Table of Contents

- Checklist

- Introduction

- Household Economy

- Community Resilience

- A Pandemic of Racism

- Election Integrity

- Healthcare Surge Capacity

- Supply Chain Management

- Universal Access to Digital Services

- Banking and Payment Systems

- Economic Resilience

- Future of Work

- Epidemiological Readiness

- Porous Lines of Defense

- Institutions

- Policy Considerations

Community Resilience

In the chain of community resilience, we are as strong as the weakest link. Each link is a person or household in a community and far too many people in the United States are living near the financial brink or at subsistence levels. More than 53 percent of U.S. households do not have an emergency savings account. This is exacerbated in times of crisis, irrespective of the cause. Whether a natural disaster, flood, hurricane, tornado, fire, or pandemic causes the turmoil, households are not adequately prepared—neither at the net savings level or with regard to insurance or other forms of third-party protection.

This is where community resilience begins to break down. The financial system is cruelest and costliest to the people who can least afford it. In addition to pernicious rates of unbanked and underbanked households, numbering more than 32 million in the United States, there are also insidious rates of underinsurance against mathematically certain risks. This is especially true in high-hazard areas, where low-income families live in low-lying areas in low-quality homes, a triple threat. Exacerbating the low levels of resilience, these very communities are among the least insured, which is saying a lot for a nation whose safety net and disaster recovery capabilities are wantonly ineffective in the face of a worsening threat landscape.

Herein, the insurance or underinsurance gap is a wide chasm of financial vulnerability, where the cost of risk crosses all lines of defense landing squarely on the taxpayer. Bridging this protection gap would have immediate benefits in not only protecting households and community coffers, but in shielding the public balance sheet, which is all too often first in line. This is partly a market failure when it comes to penetration, affordability, and value derived from private insurance and partly a failure of public insurance programs that labor under upside down actuarial models as much as they promote moral hazards—risk taking behavior without enduring the consequences.

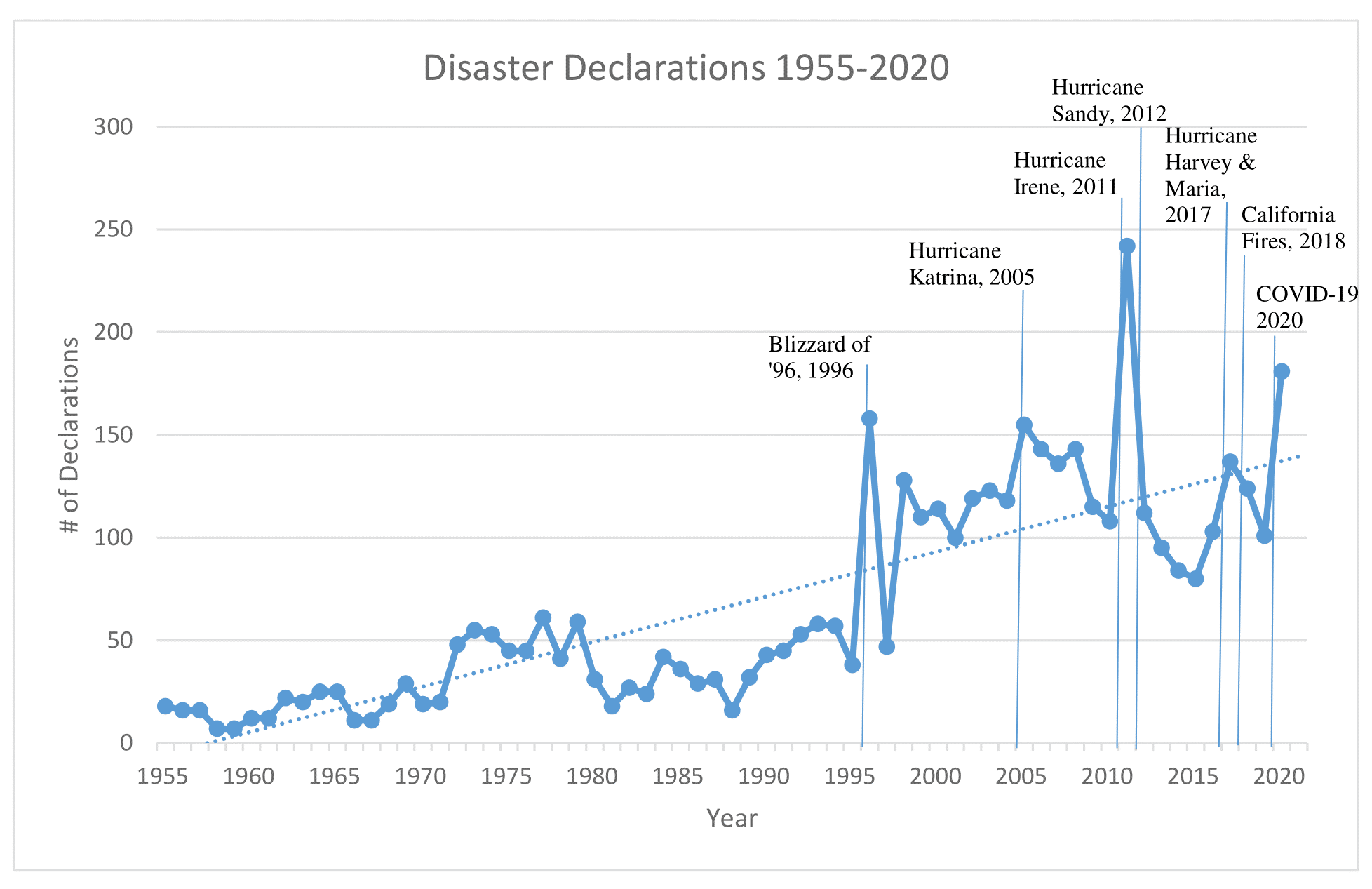

Bridging this gap is a key part of improving community resilience and the ability at the household level to spring back from catastrophic events, whether these are caused by natural, man-made or emerging threats. The run up of mega, multi-billion dollar disasters in the last 20 years suggests the national trend line of declared disasters augurs a perilous new world. It should also augur a new definition of community resilience. In the past 20 years, the rate of U.S. disaster declarations (assuming no politicization of the process), has gone up exponentially, averaging 124 per year. In the preceding 50 years up to the year 2000, the national annual average was just 24. In the pandemic, the nation’s map was flashing red, as all 50 states and territories declared “blue sky” disasters. In this environment, having the private insurance balance sheet in retreat, amidst perilously low levels of insurance uptake while the waters are rising, the winds and fires are raging, exposes fissures in community resilience.1

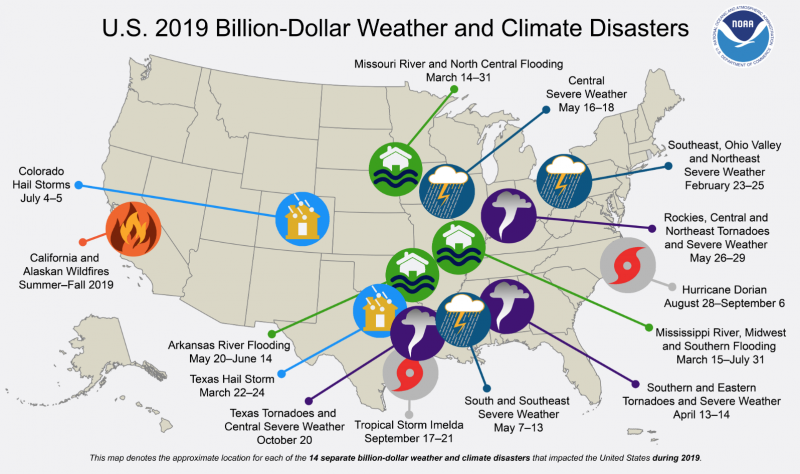

Tragically, entire communities are being wiped off the map or etched with the effects of climate change, economic degradation, and reduced productivity and competitiveness—all amplified by the pandemic—triggering a wave of human displacement. The town of Paradise, California, was obliterated in the 2018 Camp Fire event. The entirety of Puerto Rico’s public infrastructure—with the bankrupt public utility, PREPA, being the chief culprit—was devastated by Hurricane Maria in 2017, setting the U.S. territory back decades in terms of economic recovery. Puerto Rico’s disaster-displaced residents went to all 50 states, in what the international humanitarian community would characterize as internally displaced people (IDPs). The COVID-19 pandemic has only worsened these underlying economic vulnerabilities, where the hardest hit communities and people are those who were already economically marginalized.

With trillions of dollars of economic intervention and foregone economic productivity already on the table as a down payment on the future, the post-pandemic United States must address underlying community challenges in an agnostic manner to the threat environment. All-hazards management of threats that can impact communities would strengthen all of the fibers, threads, and weaving patterns that make up the community safety net. This net was already in tatters before the pandemic and it is now in desperate need of mending.

Communities facing annualized threats, such as flooding, hurricanes, tornadoes, fires, and earthquakes, are all woefully underinsured or uninsured against these risks. When Hurricane Harvey turned the city of Houston into a lake creating a citizen flotilla to rescue neighbors, as many as 80 percent of households in the path of the hurricane lacked flood insurance. When Hurricane Maria sent Puerto Rico back to the proverbial dark ages, triggering the second longest blackout in modern history (surpassed by Typhoon Haiyan in the Philippines in 2013), 79 percent of public assistance claims were denied or unanswered because of inadequate documentation. Only 13 percent of California households have adequate earthquake insurance, notwithstanding the ever-present risk that the big one might strike at any time. Indeed, as California’s fires have underscored in the last few years, the lines between private sector and public sector risk-sharing have blurred, with PG&E’s bankruptcy ostensibly being the world’s first major corporate failure triggered by climate change.

If our society is ill-equipped to contend with the economic, social and environmental costs of annual events exacerbated by climate change, we would of course seize up in the face of a 100-year pandemic. Resilience, like savings or investments that leverage the financial miracle of compound interest, also accrues. Improving the household economy and financial shock absorption at the community level across the country will improve our ability to withstand all hazards.