Table of Contents

- Checklist

- Introduction

- Household Economy

- Community Resilience

- A Pandemic of Racism

- Election Integrity

- Healthcare Surge Capacity

- Supply Chain Management

- Universal Access to Digital Services

- Banking and Payment Systems

- Economic Resilience

- Future of Work

- Epidemiological Readiness

- Porous Lines of Defense

- Institutions

- Policy Considerations

Economic Resilience

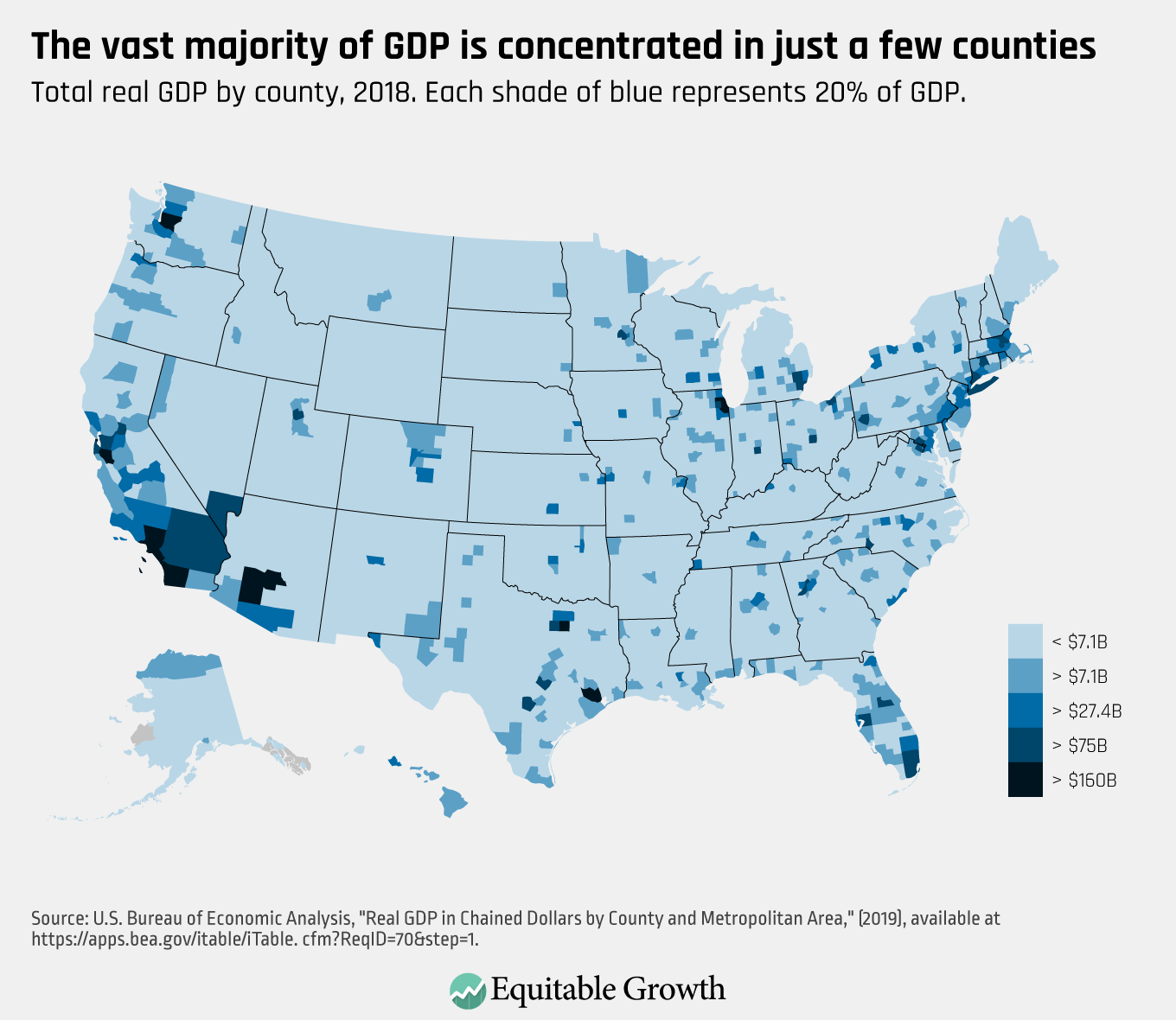

Resilience, unlike risk, benefits from compound effects. Simply put, investments in resilience, household savings and closing what insurers refer to as the protection gap, accrue. There are some fundamental challenges, however, to improving economic resilience across the United States. Many of these have as much to do with market structure as they do with systemic levels of income inequality, as well as with the relatively low dispersion across the country in terms of economic productivity.

In disaggregating the proportion of economic value and activity carried out in the United States, one-third of GDP is derived from 31 (.01 percent) U.S. counties. Therefore, as much as U.S. citizens may have won the global birthright game, inside the United States there is also a ZIP code lottery that will say a lot about your long-term prospects and the public resources (in the form of taxes and other government or community funds) that will be available to you and can be mobilized in a crisis. Some wealthy communities, such as Bolinas, California, were the first in the country to test all of their residents for COVID-19, for example, pushing the risk and spread of the virus downmarket as it were.

If long term investments in resilience compound, for example raising levees by three feet provides three additional feet of flood resilience, what is the formula to improve economic resilience in a country with 20 percent of the population relying on credit to make ends meet before the pandemic? In addition to more protections afforded through employment-related programs, facilitating access to emergency funds through home equity, unemployment insurance and credit markets can serve as important first lines of household defense, rather than relying on government largesse or public support programs singularly.

Unemployment insurance programs are fraught with political emotion in the United States, with some arguing that they discourage work, while others arguing that they are a necessary part of social safety nets. The fact remains, the broad preexistence of unemployment insurance programs can be a net benefit and a faster way of distributing direct economic relief, while accruing paid-in capital to these programs. If fears remain about how rich the benefits of these programs should be, managing claim triggers on a stepladder basis—depending on market conditions or whether a disaster is declared or not—can contribute to balancing incentives versus economic resilience. Either way, with such a disproportionately large share of the economic costs of risk being shouldered by taxpayers, creating, pre-funding, and maintaining actuarially sound financial shields can make a difference.

In a force majeure case such as the pandemic, there is often little else to turn to but these types of insurance-like programs. Therefore, we would stand to gain as a country by broadening their availability and strategically prefunding these coffers for future events, whether for rainy days or blue sky disasters. Crucially, like all well-funded insurance programs, unemployment or hardship funding can leverage the law of large numbers and produce actuarially sound prefunding for future generations of disaster survivors, saving households as much as the economy from the deleterious effects of low economic resilience and mass layoffs.

Another area of opportunity to enhance economic resilience is to look at broader standardization on moratoria for credit and debt instruments, such as mortgage and rental agreements. As is often the case in disasters, the specter of high default rates on consumer credit, loans, and other financed debt obligations shows how quickly a crisis can spill over into other areas of the economy. Yet access to credit even in normal times is often a lifeline for millions of Americans. In a disaster, credit is a major difference-maker in shoring up economic resilience, but great care must be taken to ensure a temporary credit bridge does not bleed into a debt bubble, bankruptcies, and a tidal wave of defaults, which appears to be looming over the U.S. economy.

Even before the pandemic struck, the United States was laboring under a perilously heavy debt burden, with credit cards fueling $930 billion in debt, while student loans and other forms of personally guaranteed credit spiraled to $1.5 trillion in total. Clearly, post-pandemic debt forgiveness and resetting credit records at population scale may very well be an important tradeoff in restoring consumer confidence and lifting the penalty of poverty that has barred the gates of opportunity for millions of people. Indeed, with over 25 percent of the workforce now dependent on government unemployment backstops, whether through unemployment insurance programs or payroll-focused bridge loans such as PPP, the public interest on livable wages, bridging the gender pay gap, as well as shoring up economic benefits in a harmonized manner should be prioritized.

Finally, with so many of the economic consequences of risks skipping the private sector balance sheet of insurers and risk-sharing funds only to land on the shoulders of taxpayers, more has to be done to crowd-in risk-sharing capital. Indeed, it can be seen as a market failure despite all the ingenuity and financial engineering available to shore up complex risks, from uncorrelated catastrophe bonds—which remain pitiably shallow at $10.3 billion in total—to the lack of uptake of flood, earthquake, and other insurance programs. The pandemic underscores the need for broadening the base of insurance: For each 1 percent increase in private sector risk sharing, there is a 22 percent decrease in the taxpayer burden of economic losses. It is foolish to head into a new decade so woefully underinsured against the specter of large, complex risks so certain.