Table of Contents

- The Emerging Millennial Wealth Gap: Opening Note

- Building Ladders of Success for the Rising Millennial Generation: An Initiative Funded by the Citi Foundation

- Part 1: Generational Wealth and Financial Health

- Framing the Millennial Wealth Gap: Demographic Realities and Divergent Trajectories

- Trends, Origins, and Implications of the Millennial Wealth Gap

- The Millennial Racial Wealth Gap

- The Young and (Economically) Restless: The Nature of Work for American Millennials

- The Financial Lives of Millennials: Evidence from the U.S. Financial Health Pulse

- Part 2: Components of the Millennial Balance Sheet: Assets and Liabilities

- Wealth and the Credit Health of Young Millennials

- Millennials and Student Loans: Rising Debts and Disparities

- Young Adults and Consumer Debt: The Quiet Crisis Next Time

- Homeownership and Living Arrangements among Millennials: New Sources of Wealth Inequality and What to Do about It

- Part 3: Implications for Social Policy

- Public Policy Implications of the Millennial Wealth Gap

- Addressing the $1.5 Trillion in Federal Student Loan Debt

- Policy Responses to the Millennial Wealth Gap: Repairing the Balance Sheet and Creating New Pathways to Progress

Homeownership and Living Arrangements among Millennials: New Sources of Wealth Inequality and What to Do about It

Jung Choi

Homeownership in America has historically been both a reflection of current wealth and a predictor of future wealth. Becoming a homeowner as a young adult is often a foundational step in the process of future wealth accumulation (Goodman and Mayers 2018). Yet, compared to the prior generations, fewer Millennials are buying a place of their own.

Two significant shifts in housing arrangements have become apparent for Millennials who came of age after the Great Recession: a decline in the rate of homeownership and a rise in the share of those who stay with their parents. Relatedly, household formation, marriage, and child-rearing are down. The impacts of these trends on future wealth could be long-lasting, as many younger adults will have less time to build housing wealth before they reach their retirement age.

Not only are there intergenerational gaps, but there are substantial disparities in homeownership and living arrangement across race, ethnicity, and education among younger adults. In fact, these gaps of housing equity have become exacerbated since the Great Recession, as people of color (especially Black young adults) and the less educated were hit hardest and have experienced a slower recovery. This means that changes in homeownership and living arrangements among Millennials have become new sources of wealth inequality.

Multiple factors contribute to the low Millennial homeownership rate and their delay in forming independent households. These include demographic shifts and changes in socioeconomic characteristics of the generation of young adults. However, there has also been a rise in external barriers that have made accessing homeownership more difficult. Understanding these barriers can help inform the development of effective policy interventions. This chapter presents the data trends on homeownership and living arrangement among Millennials, explores what is driving these trends, and discusses potential long-term consequences. The chapter concludes with a range of policy options that could enhance the future well-being of Millennials and upcoming generations and promote greater equity in American society.

Young Adults’ Homeownership and Living Arrangement Trends

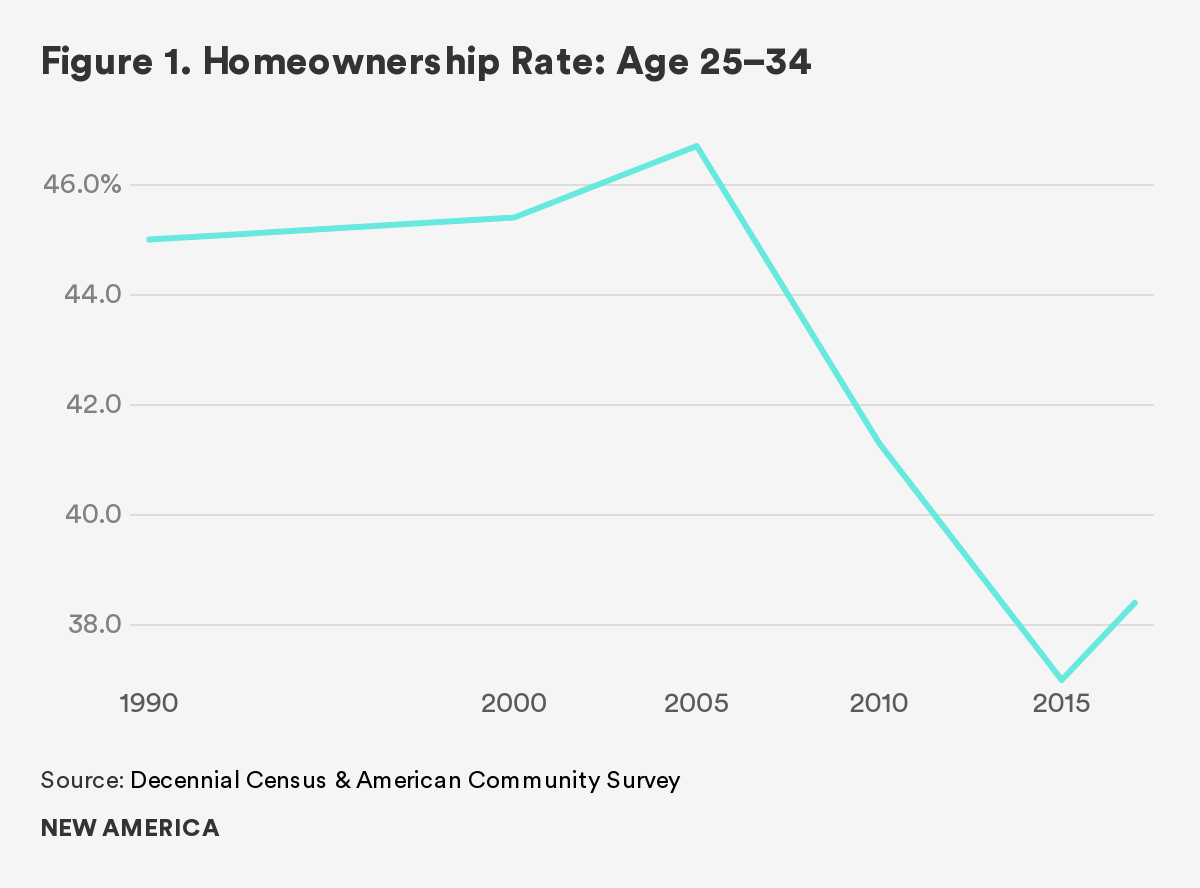

In order to understand the changing relationship of Millennials to homeownership and living arrangements, let’s take a closer look at the data.1 Figure 1 shows the homeownership rate of young adults between ages 25 and 34. The young adults’ homeownership rate peaked at 47 percent in 2005, but following the 2007 housing market crisis, the number dropped 10 percent to 37 percent by 2015. The homeownership rate of this group stood at 38 percent in 2017, ticking up slightly with the improvement in the macroeconomy. The net effect of this lower rate of Millennial homeownership is sizeable. If Millennials ages 25 to 34 had the same homeownership rate as their age cohort in 2000, there would be 1.3 million more young homeowner households than the country has today.2

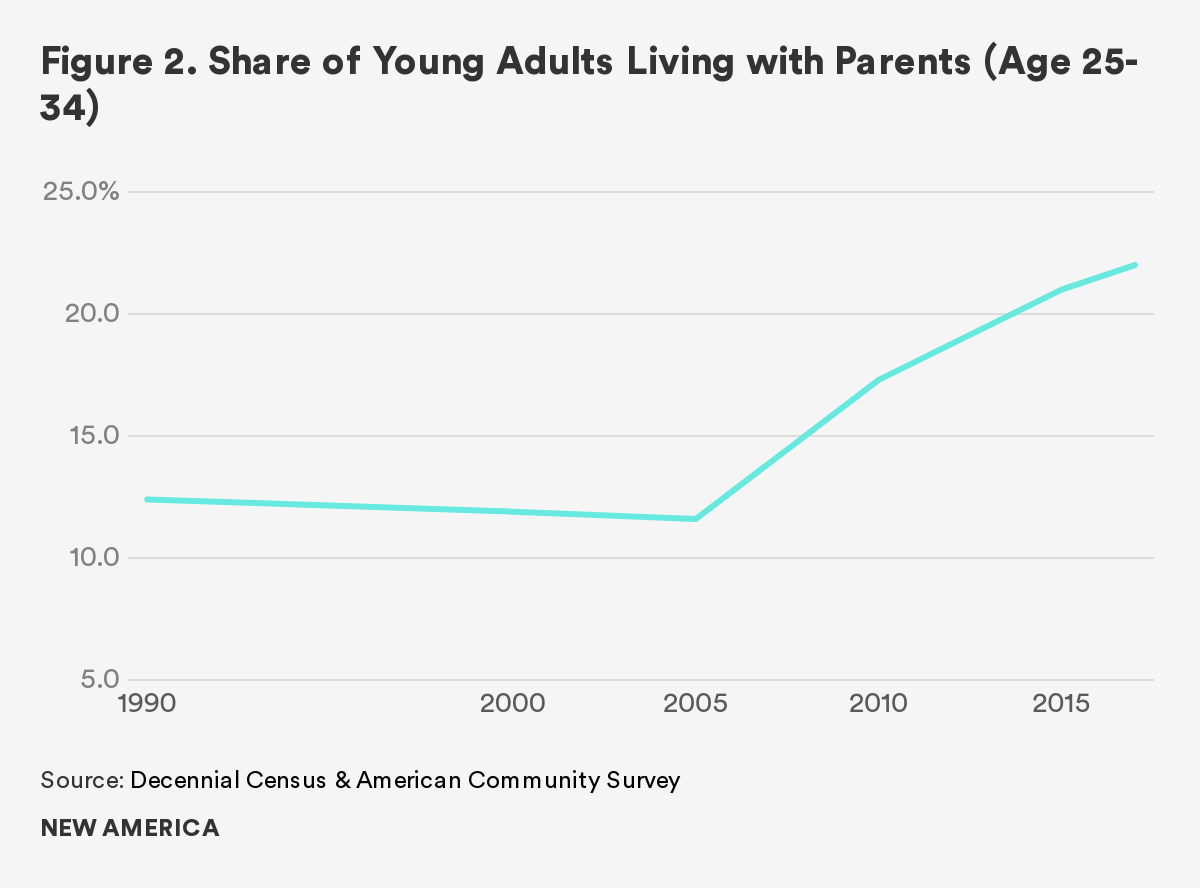

The homeownership rate captures only those who have already formed their independent households. Thus, the delay in household formation is not reflected in the homeownership rate, but it is actually an even larger factor in the generational housing disparities. Figure 1 shows that not only are Millennials delaying owning a home, but they also stay in their parents’ homes for a longer period. The share of young adults (ages 25–34) living with their parents has increased from 12 percent to 22 percent between 2000 and 2017, adding about 5.1 million more young adults living under their parents’ roofs. Unlike the homeownership rate, which has stabilized in the past few years, the share of 25- to 34-year-olds living with parents continued to go up. In general, this trend reflects a reality that Millennials are less likely to form independent households than the prior generation. If both homeownership and the rate of household formation (headship rate) in 2017 remained the same as in 2000, today there would be 2.4 million more Millennial individual homeowners ages 25 to 34.

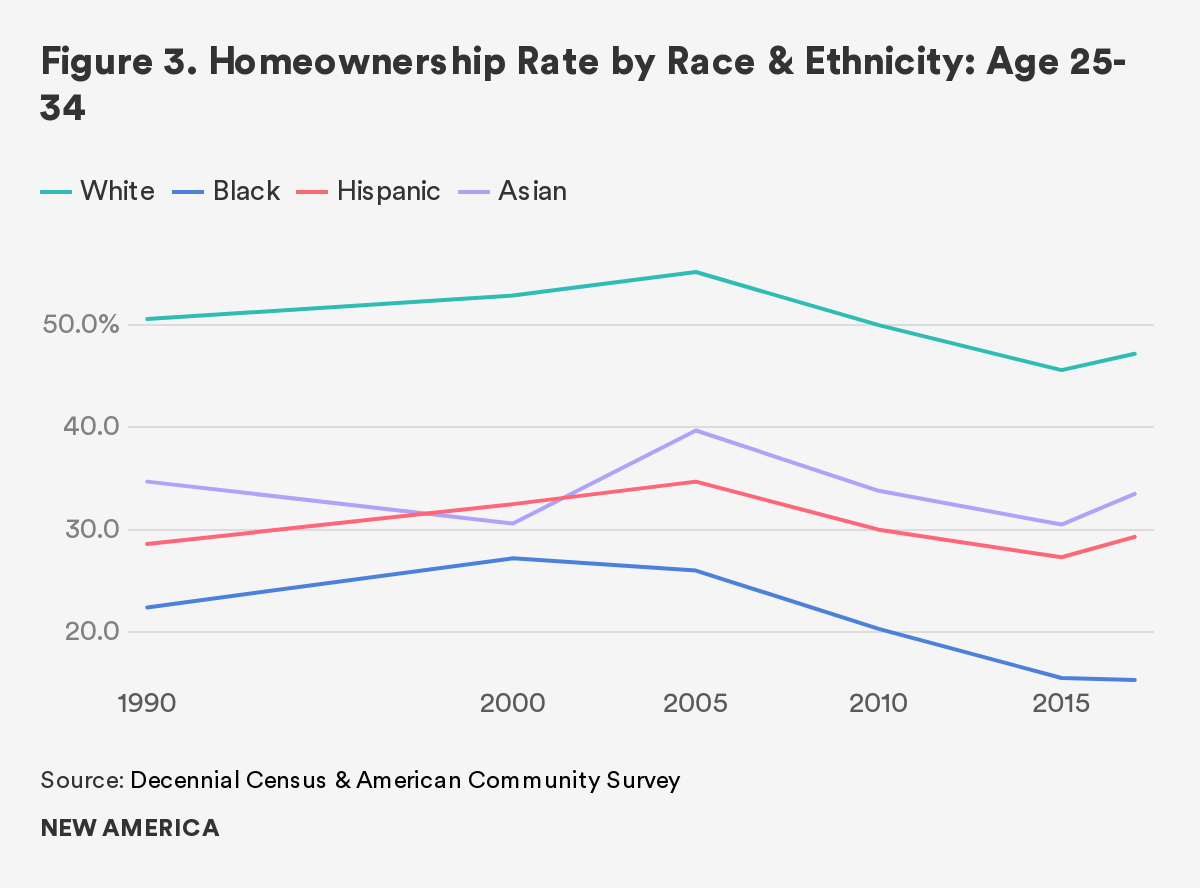

Another current housing trend of young adults is the persistent disparities in the homeownership gap by race and ethnicity and also by education. Figure 3 shows that the homeownership rate of young White households has always been higher than for people of color. While the homeownership rate has dropped for all racial and ethnic groups since 2005, from 2015 on, the rate has started to recover slightly for Whites, Asians, and Hispanics. However, the homeownership rate of young Black households continued to drop, further widening the racial homeownership gap. The Black–White homeownership gap in 2017 was 32 percent, about 6 percentage points higher than the gap in 2000. Furthermore, young Black households were the only group that did not experience an increase in homeownership during the housing boom between 2000 and 2005.

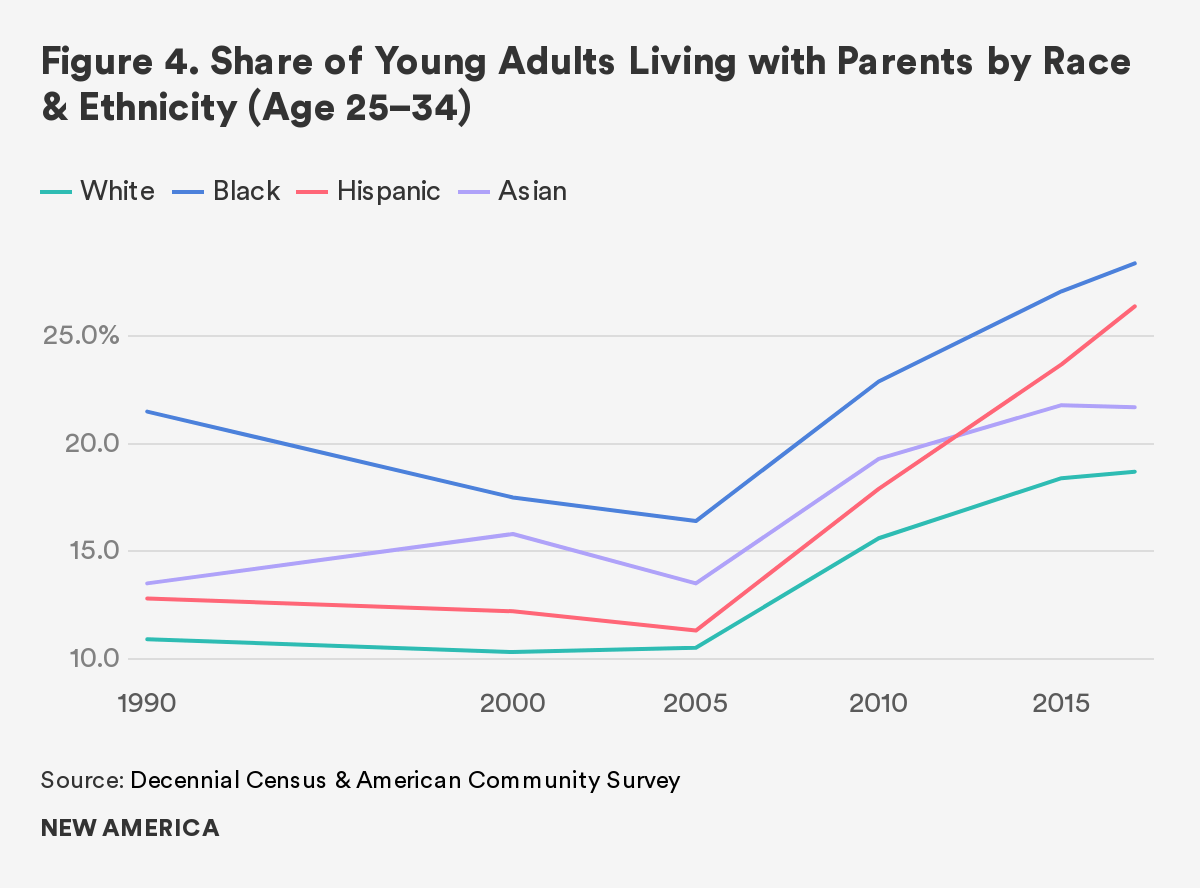

Black young adults are also most likely to live with their parents. Close to 29 percent of Black young adults ages 25–34 were living with their parents in 2017, almost 10 percentage points higher than the share of Whites who did so. Following the crisis, the share of young adults living with their parents increased for all race and ethnic groups, but the share increased most rapidly for Blacks and Hispanics.

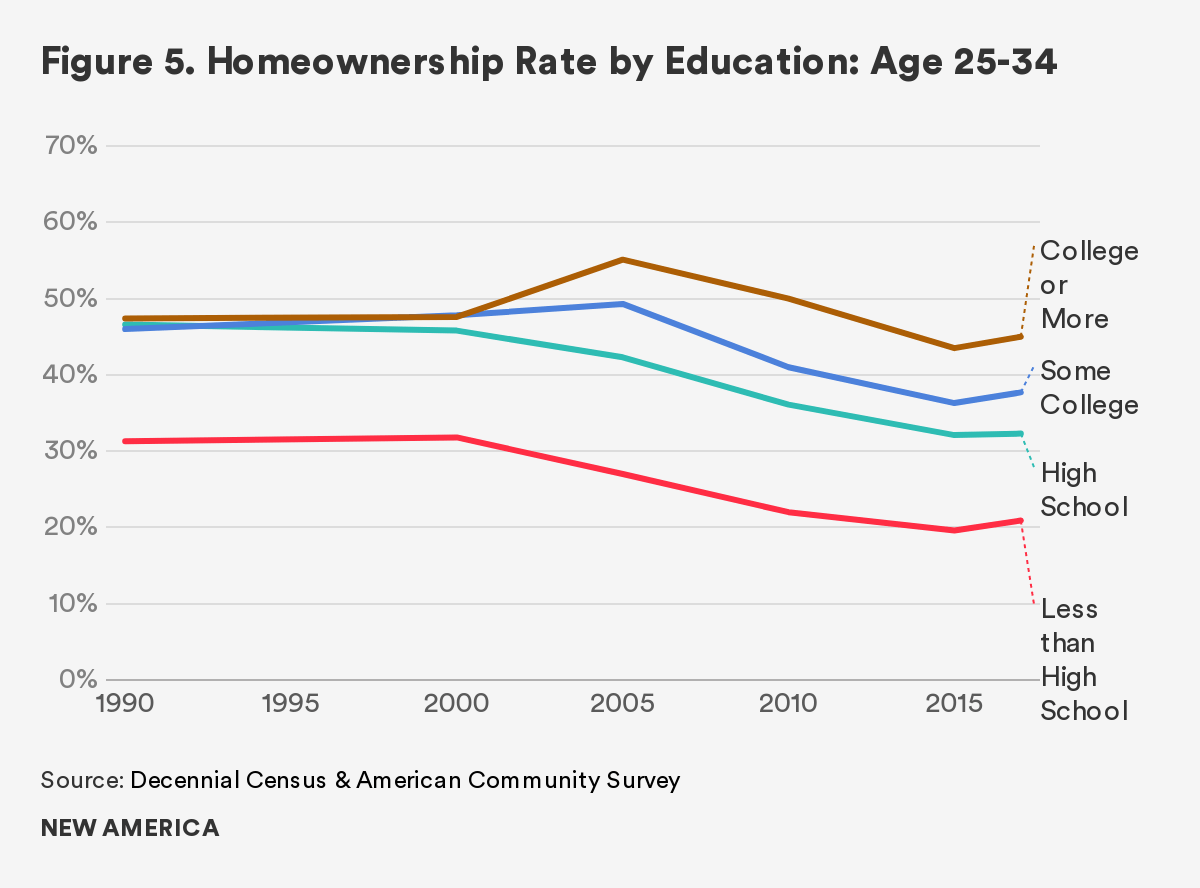

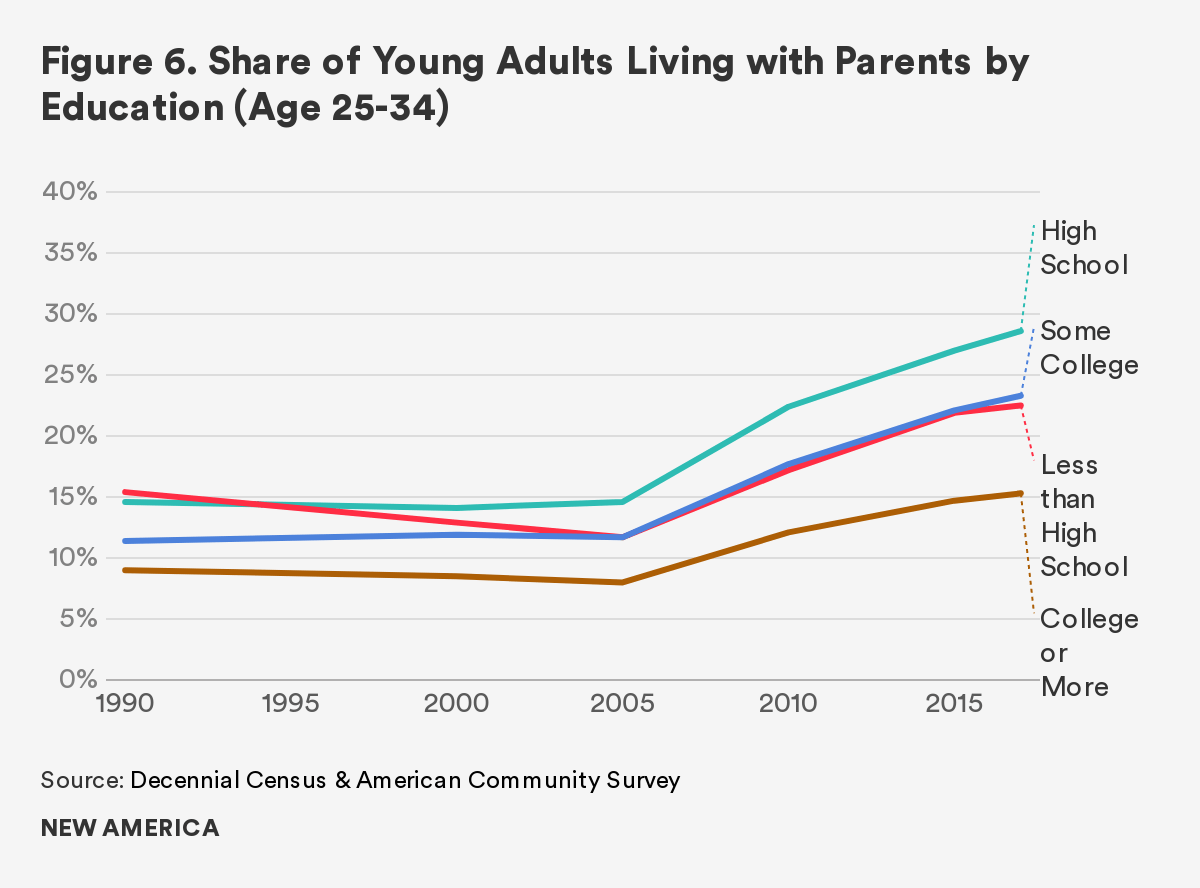

The homeownership gap across education groups also widened between 2000 and 2017. In 1990 and 2000, the homeownership rate of those with only a high school degree was similar to those with a bachelor’s degree. However, since 2000, the homeownership rate of young adults with high school or less education has constantly dropped, while the homeownership rate of those who received more education increased during the housing boom of 2000–06. Moreover, those with higher educational attainment have shown a slightly faster recovery in their rate of homeownership since 2015.

High school graduates were most likely and college graduates were least likely to live with their parents in 2017. Again, the share of young adults who lived with their parents increased for all education groups, but the rate of increase was higher for those with lower educational attainment.

Why Is Millennial Homeownership So Low?

Millennials clearly show different patterns in homeownership and living arrangements. Before crafting a policy response, it is helpful to take a deeper dive into the factors that have driven this change.

Multiple reasons can explain why Millennials are less likely to be homeowners than generations earlier. Below, five potential factors are considered.

Shifts in Preferences

Some argue that Millennials have a lower desire to become homeowners. This could be due to their personal experiences with the housing market crisis. Even if they were too young to be homeowners during this time, many young adults watched their parents lose their homes. However, this most likely explains only a small proportion of the homeownership decline among Millennials.

Public opinion research actually finds that Millennials have a similar aspiration to be homeowners as did their parents’ generation. According to the 2018 Apartment List survey of about 6,400 Millennial renters, 89 percent stated that they would want to own a home sometime in their future (Salviati and Warnock, 2018). A recent study by the Federal Reserve Board also finds that Millennials do appear to have similar preferences toward housing consumption compared to prior generations (Kutz et al. 2018). Choi et al. (2018a) found that the attitude of Millennials toward homeownership has, in fact, become slightly more negative in recent years, but suggests that Millennials’ desire for homeownership is likely to recover as the economy continues to strengthen, home prices continue to rise, and the memory of falling home values and eroding assets fades in time.

Other related attitudinal shifts among Millennials include growing preferences for living in downtown areas, or in more expensive cities where affordable homes are less available. Studies, including Choi et al. (2018a), find that Millennials are more likely to move to cities with limited growth in housing supply (e.g. San Francisco, Los Angeles, and New York) and also are more likely to move to downtown areas where the prices of homes are higher. These choices may undermine Millennial home purchases. However, cities which have experienced rising prices are also where there are greater job opportunities, explaining why those are the places where Millennials might seek to live. The data indicate that the migration of Millennials to high-cost areas is particularly concentrated among those who received more education, and it doesn’t explain why the homeownership rate has dropped more among those with less education (Choi et al. 2018a).

Delaying Marriage

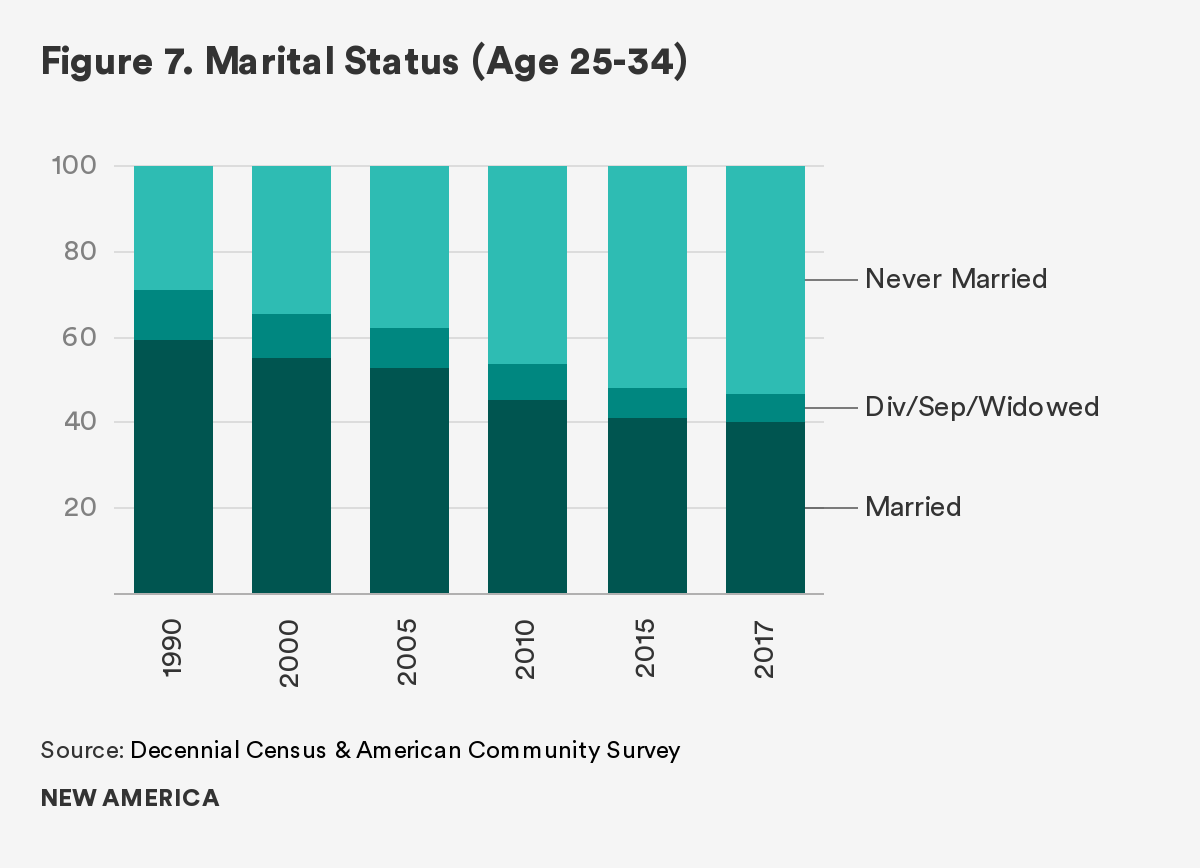

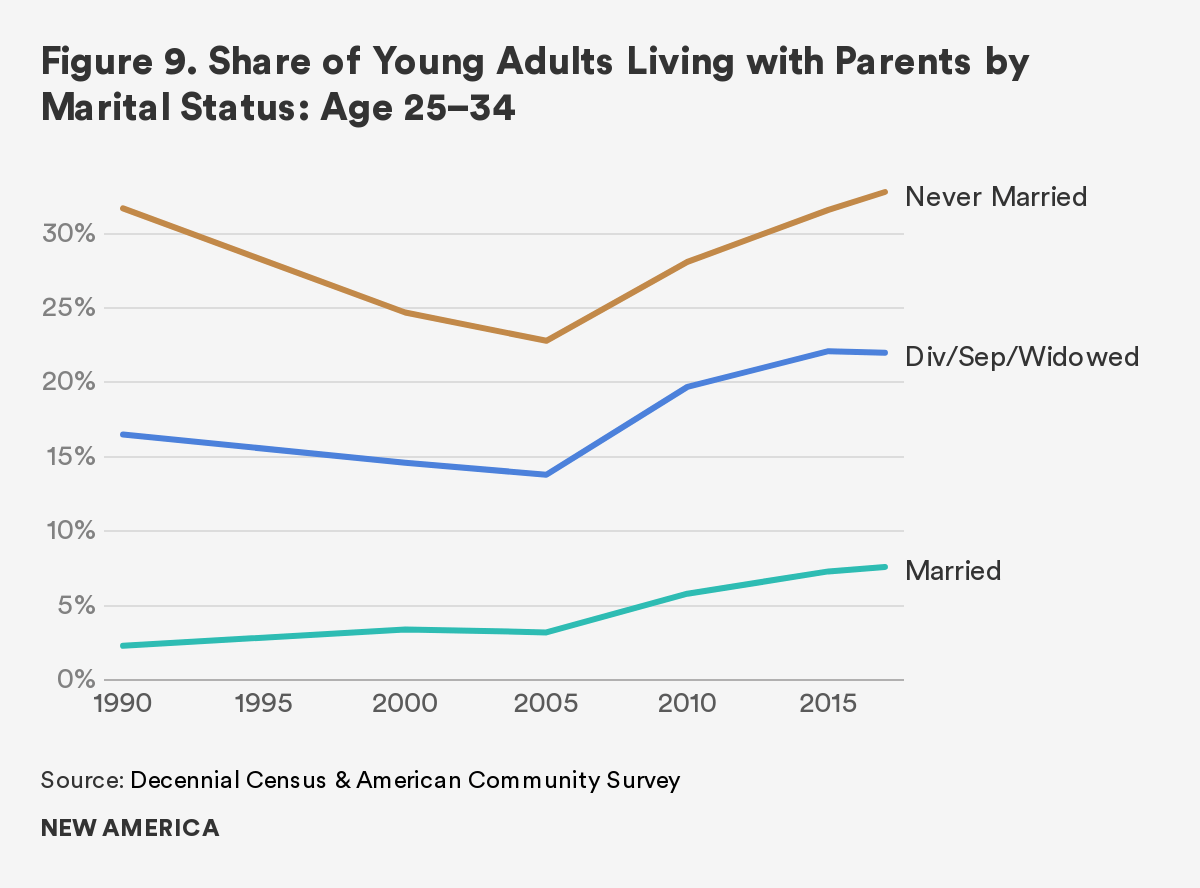

Millennials are more likely to delay marriage, a life event that is highly correlated with home buying and the decision to move out of parents’ homes. Only 40 percent of Millennials ages 25–34 were married in 2017, a substantial decrease from almost 60 percent in 1990. Those who never married increased by over 24 percentage points, from 29 percent to 53 percent.

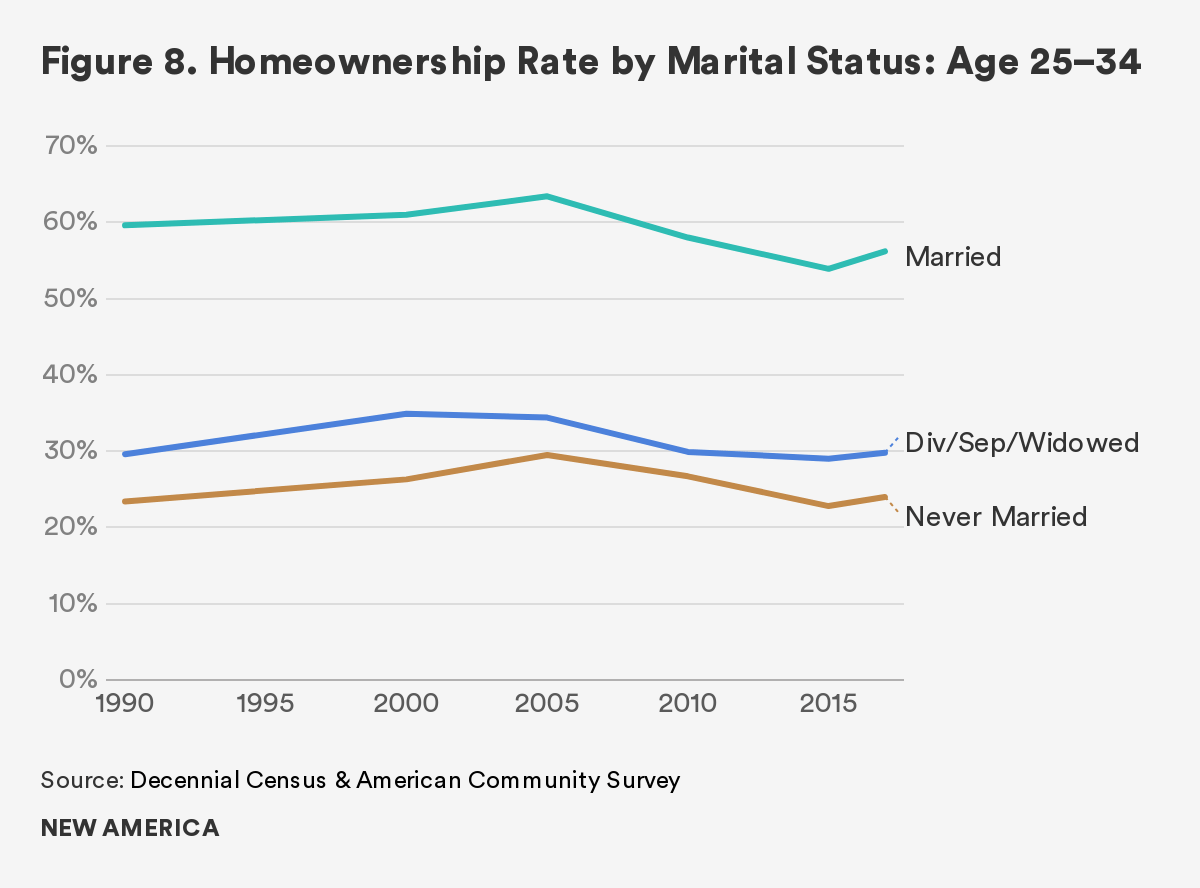

Figure 8 shows that those who are married or have experienced marriage are more likely to be homeowners than those who have stayed single. Additionally, young adults who have never married are most likely, and those who are currently married are least likely, to live with their parents. This indicates that changes in marital composition are associated with the drop in the Millennial homeownership rate as well as the increase in the share of young adults living with parents.

However, this alone does not provide a complete explanation, as married Millennials are also less likely to be homeowners and more likely to live with their parents than young adults in the prior generation (Figure 9). In fact, the Urban Institute (Choi et al. 2018a and Choi et al. 2019) finds that if the marital composition in 2017 had been the same as in 2000 while the homeownership rate and the share of young adults living with their parents stayed at the 2017 rate, the homeownership rate would increase by about 3 percentage points and the share of living with parents would increase about 5 percentage points. This narrows, but does not fully close, the gap between the prior and the current generations. It is likely there are common factors shaped by the larger economy, such as jobs, wages, and costs of living, that simultaneously affect young adults’ decision to delay both marriage and moving out of their parents’ homes.

Lack of Housing Supply

Just at the time when Millennials reach the age when many of their parents bought their first home, there has been an increasing shortage in the supply of affordable homes on the market. While home prices vary by geography, the average home prices today are higher than during the peak of the housing boom in late 2006.

Because of increasing land and labor costs, new housing construction has not kept up with the growing demand. Specifically, the number of new housing starts in 2018 is lower than that of the 1960s, when the U.S. population was only about 55 percent of what it is today. The lack of supply is driving up home prices beyond the reach of many Millennials. This supply shortage is placing upward pressure on rents, which not only means a larger share of income has to be devoted to housing costs but also makes it more difficult to save for a down payment. Choi et al. (2018) find that a 10 percent increase in the rent-to-income ratio decreases young adults’ likelihood of owning a home by 0.7 percentage points, and a 10 percent increase in residual income increases the likelihood by 0.5 percentage points, after controlling for demographic and socioeconomic characteristics. Furthermore, as both land and building costs increase, a greater portion of construction occurs at the higher end of the market, leading to a greater price increase at the lower end of the market, which has a more limited supply. These factors create significant challenges for first-time home buyers, with limited wealth and incomes, to find an affordable home which they are able to purchase.

Tighter Credit

Soon after the housing market began to collapse, access to credit tightened. This meant that potential buyers had a harder time qualifying for mortgage loans. These higher lending standards have persisted. The median credit score for mortgages at origination was 732 in March 2019—higher than the median of 692 in 2000, a period of reasonable lending standards (Goodman et al. 2019). Credit not only affects homeownership but also affects the decision to move out of parents’ homes and start renting, as landlords prefer renters who can prove their financial stability. Younger adults are more likely to have lower credit scores—the 2016 median credit score for Millennials was 640, 662 for Generation X, and 728 for Baby Boomers (Choi et al. 2018a). Furthermore, as many young adults have thin or no credit files, it is harder for them to rent a house or get a mortgage.

Lower Income and High Student Debt

During the Great Recession, the unemployment rate shot up to nearly 10 percent and incomes dropped significantly. Many Millennials entered the job market when it was harder to find work. Between 2005 and 2010 the percentage of young adults earning less than $15,000 per annum (constant 2017 dollars) increased from 27 percent to 32 percent, while those earning more than $50,000 decreased from 26 percent to 23 percent. As finding a job become more difficult, many chose to stay longer in school, pursuing a college degree or entering graduate school. This increased the number of Millennials with college degrees, but it also increased their overall debt load. Specifically, the share of college graduates increased from 28 percent to 36 percent between 2000 and 2017 (Choi et al. 2019).

During this period, student debt has more than tripled. According to the Survey of Consumer Finance (SCF), the average student debt of young adults ages 25–34 increased from $4,346 in 2001 to $17,120 in 2016. Higher student debt has a negative impact on Millennials’ attaining homeownership (Bleemer et al. 2017; Choi et al., 2018) and has deterred young adults’ decision to move out of their parents’ homes.

According to a recent Fed study, there would be 400,000 more Millennial homeowners if student loan burden had not financially constrained them (Mezza et al. 2019). The paper finds that student debt explains about 20 percent of the decline in Millennial homeownership. In a recent survey (American Student Assistance and National Association of Realtors, 2017), 75 percent of Millennials with student debt said that their student debt impacted their homeownership, and 42 percent answered that it was delaying them from moving out of a family member’s home after college graduation. Among those who answered that student loan debt is delaying their homeownership, 85 percent said that the debt is making it difficult to save for a down payment, 72 percent said it makes them reluctant to add more debt, and 52 percent said that because of their high debt-to-income ratio, they could not qualify for a mortgage.

What Are the Long-Term Consequences?

Understanding the range of reasons why homeownership rates have declined among young adults raises the question of potential long-term consequences for the economic outlook of the Millennial generation. According to the Urban Institute, those who lived with their parents between ages 25 and 34 are less likely both to form independent households and to become homeowners in the subsequent 10 years than those who moved out of their parents’ houses earlier in life (Choi et al. 2019). This suggests that the decision to delay forming households and becoming homeowners can have an impact on building future wealth. Two specific consequences demand further attention. First, families will have fewer resources available to access after retirement, potentially weakening the economic stability of future generations. Second, because homeownership and wealth transfer from parents to children, the homeownership disparities will continue to pass on to the next generation, reinforcing wealth inequality.

Lower Wealth at Retirement

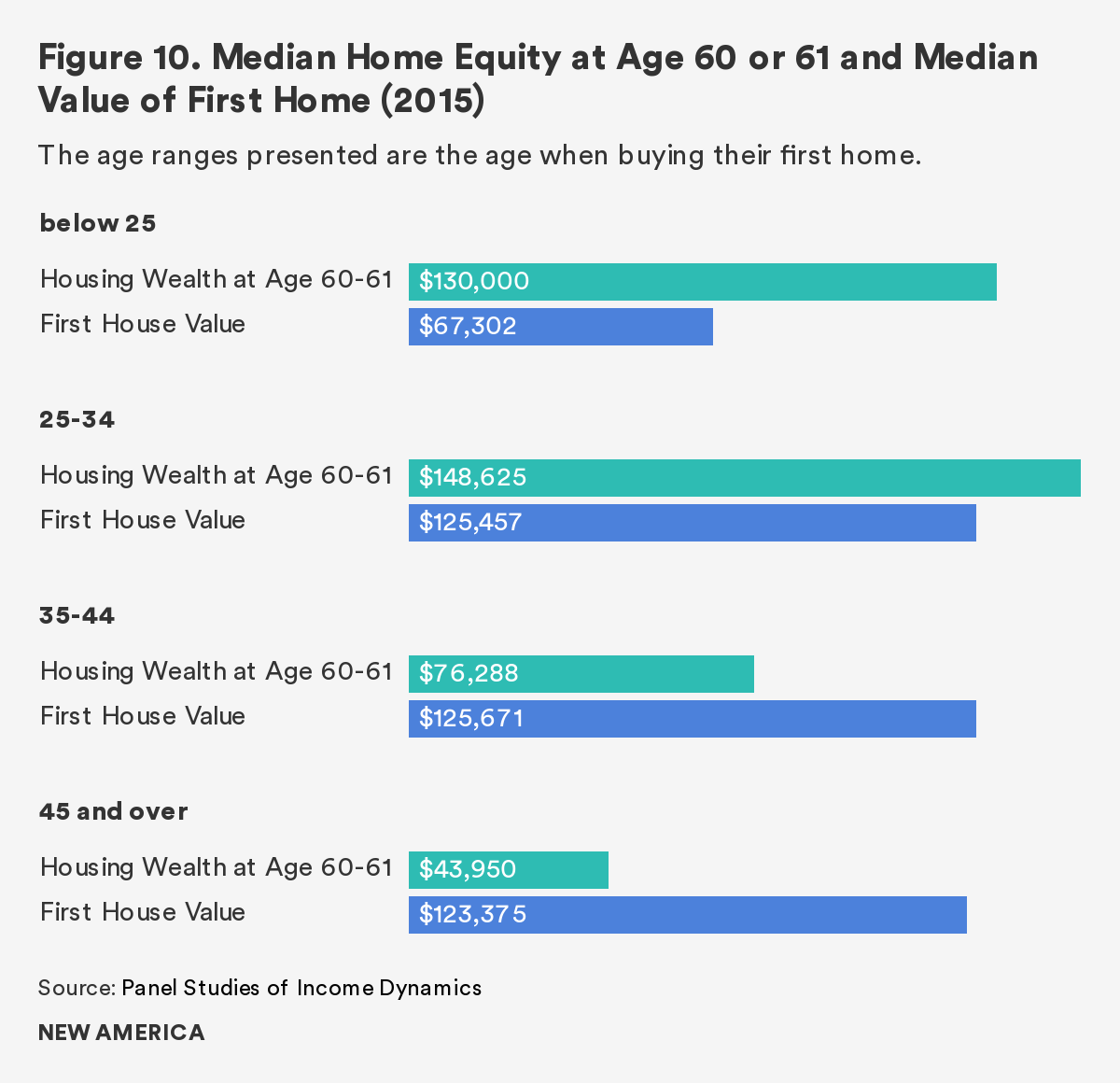

Buying a home at a younger age leads to greater housing wealth when households reach their retirement age. Using the Panel Study of Income Dynamics, Choi and Goodman (2019) calculated individuals’ housing wealth at ages 60 and 61 by the age at which they first bought a home. They found that the age of first home purchase had a significant relationship with future housing wealth. Those who bought their first homes between ages 25 and 34 had the largest housing wealth by their 60s. At age 60 or 61, their median home equity (in 2015 inflation-adjusted dollars) was close to $150,000, while for those who bought after age 45 and over, the median home equity was approximately $44,000, substantially lower (Figure 10).

While those who bought homes before age 25 have slightly lower housing wealth3 than those who bought their houses between ages 25 and 34, these young home buyers have the greatest return for their initial investment. The ratio between the median home equity at age 60 or 61 and median price of the first home decreases with the first age of home buying—the ratio is highest for those who bought their first home before age 25 (1.93) and decreases with the age of buying a first home.

With the rise in income volatility (Dynan et al. 2012) and the increase in life expectancy, housing wealth may be a more important tool for Millennials to secure financial well-being later in life. Therefore, the real impact of Millennials’ delay in homeownership may become apparent only in the decades to come.

Intergenerational Wealth Inequality

Parental wealth and whether or not a parent is a homeowner are positively associated with a child’s likelihood of owning a home later in life. Growing up with a homeowner parent could help a young adult gain access to homeownership in many ways. For example, parents could provide young adults with the necessary information about the mortgage application process. Further, having acknowledged the benefits of homeownership from growing up with a homeowner parent, the young adults may have stronger motivation to obtain homeownership. Parental wealth can have a more direct impact on a young adult’s financial ability to own a home, especially in terms of down payment. Affluent parents can more easily cosign a loan when support is needed. Lee and coauthors (2018) find that parents’ financial transfers substantially increase a young adult’s likelihood of becoming a homeowner. Charles and Hurst (2002) find that differences in parents’ ability to offer down payment assistance to their children explain a significant proportion of the Black–White mortgage application gap among Millennials.

In line with prior studies, Choi et al. (2018b) find that the children of homeowners are 7 to 8 percentage points more likely to become homeowners than children of renters, all else equal. Furthermore, a 10 percent increase in parental wealth increases young adults’ likelihood of owning a home by 0.15 to 0.20 percentage points. The study finds that the difference in parental homeownership and wealth explains about 12 percent to 13 percent of the homeownership disparities between Black and White young adults. This suggests that if policies do not respond, the Millennial experience with homeownership will have long-term consequences and even exacerbate the existing racial wealth gap.

What Can We Do About It?

After bottoming out in 2016, Millennial homeownership rate rose slightly to 38.4 percent in 2017. Despite this rise, the rate is approximately 7–8 percentage points lower than the rate Gen-Xers and Baby Boomers had at the same age. The data confirm that Millennials are less likely to form independent households, and many live in their parents’ homes for a longer period. The share of Millennials living with their parents is about 10 percentage points higher than for earlier generations, and this share has increased consistently since 2005.

Demographics and lifestyle choices, including delayed marriage, have affected the housing choices of Millennials. However, it is likely that prevailing economic conditions and institutional barriers are also creating obstacles to a higher Millennial homeownership rate. Higher rents, mounting student loan debt, tighter credit, and a limited supply of affordable housing all have made it harder to form independent households and realize homeownership. Because the low homeownership rate can have a long-term effect on future wealth and exacerbate wealth inequality for the generations to come, several policy recommendations should be pursued to increase homeownership among the Millennial generation.

Enhance Financial Knowledge and Home Buying Awareness

Financial knowledge and homeownership are highly correlated. For example, Millennials who had correctly answered a greater number of financial literacy questions were more likely to be homeowners (Choi et al. 2018a). In response, some states, such as Alabama, Missouri, Tennessee, Utah, and Virginia, require high schools to include a financial literacy course in their educational curriculum.

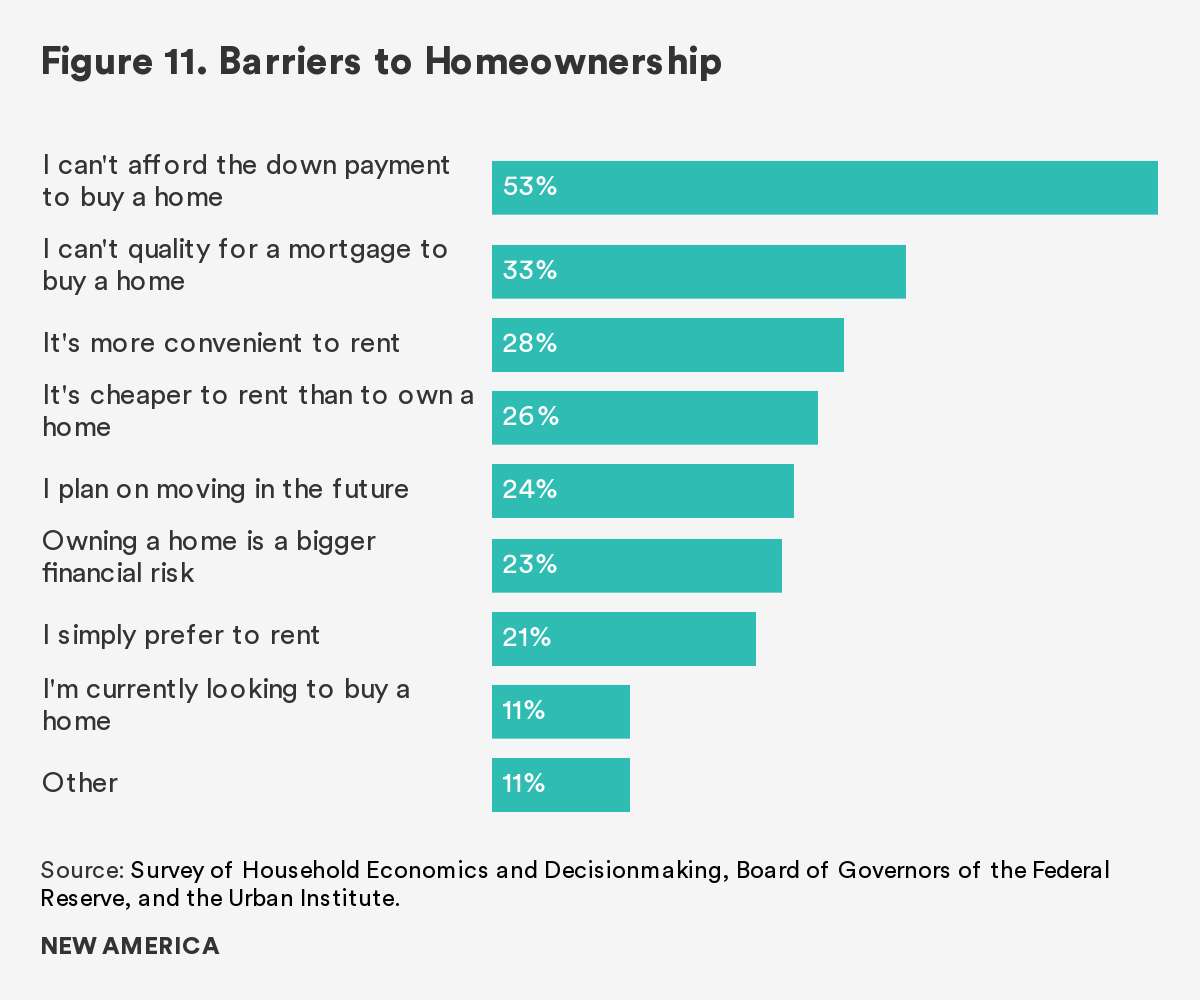

While financial education as part of a high school curriculum is a long-term solution worth promoting, there is an immediate need to give Millennials information to increase their awareness about their home buying ability. While the majority of renters point out the lack of down payment as the most critical barrier to homeownership (Figure 10), many do not have correct information about the down payment requirement or the existence of assistance programs that can make acquiring a mortgage more affordable. For example, almost 40 percent of young renters think they need to put down more than 20 percent to buy a home, but the median down payment is actually 5–7 percent (Goodman et al. 2018). Also, with Federal Housing Administration (FHA) loans, borrowers’ down payments can be further reduced to well under 5 percent. Three-quarters of young adults are unaware of their option to take advantage of this public program (Fannie Mae, 2015). Additionally, many nonprofit organizations and state housing finance agencies provide down payment assistance directed at first-time home buyers. Over 75 percent of renters do not know about or are not very familiar with such programs.

To enhance Millennial homeownership, innovative approaches to raise home buying awareness and provide the requisite financial knowledge will be necessary. Since Millennials rely heavily on computers and mobile devices, providing accessible and engaging online games and training courses could be one possible approach.

Use Technology to Simplify the Mortgage Process

Financial technology (FinTech) has the potential to streamline and increase the efficiency of the mortgage process. The current application process is extremely cumbersome, and lenders lack flexibility in working with borrowers. As a greater number of FinTech lenders enter the mortgage business, there are opportunities to identify more efficient mortgage origination and risk assessment systems, including using alternative data to evaluate a borrower’s creditworthiness. As the FinTech sector matures and offers services tailored to Millennials, a new channel to promote homeownership may be created.

Expand Credit Assessment Criteria

Mortgage applications underestimate many Millennials’ creditworthiness because they have not had time to build high credit scores. In fact, many do not even have FICO scores, the credit score used for mortgage approvals. If additional information, such as rental histories, cell phone and cable bills, and supplemental income, were included in mortgage underwriting, more Millennials would gain access to homeownership.

On-time rent payment is a good predictor of an on-time mortgage payment, as rental costs and mortgage payments are similar, in terms of amount and frequency of payment, for a comparable number of rooms (Zhu and Goodman 2018). Because most rental payments are captured in bank accounts, the information can be directly accessed from borrowers’ bank statements. Data on telecom, utility, and cable television payments could also be useful underwriting information.

In addition, Millennial income is often not fully captured during the mortgage application process. This is because current practice considers consistent income only for those who have worked in the same job or industry for two years. This doesn’t match the work experience of Millennials. For example, almost 40 percent of Millennials have a primary job with a W-2 but also earn additional income on the side (Choi et al., 2018a). Again, bank statements could help capture this supplemental income for young potential home buyers.

Ease Land-Use Restrictions to Promote Greater Supply

To increase the amount of affordable housing for Millennials to purchase, we need significant changes in land-use and zoning regulations. Since 1980, land-use and zoning cases have increased substantially and have increased land and construction costs (Ganong and Shoag 2017). As a result, developers are facing greater constraints to build, which have led to less construction and higher house prices.

Because zoning and land-use regulations are designed and implemented at the local level, executing a national-level policy will be challenging. States could provide financial incentives, e.g., reallocating housing subsidy dollars, to cities that reduce restrictions and regulation. Streamlining approval processes and allowing development by right are also possible solutions to promote greater housing supply and housing affordability. Acknowledging the problem, some localities have taken a bold approach to reform zoning and land-use regulations. For example, the city of Minneapolis recently eliminated all single-family zoning, allowing triplexes to be built anywhere in the city (Turner et al. 2019).

These four recommendations are not mutually exclusive and are not the only solutions that can help Millennials obtain homeownership or reduce homeownership disparities among young adults. Given the influence of the broader economy on housing outcomes, these recommendations need to be considered holistically in coordination with solutions in other sectors, including ways to improve the overall financial balance sheet of young adults. If earnings and savings fail to rise and debt loads remain high, future housing wealth will remain below what previous generations have experienced.

References

Dynan, Karen, Douglas Elmendorf, and Daniel Sichel. 2012. “The Evolution of Household Income Volatility.” Washington, DC: Brookings Institution.

Charles, Kerwin Kofi, and Erik Hurst. 2002. “The Transition to Home Ownership and the Black-White Wealth Gap.” Review of Economics and Statistics 84 (2): 281–97.

Choi, J. H., and Goodman, L. 2018. “Buy young, earn more: Buying a house before age 35 gives homeowners more bang for their buck.” Washington, DC: Urban Institute.

Choi, J. H., Zhu, J., and Goodman, L. 2018a. “The State of Millennial Homeownership.” Washington, DC: Urban Institute.

Choi, J. H., Zhu, J., and Goodman, L. 2018b. “Intergenerational Homeownership.” Washington, DC: Urban Institute.

Choi, J. H., Zhu, J., and Goodman, L. 2019. “Young Adults Living in Parents' Basements.” Washington, DC: Urban Institute.

Fannie Mae. 2014. “Fannie Mae National Housing Survey: What Younger Renters Want and the Financial Constraints They See.” Washington, DC: Fannie Mae.

Ganong, Peter, and Daniel W. Shoag. 2017. “Why Has Regional Income Convergence in the US Declined?” Journal of Urban Economics 102:76–90.

Goodman, Laurie, Alanna McCargo, Edward Golding, Bing Bai, Bhargavi Ganesh, and Sarah Strochak. 2018. “Barriers to Accessing Homeownership: Down Payment, Credit, and Affordability.” Washington, DC: Urban Institute.

Goodman, Laurie S., and Christopher Mayer. 2018. “Homeownership and the American Dream.” Journal of Economic Perspectives 32 (1): 31–58.

Kurz Christopher, Geng Li, and Daniel J. Vine. 2018. “Are Millennials Different?” Finance and Economics Discussion Series. Washington, DC: Federal Reserve Board, Divisions of Research & Statistics and Monetary Affairs.

Lee, Hyojung. 2018. “Are Millennials Coming to Town? The Determinants of Location Choice of Young Adults.” Urban Affairs Review 54 (5).

Mezza, Alvaro, Daniel R. Ringo, Shane M. Sherlund, and Kamila Sommer. 2017. “On the Effect of Student Loans on Access to Homeownership.” Washington, DC: Federal Reserve Board, Divisions of Research & Statistics and Monetary Affairs.

Salviati, Chris, and Rob Warnock. 2018. “2018 Millennial Homeownership Report: American Dream Delayed.” Apartment List.

Turner, Margery Austin, Solomon Greene, Corianne Payton Scally, Kathryn Reynolds, and Jung Choi. 2019. “What Would It Take to Ensure Quality, Affordable Housing for All in Communities of Opportunity?” Washington, DC: Urban Institute.

Zhu, J., & Goodman, L. 2018. “Rental Pay History Should be Used to Assess the Creditworthiness of Mortgage Borrowers.” Washington, DC: Urban Institute.

Citations

- Young adults living in group quarters, which includes college residence halls, residential treatment centers, skilled nursing facilities, group homes, military barracks, correctional facilities, and workers’ dormitories, are omitted from our analysis.

- Note that homeownership rate is calculated by dividing the number of owner-occupied households with the number of total households. The total number of households is the same as the total number of household heads. Millennials who do not form their independent households are not included in the homeownership calculation.

- Choi et al. (2019) find that the youngest buyers have lower incomes, are less educated, and therefore buy lower-priced homes, but are able to receive the greatest return compared to the initial size of investment.