Table of Contents

- The Emerging Millennial Wealth Gap: Opening Note

- Building Ladders of Success for the Rising Millennial Generation: An Initiative Funded by the Citi Foundation

- Part 1: Generational Wealth and Financial Health

- Framing the Millennial Wealth Gap: Demographic Realities and Divergent Trajectories

- Trends, Origins, and Implications of the Millennial Wealth Gap

- The Millennial Racial Wealth Gap

- The Young and (Economically) Restless: The Nature of Work for American Millennials

- The Financial Lives of Millennials: Evidence from the U.S. Financial Health Pulse

- Part 2: Components of the Millennial Balance Sheet: Assets and Liabilities

- Wealth and the Credit Health of Young Millennials

- Millennials and Student Loans: Rising Debts and Disparities

- Young Adults and Consumer Debt: The Quiet Crisis Next Time

- Homeownership and Living Arrangements among Millennials: New Sources of Wealth Inequality and What to Do about It

- Part 3: Implications for Social Policy

- Public Policy Implications of the Millennial Wealth Gap

- Addressing the $1.5 Trillion in Federal Student Loan Debt

- Policy Responses to the Millennial Wealth Gap: Repairing the Balance Sheet and Creating New Pathways to Progress

The Millennial Racial Wealth Gap

Fenaba R. Addo and Yiling Zhang

Wealth inequality among different racial and ethnic groups has been a defining feature of American society. However, new dynamics are emerging with the rise of the Millennial generation that will likely impact the extent of future divides. In this chapter, we examine racial wealth inequality among Millennial young adults. Along with summarizing wealth profiles of young Millennials of color, we explore wealth inequality within the context of historical legacies of Black-White wealth inequality, the proliferation of debt—specifically student loan debt—and the ongoing marital retreat. We also examine how the association of income and education with wealth vary significantly by race and ethnicity and contribute to pre-existing/intergenerational wealth gaps. If the trends we describe continue—and are ignored by policymakers—dramatic levels of inequality according to race and ethnicity will endure for decades to come.

Wealth Inequality and Race

According to the US Federal Reserve Bank, median household wealth in 2016 was $97,300 (Bricker et al. 2017).1 This is the amount of wealth owned by the typical family, where half have more and half have less. In general, households with higher incomes hold more wealth, and household wealth profiles increase with the age of the household head. Aggregate information of median wealth levels and its correlations with income and age, however, mask significant inequalities in wealth holdings. Wealth in the United States is highly skewed. Most of the population is concentrated at the lower ends of the wealth distribution, holding zero or negative net wealth, where their debts exceed their assets. Concurrently, the top one percent of households held 38.6% of the country’s wealth, and the top 10% held 77.2%, leaving 22.8% for the bottom 90% (Bricker et al. 2017).

The political, legal, and social context in which wealth generation has occurred historically favored White Americans, while the availability of resources to gain wealth has systematically been denied Black Americans. In other instances, factors affecting consumption choices were constrained, and incremental efforts to participate in the US economy have been far less likely to generate, accumulate, and maintain wealth (Oliver & Shapiro 2013). Given that wealth is often passed down intergenerationally, racial wealth inequalities have been reproduced over the course of American history and endure to this day (Oliver & Shapiro 2013; McKernan et al. 2014). The most recent wealth data from 2016 indicates that the median net wealth of White households was $171,000, compared with $20,700 for Latinx households and $17,600 for Black households. These figures identify the basic parameters of the racial wealth gap by capturing the wealth experience of typical families in each group. Yet absolute gaps based on average wealth are even larger given extreme concentrations of wealth at the high ends of the distribution (Bricker et al. 2017). In some respects, these figures should not be surprising given how prevailing US racial wealth inequality is rooted in intergenerational racial wealth inequality, with wealth gaps present in younger generations. However, the current distribution of wealth should also be acknowledged for its significance in creating fundamental privilege and disadvantage and undermining national aspirations of fairness and equality.

Income and Wealth

Millennials transitioned to adulthood during a period of both economic prosperity and instability, shaped significantly by the Great Recession, which spanned 2007 to 2009. Despite the large number of young adults that went to college and obtained degrees, they entered a tight labor market with young adult Millennials more likely to be unemployed compared to other working-age adults (Taylor et al. 2012). Even after the economy began to rebound, labor force participation and unemployment trends varied by race and ethnicity. Notably, Black young adults continued to have higher rates of unemployment with slower job growth post-Recession (Jones & Schmitt 2014; Kochhar 2012; Taylor et al. 2012).

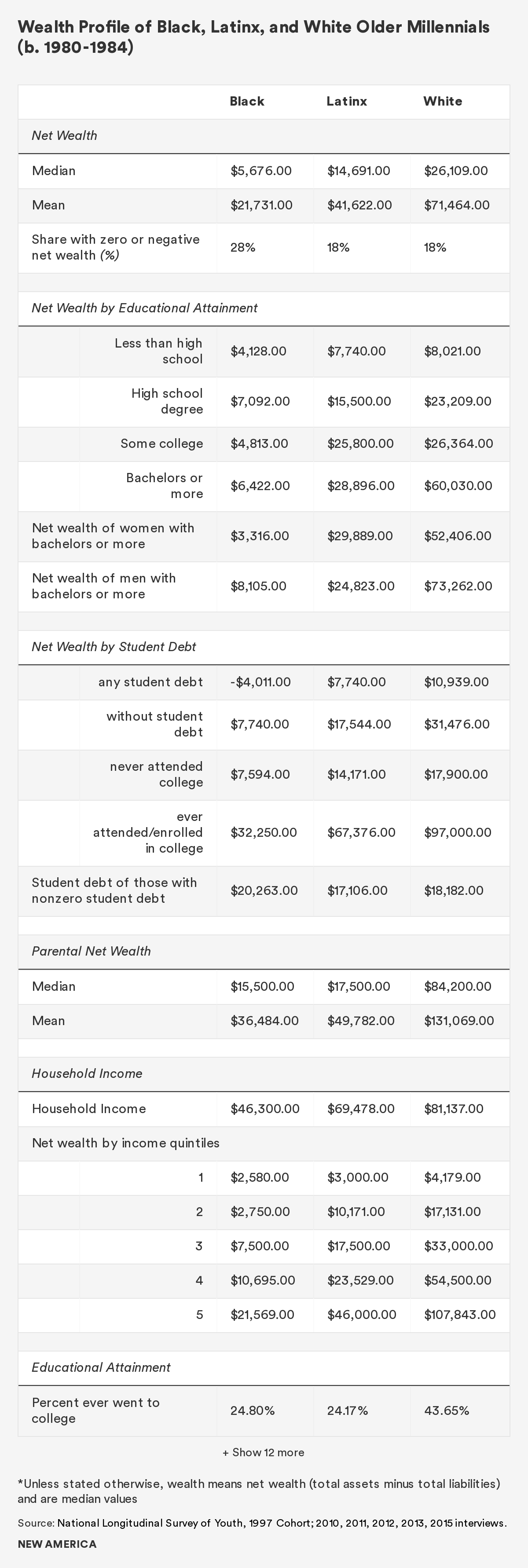

Since low wages and labor market disconnectedness are often posited as dominant explanatory factors for racial wealth differentials, this experience of different groups in the wake of economic downturns is important to consider (Aliprantis & Carroll 2019; Barsky et al. 2002). This, however, implies that the direction of causality runs from income to wealth, and ignores the intergenerational transmission of wealth and the potential for the relationship to run the other way—from familial wealth to income. In fact, Millennials’ wealth mirrors that of their parents. Among the oldest Millennials, those born between 1980 and 1984, who have had some time to get farther along on their economic trajectory, the median wealth of Latinx adults lies between that of Black and White adults. Specifically, the median wealth of Latinx Millennials is $14,691, more than twice the median wealth of Black Millennials, who hold $5,676, and slightly more than half the wealth of White Millennials, at $26,109. At the very least, racial gaps in Millennial income reflect economic inequality only to a lesser extent. By their early thirties, the median household income of Latinx adults ($69,478) was greater than that of Black Millennials ($46,300), but lower than White Millennials ($81,137).

The median net wealth by income quintiles of Millennials (presented in the table at the end of chapter) shows both a distinct hierarchy and stark disparities according to race and ethnicity. The wealth holdings across the income distribution for both Black and Latinx Millennials are below White Millennials. Specifically, Black Millennials in the top income quintile hold less than half of the median wealth of Latinx Millennials, and Latinx Millennials in the top income tier hold less than half the median wealth of White Millennials. Even at the top of the income distribution, both Black and Latinx Millennials hold significantly less wealth.

While there are disparities according to race and ethnicity in the distribution of both income and wealth, the racial wealth gap is wider. This holds true among young adults. Wealth inequality between Black and White Millennials was 2.6 times larger than income inequality, and 1.5 times larger for Latinx and White Millennials. Despite less variation in median incomes across race and ethnicity, wealth gaps among different racial and ethnic groups are large and significant.

Post-secondary Schooling and Education Debt

Higher education is the best example of unequal returns to wealth generating resources for Millennials. The data show that Millennials have pursued post-secondary schooling and obtained college degrees in young adulthood to a greater extent than previous generations (NCES 2016). While 44% of White Millennials have gone to college by the age of 30, and 35.3% have completed their degrees, in contrast, 25% of Black Millennials have gone to college, with only 18% obtaining a degree. Among Latinx Millennials, 24% have at least some post-secondary education, and 17% hold a college degree.

Not only is racial wealth inequality present in the Millennial population, but the gap also grows even larger when examining Black and White young adults with college degrees. Recent work suggests that student loan debt disparities may be contributing to these racial wealth gaps among Black and White Millennials (Houle & Addo 2018). When looking at student loan debt data, it is clear that Black Millennials took on a great deal more financial risk in pursuit of a college degree. They have acquired more education debt, and their repayment of education debt is slower (Houle & Addo 2018; Scott-Clayton & Li 2016).

Several mechanisms contribute to these observed debt disparities, including family background, postsecondary characteristics, and credit and labor market factors (Houle & Addo 2018). In response to rising tuition, students and their families have had to increasingly make up the difference between college costs and insufficient financial aid packages. However, research indicates that there were different impacts of parental wealth depending on race and ethnicity. For White young adults, their amount of education debt decreased as their parent’s wealth increased. Whereas for Black young adults, parental wealth was not associated with the amount of debt their children accumulated (Addo, Houle & Simon 2016). The Black-White wealth distributions are so incongruent that Black parents only comprise 3.2% of the top wealth quintile, which was defined as holding at least $191,000 (Addo 2018). This work suggests that intergenerational class status was not guaranteed for Millennial Black young adults. Similar to their parents and grandparents’ generations, they may find the pathway to middle-class status and long-term financial security a tenuous one.

Black borrowers also turned to private loan markets in greater percentages (Dillon & Carey 2009). Relative to federal loans, these loans are associated with costlier debt given the high and variable interest rates. They also lack similar protections afforded federal loans, such as loan forbearance, with a negligible chance of discharge in bankruptcy. And once in the labor market, Black young adults still face discrimination (Gaddis 2014). They are more likely to be unemployed or underemployed, holding jobs that do not require a college degree (Jones & Schmitt 2014). High-cost loans, discriminatory practices, and unequal wages are just a few of the structural barriers that inhibit college-attending Black Millennials from paying down their education debt at similar rates as their White counterparts.

These factors can have long-lasting consequences. There is suggestive evidence that not only are young adult Millennials acquiring student debt because of the limited wealth resources of their families, but that student loan debt is associated with lower wealth accumulation for Millennials. Young adult Millennials with student loan debt by age 30 have significantly less wealth than their counterparts with no debt, inclusive of those who never attended college and those who did. The wealth returns to a college degree appear to have greater benefits for those who either had no loans or were able to pay them back quicker.

These patterns are consistent for Black, Latinx, and White Millennials, yet the racial wealth differentials persist across all categories. Depending on whether they have outstanding student loans, White wealth is two to four times greater than Black wealth and 1.2 to 1.8 times larger than Latinx wealth holdings. Compositionally, Black and White educational debt disparities account for 10.5% of the racial wealth gap (Houle & Addo 2018); and for college graduates, for whom racial wealth gaps are greatest, it explains close to 20% (Addo 2019). Alternatively stated, if the education loan debt disparity was eliminated, wealth inequality between Black and White young adults with college degrees would decrease by 20%.

It is not surprising that the median wealth of all Millennials with any debt at age 30 is lower than those with no debt who attended college; however, their median wealth levels are also lower than young adults who never attended college. Uncovering these realities has led scholars to express concern that student loan debt may be reproducing racial wealth inequalities among the latest generation of youth (Addo, Houle & Simon 2016; Scott-Clayton & Li 2016).

It is important to note that gender wealth disparities persist despite the relative gains women continue to make in their educational pursuits. The relationship is more nuanced once the racial and ethnic diversity of Millennials is considered, however. Similar to Gen Xers, Millennial women have higher graduation rates than men, 39% compared with 30% (Frey 2018). White women have the highest graduation rates at 39.62% followed by White men, 31.24%. The wealth of White female college graduates ($52,406) far exceeds Black ($3,316) and Latinx ($29,889) female graduates but is lower than White men by almost $20,000.

The gender disparity in college completion is even greater among Black Millennials, where Black women completed college (22.76%) at almost twice the rate of Black men (13.36%). Yet, the median wealth of Black male Millennials ($8,105) was 2.5 times greater than Black female graduates ($3,316). Latinx women and men have the smallest gap in graduation rates, with less than a 4% difference. Comparable to the aggregate wealth levels, the figures for Latinx graduates lie in between the Black and White median values.

Interestingly, Millennial college graduates of Latinx descent are the closest to having gender wealth parity, with only a $5,000 difference in median wealth. And unlike Black and White college graduates, it is Latina women who have the higher median wealth. Significantly, this relationship exists only among college graduates. Not only does the median wealth of Latinx men with some college ($37,152) exceed the wealth of Latinx women with some college ($25,284), but it is greater than the median wealth of Latina college graduates ($29,889). This relationship also holds among Black college attendees (Bhattacharya, Price & Addo 2019). These wealth differences indicate that obtaining some of the highest levels of education did little to close racial wealth gaps among Millennials and is no guarantee of gender economic equality, for Black women in particular (Hamilton et al. 2015). Of course, these numbers reflect differences in several wealth-generating domains beyond education, including inherited wealth from their parents and grandparents, labor market returns, occupational segregation, asset ownership, and family structure, which we turn to next.

Marriage and Wealth

Along with distinct trends in wealth, education, and education debt that vary by race and ethnicity, Millennials’ relationship with marriage continues to diverge from previous generations and also varies by race. Specifically, Millennials are getting married later, reflected in the highest median age at first marriage, and are more likely to be never married (Bialik & Fry 2019).

With a smaller proportion married in young adulthood, the marital retreat has spread throughout the income and wealth distribution. However, it has not occurred uniformly across race and ethnic groups. Marriage rates for White, Latinx, and Asian Millennials are within eight percentage points of one another—48%, 45% and 52% respectively—and when combined with those with any marital history, more than half of their ethnoracial groups have ever married (Frey 2018). Marriage rates for Black Millennials are the lowest, at just over a quarter ever married and a fifth currently married.

The low number of women who married in young adulthood among Millennials also means there are more children born to unmarried women. A quarter of Millennial Black women were unmarried at the time of the birth of their first child, compared with 11% of Latina and 7% of White unmarried mothers. Differences in family building patterns, such as the sequencing of childbearing and marriage, and the timing of union formation, are associated with different wealth and economic outcomes. Since married individuals tend to have more per capita wealth than unmarried or cohabiting individuals, these trends in family formation and child rearing reflect another source of inequality that is compounded by characteristics of race and ethnicity (Addo & Ricketts, 2019). Not unlike previous generations of Black women, marriage is not a panacea for Millennial Black women, but it does appear to impact economic and social stratification (see Addo & Lichter 2013).

In particular, marriage’s relationship with wealth differs among White, Black, and Latinx married Millennials. Although Black married Millennials hold over two times the amount of per capita wealth of unmarried Black Millennials, their wealth holdings, $9,625, are less than single White Millennials, $12,032. This is important given the standard trope that marriage disparities cause racial wealth inequality. Married Latinx Millennials, whose marital rates are closer to White Millennials, have a little more than half their wealth, $13,777. Independent of marital status at birth, the median wealth holdings of Black mothers is low, less than $5,000; however, the median wealth holdings of Black Millennial married mothers ($4,200) was also lower than that of unmarried Black mothers at birth ($4,065).

This data indicates that among Millennials the economic bar to marriage is high and is more pronounced for Black women, in particular. Although the marriage rates of Latina women are closer to White women, their wealth holdings are about half. As fewer Millennials marry, wealth is concentrated among this small share of married households, who are already more likely to be White and socioeconomically advantaged. Given that economic markers of current and future financial insecurity, like education debt, are associated with remaining single or cohabiting among Millennials (Addo 2014), it is unsurprising that debt and wealth disparities stratify family formation patterns by race and ethnicity among Millennials.

Increasing Racial/Ethnic Diversity and Its Impact on the Racial Wealth Gap

The relative wealth positions of White and Black Millennials are analogous to those in previous generations, with White households positioned at the top and Black households at the bottom. White Millennials have more than three times the median wealth of Black Millennials, and a smaller share of them hold negative or zero net wealth. However, the story of race and wealth in America is changing with an increasingly diversified population. Due to the rise in in-migration from Latin American and Asian countries from the late 1970s through the early 2000s, the racial and ethnic composition of the Millennial population differs from earlier birth cohorts (Migration Policy Institute 2019). For example, sizeable portions of Millennials are immigrants who were not born in the United States. Fifty-six percent of Asian Millennials were not born in the US, and 36% of Latinx Millennials were born abroad, compared with 10% of Black Millennials and 4% of White Millennials (Frey 2018). Others are the first generation of children born to immigrant parents. Some have argued that racial and ethnic diversity among Millennials is evidence that the US is transforming from a majority White past to a future composed of a broad set of people of color (Frey 2018). Others, however, challenge the inevitability of this assertion given historic norms of immigrant populations to self-identify over time within the Black-White race-based binary in the US (Alba 2016; Darity 2016).

Based on the demographic composition of Millennials, a more accurate assessment of Millennial differences in wealth by race and ethnicity should account for intra-group variation in national origin,2 and the amount of wealth immigrant families bring with them to the United States. For example, data limitations have been a persistent problem when attempting to obtain more comprehensive information on the wealth holdings of Asian Americans.3 There is currently no publicly available nationally representative information on the wealth profiles of Millennial Asian Americans, who compose 6% of the Millennial population (Frey 2018).4 Their socio-economic experience is distinct in so far as Asian American Millennials have the highest college graduation and marriage rates, and their homeownership rates surpass Black and Latinx Millennials, second only to White Millennials (Frey 2018). There is evidence suggesting that in some geographic regions across the US, Asian Americans have been able to translate their educational success into greater wealth. In Los Angeles, for example, the wealth of Japanese, Asian Indian, and Chinese Americans has outpaced White households (De la Cruz-Viesca et al. 2016).5 The demographic diversity present in the Millennial population raises important questions about the relationship between race and wealth in America within the context of the labor market, post-secondary education, and marriage.

New Millennial Dimensions to the Historic Racial Wealth Gap

The racial wealth gap has been a central feature of American history. The experience of slavery and its aftermath have been endemic to the national story, driving the economy of the country, producing a Civil War, and defining political divides up to the present day. Looking closely at the experience of Millennials broken down by race and ethnicity demonstrates that this history is still with us. Specifically, there are elements of the current racial wealth gap that are historical artifacts. Given how wealth is distributed intergenerationally, we would expect these inequities to be passed down. And they have been.

There are, however, additional ways that current conditions can exacerbate wealth inequalities that are present from birth. Specifically, we have explored how persistent racial wealth gaps among young adult Millennials are extended through pathways that include access to higher education, degree completion, minimal or modest debt, and marriage to others with education and economic resources. As the Millennial and other rising generations have become more diverse, these trends are reinforcing and compounding past inequalities. Even though the Millennial wealth gap has deep roots and connections to the racial wealth gap of previous generations, it has, in fact, been extended through more recent experiences.

For example, young adult Millennials experienced significant wealth loss during the Great Recession (Emmons et al. 2018). The collapse of the housing market and subsequent foreclosure crisis disproportionately impacted neighborhoods with high concentrations of Latinx and Black homeowners (Bocian, Li, & Ernst 2010). Compared with White households, Black and Latinx households were slower to recoup this wealth post-Recession, which contributed to an increase in racial wealth inequality (Fry & Kochnar 2014). There is significant evidence that predatory and discriminatory lending practices were contributing factors in inflating the housing market in ways that triggered the onset of the Great Recession (Bocian et al. 2011). In this sense, it was traditional forms of discrimination repackaged under new systems that contributed to and compounded the country’s racial wealth gap, which is increasingly reflected in the balance sheets of today’s Millennials.

Shifts in the demographic composition of America, due in large part to immigration, are reflected in greater racial and ethnic heterogeneity. Although White Millennials are still the majority at 56%, Black, Latinx, and Asian American Millennials combined are over 40%. And yet, Millennial racial wealth inequality today reflects previous patterns, with Black households having the least amount of wealth. Evidence points to a new racialized wealth hierarchy emerging, with Latinx Americans situated in between Black and White American Millennials, and some Asian American communities at the top.

As the Millennial generation continues to age, the underlying dynamics impacting the distribution of wealth will become more complex. In the near term, the racial wealth gap in America will persist and remain large. Over an extended time horizon, the extent of the future racial wealth gap in America will hinge on a number of factors, including the potential for redistributive public policy interventions and also how Millennials choose to identify within the black-white binary.6 Undoubtedly, if we are to meet our national aspirations of fairness and equity, we will need to continue to focus attention on the role of race and ethnicity in the country’s distribution of wealth.

References

Addo, F. R., & Lichter, D. T. (2013). Marriage, Marital History, and Black–White Wealth Differentials Among Older Women. Journal of Marriage and Family, 75(2), 342-362.

Addo, F. R., Houle, J. N., & Simon, D. (2016). Young, Black, and (Still) in the Red: Parental Wealth, Race, and Student Loan Debt. Race and Social Problems, 8(1), 64-76.

Addo, F. R. (2018). Parents’ Wealth Helps Explain Racial Disparities in Student Loan Debt. In the Balance, (19), 1-3.

Addo, F.R. (2019). Racial Disparities in Student Loan Debt and the Reproduction of Inequality. Presentation.

Addo, F. R., & Ricketts, L. R. (2019) As Fewer Young Adults Wed, Married Couples’ Wealth Surpasses Others’. In the Balance. Federal Reserve Bank of St. Louis.

Alba, R. (2016). The Likely Persistence of a White Majority. The American Prospect, 27(1), 67-71.

Aliprantis, D. & Carroll, D. R. (2019) What Is Behind the Persistence of the Racial Wealth Gap? Economic Commentary (2019-03). Federal Reserve Bank of Cleveland.

Barsky, R., Bound, J., Charles, K. K., & Lupton, J. P. (2002). Accounting for the Black–White Wealth Gap: A Nonparametric Approach. Journal of the American statistical Association, 97(459), 663-673.

Bhattacharya, J., Price, A. & Addo, F. (2019). “Clipped Wings: Closing the Wealth Gap for Millennial Women.” The Insight Center.

Bialik, K. & R. Fry (2019). “Millennial Life: How Young Adulthood Today Compares with Prior Generations.” Pew Research Center.

Bocian, D. G., Li, W., & Ernst, K. S. (2010). Foreclosures by Race and Ethnicity. Center for Responsible Lending, 4-6.

Bocian, D. G., Li, W., Reid, C., & Quercia, R. G. (2011). Lost Ground, 2011: Disparities in Mortgage Lending and Foreclosures. Center for Responsible Lending, 3.

Bricker, J., Dettling, L. J., Henriques, A., Hsu, J. W., Jacobs, L., Moore, K. B., Pack, S, Sabelhaus, J., Thompson, J., & Windle, R. A. (2017). Changes in US Family Finances from 2013 to 2016: Evidence from the Survey of Consumer Finances. Fed. Res. Bull., 103, 1.

Darity Jr, W. (2016). The Latino Flight to Whiteness. The American Prospect.

De La Cruz-Viesca, M., Chen, Z., Ong, P. M., Hamilton, D., & Darity Jr, W. A. (2016). The Color of Wealth in Los Angeles. Durham, NC/New York/Los Angeles: Duke University/The New School/University of California, Los Angeles.

Dillon, E., & Carey, K. (2009). Drowning in Debt: The Emerging Student Loan Crisis. Charts You Can Trust.

Duncan, B., & Trejo, S. J. (2011). Tracking Intergenerational Progress for Immigrant Groups: The Problem of Ethnic Attrition. American Economic Review, 101(3), 603-08.

Emmons, W. R., Kent, A. H., & Ricketts, L. R. (2018) A Lost Generation? Long-Lasting Wealth Impacts of the Great Recession on Young Families. The Demographics of Wealth.

Frey, W. H. (2018). The Millennial Generation: A Demographic Bridge to America’s Diverse Future. Brookings Metropolitan Policy Program.

Kochhar, R., & Fry, R. (2014). Wealth Inequality has Widened along Racial, Ethnic Lines since End of Great Recession. Pew Research Center, 12(104), 121-145.

Gaddis, S. M. (2014). Discrimination in the Credential Society: An Audit Study of Race and College Selectivity in the Labor Market. Social Forces, 93(4), 1451-1479.

Houle, J. N., & Addo, F. R. (2018). Racial Disparities in Student Debt and the Reproduction of the Fragile Black Middle Class. Sociology of Race and Ethnicity, 2332649218790989.

Hamilton, D., Darity Jr, W., Price, A. E., Sridharan, V., & Tippett, R. (2015). Umbrellas Don’t Make it Rain: Why Studying and Working Hard Isn’t Enough for Black Americans. New York: The New School.

Jones, J., & Schmitt, J. (2014). A College Degree is no Guarantee. Washington, DC: Center for Economic and Policy Research.

Kochhar, R. (2012). The Demographics of the Jobs Recovery: Employment Gains by Race, Ethnicity, Gender and Nativity. Pew Research Center.

McKernan, S. M., Ratcliffe, C., Simms, M., & Zhang, S. (2014). Do Racial Disparities in Private Transfers Help Explain the Racial Wealth Gap? New evidence from longitudinal data. Demography, 51(3), 949-974.

Migration Policy Institute (2019). MPI Data Hub: Migration Facts, Stats, and Maps.

Oliver, M., & Shapiro, T. (2013). Black Wealth/White Wealth: A New Perspective on Racial Inequality. Routledge.

National Center for Education Statistics (NCES). (2016). Table 302.60. Percentage of 18- to 24-year-olds enrolled in degree-granting postsecondary institutions, by level of institution and sex and race/ethnicity of student: 1970 through 2015.

Scott-Clayton, J., & Li, J. (2016). Black-White Disparity in Student Loan Debt More than Triples after Graduation. Economic Studies, Volume 2 No. 3.

Taylor, P., Parker, K., Kochhar, R., Fry, R., Funk, C., Patten, E., & Motel, S. (2012). Young, Underemployed and Optimistic: Coming of Age, Slowly, in a Tough Economy. Pew Research Center.

Citations

- We use the term wealth to connote net wealth, typically calculated as the total value of a household’s assets minus the household’s total liabilities.

- Data limitations limit our ability to explore wealth differences by national origin in the present analysis.

- This is also the case for Native American Millennials. Their share of the millennial population has marginally increased, yet due to their small relative size, data sources and independent analyses are limited.

- Recent initiatives to gather more comprehensive data of wealth disparities within communities of color using multicity designs include The National Asset Scorecard for Communities of Color, which reveals vast inter-ethnic variations in wealth holdings within immigrant populations.

- In their sample, the wealth of Korean and Vietnamese households is lower than White households, but greater than Black and Mexican American households.

- See Duncan and Trejo (2011) on ethnic attrition of immigrant populations.