Table of Contents

Looking Ahead: How Climate Change Will Affect Natural Security

Shutterstock

Over the coming years, the changing climate will shape natural security in two important ways. First, rising global temperatures will affect resource availability. The changes will shift agricultural productivity poleward, increasing the length of growing seasons in cold climates, while high heat wilts crops closer to the equator. Second, as the world transitions from fossil fuels to renewable energy sources, the relative importance of resources will shift. There will also be effects on water—both freshwater and oceans—which we considered but did not fully examine for this report.

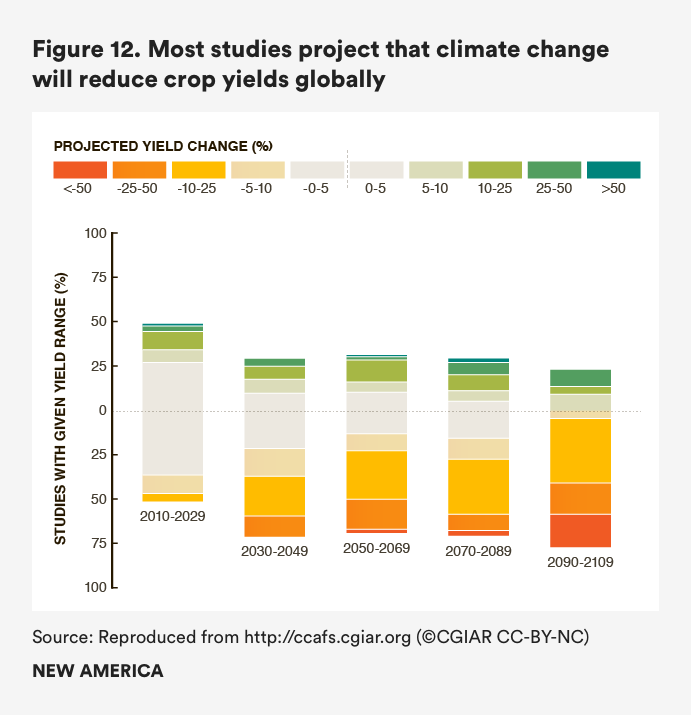

Although there is considerable uncertainty in crop yield projections, the majority of models agree that global crop yields will decline in the coming decades. Moreover, increasing global food demand will likely require development of new agricultural land and substantially increased international trade from water-abundant areas to water-scarce regions. Greater variation in weather may increase risk of drought and water stress. In the breadbaskets of the U.S. heartland and northern China, groundwater tables are already falling.

Source: CGIAR (CC-BY-NC)

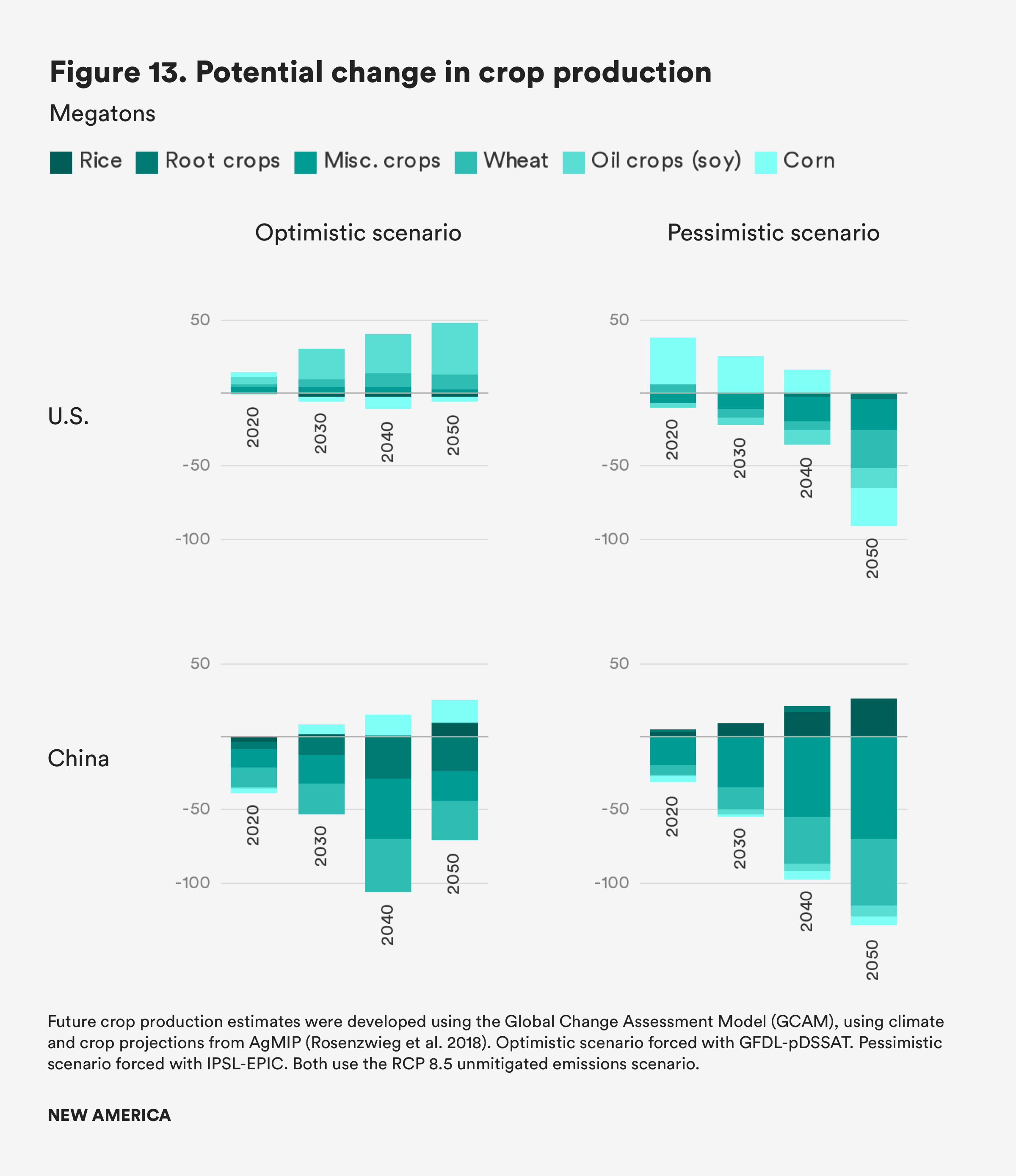

Together with the Joint Global Change Research Institute, we evaluated two global agricultural trade scenarios for 2050 and 2100 using the Global Change Assessment Model: an optimistic scenario where the net effects of climate change lead to short-term increases in productivity in the northern United States and China; and a pessimistic scenario where climate change leads to agricultural losses in both countries.1 Importantly, neither of these scenarios accounts for the possibility of increased competition for water or groundwater depletion, which may limit the availability of water for irrigated agriculture. The models also do not incorporate the effects of extreme events, such as floods, droughts, and wildfires, on agricultural productivity.

For the United States, the speed and magnitude of climate impacts will matter. In the optimistic scenario, agriculture in the south and west may suffer, but with few competing pressures for land, the United States can stay a major agricultural producer. If climate change impacts are more intense and water and heat stress put greater limits on crop productivity, U.S. farmers may no longer be able to produce a large export surplus. In both scenarios, Russia and Canada are likely to rise as important exporters.

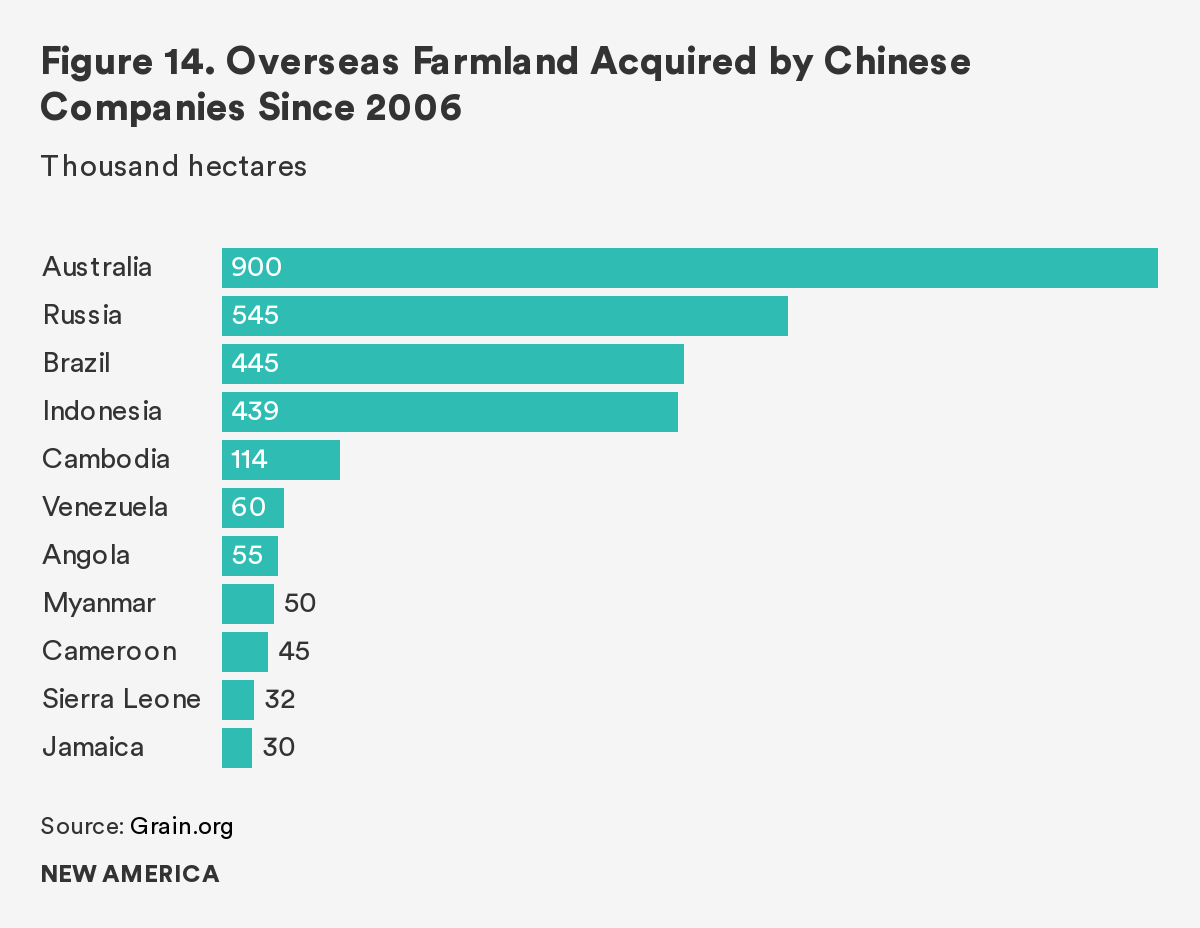

For China, the economics of land and trade are likely to mean greater imports under both scenarios, but with more urgency in the pessimistic scenario. While China currently grows enough corn, wheat, and rice to satisfy domestic consumption, climate change is likely to change this, especially for corn and wheat. Already China is increasingly looking outward for agriculture, as Chinese companies invest in purchasing agricultural land around the world. Soy producing giants such as Brazil and Argentina are likely to become more important suppliers in the short term as demand increases, especially if tariffs hamper U.S.-China trade.

The effects of these changes are likely to be felt across the world. Global agricultural markets are highly integrated, and droughts or other extreme weather events in major breadbaskets can create food price spikes around the world.

In addition to the effects on agriculture, climate change means a transition from traditional fossil fuel energy sources to renewables, though the pace of this transition is still unclear. In many places, wind and solar energy are already cost-competitive with coal-fired power plants. Automakers around the world are investing heavily in electric vehicles. Nonetheless, global greenhouse gas emissions rose in 2018.

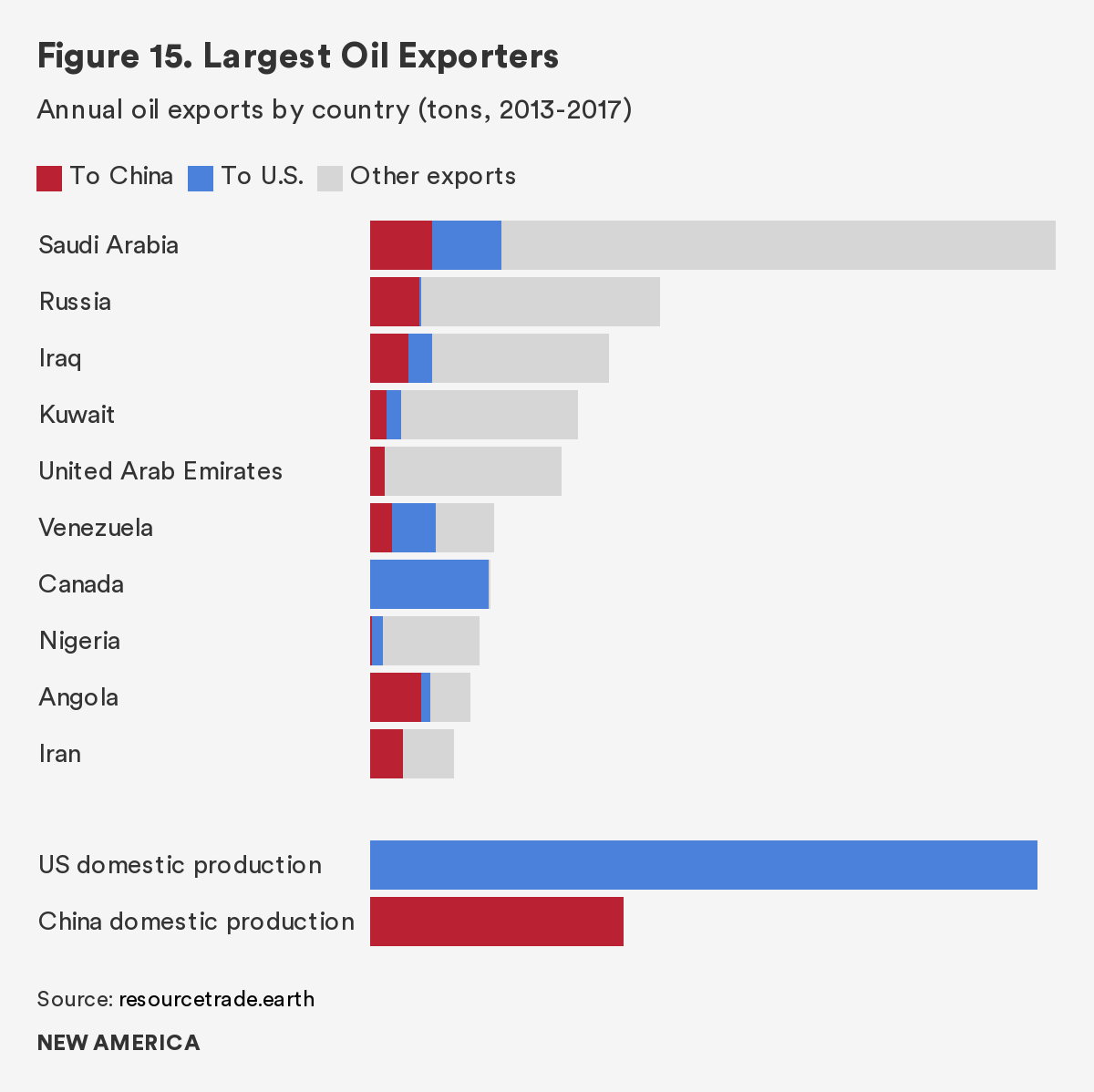

For the United States, a shift away from fossil fuels may lead to a strategic shift away from major oil-producing countries, such as Saudi Arabia, toward suppliers of critical minerals. Domestic U.S. oil production has increased substantially over the past several decades, and the United States is projected to become a net oil exporter by 2020 for the first time since 1948. Depending on the speed at which the United States adopts climate policy, a shift from gasoline to electric vehicles will further decrease oil demand. This will affect U.S. producing regions domestically, in terms of tax revenue and jobs, which is likely to refract through national politics.

A shift to clean energy technologies will also require a significant increase in critical mineral consumption. Current battery technology requires lithium and cobalt, for example, while rare earths are essential to magnets in electric motors and generators. The United States depends on China for many of these resources. The United States could produce some of these minerals at home, though not competitively in current markets. In any case, ramping up domestic mining and refining of these materials would require considerable investment, permitting, and environmental consequences, and it may take years for production to come online.

A shift to clean energy technologies will require a significant increase in critical mineral consumption.

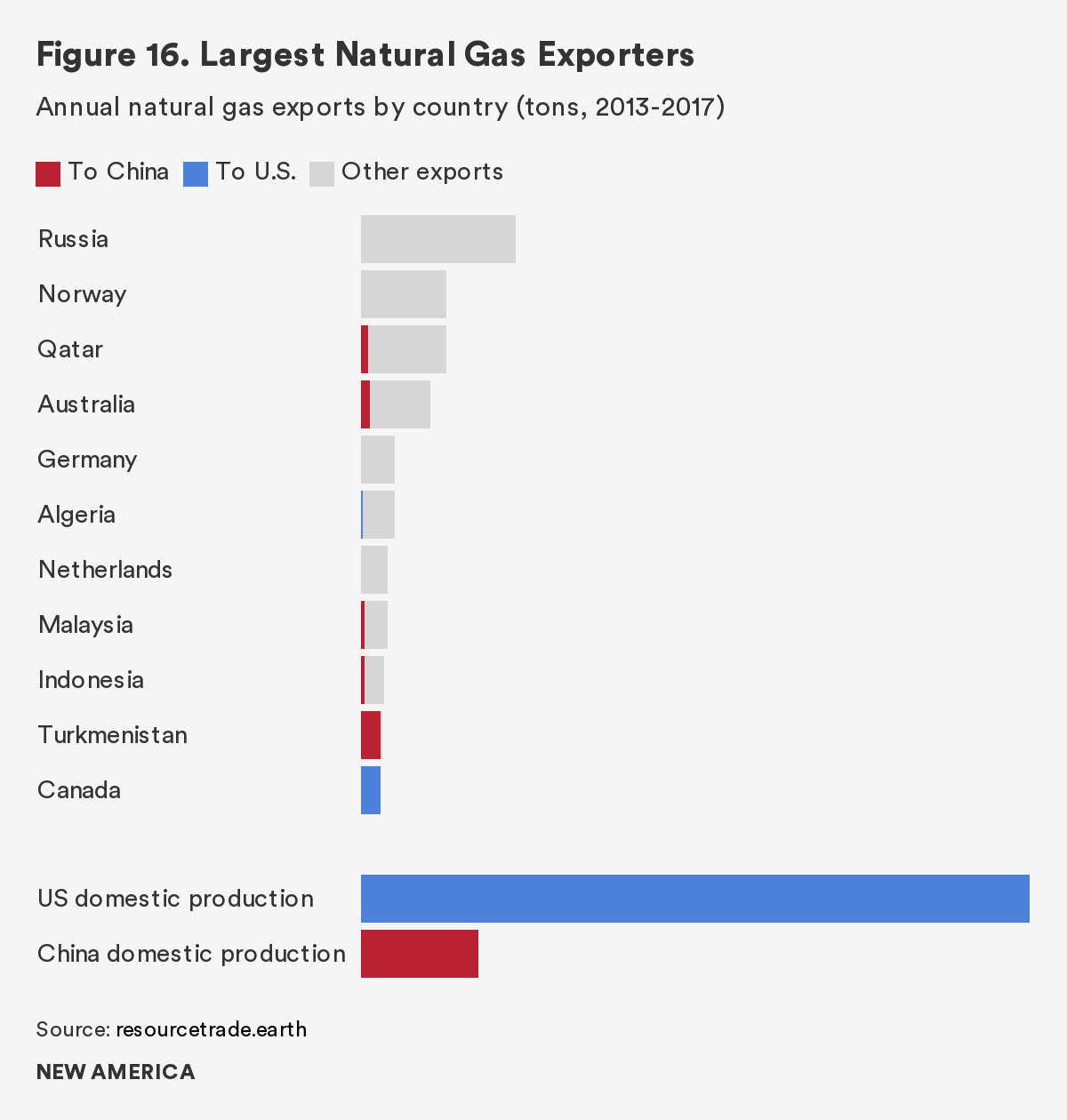

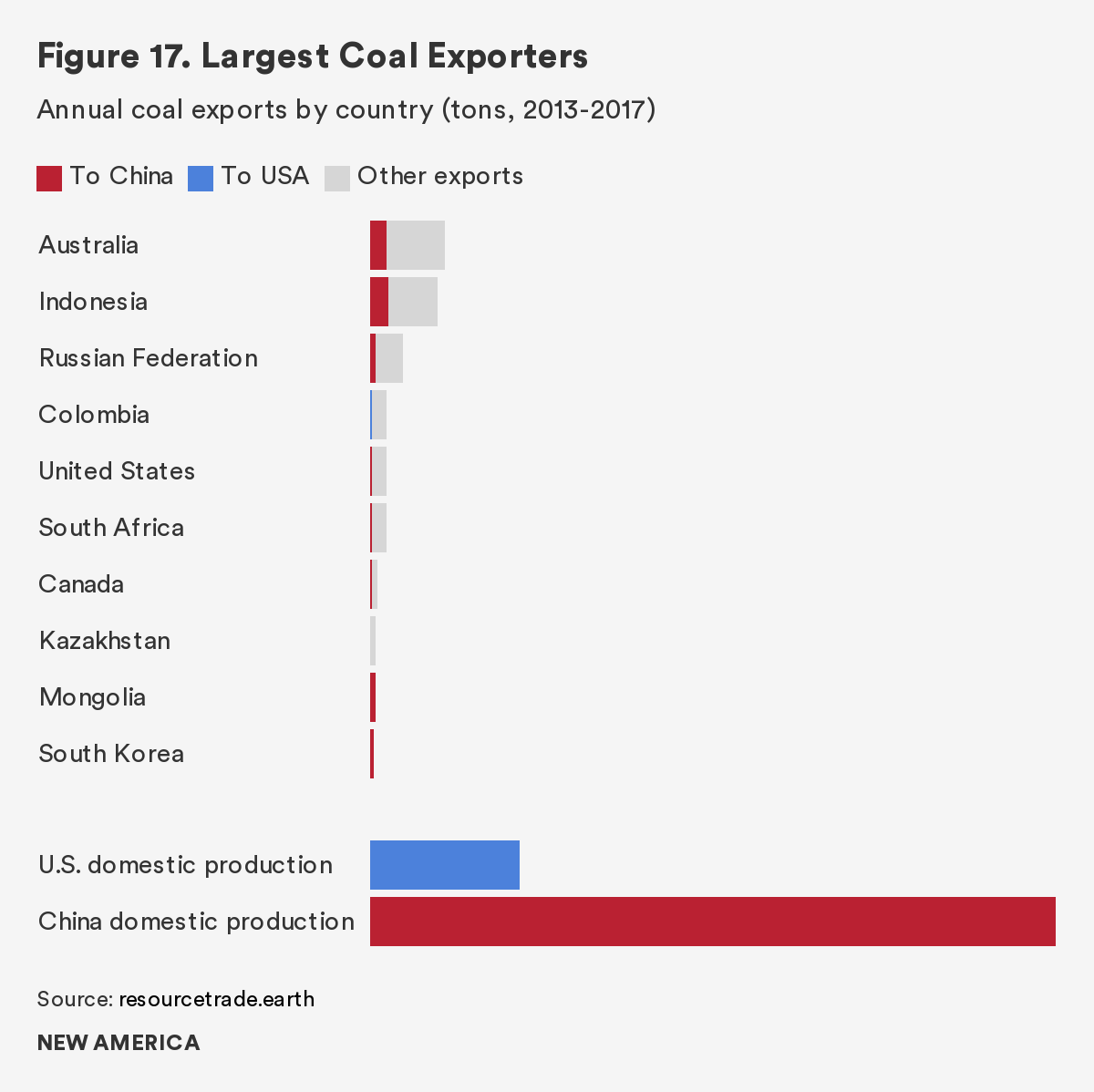

China is much less energy secure in terms of fossil fuels, although the country has substantial coal reserves and is seeking to diversify dependence on imported oil and cut greenhouse gas emissions through increased natural gas imports. China likewise is investing in renewable energy and electric vehicles, which will require increased consumption of both domestic and imported critical minerals, such as rare earth elements and cobalt. In addition to the threat of climate change, China faces domestic pressure to move away from coal due to air pollution concerns.

Energy security has long had geopolitical resonance. China’s relationships with major fossil fuel producers, such as Russia, Saudi Arabia, and Iran, have become increasingly important, with implications for the historically close ties between the United States and Saudi Arabia and the adversarial ones with Iran and Russia. In the future, as the two largest economies seek to gain a competitive edge in renewable energy technology, that will increasingly drive competition over critical mineral resources and major producing countries, such as Australia, Brazil, Chile, South Africa, and the Democratic Republic of the Congo.

The future of the world’s natural resource landscape will in large part depend on the fate of the U.S.-China relationship. Imports to the United States and China account for one quarter of the world’s trade in resources. If the two countries seek to disentangle their mutual dependence, it will result in major shifts to global supply chains and significant impacts on domestic industries. Meanwhile, new areas of resource competition are growing, and technological and climate change mean that the twentieth century’s understanding of resource security will no longer be valid. China is seeking to strengthen its natural security, investing in countries across the world. The United States’ response to this shifting landscape and the new competitive space will shape its security and prosperity in the century to come. Climate change will increasingly be a strategic driver when it comes to natural security, something China appears to be positioning for, with its diversified trade, investment, and national engagement strategy. The United States, on the other hand, appears to have no deliberate strategy when it comes to ensuring natural security in a changing climate.

Citations

- Both the optimistic and pessimistic scenarios assume business-as-usual increases in global greenhouse gas emissions (scenario RCP8.5), but use different models and assumptions in estimating climate change effects and impacts on crop productivity. The optimistic scenario uses GFDL for climate forcing and the pDSSAT crop model; the pessimistic scenario uses IPSL for climate forcing and the EPIC crop model. These scenarios do not account for increased probability of extreme weather events that may adversely impact agriculture.