CARES Act Stimulus Payments Have Reached 160 Million Households — But Could Reach Millions More

Authors’ Note: This issue is moving quickly, and we expect components of this report may become out of date as new information becomes available. The information in this report is current to the best of our knowledge as of July 1, 2020.

In the Coronavirus Aid, Relief, and Economic Security (CARES) act, Congress authorized $1,200 economic impact payments (EIPs, a.k.a. stimulus checks) to nearly every adult in the country, and tasked the Internal Revenue Services (IRS) with getting these critical funds in the hands of families. Over the last several months, faced with the implementation of one of the largest and most time-sensitive relief programs in American history, the IRS has made tremendous efforts to issue these payments quickly and seamlessly.1 The program has demonstrated what it looks like when the IRS takes seriously its responsibility to ensure that funds reach people in need—and there are valuable lessons from this experience for the administration of other tax code programs that benefit low-income families.

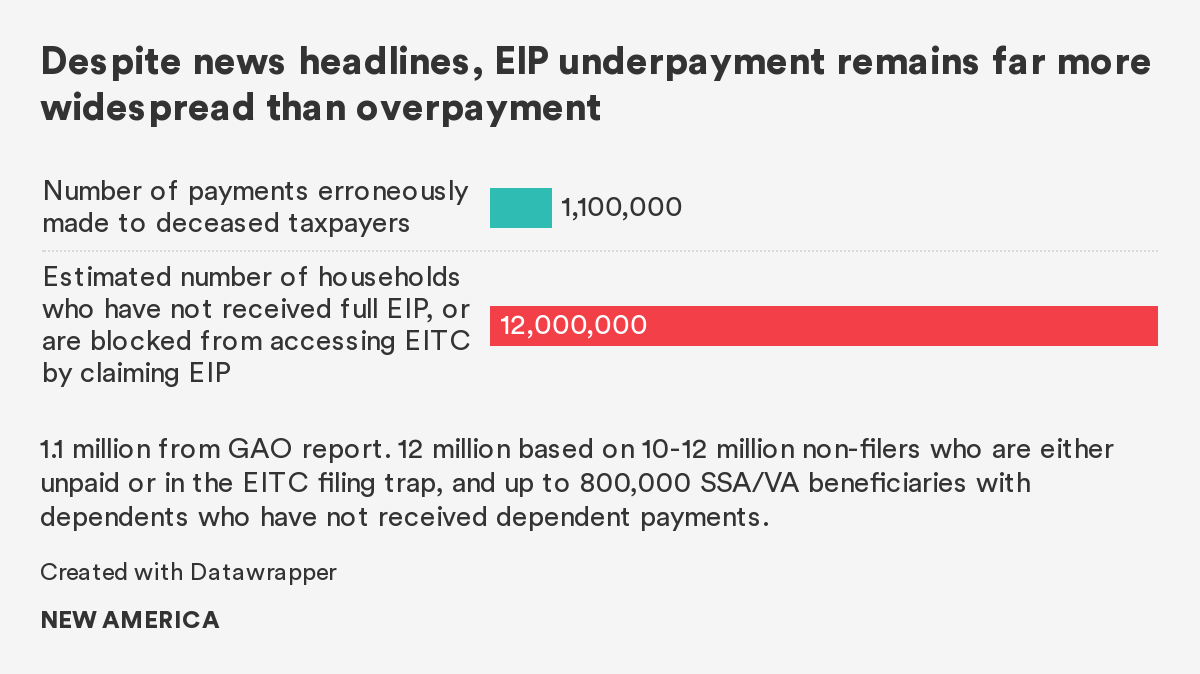

On the other hand, despite the IRS’s admirable work, the EIP rollout has been far from perfect, and requires several technical fixes. An estimated 5-10 million of the most vulnerable American households have not received their full payments yet—and as many as 6 million more have been blocked from filing taxes (and claiming critical tax credits) due to unexpected behavior of the IRS's new EIP non-filer tool. Even by conservative estimates, these issues remain far more widespread than much-discussed news of alleged erroneous overpayments to deceased taxpayers.

While the CARES Act was a promising start, additional stimulus dollars are needed to escape this recession, and many policy experts and members of Congress are rightly focused on ensuring those payments come soon, and equitably. Indeed, Congress must ensure payments continue until the economy has recovered. But Congress must also ensure the smooth delivery of these checks. Dollars can only keep families in their homes and keep food on the table if they actually reach people. It is clear that there is work to do—especially to reach low-income Americans, who are most at risk.

This report lays out the following:

- a set of technical fixes around delivery of the first stimulus payments (and similar payments in any future congressional aid),

- a set of technical fixes to ensure EIP claimants can also access other critical tax credits, and

- several medium-term reforms to increase earned income tax credit (EITC) access for low-income families, informed by the possibilities the crisis and rapid response have raised.2

Taken together, these fixes would go a long way to ensure that over 10 million economically vulnerable American households get the assistance they are already due, and that they continue to get relief going forward.

Most of these fixes can be implemented without legislation. If the IRS does not address the gaps in their implementation of the CARES Act, then Congress should address these technical fixes in the next stimulus legislation.

1) Ensuring Stimulus Payments Reach All Eligible Households, Especially Low-income Americans, of Whom 5-10 Million Remain Unpaid

The best available data suggests that, despite the IRS’s concerted efforts, 5-10 million households of vulnerable Americans have not received their full payment. An early June survey by New America and the Center for Taxpayer Rights found that community organizations and low-income taxpayer clinics around the country have generally seen dozens of cases of EIPs unpaid or underpaid, with access issues especially common among households that do not usually file taxes, and among economically vulnerable households. A survey of SNAP beneficiaries around the same time by the civic tech company Propel found that nearly a third had not yet received their payment. The precise numbers remain unclear; the IRS releases only limited statistics on payments; the Census Household Pulse Survey has not released any data on EIP receipt as of June 29;3 and in testimony before the Senate Finance Committee on June 30, IRS Commissioner Chuck Rettig repeatedly declined to give an estimate of how many payments remain outstanding. But, months into this crisis, it is past time to guarantee that all eligible Americans get the payments they deserve. In the absence of clear data on payment coverage, Congress should ask the IRS to facilitate payments to the economically vulnerable, and require the IRS to report on its progress.

1A. After July 15, automatically pay EIPs to likely eligible non-filers who have not yet registered for the payment, using W-2 and 1099 data that the IRS already has on file.

Despite the IRS’s extensive outreach encouraging non-filers to use the new “non-filer portal”4 to register for the EIP, Volunteer Income Tax Assistance (VITA) centers and social service agencies continue to report that large numbers of marginalized and vulnerable non-filers have not been able to register. The providers cite many challenges: widespread difficulty with the tool’s authentication process,5 insufficient computer access (the tool is not mobile responsive), and language barriers (the tool is available only in English and Spanish, and the Spanish version is widely considered more difficult to use6). While continued outreach is valuable, the myriad barriers to using the tool mean that getting all non-filers to register will be an uphill battle at best. Given that 6.1 million non-filers have used the portal as of June, there are likely 4-6 million more still unserved.7

There is a better way: the IRS can simply automate outstanding EIPs using data already available from information returns. The IRS would identify Forms W-2 and 1099 associated with Social Security Numbers that neither received EIPs nor filed taxes, and mail EIPs via paper check to the address reported on the forms.8 As information returns are filed for 99.5 percent of the U.S. resident population annually, this step would reach the overwhelming majority of remaining non-filers. Such automation is the natural extension of automating payments to SSA and VA beneficiaries, which the IRS agreed to do after Senators Sherrod Brown (D-Ohio), Cory Booker (D-N.J.), Michael Bennet (D-Colo.), and Maggie Hassan (D-N.H.) led Senate Democrats in requesting the change.9

If the IRS implemented a few simple filters, the probability of payments going to ineligible households would be low.

- Individuals who earn too much to qualify: Less than 10 percent of Americans actually earn too much to be eligible in the first place. Moreover, non-filing households are disproportionately low-income, so the fraction of non-filers who are also wealthy enough to be EIP-ineligible is likely even smaller.10 If the IRS further screens out individuals with significant reported investment income, the rate of payments to over-income taxpayers would be negligible.

- Individuals who could be claimed as a dependent on another person’s return and therefore do not qualify: The IRS can remove all workers under 24 who share an address with a filing adult over 36.

- Individuals whose spouses are undocumented immigrants: The IRS already automatically paid SSA and VA beneficiaries without confirming their spouses’ immigration status. While there is a small risk of some ineligible families receiving payments, it would not be new to this process.

The benefits from millions of vulnerable and eligible people getting payments they need and deserve is surely worth the possible risk of a small number of incorrect payments.

1B. Allow SSA and VA beneficiaries to claim dependents and receive additional supplementary EIP throughout 2020.11

The IRS made EIPs automatically to beneficiaries of federal cash programs (Social Security, SSI, VA benefits) who have not filed taxes in the last two years. For many beneficiaries, this was a key improvement over the 2008 approach, which required them to file “ESP-only” returns reporting $1 of income. However, lacking tax returns, the IRS had no way of knowing whether these beneficiaries had child dependents, thus deserving an additional $500 payment. The IRS asked beneficiaries to use the “non-filer portal” to declare their dependents, but provided very restrictive timelines on doing so. For Social Security beneficiaries, the IRS issued an alert on April 20 that the deadline to register dependents would be April 22.12 For SSI and VA beneficiaries (whose automatic receipt of EIPs was announced on April 15 and 17, respectively), the May 5 deadline appears to have been initially announced on April 25, but did not get widespread attention until several days later. These were very short windows in which to expect that disabled and elderly populations would be able to access the internet and fill out government forms, especially during a time in which all traditional means of tax assistance—such as VITA sites and even IRS hotlines—were unavailable. Critically, in both cases, the IRS announced that anyone missing these deadlines would have to wait until 2021 to receive the additional payment.

Setting some sort of deadline to start making initial payments to these populations was reasonable: better to start making $1,200 payments to millions of people in need than make everyone wait while those with dependents register for additional funds. But, there is no clear reason why the additional payments cannot be made later. The IRS should allow these beneficiaries to continue using the non-filer portal to register their dependents, and simply pay additional dependent payments on a rolling basis.13 Senators Ben Cardin (D-Md.) and Ron Wyden (D-Ore.) have already led a group of 13 Senate Democrats requesting this measure, and the step also earned Republican support from Senator Chuck Grassley (R-Iowa) in the June 30 Senate Finance Committee hearing. In a country where many households cannot weather a $400 unexpected expense, an additional $500 payment would be critical. No new process is required here; the IRS simply should continue allowing beneficiaries to use the tool already created for this exact purpose.

This move is especially critical if Congress intends to authorize another round of EIPs. If Congress passes another round of payments—again with $500 per dependent—and the IRS, as expected, simply uses existing payment information on file, then those who missed the brief windows in April and May will have their loss compounded.

(Note that this is distinct from a related issue, in which the IRS mistakenly did not issue $500 payments to 360,000 beneficiaries who did claim their dependents on time.14 The IRS has promised to address this critical issue by July.)

In the absence of clearer data, it is impossible to know the size of this population, but we estimate this issue affects at least 250,000 households, and possibly as many as 450,00015—most of them very much in need.

1C. Automate payments to any new SSA/VA beneficiaries who joined the benefit rolls since April.

It appears that the IRS delivered EIPs to SSA and VA beneficiaries through one-time syncs of SSA and VA data with IRS records in April or May. But millions of beneficiaries join these programs every year, including 5.6 million who begin receiving Social Security alone. While these numbers may be somewhat depressed during the pandemic, there are likely at least a million new beneficiaries of these programs since the EIP rollout, some of whom will not have filed taxes in the last two years. Repeating the data synchronization process from earlier in the spring would be a relatively easy way to make several hundred thousand more payments.

1D. Expedite or waive pending reviews or examinations on tax returns for households who have yet to receive EIPs—especially returns filed via the non-filer portal.

As of June, there appear to be millions of tax filers and portal users who have not yet received payments. Anecdotal evidence and knowledge of IRS procedures both suggest that much of the delay is due to pending reviews or examinations.16 There are likely several million households who did not file for TY2018 and filed for TY2019 just to claim the EIP; and several million more who effectively filed through the non-filer portal. These are millions of tax returns that must be processed before EIPs can go out, which are routed through the IRS’s usual business rules, and sent to examination departments if they appear suspicious for any reason—caught by identity theft filters, dependent database filters, or questionable refund filters. In normal times, the examination departments receive millions more returns than they actually have capacity to review; departments must manually release the returns they decide not to investigate in further detail, and a backlog routinely builds up in February and March before sufficient returns can be released. Now, when even more returns are being flagged for review and possible examination, and when examination departments’ capacity has been decimated by the crisis, long queues of returns are likely languishing unreleased and thus unpaid.

In this moment of crisis, the IRS must find a way to expedite these reviews and examinations; or, if that is not possible, simply waive them. This step should be especially straightforward for those who registered via the non-filer portal, since their lean returns should not need to be meaningfully reviewed. Waiving arduous oversight to speed emergency assistance has indeed been a hallmark of government programs that have moved assistance quickly enough during the crisis, such as in Berlin.17 The risk of millions of households going without the assistance they critically need in the midst of an unprecedented crisis outweighs the risk of a few overpayments.

1E. Promote and expand the economic impact payment call center to field questions about pending or incorrect payments.

Qualitative data from New America and the Center for Taxpayer Rights’s survey on EIP delivery as well as hundreds of posts on Reddit make clear that significant numbers of people took the requisite steps to receive the EIP and yet never actually received it, or received the wrong amount. While some of these issues will be resolved by waiving examinations, as described above, others are not so straightforward. Households in this situation deserve an explanation of what happened, and clear instruction on what to do next to secure their payments.

In May, the IRS finally launched a limited EIP phone line, a critical and overdue measure. Moving forward, the IRS must expand and promote this call center, encouraging phone calls to resolve issues rather than discouraging them. (The IRS’s EIP page continues to instruct taxpayers: “DO NOT call the IRS.”) The call center must be empowered to determine the current status of a payment and address common issues.

Congress may need to appropriate additional funds to ensure the call center’s efficient operation, including ensuring that call center workers can perform their duties remotely, given the uncertainty introduced by the pandemic.18

As a related recommendation: Congress should fully fund VITA sites for TY2019, especially as sites gain the ability to reopen in a limited fashion during the summer and fall. To date, Congress has appropriated only $18 million of $30 million authorized for the program. The additional funding would go a long way to ensure that low-income Americans can get the assistance they need.19

1F. Release detailed data on payments and portal users to date, to help identify gaps and target remaining outreach activities in 2020.

To the degree that Item 1A is incomplete or delayed, the IRS should also release detailed payment data that allows analysts and advocates to prioritize reforms, and identify critical regions and demographics for further outreach. Expanding on the data previously requested by Representative Richard Neal (D-Mass.) and the Ways and Means Committee, the IRS should provide detailed information on the number of:

- users of the non-filer portal,

- portal users who started but did not finish registering,

- portal users who could not successfully authenticate,

- payments issued to portal users,

- portal users whose payments have not yet been made,

- payments issued to SSA/VA beneficiaries,

- SSA/VA beneficiaries whose payments have not yet been made,

- SSA/VA beneficiaries who claimed dependents via the portal,

- households who filed in 2018 or 2019 who have not yet been paid,

- households who used the Get My Payment tool to submit direct deposit information, and

- people with TY2018 or TY2019 Forms W-2 or 1099 who have not yet filed or registered for payment.

This information would help advocates have a better understanding of where the remaining problems are.

The IRS should also release this data at the zip code or city level. There is precedent for doing so; during the administration of the 2008 economic stimulus payments, when SSA and VA beneficiaries were not automatically issued payments and had to file simplified tax returns, the IRS released data on the geographical distribution of beneficiaries who had not yet filed. Advocates used this data to create maps of unreached beneficiaries by zip code, which were critical in expanding outreach. Through careful comparison to Census data, advocates could use the same disaggregated information this year to identify hotspots of unclaimed payments, and target efforts over the coming months.

2) Fixing the “Filing Trap” That Has Prevented 6 Million Portal Users from Filing 2019 Taxes

To facilitate access to the EIP for households who do not traditionally file taxes, the IRS launched the “Non-Filer: Enter Payment Info Here” tool, or the “non-filer portal.” Unbeknownst to its users, the portal files lean tax returns on users’ behalf.20 But, due to identity theft concerns, the IRS does not allow a single taxpayer to e-file two returns in the same year. So when portal users attempt to e-file a 2019 tax return, they are blocked from doing so.21

In normal years, such households could simply file a superseding return on paper before the tax deadline, now July 15. But during the crisis, this option has not been available. Through June 17, the IRS reported it could not process paper at all, and since June 22, the IRS says . Moreover, during the crisis, gaining access to a printer and postage has been a high barrier for many families.22 There has been no viable pathway for portal users to file taxes.

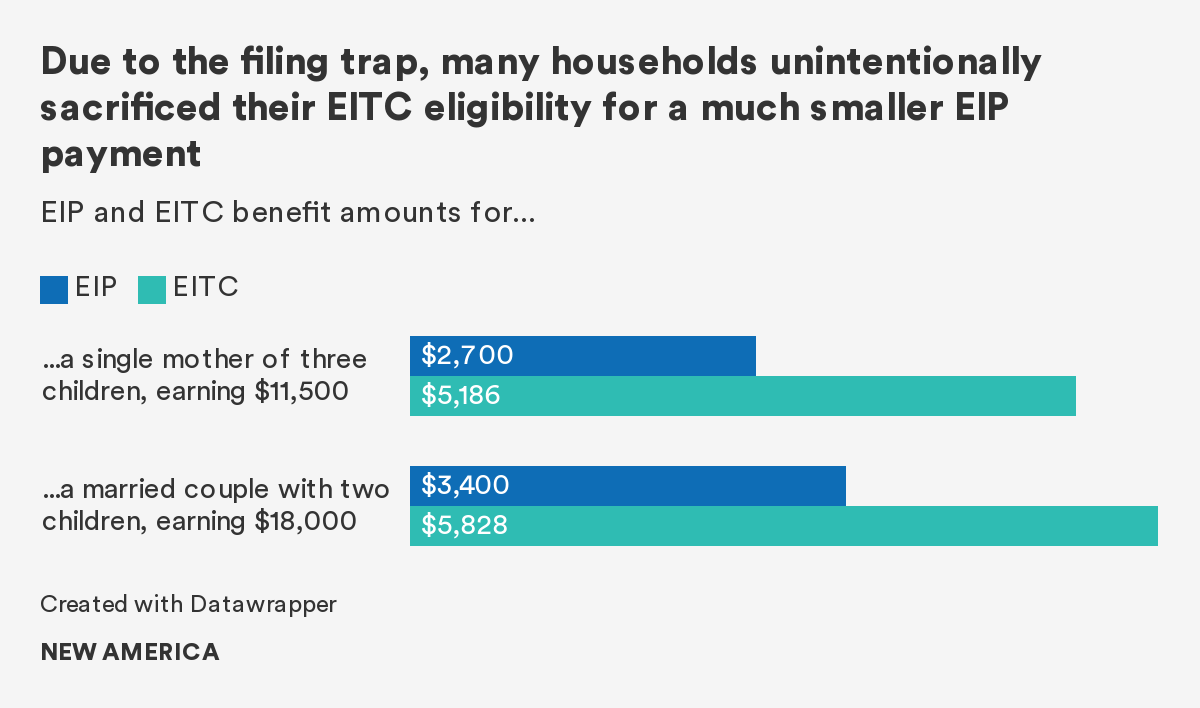

The non-filer tool was only intended for households whose income is below the tax filing threshold, who are not required to file taxes.23 But most of these households are still eligible for the earned income tax credit (EITC), and perhaps the child tax credit (CTC). So, in seeking to access the EIP, millions of households effectively sacrificed their—often much larger—EITC payment: For example, a single mother of three earning $11,500 would have received $2,700 in EIP, but would have been eligible for $5,186 in EITC. Furthermore, the IRS has reported that some households above the federal filing minimum, who technically were not eligible for the non-filer portal, inadvertently used it regardless, in their desperation to receive the EIP. (The portal’s instructions make it easy to miss this restriction.) These households are required to file tax returns, and surely intend to, but likewise have no way of doing so.

We call this issue the “filing trap,” and it currently impacts 6.1 million households, most of them eligible for EITC or other tax credits.24

On June 25, the IRS finally acknowledged the issue in a private notice to tax preparers, but provided an entirely unworkable solution: The IRS wrote that portal users seeking to file would have to file superseding paper returns by July 15, despite the fact that, as of eight days earlier, the IRS was insisting that no one file a paper return, under any circumstances.25 How portal users were expected to learn of this requirement and submit a superseding paper return within three weeks, despite likely being unaware they ever filed a tax return in the first place, the IRS did not say. Moreover, these paper returns will likely languish in the IRS’s severe paper backlog, and will not be issued refunds for months. The IRS also promised in the same notice a capability to submit an amended tax return electronically, through online submission of Form 1040-X, but wrote that the capability would not be available until approximately August 17. Moreover, unlike superseding returns, the IRS has no legal requirement to process amended returns expeditiously, and has made no commitment to process Forms 1040-X in calendar year 2020. So even if filing trap households are willing to miss the July 15 deadline and use the e-1040-X, there is currently no guarantee they will receive critical funds any time soon.

Nothing about this process is viable for households in the filing trap, and most will be effectively blocked from accessing a critical anti-poverty program when they need it most. In the words of Senator Michael Bennet (D-Colo.) from the June 30 Senate Finance Committee hearing: “Until a suitable online system is put in place to deal with this filing trap created by the IRS’s system, millions will go without the money they desperately need.” Moreover, the IRS has long had a stated goal to increase EITC participation beyond its current level of around 80 percent—and it is squandering an unprecedented opportunity to do so. Through the EIP campaign, perhaps millions of new households have been brought into the filing process for the first time, and are easier to reach with EITC than ever before. The IRS should proactively take advantage of this opportunity, not enact new barriers to access.

The IRS should create a straightforward solution for these households to file taxes, but also take two key proactive steps to meet them where they are with the EITC.

2A. Create a viable and straightforward method for users of the non-filer portal to file 2019 taxes.

First, the IRS must extend the filing deadline for these households, who through no fault of their own are unable to meet the current deadline. By the time clear guidance reaches portal users, July 15—the deadline to file superseding returns—will likely have passed, and households would have to settle for filing amended returns. But, unlike superseding returns, the IRS is not required to quickly review and process amended returns, and it is critical these low-income households not be moved to the back of a long queue when the IRS already faces diminished capacity.

Second, the IRS needs a simple electronic process for households in this trap to get out of it, for the millions of households without access to a printer and postage.26 Given the IRS’s announcements to date, it seems likely the e-1040-X is intended to be just this fix. If so, the IRS must expedite its launch, and guarantee that returns submitted this way will be processed in calendar year 2020. If necessary, Congress should appropriate additional funds to ensure the IRS can stand up a specialized unit for this expedited processing.

Third, and perhaps most important, the IRS must communicate clearly and proactively about these processes. Most households in the filing trap are likely unaware they filed taxes at all; the idea that they will have to “modify” a return they never intentionally filed is extremely unintuitive. It is incumbent on the IRS to explain in plain language what happened, and what households can do to address the situation.

These short- and medium- term fixes may be difficult for the IRS to implement, but households in the filing trap have a legal right to file their taxes. Having created the trap, the IRS must also find a solution for it, and Congress should ensure the IRS has capacity to get the job done.

2B. Automate payment of the childless EITC for portal users.

Under current policy, when the IRS receives a tax return from a childless household that appears eligible for but has not claimed the EITC, it sends a letter to the filer (CP-27) flagging the possible oversight.27 (This letter is only sent to around 275,000 filers, for whom the IRS has a relatively high degree of certainty that the filer is eligible, although the participation gap among childless filers is slightly larger.) Recipients can sign the form and return it to claim the credit, and 57 percent of them do, according to a recent Treasury IG (TIGTA) report. But this scheme is imperfect in the best of times, leaving out hundreds of thousands of households who do not receive or do not return the CP-27 notice, not to mention taking extra weeks or months to send the refund.28 In the current situation, with portal users confused about their tax filing status, with the IRS still short on capacity to process paper forms, and with the underlying issue fundamentally the IRS’s own fault, it is simply not enough.29

There is a better way: The IRS can use its Summary Assessment Authority (SAA) to simply automatically pay the childless EITC to eligible portal users, as a math adjustment, rather than nudging the taxpayer to claim it and hoping she takes action. The IRS can use the W-2 and 1099 data it already has on file to calculate earned income, and to weed out any taxpayers with excess investment income. (The IRS can make these payments to all households, even those with children, and simply pay the difference if the household later claims the full with-child EITC.) This relatively simple step would provide an average of $280 to about 300,000 to 400,000 taxpayers.30 This is not a new proposal: the National Taxpayer Advocate has repeatedly argued for it;31 TIGTA advocated it; and Senators Sherrod Brown (D-Ohio) and Catherine Cortez Masto (D-Nev.) have asked the IRS as recently as this January why it had not yet been implemented.

There are in principle several barriers to implementing this scheme,32 but all of them can be easily resolved:

- The CP-27 serves to confirm several eligibility requirements that the non-filer portal does not collect. But the two primary items—that the claimant is not herself a dependent, and that the claimant has proper immigration status to receive payment—are also requirements for the EIP. Any taxpayer to whom the IRS has issued an EIP inherently satisfies these requirements.

- The CP-27 does serve to confirm one additional piece of information not collected via the non-filer portal or required for the EIP: that the taxpayer lived in the United States for at least six months. Without this criterion, the taxpayer is ineligible for childless EITC. Given the enormity of the current crisis, the IRS should exercise its administrative discretion with respect to this requirement for TY2019, and simply assume that filers with a domestic address on their portal submission and on their 2019 Forms W-2 or 1099 meet the residency requirement.33 The probability that any taxpayer would have lived in the United States when they were paid in 2019 and when they used the non-filer portal in spring 2020 but did not live in the United States for six months of 2019 is extremely low.

- The IRS has argued at times that it needs further statutory authority to make these payments using SAA at all.34 While it is unclear why SAA is insufficient as currently devised, it would be trivial for Congress to mandate these automatic payments, thus creating the requested authority.

Given limited IRS capacity, the IRS could also implement this automated process for all taxpayers likely eligible for the childless EITC, not just those who are portal users, and thus do away with the CP-27 program for TY2019 altogether.

2C. Streamline the process of claiming with-child EITC benefits for portal users.

Unfortunately, unlike the childless EITC, the with-child EITC cannot be easily automated because the IRS does not have key data on child residency. The simplest step the IRS can take in this context is to expand the CP-09 program, which allows families to easily claim with-child EITC after filing taxes: Increase the number of covered households, deliver CP-09 notices in tandem with payment of the childless EITC, and ensure sufficient capacity to process these forms despite the paper backlog.

The CP-09, which the IRS mails to filers who appear eligible for the with-child EITC but did not claim it, invites taxpayers to confirm their eligibility via a short form and mail it back to claim the credit. Usually, these mailers are sent only to a small fraction of the seemingly eligible non-claimant filers, who themselves are a minority of the EITC participation gap. At least for TY2019, the IRS should issue CP-09s broadly to any plausibly eligible household, including users of the non-filer tool. About a quarter of CP-09 recipients generally return it, meaning that this simple step is imperfect but could quickly get payments averaging $3,00035 to roughly 1 million households.36

To increase participation, the IRS should couple the CP-09 mailers with the automatic childless EITC payments described above.37 The CP-09 would thus consist of a check for the childless EITC, and a streamlined process to apply for the remaining, with-child portion of the credit. Including the childless portion of the payment may well induce additional households to claim the remainder of their refund, by demonstrating the real possibility of accessing funds.

3) Longer-term Reforms Inspired by the Crisis

For all the concerning issues identified above, the EIP delivery has also been extremely impressive. Faced with the task of issuing over 150 million payments at the height of a crisis that had decimated its capacity, the IRS took bold, powerful, and unprecedented steps to facilitate delivery. Within weeks, the IRS had launched a new tool for non-filers and automated payments to nearly 20 million beneficiaries. When the IRS takes seriously its mandate to get funds to people in need, it has the capacity to do so.

Building on this experience, Congress should ask the IRS to facilitate delivery of the critical EITC and CTC with the same commitment it has shown for the EIPs. A few components of the EIP initiative in particular should be replicated.

3A. Iterate on the non-filer tool and promote it for EITC-eligible non-filers.

For years, the IRS has struggled to increase the EITC participation rate above 80 percent. Two thirds of the participation gap consists of households who do not file taxes , and a variety of interventions have had low success in inspiring these households to do so. But, in the non-filer tool, the IRS has highlighted a powerful solution: Make filing easier for these households, and promote it as a quick and easy way to get money. For all of the usability issues afflicting the portal, it is a powerful proof of concept that such a streamlined filing process for low-income households is possible.

Through the non-filer portal, the IRS is already collecting the majority of the data it needs to pay the EITC. In the data it collects on dependents, the IRS already knows if children pass the “relationship test” for EITC eligibility. The IRS would need to add only two questions:

- Whether the taxpayer has lived in the United States for six months of the last year, which establishes eligibility for the childless EITC.

- Whether the child in question lived with the taxpayer for at least six months of the last year, which—in conjunction with the relationship data already collected—establishes eligibility for the with-child EITC.

With these questions added, the IRS could use the non-filer portal as a perennial “Get My EITC Payment” portal for otherwise-non-filers. Income would be calculated using the data the IRS already has on file.38 Because the EITC plateau for most households generally begins at or above the filing minimum, the IRS would not be at risk of overpaying the credit on account of having some income go unreported; taxpayers with additional income are free to file a full return declaring that income to claim more EITC. To avoid any esoteric edge cases, the IRS could begin by making the tool available only to households with relatively simple tax situations—e.g., households with only W-2 income—and iteratively expand it each filing season.

Anecdotal data suggests that many households who traditionally do not file did use the portal to claim average payments of around $1,700.39 The IRS would simply run the same process for EITC in the future, in which the average payment for families with children is over $3,000, and could make substantial progress in closing the participation gap.

As discussed above, the portal does currently suffer from serious usability issues, which would have to be addressed before re-launching it for EITC registration. The portal should be:

- Available in a variety of languages

- Mobile-responsive

- Rigorously user-tested and written in plain language so that average families can understand it

The IRS should contract with a high quality tech team inside or outside of the government to make these improvements. With the current portal, the IRS has proven that such a plan is viable.

Senator Brown asked about the prospect of this reform in a Senate Finance Committee hearing on June 30, and IRS Commissioner Chuck Rettig committed to its implementation.

3B. Automate the childless EITC going forward.

If the IRS implements Item 2B, it will have provided proof of concept for an ongoing automation of the childless EITC. The IRS should continue such automation in future years, and should implement changes to facilitate it. Specifically, the IRS should ensure it collects via Form 1040 any additional pieces of data it needs to automate childless EITC payments. Principal among these data items is U.S. residency, which could be easily added to the 1040, as TIGTA has recommended in detail. The IRS may also need to collect information about dependency, which could be added as well. The IRS should make these changes, and should exercise its administrative discretion by assuming eligibility under the additional requirements, allowing such automation until the change can be made.

3C. Beginning TY2020, make EITC/CTC benefits available via debit card.

Many experts have long argued for making EITC/CTC benefits available via debit card, to curtail the impact of exploitative financial services like “refund anticipation checks” and check cashing services. The experience with the EIP, in which the IRS has issued millions of payments via Direct Express cards, proves this is possible. The IRS should offer this option to low-income taxpayers receiving refunds in future tax years. In future years, the IRS should also address basic usability issues around the cards, including unclear mailing processes that caused some beneficiaries to discard the cards; contradictory instructions on the printed materials and the website; and a daily limit to bank transfers, which prevented some beneficiaries from accessing the funds promptly.

3D. Make EITC benefits exempt from offset.

Most anti-poverty programs are exempt from offset — that is, Treasury does not intercept these payments to pay down individuals’ debts to state and federal agencies — in recognition of the reality that low-income households desperately need all the money these programs provide. Tax refunds, including the EITC, are not; and VITA centers regularly report this is a major barrier for low-income households, who frequently ask about this issue before beginning the filing process. Recognizing the payments’ role as a critical anti-poverty program for low-income households, Congress smartly largely exempted the EIPs from offset.40 Recognizing the similar role of the EITC, it is time Congress do the same for that credit as well.

3E. Continue the waiver that makes facilitated self-assistance (FSA) tax prep software available remotely.

Facilitated self-assistance (FSA) is user-friendly tax preparation software, which low-income taxpayers have historically been eligible to use at VITA sites. The software is developed by TaxSlayer and other FreeFile companies, and is intended to be used only in a computer lab under the guidance of VITA volunteers.

In April 2020, recognizing the barriers to VITA sites’ operation, the IRS allowed FSA to operate remotely: VITA sites could provide the FSA link to taxpayers not literally on-site, provided they had capacity to answer questions from taxpayers within 24-48 hours. This waiver, which addresses the tax preparation needs of a significant portion of low-income taxpayers, should be extended beyond the current crisis.

As is expected in any large new program, the stimulus rollout was imperfect, and a few key steps are critical to ensure that the promised funds do reach all eligible families, especially those most in need. Congress and the IRS should finish the job; making these fixes would be life-changing for millions of families.

Moving forward, the IRS should build on the hard work it has done on the EIP program, bringing it to bear for other tax benefits like the EITC. The adaptations the IRS made to expedite these payments were transformative. The same innovation, and the same commitment to reach every family, is what will ensure that all Americans get the assistance they deserve — not just today but in coming years as well.

Downloads

Citations

- Indeed, the IRS’s initiative in proactively issuing EIPs meant that many advocates’ initial worst fears — including our own — did not come to pass. source

- This paper addresses only technical delivery issues, and does not address any broad-scale redesign of tax credits, which may be advisable in the long-run. We refer readers to the larger proposals from the Tax Policy Center – source, the National Taxpayer Advocate – source, and the Economic Security Project – source that increase the frequency of EITC payments and bifurcate the EITC into separate childless worker and child credits, among other critical steps.

- The June 11 wave of the Household Pulse Survey for the first time contained questions on the EIPs—but only regarding what households spent or planned to spend them on, not whether they were actually received, and received in full.

- Formally known as the “Non-Filer: Enter Payment Info Here” tool.

- Many VITA sites have reported seeing more clients than usual rejected over their authentication PIN, clients who have no recourse as the IRS has generally not been accepting phone calls about the EIP.

- Based on the authors’ interviews with organizations overseeing VITA sites.

- Based on 10-12 million total non-filers who are not otherwise automatically paid, and 6 million already using the tool. For estimates of total non-filers, see CBPP’s estimate of 12 million – source – and our own estimate of 10 million – source

- If the IRS determines that addresses on Forms W-2 and 1099 are not reliable, or that they constitute the “last known address” as defined in the statute, the IRS could first send a letter to these individuals using the W-2 or 1099 address, asking them to advise the IRS of their current address. The IRS would use income data on the forms to determine the amount of the EIP.

- Some advocates have proposed an analogous process using states’ Medicaid and SNAP benefit rolls: Beneficiary data would be shared with the IRS, which would then issue a payment to any beneficiary not yet paid. However, this proposal has generally met with privacy objections, and would remain more difficult to implement given that Medicaid and SNAP data is stored in 51 different state systems.

- Keep in mind, as well, that any household wealthy enough to be ineligible for the EIP is required to file 2019 taxes by July 15.

- For more detail on this, including its due process implications, see Nina Olson’s article about this issue. source

- The IRS had made a version of this announcement on April 15, this first one was not widely reported; and even then, provided beneficiaries only a week to act. The timeline—and the Taxpayer Advocate’s rationale for it—is outlined here. source

- Some advocates have been concerned that this process would be impossible, because the IRS would have filed dummy tax returns for these beneficiaries behind the scenes, in order to effect the payments. If it had, then beneficiary households would be blocked from using the non-filer portal again in 2020, and the IRS would have to come up with another solution. However, tax clinics have reported their SSA/VA-beneficiary clients have not been blocked from continuing to use the non-filer portal.

- While a June 25 GAO report estimated this number at 450,000 – source – IRS Commissioner Chuck Rettig reported the figure at 360,000 in his June 30 testimony before the Senate Finance Committee. source Both GAO and Rettig’s testimony reflected the IRS’s commitment to finish making these payments in July.

- Analysis by the Center for Poverty and Social Policy at Columbia University, on behalf of New America. Based on CPS data, CPSP analysts estimate there are 813,000 recipients of Social Security, SSI, or VA benefits who do not file taxes and have at least one dependent child in the household under age 17. Meanwhile, the IRS reports that 360,000 beneficiaries did claim dependents correctly but erroneously were not paid. This leaves up to 450,000 beneficiaries who may have missed the deadline. According to data from a survey circulated to low-income taxpayer clinics and community agencies by New America and the Center for Taxpayer rights, nearly half of agencies reported seeing “a few” or “many” cases of beneficiaries in these programs not being able to claim dependent children before the deadlines—which suggests the issue is at least somewhat widespread. We assume that at least around half of the remaining beneficiaries will have failed to do so.

- This is based on the types of cases being raised by VITA sites and community organizations, as well as those flagged on the Reddit forum about relief checks. source

- See the New York Times: “They also streamlined applications and approvals, requesting only that applicants be honest and simply checking their tax identification number and a few other basic facts rather than verifying all the information before making payments.” source

- Given that the IRS spends $1.8 million to operate a similar set of communications for CP-09 and CP-27 notices, which together comprise about 10 percent of the current EIP delivery gap, we estimate this cost may be approximately $15 million. However, this estimate is subject to significant uncertainty, given that tele-work may require additional equipment, or may allow the IRS to simply reassign existing staff. source

- Insofar as VITA sites may continue to help taxpayers with EIP access through the end of the calendar year, the IRS must also clarify whether the tax preparation software that sites use will be made available past October 15.

- For months the IRS did not directly confirm this point, but it was the only hypothesis consistent with a wide range of evidence. Nina Olson lays out much of that evidence in this post. source Additionally: (1) IRM 21.6.3.4.2.13 states: “Individuals who don’t normally file a return can use the Non-Filers Tool on irs.gov to register for an Economic Impact Payment. The taxpayer will enter basic information, such as SSN, name, address, and number of dependents, which creates a basic 2019 Form 1040 filing. The Service will use this information to determine eligibility and calculate the payment. NOTE: Returns filed using the ’Non-Filers Tool’ can be identified with $1 of taxable interest income, $1 total income, and $1 AGI.” This language suggests the portal is filing returns. And, finally, (2) VITA sites have reported that tool users have been blocked when they attempt to efile a second return, on the grounds that they have already filed one. The IRS finally confirmed the behavior in late June.

- VITA centers and low-income taxpayer clinics have reported widespread instances of this issue in practice.

- VITA sites have reported having to mail printed returns to their clients.

- The landing page states not to use the tool if “Your 2019 gross income exceeded $12,200 ($24,400 for a married couple) or other reasons require you to file a 2019 federal tax return.”

- In a Senate Finance Committee hearing on June 30, IRS Commissioner Rettig reported that 6.1 million non-filers had used the portal. source Note this is a larger number than the 3.7 million users that the National Taxpayer Advocate reported in late June. source

- This was also a dramatic about-face for the IRS. Most advocates, reading the tea leaves of earlier IRS announcements, were confident that the IRS would promote the 1040-X as the primary solution to this issue. source Some VITA centers reported holding off filing paper returns as they waited for the 1040-X to become available.

- In principle, the most direct fix would be to rewrite the e-File processing rules to allow superseding electronic returns. However, we suspect that such a fix is infeasible: It would require the IRS to rewrite basic portions of the e-File backend right as tens of millions of households are trying to use it to file their 2019 taxes.

- The equivalent letter for households with children is the CP-09.

- A large body of research—including a critical new study out of California—continues to show that minor nudges are insufficient to get all families to access the EITC. source

- It is also worth underscoring that, as currently constituted, the CP-27 and CP-09 are quite hard to use—and in some cases are outright incorrect. TIGTA already documented at length a major error on the circa-2015 CP-09, which caused households to incorrectly determine their own eligibility. source Incredibly, the 2019 versions of both forms continue to have an error in the same section. (See CP-27: source and CP-09 source ) On the form, households check any boxes that apply to them, and are told that checking the box makes them ineligible. Among the checkboxes is: “I (or my spouse and I) did not have earned income or excess investment income in 2018.” But the second half of this statement is backwards; the IRS wants to weed out people with excess investment income, not write them in. The statement should read “I (or my spouse and I) did not have earned income, or did have excess investment income, in 2018.” Moreover, the statement refers taxpayers to Publication 596 for a definition of the terms, but Publication 596 does not once reference the phrase “excess investment income.” source And, additionally, the TY 2018 CP-27 erroneously references tax year 2016 instead of 2018 throughout the form.

- TIGTA estimates that 1.7 million people in the participation gap are filers. Table 5 of Jones and Ziliak (2019) suggests a little over 20 percent of recipients are childless, which would suggest around 300,000 non-filing childless workers. source Meanwhile, CP-27s are sent to a little under 300,000 people, and it stands to reason that a higher portion of childless non-claimants receive notices than with-child claimants, given the simplicity of the eligibility rules (see TIGTA Appendix V), so the CP-27 population probably represents a majority of childless workers in the participation gap. This points to around 300-400,000 childless workers. The average payment to CP-27 recipients was $259 per TIGTA in 2014; we inflate this by 8 percent to 2020 dollars.

- See, e.g.,National Taxpayer Advocate, Special Report to Congress: Earned Income Tax Credit, p. 43. source

- An additional concern is that taxpayers with children might be considered ineligible for the childless EITC. Indeed, prior to 2017, IRS guidance specified that a taxpayer with a qualifying child was not eligible for the childless EITC, even if she did not claim the with-child EITC. This would arguably prevent the IRS from automatically paying the childless EITC, given that the taxpayer may have qualifying children and thus be ineligible. However, as Elaine Maag at the Urban Institute has noted, between 2016 and 2017 this guidance changed, so that the taxpayer is now eligible for the childless EITC (see Example 11 in the above links). 2016: source 2017: source

- Congress could also act to formally waive the requirement for TY2019.

- See National Taxpayer Advocate, Objectives Report to Congress, Fiscal Year 2020 p. 35. source During the June 30 Senate Finance Committee hearing, IRS Commissioner Rettig made the same argument in response to questions from Senator Maria Cantwell (D-Wash.); and Senator Brown noted that the IRS had given much the same answer in response to his January 2020 letter.

- Policy Basics: The Earned-Income Tax Credit. source

- In normal times, the EITC participation gap contains around 1.3 million filer households with children, all of whom could receive CP-09s. Given the increase in filing due to the EIP, this number is surely much larger for TY2019.

- Although more households are eligible for with-child EITC than childless EITC, all portal users should be eligible for both.

- By February 14, 2019, the IRS had received 219 million Forms W-2. (National Taxpayer Advocate FY 2020 Objectives Report to Congress, p.22.)

- As of May 22, the average EIP payment was approximately $1,680. source

- The EIP was exempt from all offset except for child support obligations.

More About the Authors

Tara Dawson McGuinness

Founder & Executive Director, New Practice Lab

Nina Olson

Executive Director, Center for Taxpayer Rights

Gabriel Zucker

Fellow, Public Interest Technology

Issues

Programs/Projects/Initiatives

Topics

Related