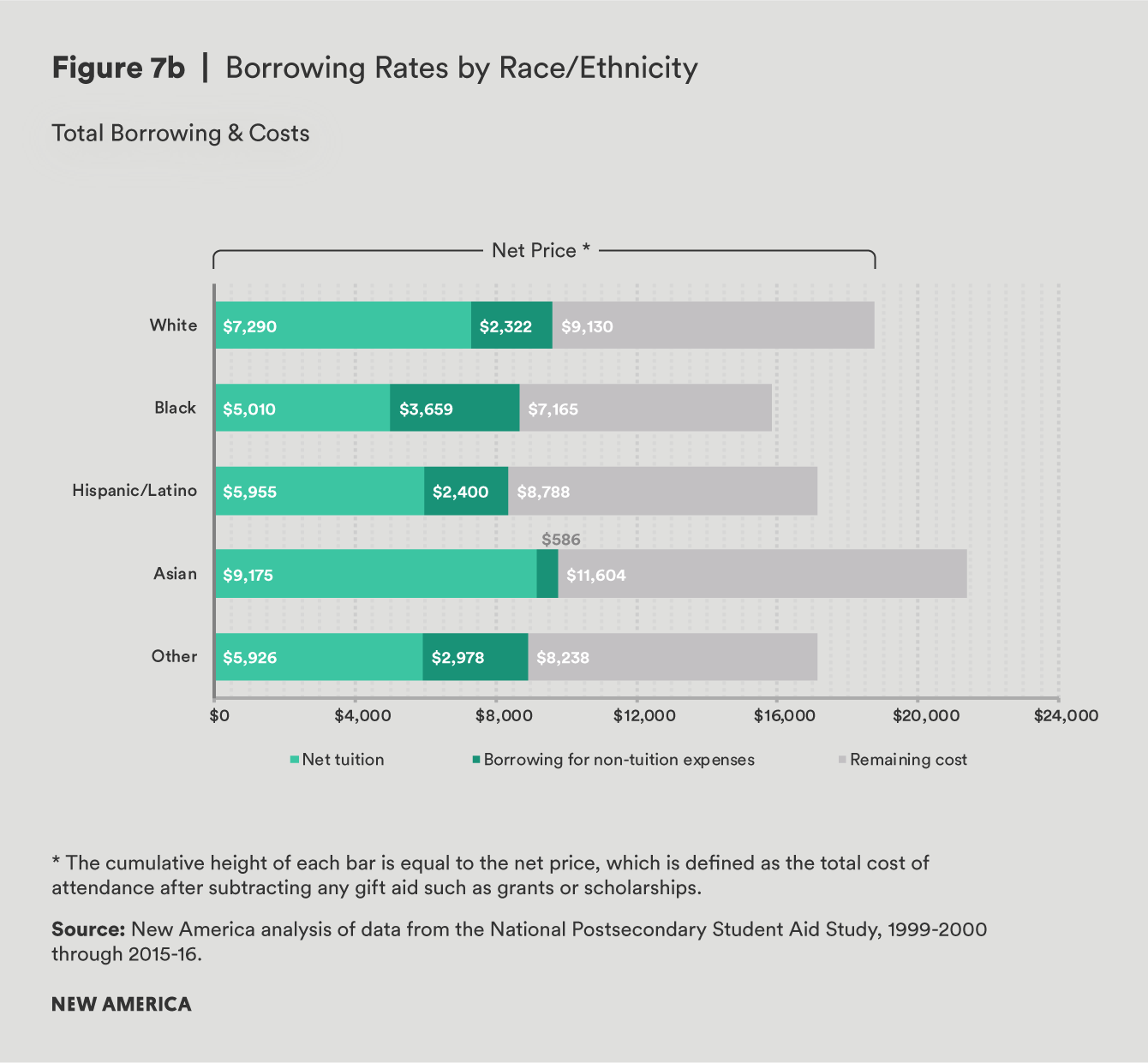

Race/Ethnicity

Black students were significantly more likely than any other racial or ethnic group to borrow for their education, but they are also far more likely to borrow in excess of the net price of tuition. In contrast, Asian students—the group which borrowed the least often—were also the least likely to borrow in excess of tuition. For white and Hispanic students, the share of students borrowing overall and the share borrowing above the cost of tuition were comparable.

While there is wide variation in the rate at which students from different ethnic and racial groups borrow, among those who do, there is only a slight range in average annual loan amounts, from a low of $8,395 for Hispanic borrowers to a high of $9,761 for Asian borrowers. Upon closer inspection, however, there are key differences in the amount borrowed for non-tuition expenses among these groups. On average, black borrowers use more than $3,600 of their total loans for non-tuition costs, compared to white and Hispanic borrowers, who take out more than $1,000 less for their non-tuition expenses. At the low end, Asian students borrow only $586 for their non-tuition expenses.

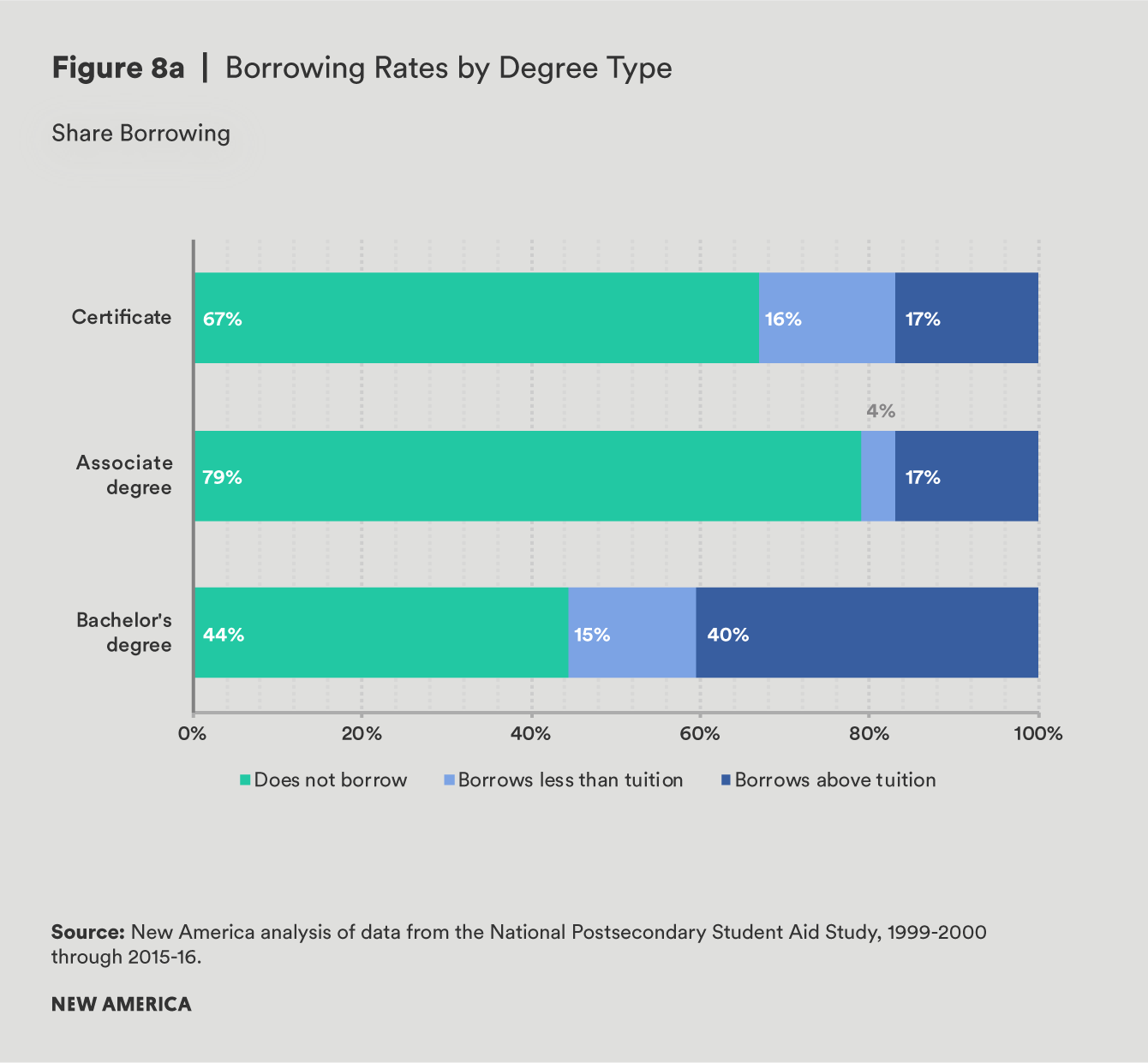

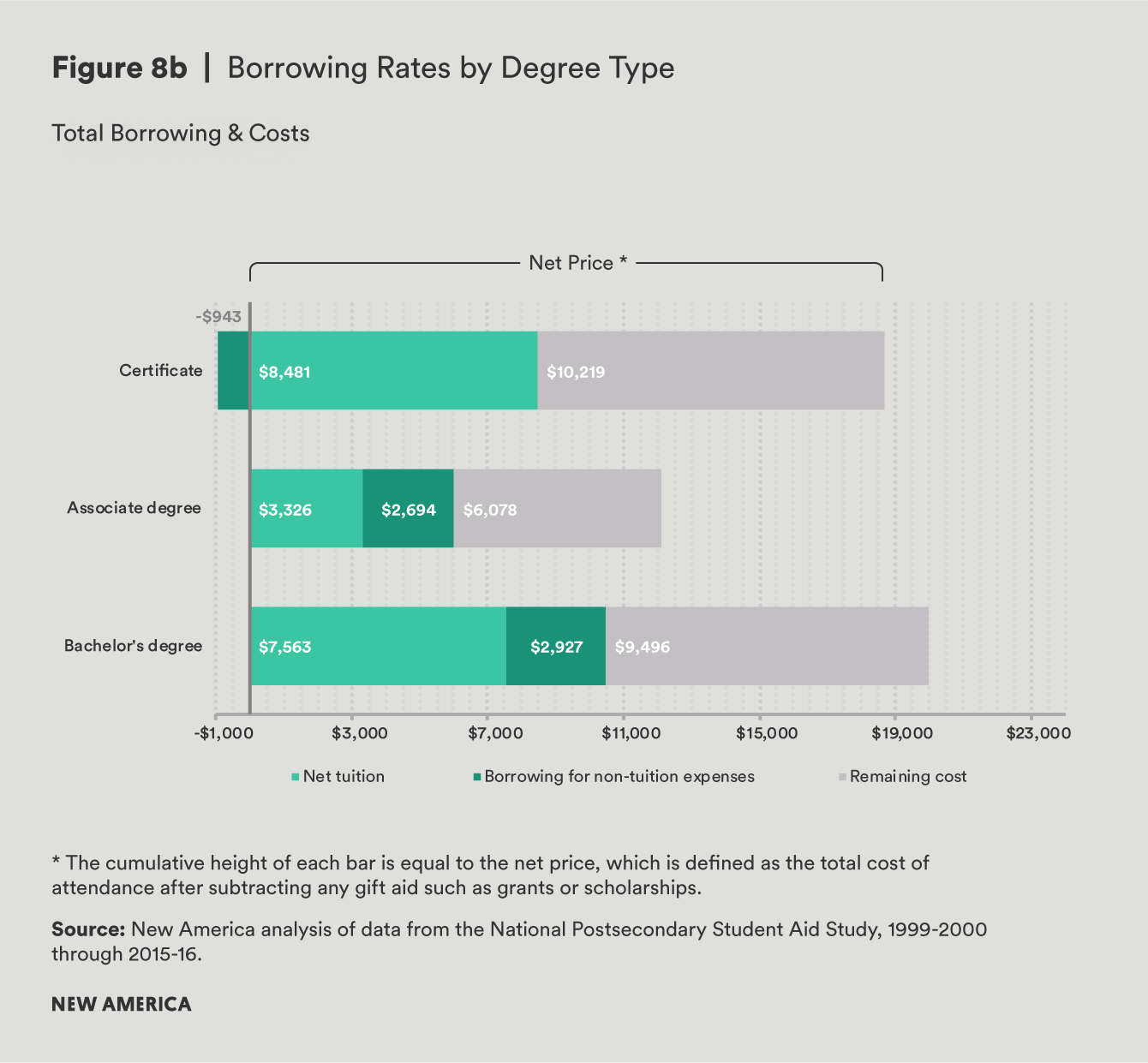

Degree Type

A larger share of bachelor’s degree-seeking students borrow compared to other degree levels, followed by certificate-seeking students, and then associate degree-seekers, who borrow at the lowest rates. Notably, although a smaller share of students borrow, those in associate degree programs are just as likely to borrow in excess of their net tuition price as those enrolled in certificate programs.

Overall, students in bachelor’s degree programs are not only far more likely to borrow, but they are also the largest share of students to borrow above the price of tuition. Whereas 40 percent of students pursuing a bachelor’s degree borrow more than they pay in tuition and fees, only 17 percent of students in an associate or certificate degree program do so. This is true despite the fact that the net prices students pay are actually higher for certificate-seeking students than those in bachelor’s degree programs. The average bachelor’s degree-seeking borrower takes out several thousand dollars more, yet pays less in tuition and fees than the average certificate-seeking borrower. As a result, the amount that can be attributed to non-tuition costs is higher for bachelor’s degree students.

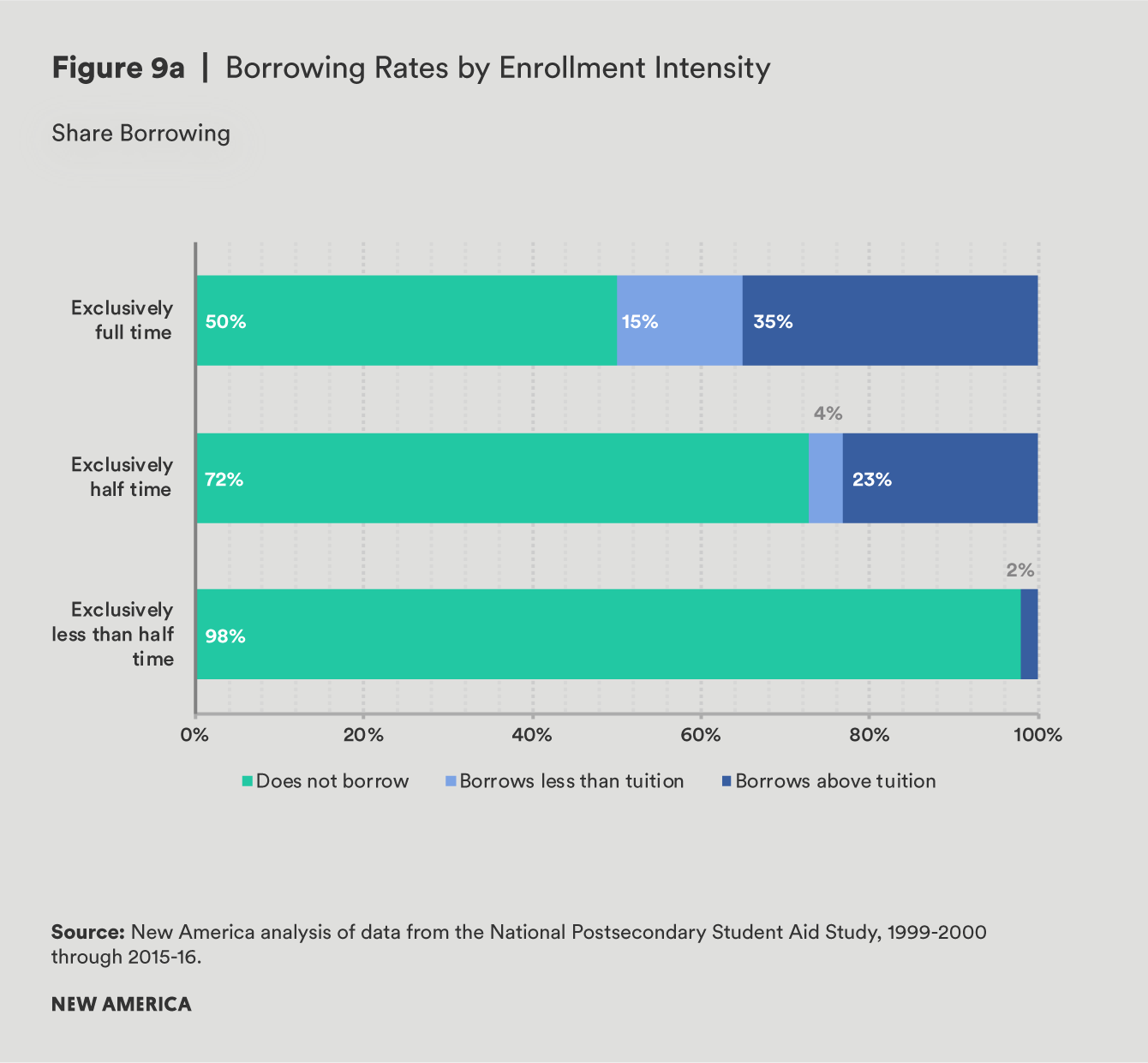

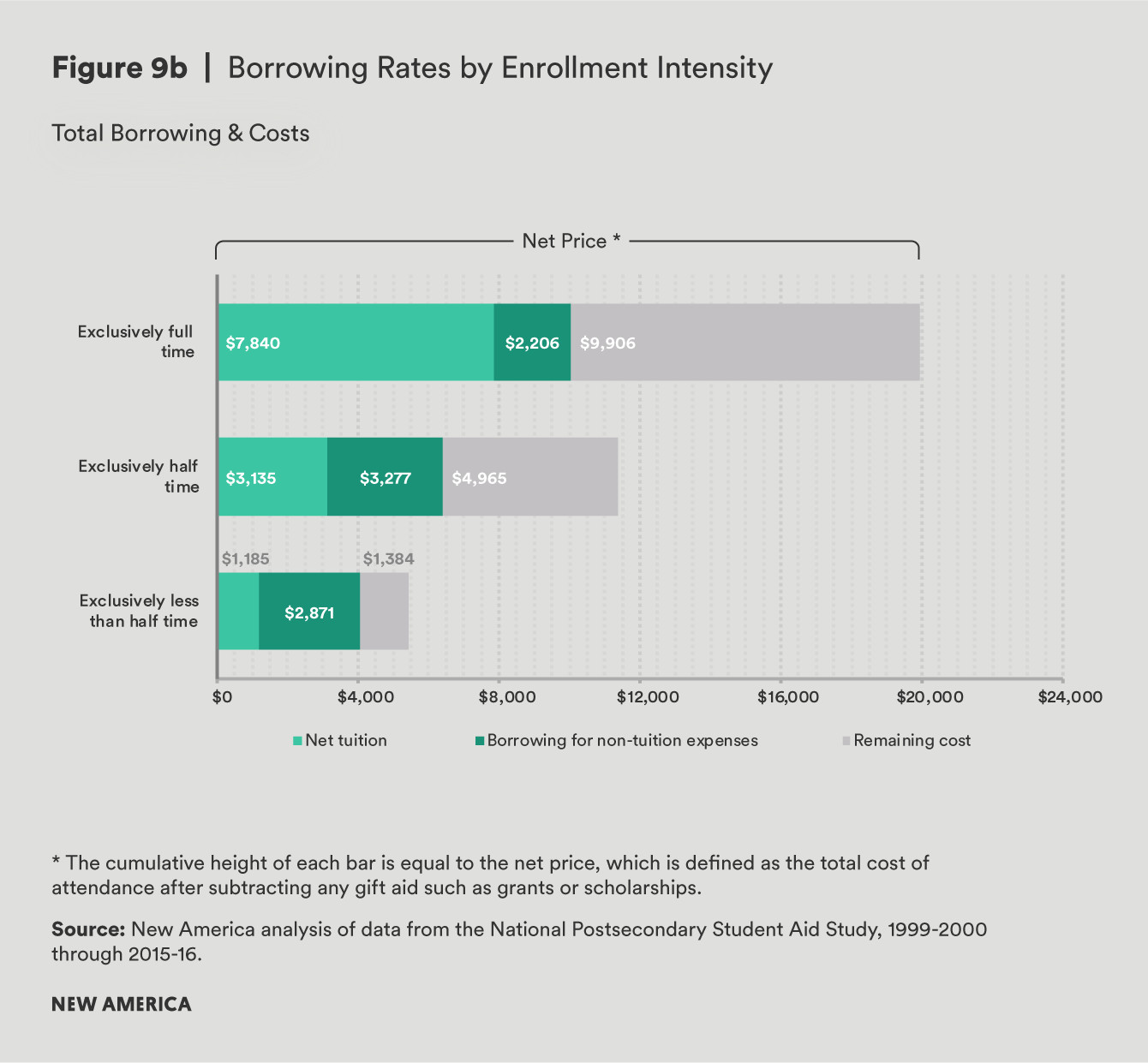

Enrollment Intensity

Student borrowers who enroll part time are much less likely to borrow than those who go to school full time. While 50 percent of full-time students borrow, only about 30 percent of those who enroll at least half time but less than full time take on debt. Among borrowers, those who enroll part time borrow nearly $4,000 less than those who enroll full time, but surprisingly, this does not necessarily mean part-time students borrow less for their non-tuition expenses. Gaps in total borrowing by enrollment intensity are more than offset by differences in the net tuition paid. In other words, the average part-time borrower faced a net tuition of just $3,061, nearly $5,000 less than that paid by the average full-time student. And as a result, part-time students applied more of their debt toward their non-tuition expenses.

One explanation for this counterintuitive finding is likely related to how loan limits are set. Unlike the federal Pell grant, loans are not prorated for part-time students. This means that students who enroll part time are still eligible to borrow the same amount for their non-tuition costs as their full-time peers. In some cases, there may be valid reasons for part-time students to borrow for their non-tuition costs, such as needing to borrow to reduce work hours while enrolled. Nonetheless, there could be valid concerns that these students are borrowing more than is absolutely necessary.

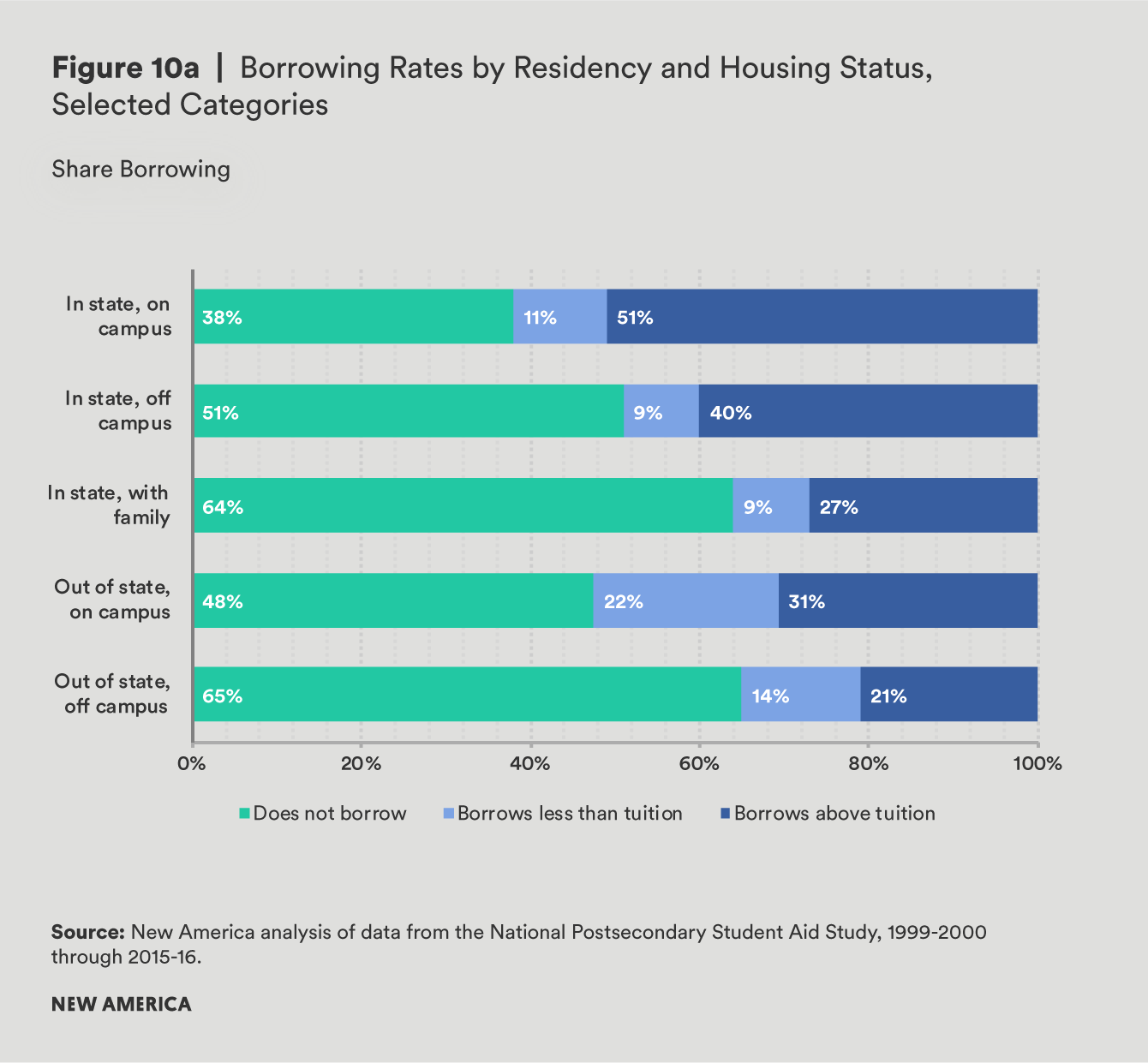

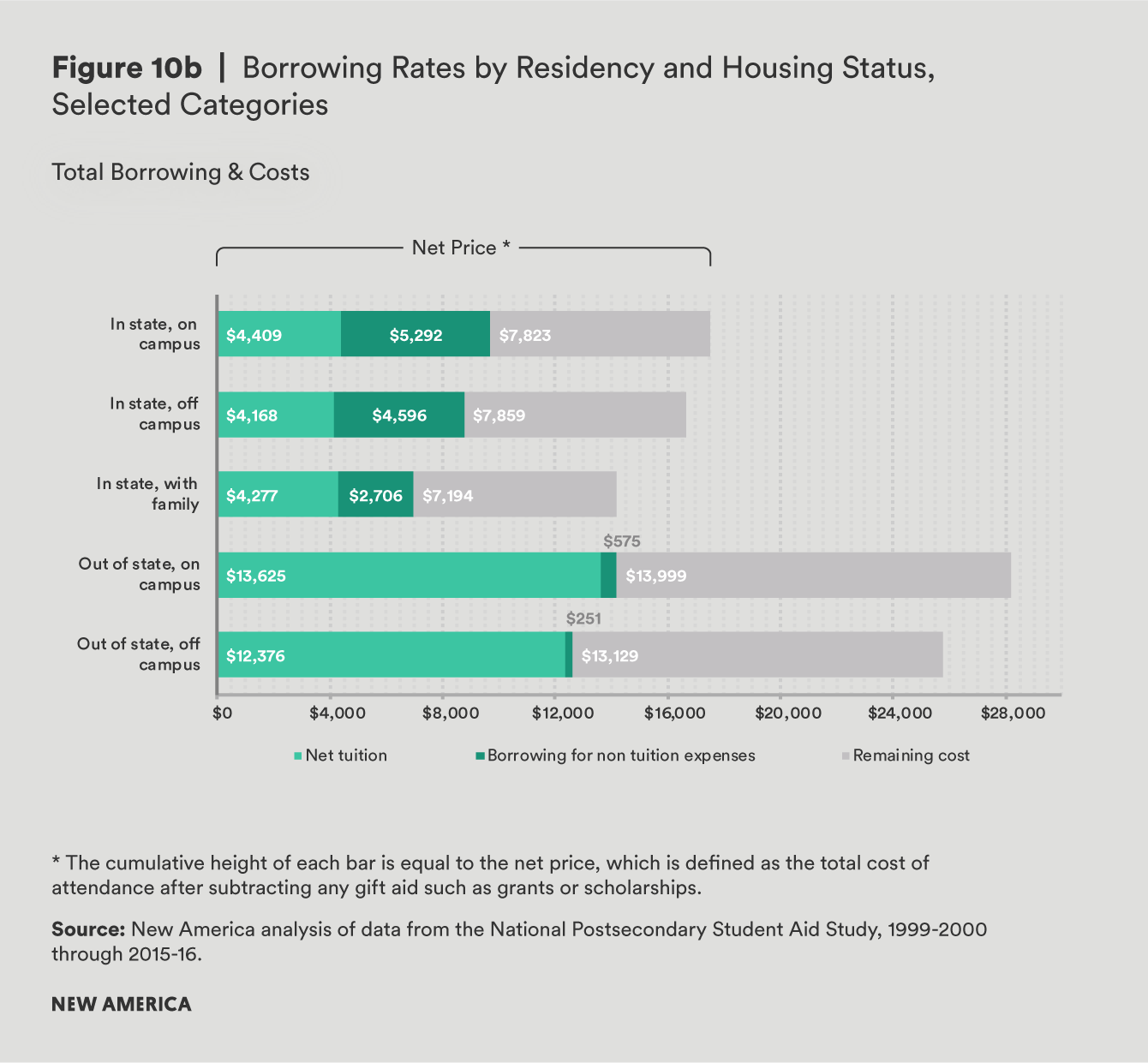

Residency Status and Housing

Where a student lives may also impact his borrowing decisions. At public four-year institutions especially, where students must choose whether to either attend college within or outside their home state and to live on or off campus, the likelihood that a student borrows, and the average amount of debt taken on, can differ dramatically.

While a larger share of those attending public four-year institutions in-state take out student loans relative to their out-of-state peers, the debt loads that out-of-state students assume are far greater than for those attending in-state. Students attending college out of state who live on campus borrow an average of $14,200, which is more than all other groups, and over twice the amount that students borrow if they are living in-state with their families. Regardless of whether they live on or off campus, students attending a public university in-state take on slightly more debt to cover their non-tuition costs than they did to pay for tuition. On the contrary, students attending college out of state borrow very little above the cost of their tuition: nearly all of the amount that out-of-state students borrow covers tuition.