Tables – Relief Payments

Note: This article was accurate as of its publishing on April 8. Since then, there have been multiple new developments. On April 10, the IRS released a self-service tool for non-filers, partially addressing the issues we raise in Section 3. On April 15, the IRS released a self-service tool for filers, partially addressing the issues we raise in Section 4. On April 15, the IRS announced SSI beneficiaries will be paid automatically; on April 17 they announced the same for VA beneficiaries, addressing the issues we raise in Section 2. And, in the course of these IRS updates, the messaging on irs.gov has somewhat improved, partially addressing the issues we raise in Section 1.

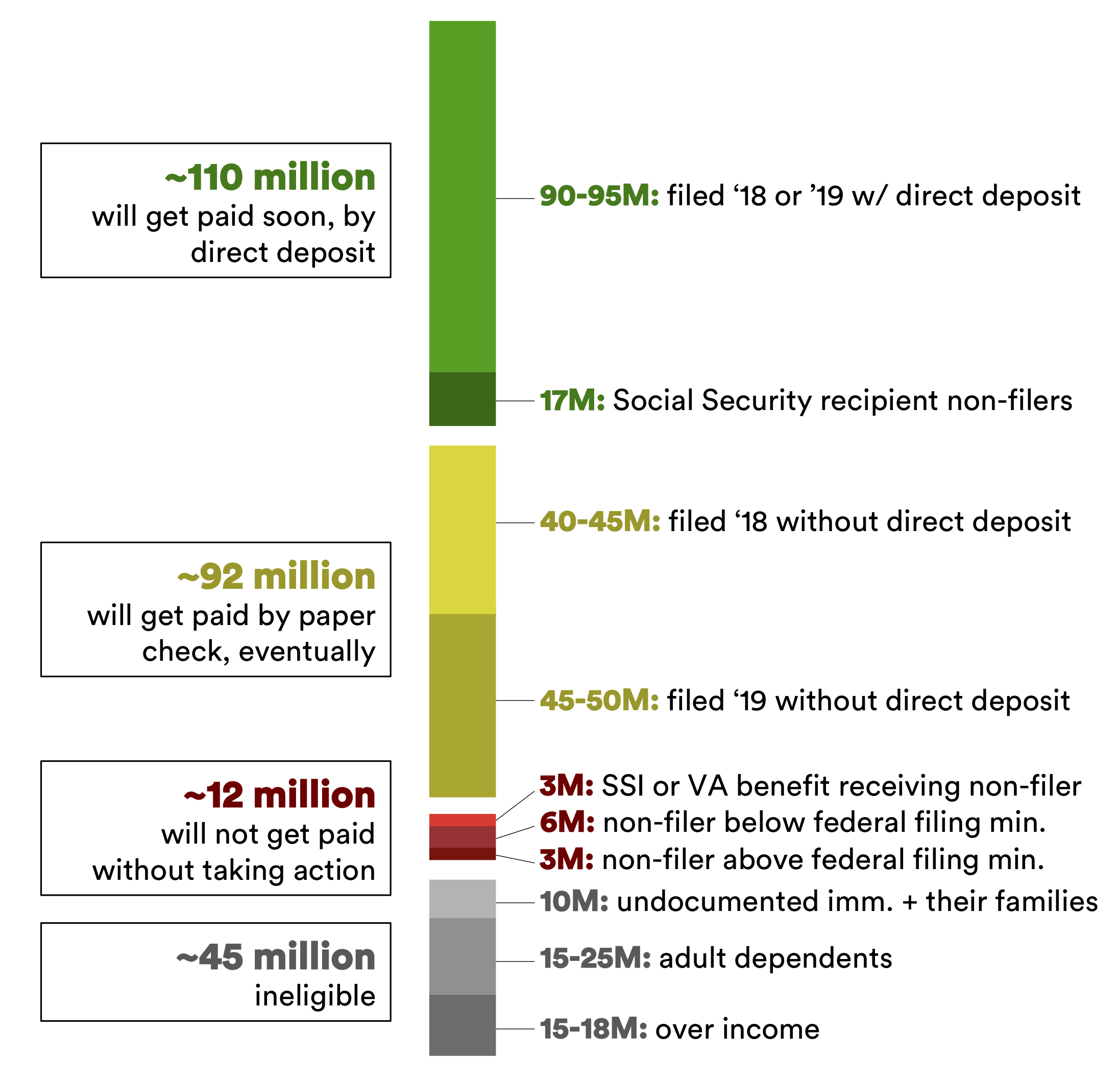

Nearly two weeks ago, Congress passed the CARES Act, which included one-time coronavirus relief payments to most American adults ($1,200 for individuals, $2,400 to joint filers, and an additional $500 per dependent)—a modest but critically necessary step.1 But Congress and the administration seem to have given little thought to how these dollars will actually reach people, especially those with severe disabilities, and low-income families who don’t earn enough to file taxes. We estimate that only half of eligible families will receive funds this month, with 10 million of the most in-need Americans unlikely to receive checks at all; to say nothing of the millions of vulnerable people denied eligibility altogether by the law.

This emergency legislation will only be impactful if the money can be spent by the people who really need it, when they need it—in time to pay overdue rent, buy groceries, and keep their families afloat. At this rate, it will not. Our rough estimates suggest:

- Nearly 10 million intended recipients earn less than the federal filing minimum and do not file taxes, and will not receive a stimulus payment unless they file a simplified return with the IRS, via an as-yet unannounced process. This population includes around 3 million individuals receiving Supplemental Security Income (SSI, for the aged, blind and disabled) or veterans disability benefits, whose existing payment information the government has on file, but has declined to use.

- Another 3-4 million low-income Americans who failed to file taxes last year must file a 2019 return to see any relief payments, and find a way to do so without access to in-person tax preparation services.

- Nearly 100 million taxpayers without direct deposit information on file will have to wait as much as several months for the IRS to finish mailing paper checks, or directly provide the IRS their payment info—again, via a process whose details remain unclear.

- And, across all these populations, over 8 million families without adequate banking services may be generally out of luck, with even predatory check cashing services closed during the national shutdown.

- Meanwhile, at the design stage of the legislation, tens of millions of Americans were denied eligibility altogether, including immigrants and their family members, and dependents over age 16.2

These estimates are based on publicly documented statistics and research, and are subject to some uncertainty. Click here to download sources and please reach out with better estimates.

The point of these stimulus dollars is to help people in crisis and keep the economy moving. The administration must do better with the delivery of these dollars. Here are five steps the government (in particular the IRS) must take immediately:

- Communicate clearly, proactively, and directly to the American people about when and how they will receive payments—especially for the most vulnerable and those that will not get money without taking action.

- Automate payments to 3 million SSI and veterans benefits recipients who do not file taxes.

- Develop and execute a clear strategy to get funds to nearly 10 million other nonfilers.

- Develop and execute a clear strategy to expedite payment for 65 million families without direct deposit.

- Develop and execute a clear strategy to get funds to over 8 million unbanked families.

1. Communicate clearly, proactively, and directly to the American people about when and how they will receive payments—especially for the most vulnerable and those that will not get money without taking action.

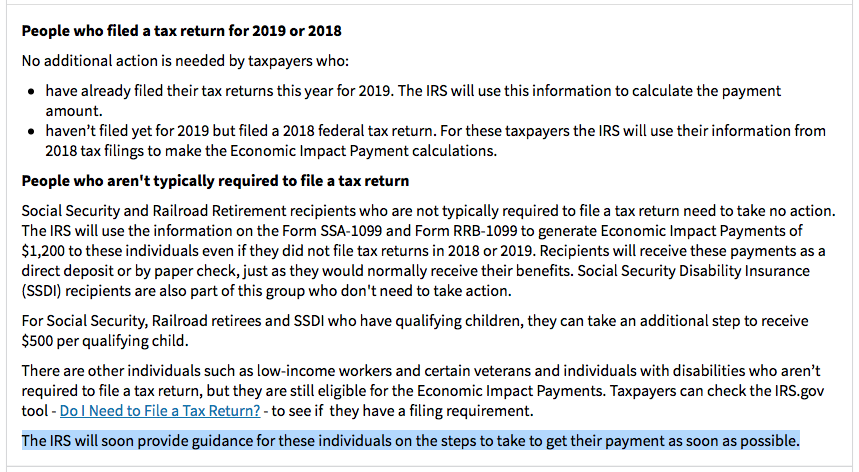

Under current policy, over 100 million Americans must take action to get their payments before the summer. But the IRS’s public communications to taxpayers have been inconsistent, unclear, and slow—especially for families and individuals whose survival depends on this cash. IRS’s latest website update on April 73 leads with: “Here is what you need to know about your Economic Impact Payment. For most taxpayers, payments are automatic, and no further action is needed.” For over ten million non-filers not receiving Social Security, who will receive no payment at all until they take action, the IRS, to put it mildly, buries the lede:

For around 90 million filers without usable direct deposit information on file, the IRS provides no process to expedite payment (despite promising such a process on an earlier draft of the website), and no information at all about how long it will take for checks to arrive, despite widespread public reporting of timelines extending to September.

On Saturday, April 4, TurboTax stepped prominently into this vacuum with a much-trumpeted coronavirus stimulus payment website, which they originally alleged to be the product of a partnership with the IRS, a claim they since quietly retracted. The Stimulus Registration tool TurboTax offers for non-filers appears to simply populate a Form 1040, and, despite TurboTax’s initial advertising, does not appear to have been publicly endorsed or even acknowledged by the IRS. Filers seeking only to update their direct deposit information, meanwhile, cannot do so on this website. TurboTax has tweeted at its customers that the IRS plans to launch a separate portal for direct deposit information, a promise that is no longer anywhere to be found on the IRS’s own website. TurboTax’s promotion has unsurprisingly driven taxpayers to the company with questions about the payments in general, but the company’s Twitter feed has in fact become a major source of misinformation about the payments.4

Even if the Stimulus Registration tool were usable and coherently advertised, the IRS, not a private company, should be providing information and guidance about how to access this government benefit. The IRS must communicate immediately and clearly about what it expects taxpayers to do to receive these payments. The government should not be offloading this communications responsibility to a private company.

2. Automate payments to 3 million SSI and veterans benefits recipients who do not file taxes.

Initially, Social Security recipients who do not file taxes were told that, like any other non-filers, they would have to file a return to receive any relief payment. After public outcry, the IRS thankfully reversed course on April 1, announcing they would use payment information on file with the Social Security Administration to make payments to retirees receiving benefits.5 This closed a critical loophole for 17 million seniors, a gap which led to over 20 percent of Social Security recipient non-filers not receiving stimulus payments in 2008.

But the administration left out other government beneficiaries from these automatic payments, including Supplemental Security Income (SSI) recipients (blind, disabled, and elderly people with very low incomes)6 and veterans receiving disability compensation.7 On April 3, 44 Senate Democrats asked the administration to step up and make automatic payments to these 3 million highly vulnerable people, a case also powerfully made by the Center on Budget and Policy Priorities. As of this writing, the IRS has not done so. Overnight, the IRS could, as it did for Social Security recipients, make funds accessible to around 3 million highly vulnerable people.

3. Develop and execute a strategy to get funds to nearly 10 million other non-filers.

Nearly 10 million eligible Americans have not filed 2018 or 2019 taxes and do not receive SSA or VA benefits, meaning they will need to file a return to see any payment. The majority of these people earned less than the federal filing minimum and were not required to file at all; and even those who were above the minimum are generally still low-income.8 Somehow, these individuals are expected to file a 2019 return without walk-in tax preparation services available, with VITA services on hold in most states, in many cases without reliable Internet connections at home, and amid fear of disciplinary action from the IRS. It is hard enough to reach these households—the majority of whom are eligible for the Earned Income Tax Credit (EITC) but fail to claim it9—in the best of times, and it will be even harder now.

For those below the minimum, IRS has promised a simplified form, with which families can register for payments without filing a return. While admirable in theory, this measure is insufficient at best; the idea that marginalized families, who struggle to file taxes in normal times, will be able to identify themselves as below the filing threshold and navigate an only slightly simpler form is highly optimistic, especially under the circumstances.

Worse, encouraging these families to file the simplified form deprives them of EITC funds they deserve (which could be even larger than their stimulus payment), in an environment in which they are sorely needed. Expending great efforts to get these families documented with simplified returns, just to leave billions in EITC subsidies on the table, is hardly a good use of resources. If there is to be a simplified form, the IRS must ensure it establishes EITC eligibility as well.

This is to say nothing of the only process publicly offered to non-filers so far: a relatively complex tool hosted on TurboTax, with insufficient advertising or documentation, which appears to have generally left users confused. This solution is barely simpler than a 1040. Indeed, it seems to simply populate a 1040. It is not clear to what degree the IRS has endorsed this application at all. But if the government moves forward with a simplified form as the basis for non-filers’ registration, it must do better than this.

There are two choices: either the IRS must identify creative measures to automatically send these checks to people, perhaps partnering with other federal or state agencies providing cash benefits; or the government must undertake aggressive measures to provide remote tax preparation services to these vulnerable families on lockdown, perhaps including additional leniency from the IRS in enforcement. Creating a slightly simplified form and just hoping for the best will leave millions without the cash they were promised.

4. Develop and execute a clear strategy to expedite payment for 65 million families without direct deposit.

We estimate 65 million families filed taxes in 2018 or 2019 but do not have reliable direct deposit information on file, including those who received refunds by check, those who paid liabilities via check or credit card, those who received refunds via temporary accounts created by tax preparers (e.g. Refund Anticipation Checks, or RACs), and those whose bank account has otherwise changed since last filing. This group includes some of the most vulnerable filers, disproportionately representing the underbanked, the homeless, and other transient populations. (Other public estimates of this population are as high as 100 million families.10) The Washington Post reports that the IRS plans to mail these checks in installments of 5 million per week, meaning it would take months for all checks to arrive. Admirably, the checks will be prioritized by income, with the poorest seeing funds first. But, for many families across the income distribution, funds were critical yesterday, not in July.

In web copy posted prominently from March 30 to April 6 (and still available online as of this writing on a news release), the IRS promised a solution: “In the coming weeks, Treasury plans to develop a web-based portal for individuals to provide their banking information to the IRS online, so that individuals can receive payments immediately as opposed to checks in the mail.” But, in the latest version of the site, this promise is gone along with any mention of what such families can or should do. Until such a tool appears, around 40-45 million of these households who have not yet filed in 2019 can file their 2019 taxes with direct deposit; but, with the filing deadline moved to July and many tax preparation services on hold during the lockdown, the prospects of that happening are slim. Meanwhile, the 45-50 million who already filed 2019 taxes without direct deposit seem to have no recourse at all.

In the 21st century, waiting months to mail a paper check is not an acceptable solution. The IRS must provide a simple and secure11 portal for direct deposit information, or pursue another creative solution to get these funds out faster, such as those powerfully recommended by Brookings. At the very least, clear and reliable communication surrounding this process is critical. Tens of millions of families in need should not be left entirely in the dark as to when help may arrive.

5. Develop and execute a strategy to get funds to over 8 million unbanked families.

Even once all payments are made, over 8 million families among both filers and non-filers will struggle to access them. Again, the crisis lies bare existing economic inequities: According to the FDIC, nearly 7 percent of in-need American households are entirely unbanked, relying on predatory financial services to cash checks even in the best of times. During the nationwide shutdown, the businesses that usually “serve” this population are closed—and even if these families are lucky enough to receive relief checks, it is entirely unclear what they will actually do with them. Federal and state governments must design strategies to reliably reach these families, perhaps in partnership with Bank On or other similar initiatives.

Relief funds are critical, and Congress, thankfully, may already be working on new stimulus legislation. But generous benefits will make no difference if they are not accessible to the people who need them. In the words of Mike Bracken, founder of the GDS (the UK’s Digital Services team): “The strategy is delivery”—and, far too often, policymakers neglect to meet citizens where they are. Instead, complex processes and bureaucracy keep benefits inaccessible to huge portions of the population. It is time for this administration to prioritize getting this support to the tens of millions of Americans who need it most. The law is a first step, but its delivery is what will make the difference for those seeking to pay their rent or put food on the table.

Updated at 1:00pm ET on April 10: After publication, we became aware that TurboTax had removed wording about IRS partnership on their Stimulus Registration tool from the press release announcing their stimulus registration tool. The old version of the press release, which includes the IRS partnership language, is available here. This article has been updated to reflect this change.

Downloads

Citations

- The appropriation totals an estimated $300 billion source

- As has been well documented by other advocates, Congress left two large populations out of the relief payments in the CARES Act. First, the law provides no payments to 15-25 million adults over age 16 claimed as a dependent on someone else’s return, which includes most college students, some adults with severe disabilities, and seniors receiving extensive care from their adult children — even for the millions of these Americans who filed their own returns. On the other hand, bafflingly, those who claim these individuals as dependents are also ineligible for the $500 subsidy for those who claim minor dependents. In the Senate, Senator Tina Smith and 14 Democratic colleagues have introduced legislation to fill this gap, source; in the House, Representative Angie Craig and 86 bipartisan colleagues have done the same, source. Second, the law provides no coverage to anyone in a household where at least one immigrant pays taxes under an ITIN rather than a SSN, punishing tax-paying immigrants as well as the citizens they live with — around ten million people, in all. Representatives Chu, Grijalva and Correa have introduced legislation to fill this gap, source

- Cached link, accessed April 8 at 10:58am ET. As of 4:55pm ET on April 8, no visible edits had been made to this page.

- TurboTax’s role in this story deserves independent attention. TurboTax has loudly advertised its collaboration with IRS, and driving taxpayers to a website that prominently features its own tax preparation services — services that IRS has rightly cited for predatory behavior, source. Even taxpayers who use the site only for TurboTax’s Stimulus Registration tool must create TurboTax accounts and provide their most sensitive data to a private company, which turns around and uses that data to, again, advertise its own tax preparation services. IRS is publicly warning taxpayers of schemes to exploit the crisis to capture their personal information — but, in effect, this is exactly what the TurboTax partnership is doing, source

- Note that Social Security payments are nearly universally made by direct deposit, so essentially no recipients are being funneled into the long queue for checks by this decision, source

- While the IRS’s latest guidance is confusingly worded, the bottom line remains that only SSA-1099 and RRB-1099 income was noted in the updated filing, neither of which reports SSI income. The Congressional Research Service confirms the point that SSI recipients must file a return, source

- There could be a logistical rationale for this move: Social Security OASDI benefits are reported to IRS on SSA-1099 Forms, whereas SSI and veterans benefits are not. But, according to Senate Democrats, the process that the IRS is actually following for SS recipients is not based on the 1099s, but rather will sync IRS data with SSA data. There is no clear reason this process could not be easily applied to SSI and veterans benefits.

- Cilke (2011) reports that non-filing wage earners have a mean of $13,837 in earned income. Those above the single filing threshold — a proxy for those actually above the filing threshold, in the absence of relationship status data — have a mean of $31,435 in earned income. But, since income is log-normally distributed, the median income will be much lower than this, putting most of these earners in the bottom third of the income distribution, source

- In this way, as so many others, the coronavirus crisis lays bare glaring societal inequities: every year, millions of families eligible for thousands of dollars in EITC refunds do not claim their money. If EITC outreach were what it should be, these families would be filers already.

- The 100 million estimate is reported in The Washington Post, citing internal Treasury documents, source; and Fortune, citing a Ways and Means Committee document, source. This figure does not seem consistent with known data about the prevalence of direct deposit, and the total number of eligible returns.

- The security of such an application is of course a significant concern, and should be at the center of any development plans. The US government has existing expertise through the United States Digital Service (USDS) and 18F.

More About the Authors

Gabriel Zucker

Fellow, Public Interest Technology

Tara Dawson McGuinness

Founder & Executive Director, New Practice Lab