The 2019 Leaders List: The 25 Most Responsible Asset Allocators

Abstract

The Responsible Asset Allocator Initiative (RAAI) at New America seeks to mobilize large pools of capital toward responsible investing, and supports the United Nations Sustainable Development Goals (SDG). The RAAI focuses on Sovereign Wealth Funds (SWF) and Government Pension Funds (GPF)—a group of institutional investors that have the scale, scope, and inclination to make a positive impact in this space.

As part of the RAAI, New America partnered with the Fletcher School at Tufts University to analyze and rate almost 200 sovereign wealth funds and Government pension funds against principles and criteria for responsible and sustainable investing. RAAI constantly seeks to refine its processes and outputs. As a result, researchers increased the number of criteria for evaluation from 12 in 2017 to 20 in 2019 with two criteria per each of the 10 principles: Disclosure, Intention, Clarity, Integration, Implementation, Commitment, Accountability Partnership, Standards, and Development.

By assessing and scoring the performance of asset allocators against these principles, and highlighting the performance of the Leaders (the 25 highest scoring sovereign wealth funds and government pension funds), RAAI provides a benchmark of peer excellence that serves as a catalyst for responsible investing among the broader community.

Acknowledgments

Partners

The Fletcher School at Tufts University

Team

Tomicah Tillemann, Chairman, Responsible Asset Allocator Initiative at New America

Scott Kalb, Director, Responsible Asset Allocator initiative at New America

Research/Fund Reviewer

Patrick Schena, Adjunct Professor, Co-head SovereigNet, The Fletcher School at Tufts University

Dia Banerjee, Master of Law and Diplomacy, The Fletcher School at Tufts University

Katie Panella, Master of International Business, The Fletcher School at Tufts University

Shrinal Sheth, Master of International Business, The Fletcher School at Tufts University

Anuradha Gurung, Senior Consultant, KLTI Advisors

Julia Rhodes, Program Assistant, Blockchain Trust Accelerator

Qiuyun Shang, Fellow, Blockchain Trust Accelerator

Technical Support

Maria Elkin, Deputy Director of Communications, New America

Zachary Schwartz, data visualization

Introduction

Incorporating long-term environmental, social, and governance (ESG) related concerns into the investment decision-making process is an important way for institutions to optimize returns, reduce risks, and identify opportunities for future growth, all while aligning portfolios with broader goals of society.

Regretfully, many regulators, legal advisors, and consultants who work with large asset allocators like sovereign wealth funds (SWF) and government pension funds (GPF), continue to recommend a false choice: either optimizing returns or considering ESG issues. This remains the case despite academic study after study showing that companies with higher scores on material ESG metrics generate higher financial and economic returns over time. It also seems to disregard mounting pressure from stakeholders and beneficiaries who would like to see their savings invested in a way that reflects their ethical and moral preferences.

General practices are evolving and, increasingly, institutional investors are adding non-traditional environmental and social factors to their portfolios. In particular, leaders in the SWF and GPF communities are seeking to make an impact in fields related to the UN Sustainable Development Goals (SDG) such as climate change, gender diversity, sustainable infrastructure, and universal health care, while delivering financial returns for their constituents. Despite these efforts, however, the amount of capital that is deployed responsibly and sustainably remains far below its potential.

For stewards of long-term capital, like sovereign wealth and government pension funds, the question is not can they afford to invest responsibly but rather: Can they afford not to? The world is shifting toward more socially conscious and environmentally friendly investing practices. The Responsible Asset Allocator Initiative supports this trend, monitoring the progress of the world’s largest investors toward responsible investing and providing a benchmark for future growth.

Update at 4:15pm, April 22, 2019: This report has been changed to correct the name of one asset allocator from ”OPSEU Trust (OPTrust)” to “OPTrust.”

Asset Allocators, Principles and Criteria

The Responsible Asset Allocator Initiative at New America seeks to mobilize large pools of capital toward responsible investing, and supports the United Nations Sustainable Development Goals. The RAAI focuses on Sovereign Wealth Funds and Government Pension Funds—a group of institutional investors that have the scale, scope, and inclination to make a positive impact in this space.

Together, these asset allocators manage over $30 trillion of assets on behalf of savers in their respective nations, to help ensure their financial security and to pay for their retirement, healthcare, and long-term savings needs. Sovereign wealth funds and government pension funds are accountable to their contributors and beneficiaries, who in addition to wanting stable returns, are interested in issues related to the SDG: climate action, gender equality, innovative sustainable infrastructure, education, and healthcare.

SWF and GPF are particularly well-suited to be trailblazers in responsible investing and sustainable development, given their long-term investment horizons (that often span generations), scalable assets, large internal resources, and investment capabilities. Where sovereign wealth funds and government pension funds go, companies and capital markets often follow.

While there is general consensus among academics and practitioners on the importance of responsible investing to long-term value creation, some asset allocators still face challenges integrating ESG considerations into their investment portfolios. Although numerous ESG tools exist, they are often onerous and complicated to implement, and they are not customized for the needs of the asset allocator community.

This is where the Responsible Asset Allocator Initiative comes in. The RAAI provides a benchmark of asset allocator best practices, enables knowledge-sharing among peers, and helps set a policy agenda and advocacy program to mobilize more capital into responsible investments. Asset allocators already are shifting investment practices to achieve financial goals without extracting social and environmental value. The notion of investing people’s savings in companies that pollute the environment or that employ child labor, in order to make an extra ten cents of returns, is going away. While supporting this trend, the RAAI takes the next step: helping asset allocators to add social and environmental value in line with the preferences of savers, while generating the risk-adjusted returns they require.

Principles and Criteria

As part of the RAAI, New America partnered with the Fletcher School at Tufts University to analyze and rate almost 200 sovereign wealth funds and public pension funds against principles and criteria for responsible and sustainable investing. RAAI constantly seeks to refine its processes and outputs. As a result, researchers increased the number of criteria for evaluation from 12 in 2017 to 20 in 2019 with two criteria per each of the 10 principles: Disclosure, Intention, Clarity, Integration, Implementation, Commitment, Accountability Partnership, Standards, and Development.

By assessing and scoring the performance of asset allocators against these principles, and highlighting the performance of the Leaders (the 25 highest scoring sovereign wealth funds and government pension funds), RAAI provides a benchmark of peer excellence that serves as a catalyst for responsible investing among the broader community.

The 10 core principles and 20 associated criteria were selected based on discussions with asset allocators and from guidelines by multilateral institutions and agreements across the field of ESG and sustainability, including, but not limited to, the Principles for Responsible Investing (PRI), the United Nations Global Compact (UNGC), the OECD Principles of Corporate Governance, regional and global sustainable investment forums (Eurosif, RIAA, GSIA), the Investor Network on Climate Risk (INCR/CERES), the UN Sustainable Development Goals and the International Forum on Sovereign Wealth Funds (IFSWF).

The 10 principles and 20 criteria can be reviewed below.

Principle 1: Disclosure

| Criteria Number | Criteria | Description |

|---|---|---|

| 1A - Organization | The Fund should disclose information on its organization in a dedicated website or in an annual report. | Information on the organization should include mission, founding principles, formation, structure, constraints, and employee data. |

| 1B - Financials | The Fund should disclose information on its investments in a dedicated website or in an annual report | Information on investments should include investment policy, asset allocation, portfolio weightings, investment beliefs, details of investments, and performance metrics. |

Principle 2: Intention

| Criteria Number | Criteria | Description |

|---|---|---|

| 2A - Statement on RI | The Fund should make a statement of intent on responsible investing. | The statement should define what responsible investing means to the organization, why it should be included in the investment process and the Fund’s intent to do so. |

| 2B - Downloadable Report | The Fund should publish a stand-alone report on its responsible investing or ESG program. | The standalone report may include aspects of the Fund’s responsible investing program, such as principles, goals and objectives, strategies, resources and staff, examples of investments, and performance. |

Principle 3: Clarity

| Criteria Number | Criteria | Description |

|---|---|---|

| 3A - Objectives for RI | The Fund should define the organization’s objectives for responsible investing. | Objectives may include investment themes such as climate change, gender equality, and sustainable infrastructure; targets, such as certifying 80 percent of real estate holdings as GRESB “compliant” or allocations to specific strategies, for example, five percent for renewable energy. |

| 3B - Strategies for RI | The Fund should explain the strategies it employs or intends to employ to achieve its responsible investing objectives. | Strategies may include values-based approaches such as exclusions, normative-based screening, and impact investing, or value-based approaches such as best-in-class investing, thematic investing, ESG integration, and active ownership and engagement. |

Principle 4: Integration

| Criteria Number | Criteria | Description |

|---|---|---|

| 4A - Integrating ESG | The Fund should integrate ESG into the investment decision-making process across the portfolio. | This disclosure may include a description of the fund’s ESG integration program across the portfolio or a detailed look at the approach taken by the firm to integrate ESG into the investment decision-making process of specific asset classes. |

| 4B - Methodology | The Fund should provide information on how ESG is integrated across the portfolio. | Information may include ESG integration in different asset classes, for example public and private equity, real estate and infrastructure, or the inclusion of specific ESG criteria, like environmental issues, across all investments. |

Principle 5: Implementation

| Criteria Number | Criteria | Description |

|---|---|---|

| 5A - Examples of RI | The Fund should provide details on specific responsible investments, in line with its program. | Specific examples may include responsible investing-related funds, such as a clean tech fund or an education fund; or individual investments, such as a renewable energy project or an affordable housing project. |

| 5B - Measuring RI | The Fund should provide information on how it measures and monitors responsible investments in the portfolio. | Information may include benchmarks the Fund uses, e.g. a customized index for exclusions or best-in-class strategies; information on reporting results of proxy votes; or results of engagement with portfolio companies on ESG risks. |

Principle 6: Commitment

| Criteria Number | Criteria | Description |

|---|---|---|

| 6A - Staff, Resources | The Fund should disclose resources and staff dedicated to responsible investing. | Resources may include software and data packages, research tools, consulting services, and meetings or training courses. Staff may include the head of the responsible investing effort, a dedicated team, or a senior executive managing the responsible investing program. |

| 6B - Socializing RI | The Fund should socialize a culture of responsible investing throughout the organization. | Evidence of socialization may include discussion of investment teams adopting responsible investing practices, firmwide meetings, communications from the board and senior executives to stakeholders and to staff, and information on how responsible investing is included in the incentive structure. |

Principle 7: Accountability

| Criteria Number | Criteria | Description |

|---|---|---|

| 7A - Financial Returns | The Fund should provide information on financial returns of responsible investments. | Information may include financial returns of responsible investing-related funds, individual investments—like an alternative energy project—or sections of the portfolio integrating ESG criteria. Financial returns that measure alpha or risk-reduction of responsible investments are especially valuable. |

| 7B - ESG Returns | The Fund should report on progress toward achieving responsible investing goals in the portfolio. | Reporting may include progress toward objectives, such as lowering carbon footprint, creating jobs, producing clean water, fostering greater participation of women on boards, achieving higher graduation rates, building low income housing units, or meeting targets for deploying a percentage of AUM in RI. |

Principle 8: Partnership

| Criteria Number | Criteria | Description |

|---|---|---|

| 8A - RI Partners | The Fund should partner with recognized organizations on responsible investing. | Information should include membership or relationships with organizations that promote responsible investing, for example the PRI, CDP, UNEP, TCFD, and ICGN. |

| 8B - RI Leadership | The Fund should take a leadership role in partner organizations on responsible investing. | Leadership roles in partner organizations may include chairing a committee, sitting on a board, leading projects on ESG or SDG-related investing, or working with government agencies to advocate policy changes and reform. |

Principle 9: Standards

| Criteria Number | Criteria | Description |

|---|---|---|

| 9A - Uniform Standards | The Fund should adopt recognized standards for its responsible investment practices. | The Fund may develop proprietary metrics but it should also identify uniform and consistent standards to use for its responsible investing practices, such as those provided by the PRI, the GRI, SASB, and the GRESB. |

| 9B - External Managers | The Fund should provide information on how it works with external managers on responsible investing. | This may include templates and guidelines for external managers to guide their investing and reporting, such as the GRESB for real estate and infrastructure mandates. It may also include discussion of engagement with external managers to customize mandates in-line with the Fund's responsible investing practices. |

Principle 10: Development

| Criteria Number | Criteria | Description |

|---|---|---|

| 10A - Referencing SDGs | The Fund should reference the UN Sustainable Development Goals (SDGs). | This may include analysis of the SDGs related to the Fund’s investment goals, or information on investments that conform with and reference select SDG goals, such as investments in healthcare (SDG 3), education (SDG 4), sustainable infrastructure (SDG 9&11) and renewable energy (SDG 7&13). |

| 10B - Frontier Markets | The Fund should invest in smaller emerging markets, including foreign frontier markets, and apply responsible investing practices in those markets. | Smaller, non-BRICS EM include EM other than Brazil, Russia, India, China and South Africa. The Fund should invest in these markets not only through passive, market-cap weighted indexes but also in active or customized strategies that incorporate responsible investing practices. Funds not permitted to invest directly in these non-BRIC EM may invest instead in companies with substantial business in these markets. |

The RAAI Leaders List and Index

The 25 Most Responsible Asset Allocators

The 2019 RAAI Leaders List: The 25 Most Responsible Asset Allocators is comprised of the 25 top scoring funds in the RAAI Index as rated against 10 core principles and 20 criteria for responsible investing practices (see Principles and Criteria for more). The Leaders were selected from the 197 sovereign wealth funds and government pension funds that were rated and include six SWF, 18 GPF and one global fund (as a multilateral institution, the UNJSPF is classified as a global fund). The Leaders stand out for their commitment to responsible, long-term investing, integration of ESG risks into their portfolio decision-making process, and leadership in reflecting saver’s preferences on key issues such as climate change, gender equality, fair labor practices, sustainable infrastructure, education, and healthcare.

Together, this impressive group of Leaders on responsible investing have a combined AUM of $5.9 trillion, and individual funds ranging from a low of $26 billion to a high of nearly $1.5 trillion in assets.

To put this in context, the combined asset base of this group is larger than the GDP of every country but the United States and China. The Leaders List is diverse with asset allocators from four major geographic regions: the Americas (Latin and North America), Asia (Central Asia, East Asia and Australasia), EEMEA (Eastern Europe, Middle East and Africa) and Europe (Europe and Other), 13 countries and one global fund.1

Europe is the most well-represented continent, including 10 asset allocators that comprise over 40 percent of AUM in the Leaders List. European Leaders include three from France, two each from the Netherlands and the United Kingdom, and one each from Denmark, Norway, and Sweden. North America is second, with eight funds in the Leaders List (together comprising 26 percent of assets), including five from Canada—the country with the highest number of Leaders—and three from the United States. Asia has five asset allocators on the Leaders List, with two from Australia, and one each from Japan, Malaysia, and New Zealand. Asian funds represent only 20 percent of the Leaders but comprise almost 30 percent of total assets. Lastly, the EEMEA region had but one representative on the Leaders List—a South African government pension fund with $150 billion in assets.

The Leaders and Finalists Table

Error: Data visualization bundle URL missing.

Responsible Asset Allocator Map

Error: Data visualization bundle URL missing.

Regional Composition of Leaders

Error: Data visualization bundle URL missing.

Responsible Asset Allocator Index

Error: Data visualization bundle URL missing.

Update at 4:15pm, May 13, 2019. This report has been corrected to fix the ratings of Government Pension Fund – Global (Norway) and Government Pension Fund (Thailand), which were mistakenly swapped previously, on the Responsible Asset Allocator Index table.

Performance Analysis of the Leaders

The Leaders List funds scored significantly higher than other rated funds on the index, providing a benchmark of excellence for the broader asset allocator community. Note that the Finalists—the funds that ranked 26-50 on the index—were not far behind in terms of scoring performance. Of the 197 rated funds, the Leaders scored an average of 96 points (out of 100), while the Finalists scored an average of 89 points. The rest of the 147 rated funds only scored an average of 33 points.

Performance on key criteria shows a stark difference between the responsible investing practices of the Leaders and Finalists and the rest of rated funds, indicating that much work remains to be done. For example, every Leader and Finalist has:

- issued a statement on their responsible investing policies in their annual reports or websites, compared with only 42 percent for the rest of funds.

- joined partner organizations to learn about best practices and share knowledge on responsible investing, compared with 43 percent for the rest of funds.

- integrated environmental social and governance risks into their investment decision-making process, while only 24 percent of the rest of funds do so.

These are relatively straightforward criteria, and it is surprising that so many funds rate poorly on them, in the opinion of the reviewers.

Note, Leaders and Finalists also have room for improvement. For example:

- On the Principle of Development, Criteria 10B—Investing in frontier markets and following responsible investing practices while doing so—the rest of funds scored an average of 24 percent. However, the Leaders and Finalists, with average scores of 60 percent and 48 percent respectively, could do much better.

- On criteria 10A—Referencing the SDGs in the annual report or website—the rest of funds scored a shockingly low 4 percent average, while the Leaders and Finalists scored an average of 76 percent and 36 percent respectively.

- Only 88 percent of Leaders and 56 percent of Finalists have a downloadable report with details on their responsible investing practices. While relatively good scores, we expect nothing less than 100 percent on this criteria going forward.

How the Leaders Stack Up Against the Rest: Identifying Coverage Gaps

Error: Data visualization bundle URL missing.

Citations

- The United Nations Joint Staff Pension Fund, a global public pension fund, is on the Leader’s list and is included in the ‘Europe and other’ regional category.

Why the Leaders Matter

The total assets controlled by the top 25 funds on the Leaders List—$5.9 trillion—is…

- Larger than the GDP of every country in the world except the United States and China

- Larger than the combined GDP of 145 countries

- 37 times bigger than all official development assistance (ODA) extended in 2017

- 28 times bigger than total loans and disbursements of the ten key multilateral development banks (MDB) in 20171

Channeling just 1 percent of the total capital of the Leaders toward responsible investing and related sustainable development goals would create a pool of resources…

- Larger than the GDP of 107 countries

- Equivalent to 130 percent of total loans, grants, investments, and guarantees provided to developing countries by the World Bank in FY 2018

- Almost three and a half times all financial services extended to developing countries by the International Bank for Reconstruction and Development (IBRD) in 2018

- More than four times the amount of interest free loans and grants to the world’s poorest countries extended through the International Development Association (IDA) in 2018

The 25 asset allocators on the Leaders List…

- Received an average total score of 96 (out of 100) on the Responsible Asset Allocator rating system

- Represent funds from Africa, Asia, Australasia, Europe, and North America

- Punch above their weight, comprising 12.5 percent of total funds but 30 percent of total assets of the 197 asset allocators that were rated

Citations

- Data sourced from annual reports of the World Bank Group and other MDB.

Lessons from the Leaders

The lessons from the Leaders that the Responsible Asset Allocator Initiative shared in 2017 still hold true in 2019.

Ten Recommendations for Success

- Know Yourself. Identify your principles and investment beliefs, then build your investments around that framework. Work to understand the non-traditional financial risks that could impact long-term value creation in your portfolio and make sure those risks are properly priced and addressed. You can only engage effectively with portfolio companies and stakeholders if you truly understand and believe in your approach.

- Normalize the conversation with the board. Make sure the board, senior management, and the organization are on the same page when it comes to ESG. Agree on standards that make sense to your stakeholders. The board should approve your responsible investing statement as a core component of the fund’s investment philosophy.

- Work hard on communicating. Develop a culture of transparency. Being open about responsible investment practices promotes trust and confidence among stakeholders, the public and the investment community, all key to success. Continually refine your communication protocols. If you don’t communicate your responsible investing principles and investment framework effectively, it will limit your chances for success.

- Be a Leader, not a follower. The trend toward sustainable and responsible investing is gaining momentum, supported by academic evidence, government policies, stakeholder interest, and public preferences. Funds on the Leaders List are early adopters, and they have recognized that it is better to get ahead of the curve on responsible investing than to wait and have the issue forced upon them.

- Start with the low-hanging fruit. When it comes to implementation, begin with the tasks that are easiest for your organization. For example, introducing ESG into the due diligence process for private equity may provide a quick win. The process already exists, you simply need to define additional criteria and standards.

- Build internal champions. For many funds on the Leaders List, sustainable investing has become part of the DNA that permeates the organization. Early on, however, the leaders noted how important it was to develop internal champions who could help in setting goals, working with staff, and moving the agenda forward.

- Join a responsible investing association. Use your peers as a sounding board. Exchange ideas with the community. Get a roadmap. See how you compare with like-minded institutions. Benchmark yourself and show the results to the Board and to stakeholders. Understand that this is a “live” process. Work on building up your expertise and assimilating best practices from peers with shared values.

- Don’t try to save the planet; stick with stewardship. Your work should always be aligned with the financial objectives and goals of the fund. A robust responsible investing program really means making sure that the companies you invest in know what they are doing, operate with a long-term perspective, understand both traditional and non-traditional risks, and price and address those risks properly and consistently.

- Socialize your responsible investment beliefs throughout the organization. Fund leadership must carry the torch, set goals, and challenge the organization to deliver, but if you really want to build a successful, sustainable investment process, everyone needs to buy in, from top to bottom. Create an environment where investment professionals at the fund understand and internalize non-traditional ESG risks. Make ESG considerations part of everyone’s evaluation process.

- Set up a reporting framework to monitor your progress. Establish goals and metrics to help gauge your organization’s success over time. Has the carbon footprint of the portfolio been reduced? Have portfolio company governance practices improved as the result of engagement? How often did you vote against managements and on what issues? Report publicly and transparently on the outcomes of your efforts.

Alternative Choices

- Emphasize the long-term. Asset allocators must constantly iterate long-term goals and objectives for their funds. An important part of this message is to articulate that the inclusion of ESG factors in the investment process is vital to long-term risk mitigation, growth and value creation.

- Engage and cooperate. The Leaders will divest holdings in companies as a last resort, for example if they violate the Fund’s investment beliefs or normative based principles, but it is not their preferred strategy. They would much rather engage with managements and work together to achieve positive externalities. They also believe in cooperating with like-minded institutions to build capacity and promote systemic change.

- Turn consultants and external managers into allies on responsible investing. Ask about standards they use and risks they feel deserve the most attention. Learn from their experience, take advantage of their data sets, see what tools they can offer. Put your external managers on the front lines in working with portfolio companies. Give them uniform standards and ask them to report back on sustainability metrics for the companies they own on your behalf.

What’s New? Comparing the 2019 and 2017 RAAI Leaders List

When comparing the 2019 and 2017 Leaders Lists, three major differences stand out.

It was harder to make the Leaders List in 2019 than it was in 2017, because of increased competition and a higher bar for inclusion. In 2019, 197 asset allocators were rated compared to 121 in 2017. Additionally, in 2019, asset allocators were rated on 20 criteria, eight more than in 2017, and a higher score was needed to qualify. Leaders in 2019 needed to score at least 94 to make the cut, versus a minimum score of 90 in 2017.

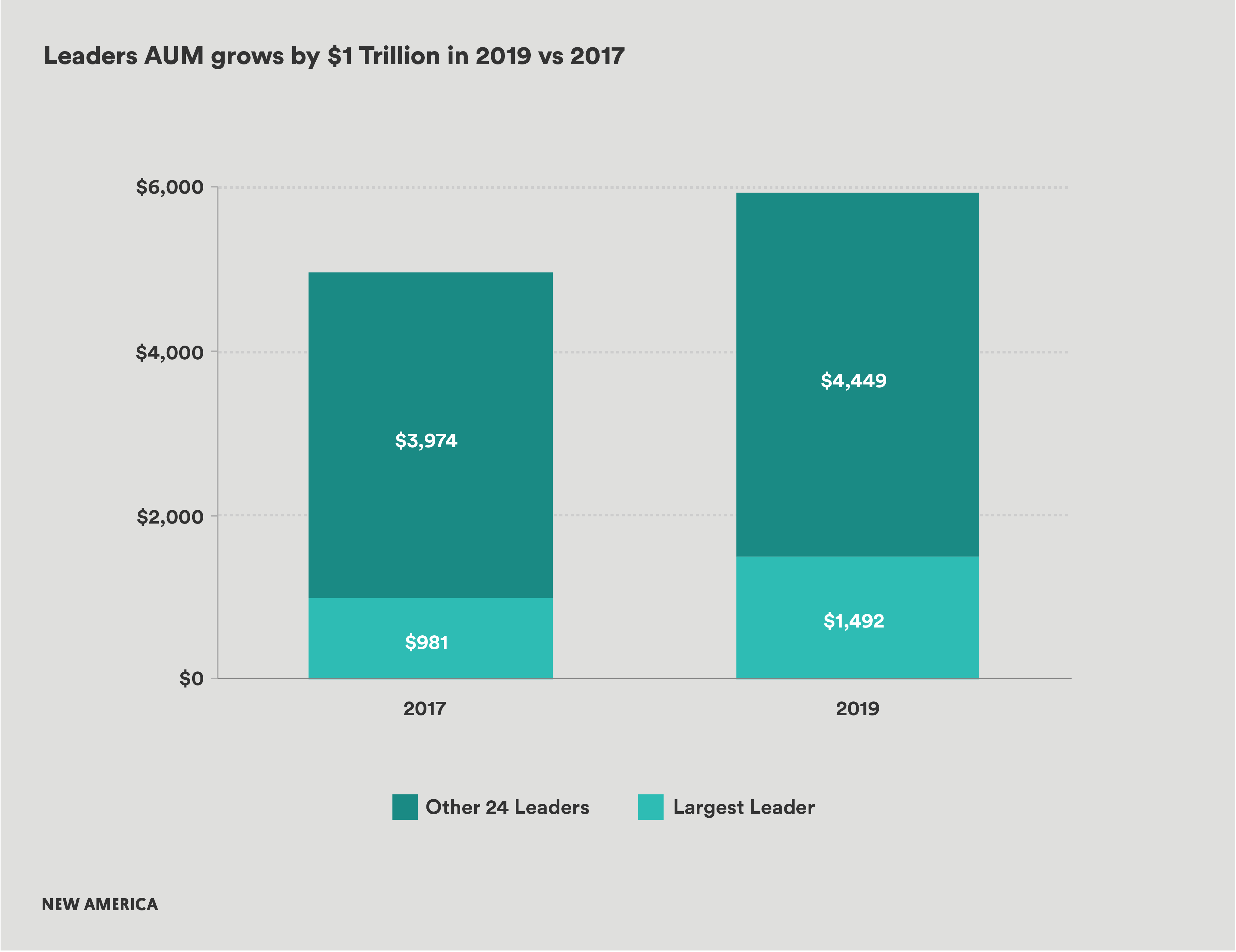

The total AUM of Leaders in 2019 is $1 trillion higher at ($5.94 trillion) than it was in 2017. This indicates that larger, more mature asset allocators are increasingly focused on responsible investing and hence more assets are being deployed toward social and environmental goals alongside financial returns. Part of the jump in assets was due to the inclusion of the Government Pension Investment Fund (GPIF) of Japan, the world’s largest government pension fund with assets of $1.5 trillion. However, even excluding the AUM of the GPIF, the next 24 Leaders together accounted for $4.45 trillion of AUM, versus $3.97 trillion for the equivalent group of Leaders in 2017.

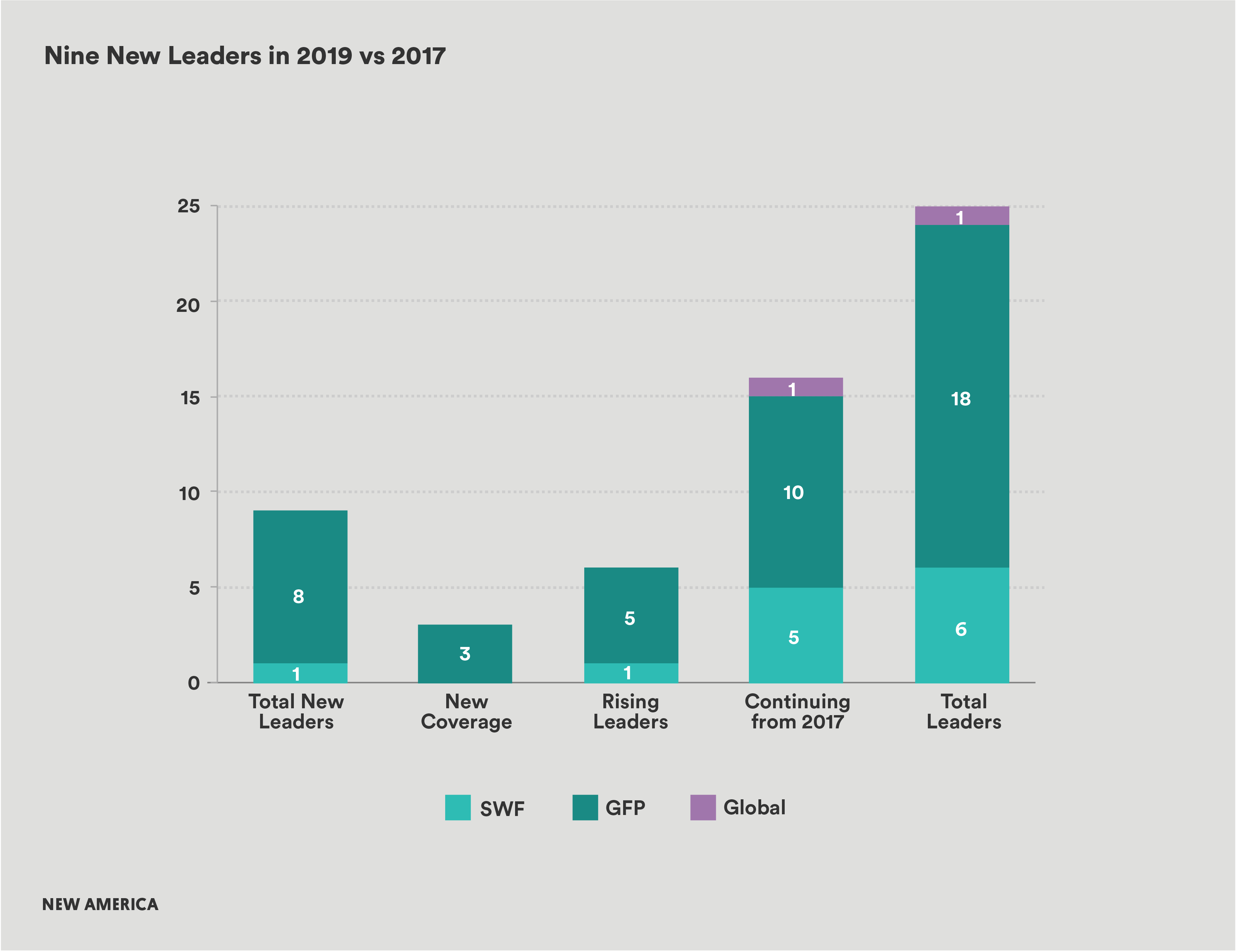

The Leaders List is dynamic, with room for improvement from previously rated funds and the opportunity for newly rated funds to be recognized for their leadership on responsible investing. Nine new asset allocators were selected for the Leaders List in 2019 – three were new to the RAAI and not covered in 2017: PensionDanmark of Denmark, Strathclyde Pension Fund of the UK and RPMI Railpen, also from the UK . Of the remaining six new Leaders, all were ranked in the second quintile in 2017 (that is, those funds that ranked 26-50), and were able to raise their scores in 2019, including: Australian Super and Victoria Funds Management Corp of Australia, Fonds de Reserve pour les Retraites (FRR) in France, the Government Pension Investment Fund (GPIF) in Japan, the UC Regents Investment Funds in the US and the California State Teachers' Retirement System (CalSTERS), also of the US.

Methodology

Constructing and Refining the Universe of Funds

To construct the universe of funds for the 2019 study, researchers utilized updated lists of sovereign wealth funds and government pension funds from the 2017 study, as compiled by the International Forum of Sovereign Wealth Funds, the Organization for Economic Co-operation and Development (OECD), the Pacific Pension & Investment Institute (PPI), Professor Paul Rose at the Ohio State University Moritz College of Law, and the Sovereign Investor Institute’s Sovereign Wealth Center. In addition, two more lists were added for the 2019 study, compiled by Northern Trust, and Willis Tower Watson.1

This resulted in a comprehensive list of 624 asset allocators (compared to 298 in 2017). The comprehensive list was then cleaned of all duplicates and sub-managed accounts, eliminating 153 funds and resulting in a universe of 471 asset allocators to be analyzed, with total assets under management (AUM) of $30 trillion.

Researchers then went through a series of steps to arrive at the final list of funds to be rated. First, all asset allocators other than SWF and GPF, the focus of the RAAI, were eliminated from the universe (including private and corporate pension funds, endowments, foundations, philanthropic organizations, family offices, insurance firms and asset managers).

Second, to ensure the SWF and GPF were sufficiently large and had adequate data for ratings consideration, researchers eliminated funds with less than $2 billion of AUM, and that could not be evaluated on responsible investing practices because they:

- had highly constrained portfolios (for example, investing only in treasuries);

- were newly established with insufficient data;

- were not yet funded or

- did not have information available in English.

This eliminated 263 funds with AUM of $10 trillion.

Finally, funds were eliminated from ratings coverage if

- AUM had been substantially depleted or removed by stakeholders,

- the fund had been dissolved,

- the fund was embroiled in legal action due to fraud or scandal,

- AUM had been frozen or

- the fund’s mission and/or remit had been substantially changed, leading to reassessment of investing goals and processes.

This last step eliminated 11 funds, leading to the final list of 197 asset allocators that were rated, comprising AUM of $21 trillion. The top 25 scoring asset allocators, with AUM of $5.9 trillion, were selected for “The RAAI Leaders List: The 25 Most Responsible Asset Allocators” in the world.

| Number of Funds | Process | AUM $bn |

|---|---|---|

| 624 | Comprehensive List of Funds Screened | N/A |

| 153 | Duplicates | N/A |

| 471 | Universe - Asset Allocators Analyzed | $30,429 |

| 263 | Excluded* | $9,522 |

| 11 | Suspended* | $331 |

| 197 | Rated Asset Allocators | $20,566 |

| 25 | Leaders | $5,943 |

Rating Framework

Each of the 197 asset allocators in the final list were rated across 20 criteria, two for each of the 10 core principles, up from 12 criteria in 2017 (see Principles and Criteria section for more). Reviewers analyzed information from the public domain to rate each fund, including annual reports, company websites, reports, articles, and other publicly available information. Rated funds received either full or zero points for each criteria; no partial points were assigned. Each fund was analyzed by an independent reviewer and then ratings were double-checked by an expert.

Once scores were aggregated, asset allocators were rank ordered and divided into quintiles such that quintile cut-off scores ensured a similar number of asset allocators in each quintile (about 40 asset allocators per quintile in 2019 compared to 25 per quintile in 2017). Quintile 1 comprises the highest-rated asset allocators, while quintile 5 comprises asset allocators that received the lowest ratings.

Only some of the asset allocators in quintile 1 made the Leaders List in 2019 (in 2017, when there were a total of 121 rated asset allocators, all the asset allocators in quintile 1 qualified as Leaders). In 2019, a new Finalists category was created to recognize the next 25 highest ranked funds (i.e. those ranked 26-50).

The RAAI index provides the first comprehensive analysis of the responsible investment practices of the world’s largest SWF and GPF, but there are limitations to this study. The criteria, while expanded and customized for asset allocators, are by no means an exhaustive list of responsible investing characteristics. Some important metrics may be overlooked. Second, only SWF and GPF that disclose information in English are rated. Thus, it is possible that a SWF and GPF with good responsible investing practices but limited English disclosures could be overlooked by this study. In addition, awarding full or zero points for each criteria leaves little scope for nuanced analysis and ratings. Finally, since the index only covers SWF and GPF, there are many worthy asset allocators that are not included in the study.

Citations

- International Forum of Sovereign Wealth Funds, “Our Members,” as of June 2018; Northern Trust, The Local Government Pension Scheme: Beyond Asset Pooling, May 2018; Organization for Economic Cooperation and Development, Pacific Pension Institute, Annual Survey of Large Pension Funds and Public Pension Reserve Funds: Report on Pension Funds’ Long-term Investments, 2016; Pacific Pension Institute, “Members: Asset Owners and Allocators” as of June 2018; Rose, Paul, “North American Dream: The Rise of U.S. and Canadian Sovereign Wealth” (April 9, 2014). ESADEgeo 2014 Sovereign Wealth Fund Report; Sovereign Investor Institute’s Sovereign Wealth Center, “Fund Profiles,” 2018; Willis Towers Watson, “The World’s 300 Largest Pension Funds – Year Ended 2016,” September 2017.

Glossary of Terms

- AUM – Assets under management

- ESG – Environmental, social, and governance

- EuroSif – European Sustainable Investment Forum

- GPF – Government pension funds

- GSIA – Global Sustainable Investment Alliance

- IBRD – International Bank for Reconstruction and Development

- IDA – International Development Association

- IFSWF – International Forum of Sovereign Wealth Funds

- INCR/CERES – Investor Network on Climate Risk

- MDB – Multilateral development banks

- ODA – Official development assistance

- OECD – Organization for Economic Co-operation and Development

- PRI – Principles for Responsible Investing

- RAAI – Responsible Asset Allocator Initiative

- RIAA – Responsible Investment Association of Australasia

- SDG – Sustainable Development Goals of the United Nations

- SWF – Sovereign wealth funds

- UNGC – United Nations Global Compact

More About the Authors

Scott Kalb

Director, Responsible Asset Allocator Initiative