Table of Contents

- Executive Summary

- Introduction: Past, Present, and COVID

- Methodology and Definitions

- Housing Loss and Poor Data

- Housing Loss in the United States: Our National Rankings and Maps

- Housing Loss in Forsyth County, North Carolina

- Housing Loss in Maricopa County, Arizona

- Housing Loss in Marion County, Indiana

- Policy Recommendations

- Conclusion

Housing Loss in Forsyth County, North Carolina

“We were known for our manufacturing…” – County Official1

Introduction

In recent years, Forsyth County, North Carolina has made national news for its low rates of economic mobility and high rates of poverty concentration. A 2015 Harvard University study found that Forsyth County has the third worst economic mobility in the United States, and a 2014 Brookings study found that Winston-Salem, the county seat, has the second fastest rate in the growth of poverty concentration in the country.

How are these economic mobility roadblocks bound up with housing, a fundamental human right that for so many across the United States is under threat? To answer that question, researchers from New America’s Future of Property Rights program teamed up with Wake Forest University and Winston-Salem State University to analyze five years of Forsyth County eviction, mortgage foreclosure, and tax foreclosure data. We also interviewed government officials, housing advocates, real estate developers, journalists, lawyers, service providers, and community members in order to gain an in-depth understanding of local issues related to housing loss. We wanted to know how often residents lose their homes—whether through eviction, mortgage foreclosure, or another mechanism; who is most at risk of losing their home; where within the county this loss is most acute; why people are losing their homes; and what happened after they did. These diverse interviews evoked an array of common themes steeped in a history of deindustrialization, racial segregation, low wages, and gentrification.

However, in the midst of completing this research, the world changed. As the COVID-19 pandemic swept across America, it rapidly became clear that we would release this report at a time when millions of Americans are without jobs and at risk of losing their housing. This report became more than a way to show historic housing loss, but a tool city leaders could use to better predict where the hardest-hit neighborhoods of their city may be.

The root causes of housing loss are only being exacerbated by the COVID-19 crisis in Forsyth County. As many have predicted, the wave is coming: on July 1st evictions resumed in Forsyth County for those who do not live in subsidized affordable housing, and the Coronavirus Aid, Relief, and Economic Security (CARES) Act eviction moratorium for federal public housing, housing choice vouchers, FHA-insured multifamily properties, and multifamily-assisted properties expired on July 25. On September 1 the Centers for Disease Control (CDC) announced a nationwide ban on evictions until the end of the year. However rent will still be due on January 1, and thus far the government has not offered rent forgiveness and only limited relief.

For several months the U.S. Census Bureau has been conducting a weekly Household Pulse Survey focused on tracking the fallout from the pandemic. In North Carolina, the Pulse Survey conducted between July 16th and the 24th found that 23 percent of households across the state were housing insecure, meaning that they either missed their rent or mortgage payments last month or believe they will not be able to pay this month, and that 45 percent of households reported that at least one person in their household has lost employment income. Further, the Bureau of Labor Statistics reported in June that the county had an unemployment rate of 8.2 percent, double the rate in June 2019. Taken together, it is clear that this economic snapshot does not bode well for already struggling households in Forsyth County.

The pandemic may have shone a light on the scope of potential housing loss in Forsyth County, but as this report shows, the crisis has been there all along.

Background and Context

Located in the central Piedmont region of North Carolina, Forsyth County holds a population of around 350,000, making it the fourth-most populous county in the state. Winston-Salem, a city of roughly a quarter-million, is both its county seat and largest city. Along with the nearby cities of Greensboro and High Point, Winston-Salem is part of the Triad, a significant metropolitan area regionally.

The county’s socioeconomic history is critical for contextualizing recent trends in housing loss. Winston-Salem was historically home to major manufacturers including Reynolds Tobacco, Hanesbrand, and Western Electric. Throughout the mid-twentieth century, thousands of middle-class workers depended on good-paying union jobs throughout the county, though most unions were ultimately driven of town. Still, workers at these factories could earn middle-income salaries without college degrees well after unions were disbanded.

As a result of federal trade policies and the general transformation of regional economies, many factories have disappeared in recent decades, resulting in a 39 percent decrease in manufacturing jobs between 1990 and 2010.

Racial discrimination throughout the twentieth century played a key role in shaping the housing landscape of Forsyth County. Before successfully fighting for unionization with the Local 22 (FTA), Black workers were often forced to work the harshest jobs for little pay, including toiling on the factory floor for 54 cents an hour. Union and political activism after World War II radically reshaped the county as Black workers demanded and won their right to better conditions, higher pay, and safe participation in local and federal elections. Despite this, Black households were excluded from many Winston-Salem neighborhoods: a local ordinance mandated segregation in housing until it was struck down by a 1940 North Carolina Supreme Court ruling. Even then, the redlining of non-white neighborhoods, as well as the theft of informal family land, or heirs property, prevented Black households from building intergenerational wealth via property ownership.

Black neighborhoods near downtown Winston-Salem, including Happy Hill, were razed in the 1950s in order to construct government buildings and U.S. Route 52, part of nationwide urban renewal projects. Today, Route 52 is an informal dividing line between white and non-white communities in the city. Most census tracts west of the highway are predominantly white, and some contain less than 10 percent non-white residents. Conversely, tracts east of U.S. 52 are home to predominantly Black and Latinx households, with some tracts occupied by less than 3 percent white residents.

Other communities throughout Forsyth County, that make up the suburbs of Winston-Salem, tend to be demographically wealthier and whiter than neighborhoods east of Route 52 or further away from downtown Winston-Salem. In these areas, there are higher rates of homeownership, lower poverty levels, and, according to our housing loss index, lower rates of home loss.

As a result of these and other factors, portions of Forsyth County suffer from concentrated poverty and low economic opportunity. But Forsyth County policymakers have recently taken steps to increase economic growth. Local officials pride themselves in successfully fostering a community of small businesses and entrepreneurs. Hospitals, universities, and the nonprofit sector, already dominant employers in the economy, also continue to grow. While this economic transformation is attracting highly-skilled outsiders to the area, poor communities in East Winston and elsewhere continue to struggle with the transition to a post-industrial economy.

How, Where, and When Are People Losing Their Homes?

“Low-income individuals rent, and often bounce between properties…” – Executive Office, Local Nonprofit2

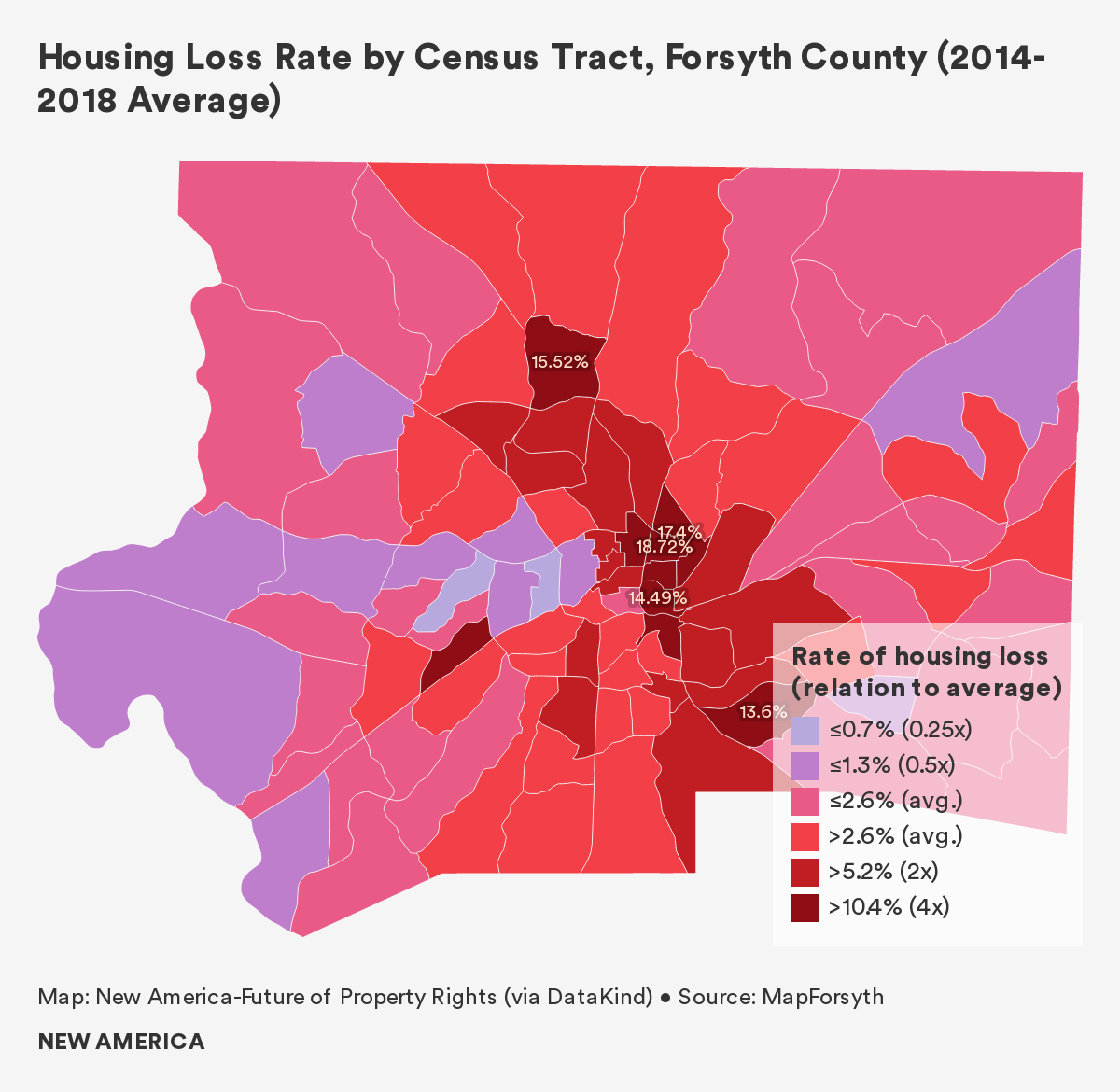

According to our national housing loss index, Forsyth County, North Carolina experienced a housing loss rate (accounting for both evictions and foreclosures) of 2.6 percent between 2014 and 2018.

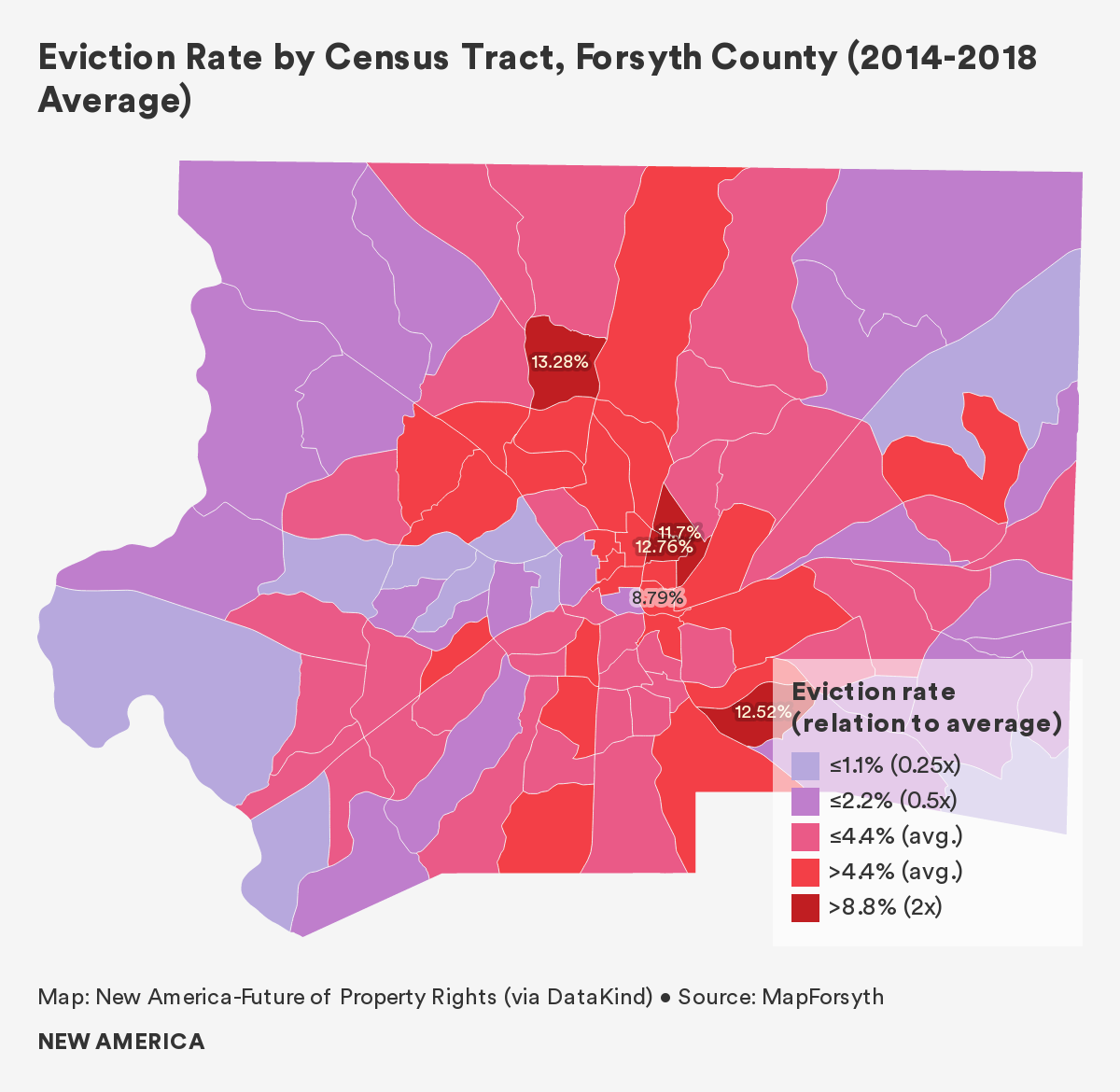

Evictions: Roughly 38 percent of households in Forsyth County rent their homes, yet evictions accounted for approximately 80 percent of all housing loss in the county from 2014 to 2018. The overall eviction rate for renter households was 4.4 percent during the study period.

A tenant can be evicted in North Carolina for nonpayment of rent, overstaying a lease, violating a lease agreement, or criminal activity. Based on key informant interviews, many low-income tenants in Forsyth County are evicted for non-payment of rent. These households are most often vulnerable to eviction as a result of a major life event, such as the loss of income or a job, or a medical emergency.

The eviction rate in Forsyth County is generally higher in census tracts with larger minority populations, as well as in tracts with more households living below the poverty line. Geographically, high loss tracts are concentrated to the east of downtown Winston-Salem, in East Winston. Based on analysis of data provided by MapForsyth, four census tracts all experienced eviction rates over 10 percent, the highest rates locally.

Census tract 28.06, which is located north of downtown and is bisected by Route 52, has the highest eviction rate of over 13 percent. According to ACS data (2012–2016) a majority of residents in this tract are non-white, as 40 percent of households are Black and over 14 percent are Latinx. Two-thirds of all residents in this tract are renters, of which 40 percent spend more than 30 percent of their income on rent.

Two other tracts with high eviction rates are located to the northeast of downtown Winston-Salem, close to Smith Reynolds Airport. According to ACS data (2012–2016) census tract 5, which has an eviction rate of over 12 percent, has a non-white population of over 90 percent. More than two-thirds of all residents earn less than $25,000 per year, and more than 40 percent utilize SNAP benefits for food costs. Directly adjacent to tract 5 is tract 16.02, which has an eviction rate of over 11 percent. The tract has a non-white population of over 80 percent, one-third of residents earn less than $10,000 per year, and over half utilize SNAP benefits. More than 70 percent of households in both tracts rent their homes, of which over half are rent-burdened.

The fourth census tract, tract 34.03, has an eviction rate of over 12 percent, and is located to the southeast of downtown. The tract reports a median household income of $34,898, and 37.7 percent of residents live below the poverty line. Most striking, half of tract residents are Latinx, and half of that group was born outside of the United States.

The geography of loss is unsurprising, as East Winston neighborhoods have long suffered from a legacy of disinvestment and racist public policies. Located beyond U.S. Route 52, the area is predominantly Black and Latinx. While a small entrepreneurial community is active in the area, the majority of residents suffer from lack of access to well-paying jobs, high-performing schools, public transportation, and grocery stores.

Due to a history of intentional segregation, the concentration of Black households to the east of the highway is no accident. As a result of this historic inequity, shared an executive officer at a local nonprofit, a small group of investors owns a large amount of substandard rental properties, with low-income renters often bouncing between complexes.

Worse, manufacturing expansion and environmental injustice such as poor air quality have negatively impacted minority households for generations.

Power differentials that have their roots in historic inequities also exist in small claims court, where eviction cases are heard. Many interviewees emphasized that the lack of legal representation for tenants in eviction proceedings results in rulings that overwhelmingly favor landlords. Evictions in Forsyth County often exceed 3,000 per year, but only 200 cases or so receive pro-bono legal representation, according to a local journalist.

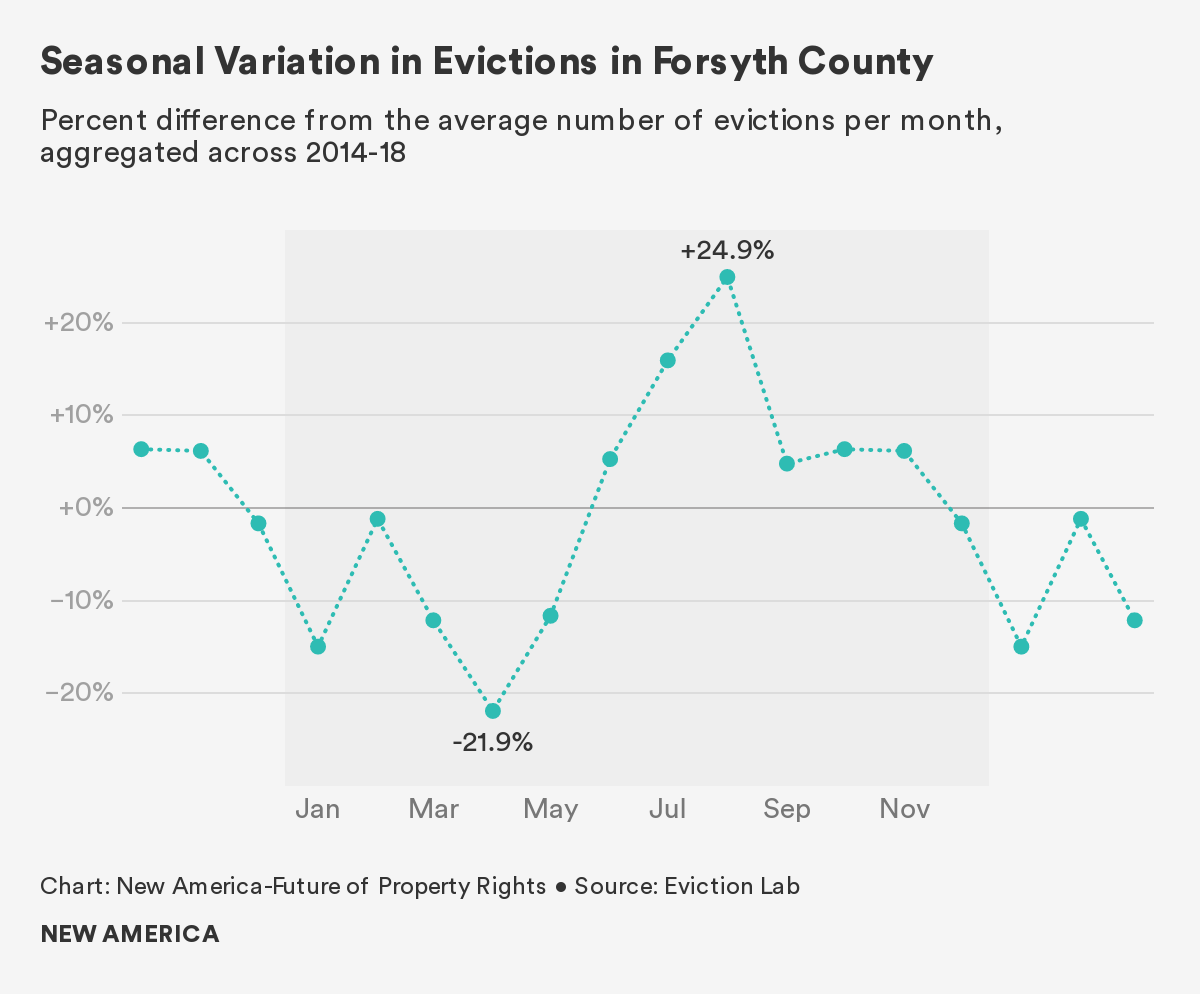

A Spotlight on Summer Evictions

Data suggests that evictions spike during the summer. Between 2014 and 2018, April saw the lowest monthly average with 160 evictions, while August saw the highest monthly average at 256—a 60 percent increase. One potential explanation for the drop in evictions in April could be a result of households receiving their tax returns, and having extra money to put towards essential costs.

Although in-depth research into seasonal variation in evictions is outside the scope of this report, we speculate that three factors drive this uptick during the warmer months. First, the high costs of air conditioning and other utilities might place financial strain on renters. Second, the high costs of childcare and lack of school-based food support programs during school vacations might place additional financial strain on renters. Third, landlords may be more willing to evict unsatisfactory tenants during the middle of the year, because it is typically easier to re-rent homes during the summer. However, we note that these factors are simply speculative and more research is needed to better understand this trend.

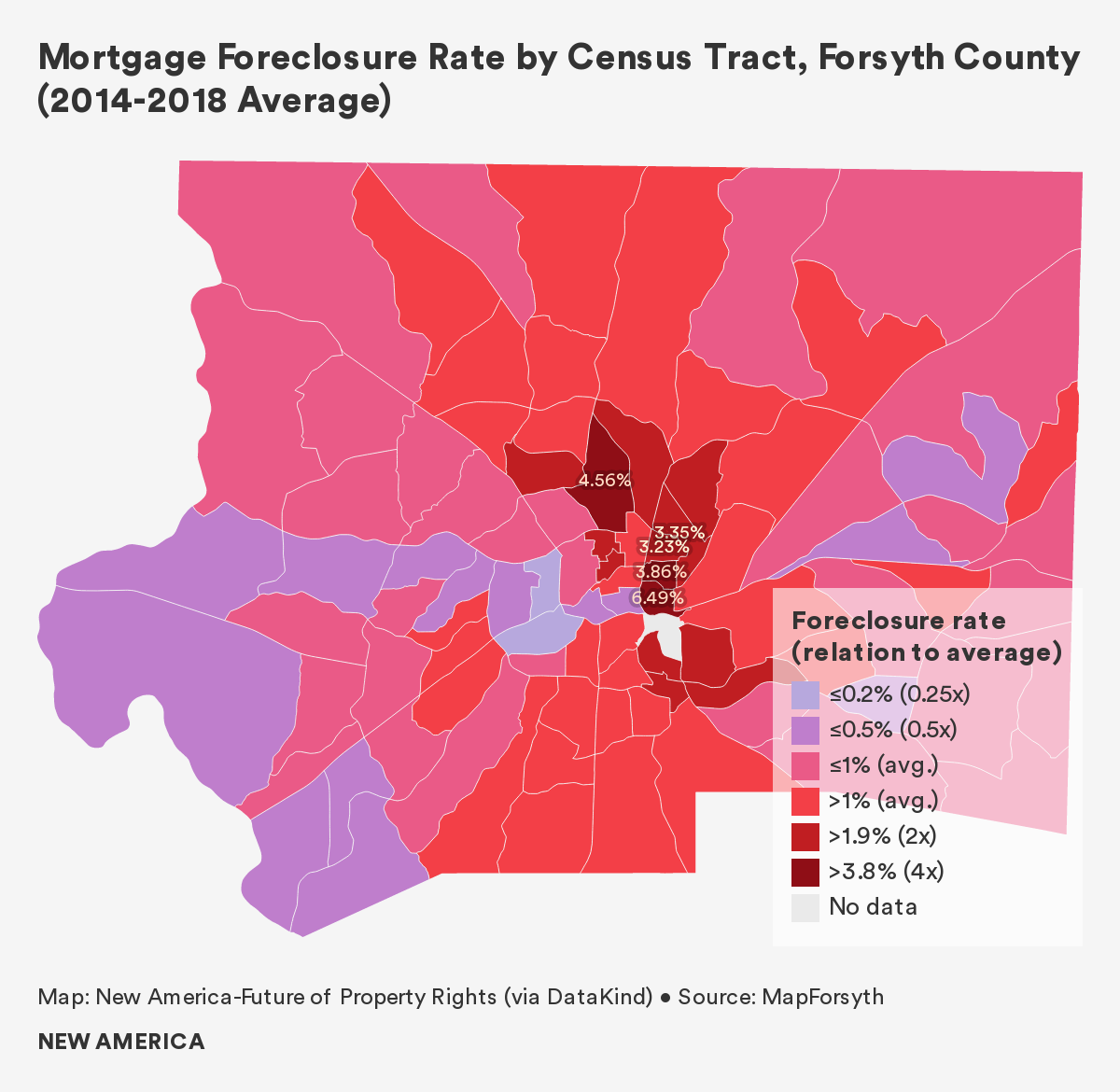

Mortgage Foreclosure: The number of yearly mortgage foreclosures in Forsyth County decreased by approximately 64 percent between January 2014 and December 2018. Slightly more than two-thirds of all households in Forsyth County own their homes, yet mortgage foreclosures only account for a fifth of housing loss during this five-year span. This suggests higher levels of housing stability among homeowners, as the average rate of foreclosure among households with a mortgage in Forsyth County was 1 percent.

Census tract 7, directly east of downtown Winston-Salem, in East Winston, experienced the highest mortgage foreclosure rate in the county between 2014 and 2018, at 6.5 percent. This census tract has a 94 percent renter occupancy rate, which suggests that foreclosures in this tract had the secondary impact of displacing renters. Median household income in the tract is $19,861 and the population is 71.1 percent Black, according to 2018 ACS data.

Two other census tracts in Forsyth County display mortgage foreclosure rates over four times the county average. Tract 6, which sits directly to the north of tract 7 in East Winston, reports an average mortgage foreclosure rate of 3.9 percent. The tract is similarly home to poor and Black households, with a median household income of $17,550, 48 percent of residents living below the poverty line, and 71 percent of the population identifying as Black.

In north Winston-Salem, tract 14 experienced an average mortgage foreclosure rate of 4.6 percent between 2014 and 2018. Residential neighborhoods in the tract sit close to the Wake Forest campus, the university’s athletic complex, and Smith Reynolds Airport. Median household income in the tract is $26,844, while 38.7 percent of households live below the federal poverty line and 59.7 percent of the population is Black.

Many tracts located in the west of Forsyth County report average to below-average rates of mortgage foreclosure, around 0.5 to 1 percent. Census tracts in the north and east generally express rates of 2 percent or below.3 Sitting outside of Winston-Salem city limits, many of these tracts include large percentages of white households. Overall, outlying towns such as Kernersville, Lewisville, and Tobaccoville are two-thirds white, at least, and median household incomes are near or higher than the national average.

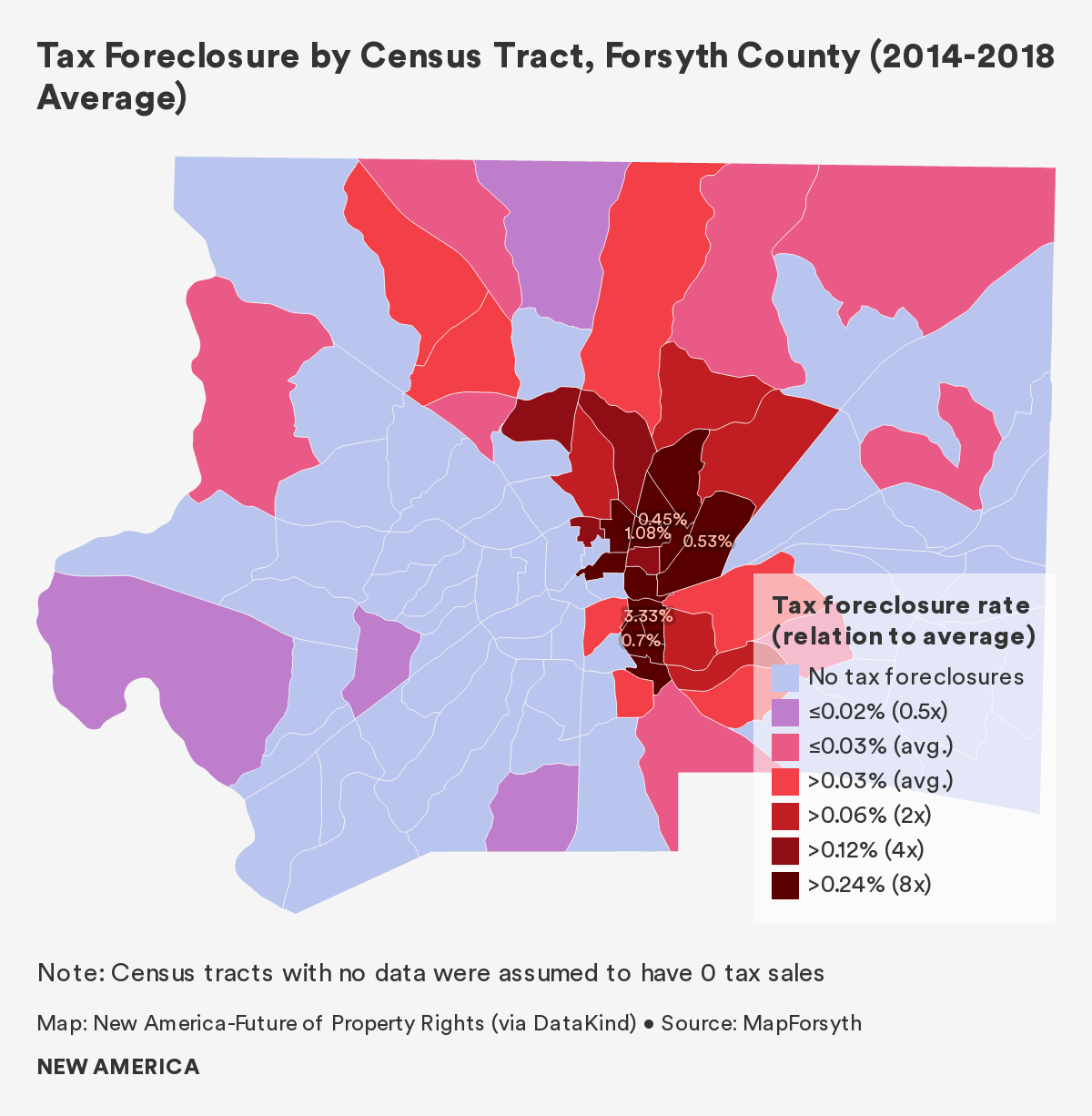

Tax Foreclosure: Tax foreclosure results from long-term non-payment of property taxes, usually over the course of several months or years. North Carolina is a “tax deed state,” meaning that investors bid on the deeds of tax-delinquent properties at public auctions. After a sale, the original property owner is given a short period of time to redeem the tax sale, or pay off back taxes, and keep the property. Otherwise, the title of property is transferred to the investor.

Data provided by MapForsyth unfortunately does not differentiate between owner-occupied properties, rental properties, and commercial or industrial properties. As a result, we were not able to calculate the tax foreclosure rate among homeowners without a mortgage—the demographic inherently at risk of tax foreclosure. Nonetheless, a map indicating tax foreclosures per total owner-occupied households in each census tract between 2014 and 2018 provides valuable insights.

Based on available data, only 140 tax sales were recorded during the five-year period measured. Many tracts were not listed in the data, and we do not know whether this is because no tax lien sales occurred in the tract, or because data was unrecorded or incomplete. Therefore, tax foreclosure results should be viewed with caution.

One census tract lying to the southeast of downtown Winston-Salem, tract 8.01, is worth highlighting. Encompassing parts of the Columbia Heights neighborhood, the tract reports the county’s highest tax foreclosure rate at 3.3 percent. Based on ACS data, the census tract appears distressed—to say the least. The median household income is $11,000 and 80.6 percent of households live below the poverty line, approximately five times the county average. The average property value in the tract is $44,400, while 30 percent of all units are vacant. The tract is also home to Winston-Salem State University, so low- or no-income students may be influencing the economic breakdown provided by ACS Data.

Our Housing Loss Index in Forsyth County:4 In order to measure housing loss that includes both evictions and mortgage foreclosures, we first calculated each census tract’s housing loss rate. The housing loss rate combines the total number of evictions and the total number of mortgage foreclosures in a given census tract, and then normalizes that sum by the total number of renters and the total number of homeowners with a mortgage within the census tract.

We then converted the housing loss rate into a housing loss index by comparing a given census tract’s housing loss rate to the county average. A census tract with a housing loss index of 1 experiences a housing loss rate equal to the county average, while an index of 3 indicates that the tract experiences a housing loss rate that is three times the county average.

Census tracts that express the highest values within our housing loss index are primarily located in East Winston. A few of these tracts lie directly to the east of U.S. Route 52, while others lie between Smith Reynolds Airport, the Wake Forest University athletic stadiums, and the local fairground. The two tracts with the highest housing loss rates, six and a half or more times the county average, lie near the airport. These tracts are primarily home to poor and minority households, including disproportionate percentages of Black and Latinx residents when compared to the county average.

Other tracts that experience housing loss rates more than five times the county average are located to the north and south of downtown on the east side of Route 52. All four tracts with high housing loss index scores also express high rates of eviction, which pushes them to top of the county index, despite having low foreclosure rates.

By contrast, census tracts outside of Winston-Salem city limits generally express housing loss rates well below the county average. These tracts comprise parts of smaller towns in Forsyth County, such as Clemmons, Bethania, and Walkertown, many of which have a housing loss rate around half of the county average. These communities are primarily white, in comparison to a considerably more diverse Winston-Salem, and many report significantly higher median household incomes.

Who is Losing Their Home?

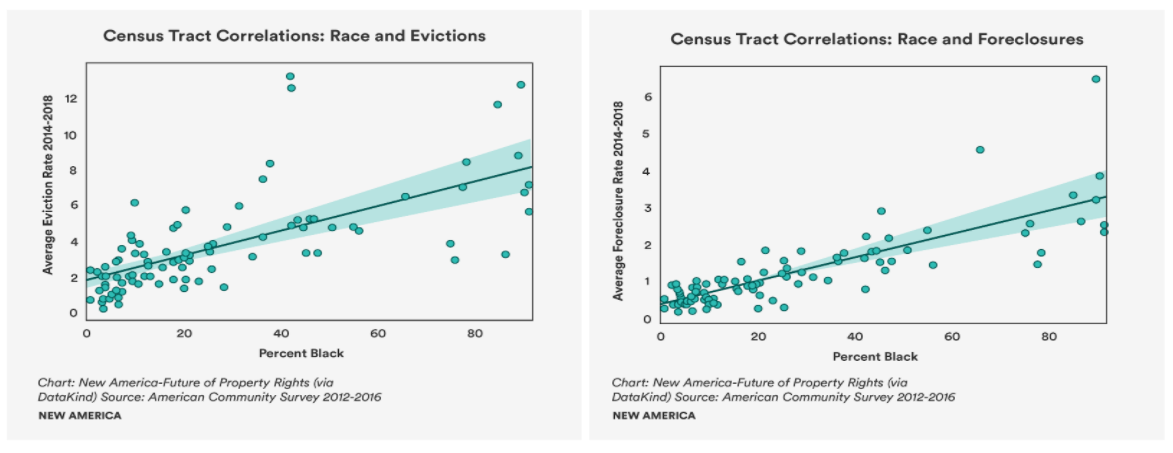

Census tracts with predominantly non-white residents had substantially higher rates of eviction, mortgage foreclosure and overall housing loss. In particular, we found a strong positive relationship between the number of Black households in a census tract, and the rate of mortgage foreclosures. Predominantly Latinx census tracts also showed higher rates of evictions and mortgage foreclosures than white census tracts, but the relationship was not nearly as strong as for Black households.

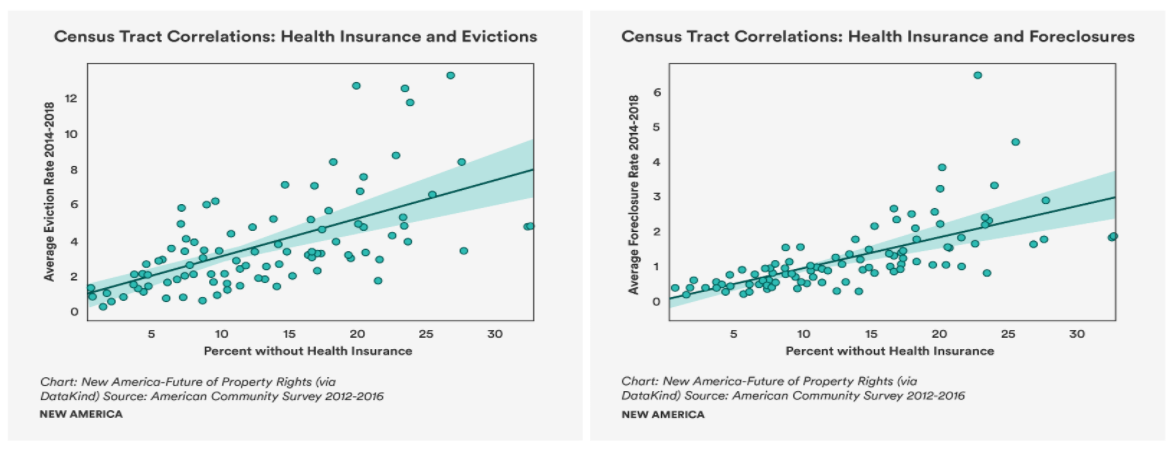

We also found that as the percentage of residents without health insurance in a census tract increases, so does the rate of housing loss, and in particular the rate of mortgage foreclosure. Many low-paying jobs do not provide health insurance, and this finding suggests that these at-risk households are generally housing cost-burdened on low income, or cannot pay for housing and medical treatment following an unexpected emergency.

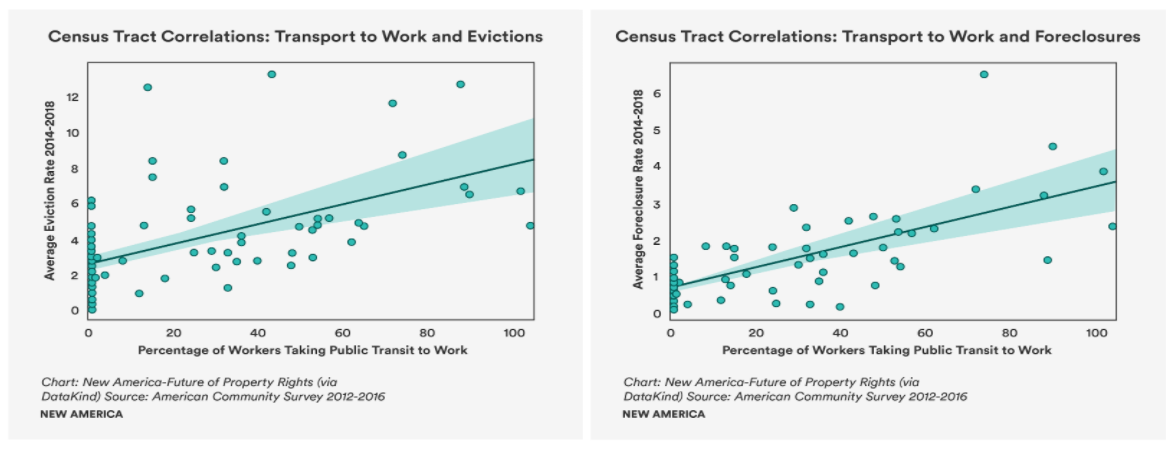

Tracts with a larger share of households that rely on public transportation for work commutes had substantially higher rates of mortgage foreclosure and overall housing loss. Local stakeholders observed that dependence on unreliable public transportation systems can lead to repeated tardiness or absence from work, job loss, and a subsequent inability to pay rent.

Census tracts in Forsyth County with higher shares of single-parent households had higher rates of home loss, and in particular higher rates of eviction. A lack of two incomes, the high costs of childcare, and difficulties in maintaining steady employment amid other responsibilities may all contribute to this elevated risk.5

Finally, as incomes, property values, and the percentage of owner-occupied units in a census tract rise, housing loss rates fall. This finding is unsurprising, as wealthier households more easily become homeowners; can buy more expensive homes; and usually do not struggle to pay monthly housing costs. Conversely, census tracts with lower incomes had higher rates of home loss. Specifically, households with median incomes between $10,000 and $34,999 were most strongly associated with higher rates of mortgage foreclosure.

Why Are People Losing Their Homes?

“Missing a single day of work or blowing a tire can lead to eviction” – Assistant Director, Local Nonprofit6

Housing insecurity in Forsyth County is complex and multifacveted. Based on key informant interviews, however, common themes surrounding insecurity emerged, notably the significant lack of affordable housing stock, which is exacerbated by poorly-paying jobs. Stakeholders also shared that long-time residents in Winston-Salem, and particularly in East Winston, are fearful of gentrification and subsequent displacement. While some data indicates ongoing demographic changes, there is limited evidence supporting actual displacement.

The Affordable Housing Crunch: The current supply of affordable housing in Forsyth County is quite simply insufficient to keep pace with demand. A 16,244-unit shortage of affordable rental housing for extremely-low-income households exists in Winston-Salem alone. Households that earn less than 30 percent area median income (AMI) can afford an apartment for $464 in monthly rent, but the fair-market rate for a two-bedroom apartment in the city is $729.

An additional 14,000 units of affordable housing are needed in Winston-Salem by 2027, with at least half for residents 65 years and older. Unfortunately, efforts to increase the supply of low-income housing are stymied in part by a lack of funding. Most affordable rental stock in Forsyth County is constructed via the federal low-income housing tax credit (LIHTC) program. The North Carolina Housing Finance Agency awards funding to projects in the county, but the application process is extremely competitive; only a few projects are funded each year. The 16 projects from the last decade added only 1,148 units of affordable housing throughout the entire county.

The Housing Authority of Winston-Salem runs the local housing voucher program, which provides access to quality homes for low-income households throughout the city. However, landlords are often unwilling to accept vouchers and there are not enough vouchers to support all those in need. The waitlist for the Section 8 Voucher (also known as the Housing Choice Voucher) program is currently closed to new applicants, and those who are on the list often wait years to receive support.

The county government also strives to promote homeownership, but reach is limited. The Department of Community and Economic Development, for example, operates a program to subsidize down payments and provide financial training for low-income households interested in becoming first time homeowners. This initiative has assisted over 800 families since the 1990s, but often turns away applicants due to the lack of a job or poor credit. More broadly, it is simply unrealistic to expect the program to benefit the approximately 56,000 renter households in the county.

North Carolina state policies also contribute to a shortage of affordable housing options. Due to preemption laws that prohibit local governments from establishing rent stabilization policies on properties that do not receive public subsidies, low-income tenants residing in unsubsidized housing are not protected from large rent increases. However, the efficacy of rent stabilization policies, like rent control, is hotly debated by economists.

Similar to many places around the country, Housing Choice Voucher availability in Forsyth County does not keep pace with demand.7 Not only that: program participants are often turned away by landlords, as North Carolina lacks state laws that prevent income source discrimination.

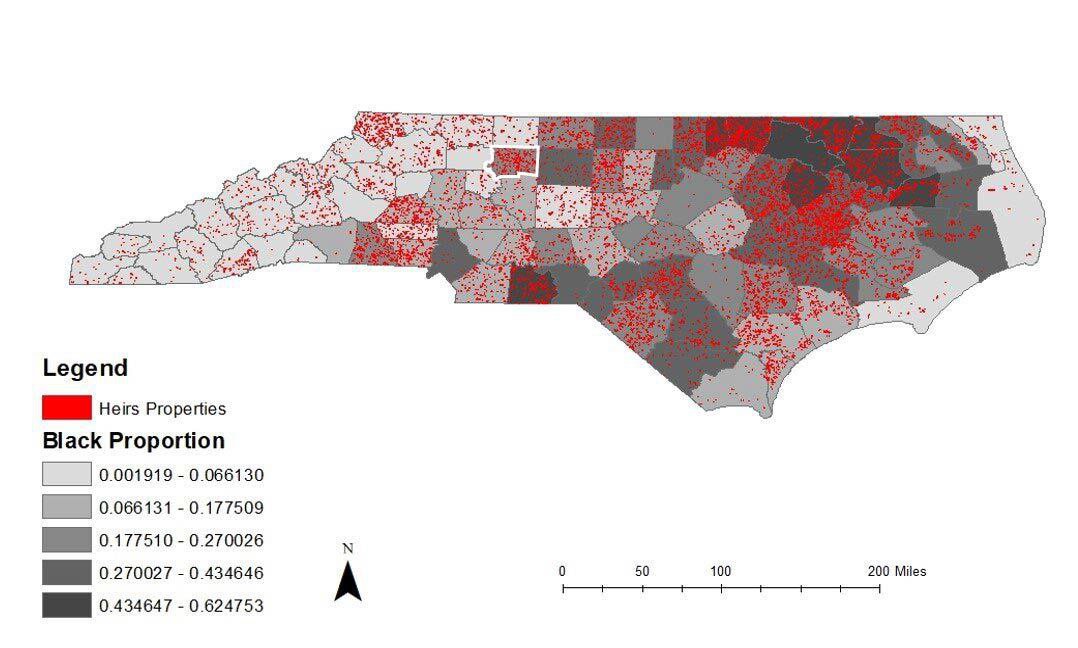

Heirs Property in Forsyth County

In Forsyth County, similar to other areas of North Carolina, some property is held through a form of tenancy-in-common known as heirs property. According to United States Department of Agriculture (USDA) research, Forsyth County has 1,524 heirs properties, the fifth highest number in North Carolina.

Heirs property disproportionately (though not exclusively) impacts Black homeowners in North Carolina. The legal structure of heirs property exposes holders to significant vulnerability. Because heirs property is passed down through generations outside the formal probate process, it often lacks “clear title.” As a result, owners may be barred from using the land as financial collateral, and may not be able to prove their ownership of the property. Equally problematic is that each heirs property owner controls all of the property equally—an undivided interest in the whole. As property is passed down through generations, the ownership—and decision-making responsibility—becomes split among dozens of owners.

Johnson Gaither, C., "North Carolina Heirs’ Property Estimation," USDA Forest Service

As noted in a recent USDA report:

“Decisions regarding management or disposition of the property generally require unanimous agreement among the owners. This can keep the property from being used productively, such as being rented or farmed, or it can discourage owners from investing in maintenance and upkeep. More tragically, too often this situation has allowed long-time owners and residents to be dispossessed of their lands through legal maneuvers from non-family members, particularly where outside development pressures have made property values increase, such as in coastal areas.”

In Forsyth County, one family we spoke with has seen much of their heirs property sold to developers, displacing both family members and long-term renters. This has also prevented some family members who live in the area from benefiting from the development of vacant land.

Whereas heirs property is often thought of as a rural problem, key informant interviews revealed that heirs property is prevalent within the city limits of Winston-Salem. Stakeholders told us that this property often falls into blight and disrepair because its many owners, burdened by a convoluted ownership system, are loath to invest in its upkeep.

Low Wages: Based on interviews, limited access to livable wages is a significant contributor to housing instability in Forsyth County. Wages are not increasing at the same rate as housing costs. According to a county official, rent costs increased approximately 5.5 percent in recent years, while wages decreased for 30 percent of county residents. Between 2008 and 2017, income per person in Winston-Salem declined from 93 percent to 90 percent of the national average.

The steady loss of manufacturing jobs, along with an increase in low-wage service sector employment, now contributes to almost half of all renters in Forsyth County being cost-burdened by housing. The results of this financial strain are expected: according to the Crisis Control Ministry, a local social service provider in Winston-Salem, clients’ most common complaint is an inability to pay rent. Many of those seeking support earn minimum wage, a meager $7.25 per hour in North Carolina.

A relatively minor emergency is often catastrophic for low-income households. Wage workers, in particular, can experience unreliable incomes that create budgeting difficulties. Blowing a tire, or missing a single day of work, for example, can lead to nonpayment of rent and eviction. The city bus system in Winston-Salem is notoriously unreliable and inaccessible, and many poorer Black and Latinx residents cannot plan consistent commutes. Tardiness or poor work attendance can quickly spiral into firing, unpaid rent, and housing loss.

Further, according to the director of a local housing nonprofit, some companies in the county reduce work hours to avoid requirements for providing employer health insurance and benefits. Instead of employees working one full-time position, they are forced to work multiple jobs to make up the hours lost, while still lacking access to critical health insurance coverage. In Forsyth County, over 12 percent of all residents lack health insurance coverage. For those without insurance, a medical emergency can result in the inability to pay for housing costs.

Gentrification, Displacement, and Concentrated Poverty

As Winston-Salem undergoes an economic transformation, many areas adjacent to downtown are experiencing increased investment. Lower-income neighborhoods, such as Boston-Thurmond, Columbia Heights, and East Winston are targeted by developers in search of cheap property. Redevelopment is lucrative for some, but new investment can also result in the displacement of long-time residents. Concerns are especially acute in the East End, with development increasing on East 5th Street.

In general, gentrification and resulting displacement results in a wide range of consequences. Due to growing lack of affordable housing options in redeveloped neighborhoods, many of those displaced are unable to find adequate replacement housing and move away from their community. A cyclical process drives more outside investment, raising the cost of living in these neighborhoods, and resulting in even more residents losing their homes.

{kind=link}

A local government report found that white residents are moving into downtown Winston-Salem at five times the rate of Black residents. But research from the University of Minnesota indicates that this gentrification is not actually resulting in displacement. This finding does not invalidate local fears concerning gentrification, however, nor does it negate future development and displacement.

At the same time, areas outside the core of Winston-Salem are experiencing increases in the concentration of lower-income residents of color. Several census tracts in the south and east section of Winston-Salem are designated as being racially or ethnically concentrated areas of poverty (R/ECAP), showing how the entire city has been impacted by this demographic shift. These designated areas often have low access to community amenities such as grocery stores and parks, and have suffered from historic segregation and disinvestment that has limited the economic mobility of residents.

What Happens After People Lose Their Home?

Housing loss is not only traumatic for residents who are displaced, but a shock to broader systems as well. These consequences are felt in schools, neighborhoods, and homeless shelters throughout the county.

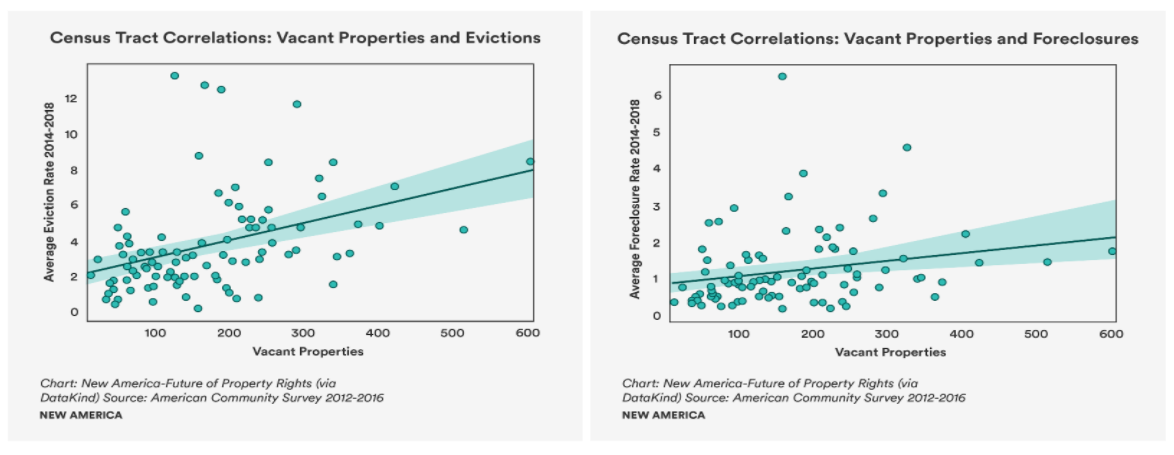

Neighborhood Neglect: A 2017 report found that foreclosed and vacant properties had real impacts on the communities in which they are located. The study found that for each foreclosed home, the economic impacts on the entire community were valued at over $170,000. These costs include reduction in property values of adjacent houses, increases in crimes and fires, and a reduction in property tax revenue for local governments.

There are over 6,000 vacant properties in Winston-Salem, with the majority located in the east/northeast and southeast planning wards of the city. Each of these vacancies impact the entire neighborhood, driving the value of other houses down, and the crime rates up. These same neighborhoods are also vulnerable to patterns of housing problems in rental units, with 50 percent of units having some sort of maintenance issue.

Our research found that census tracts with higher numbers of vacant properties also have high rates of housing loss, particularly evictions. There are many possible explanations for these correlations including high crime rates, low property values, and maintenance issues that could also be common in these tracts. More research is needed to determine the direct impact of vacant properties on housing loss in Forsyth County.

Tenants who have a history of eviction may be forced to live in substandard units for lack of a better option, as many landlords refuse to rent to tenants with a history of eviction or poor credit. Because their tenants are short on housing alternatives, this may further incentivize landlords to neglect their properties, driving neighborhood blight. This neglect spirals and drives disinvestment in the community, creating increasingly lower-opportunity neighborhoods without access to critical amenities like good schools, grocery stores, and quality employment.

A 2016 Food Access Report found that over 60,000 individuals in Forsyth County were food insecure, with large portions of the northeast, south, and southeast sections of Winston-Salem categorized as food deserts. Often in these areas, more than 33 percent of residents must travel more than a mile to get to a grocery store, limiting the potential for low-income families who do not own personal vehicles from easily accessing healthy, fresh food.

Education: Stable housing leads to stable education. Students whose families are evicted might be forced to switch schools multiple times in a single year. The Winston-Salem school system allows for school choice in designated zones throughout the county. Children can attend public schools outside of their neighborhoods, but parents must provide transportation. While a family that is displaced from their home has the ability to continue sending their children to the same school, it is often infeasible for parents to transport their children to a previous school if they have moved across town.

Key informants estimate that the county’s lowest performing schools have a turnover rate of between 20 percent and 50 percent; meaning that between one-fifth to half of students finish the school year at a different school than the one they started at, disrupting the education of thousands of students each year.

As a result of school choice policies, some underfunded schools are segregated and underpopulated, while schools in more affluent neighborhoods are overcrowded with students whose parents can transport them to better schools.

Additionally, public schools in Forsyth County rely primarily on county budgets for funding. This has led to complaints that the school board has discriminated against the very same segregated schools with predominantly Black and Latinx students regarding funding decisions for maintenance.

Lack of Access to Public Transportation: In Forsyth County, inadequate public transportation impacts economic security and housing stability in numerous ways. Many low-income residents may not have access to personal transportation, and as a result, choose to live near public transit. Local experts indicated, however, that some of the largest employers in the county are either not located on current bus routes, or typically have work shifts that do not align with current bus schedules. Herbalife and Caterpillar, for example, which collectively employ hundreds of residents, are inaccessible via public transit. Further, employees at the two top employers in the county, Novant Health and Wake Forest Baptist Medical, often work 12-hours shifts that end or begin outside of the hours that buses are typically in service.

Lack of access to public transit creates additional barriers for accessing other amenities such as libraries, grocery stores, and parks. Winston-Salem has a walk score of only 23.4, the third worst, and well below the average of 49 for cities with more than 200,000 residents, showing how dependent on cars residents are.

Jobs that are traditionally located downtown, or in the main ring of businesses around downtown, may become inaccessible for employees who have been displaced from their housing, exacerbating the impacts of housing loss. Many residents must transfer buses several times to reach their work destination as a result of the hub-and-spoke design of the local public transit system. In a 2019 report, CSEM found that individuals who rode the bus spent over eight times as long commuting to work than those who drove their cars. They did the math and discovered that the opportunity cost of their long commutes was worth more than $4,000 each year.

Homelessness: Families displaced from their housing as a result of eviction or foreclosure are at risk of homelessness, and sometimes resort to temporarily living with friends or family members. These living arrangements quickly lead to overcrowding, which is a well documented issue within Forsyth County. Overcrowding is particularly dangerous during public health emergencies, like the coronavirus pandemic.

Those unable to find community support can end up in a shelter, in their car, or on the street. In 2018, Winston-Salem and Forsyth County adopted a 10-year strategic plan to end homelessness that focuses on expanding policies for “light touch” interventions for families at risk of housing loss.

Some new research shows correlation between displacement as a child and the potential for homelessness as an adult, showing how one generation’s childhood experiences with forced displacement may contribute to future generation’s economic and housing instability. This poverty trap results in the inability for low-income families to climb the social mobility ladder.

Policy Recommendations

Housing insecurity does not have to be the norm in Forsyth County. There are several policies that can be implemented to prevent housing loss, support the maintenance and creation of affordable housing, and revitalize entire communities.

Certain policy solutions were voiced across all three of our case study locations; we included these commonly proposed solutions in our policy recommendations section, as we believe them to be broadly applicable across the country. These recommendations include but are not limited to: improving housing loss data; expanding the social safety net and increasing wages; expanding affordable housing options through voucher programs, trust funds and tax credit programs; and increasing parity between landlords and tenants, for example by improving tenants' legal rights. Below are four additional policy recommendations that were unique to our Forsyth County case study.

Expand Homeownership Programs: Forsyth County finances the Housing and Community Development Home Ownership Program, a program that provides down payment assistance to low-income families. Similarly, the state runs the Community Partners Loan Pool, which provides down payments as a deferred second mortgage with a zero percent interest rate. This loan is only repaid at the end of the loan period or when the house is sold. These programs should be expanded to provide homeownership opportunities to marginalized community members.

Adopt Forward-Thinking Development Policies: Forsyth County should be more aggressive in buying land for future affordable housing development. Local governments often wait for market-driven redevelopment before addressing issues of affordability and displacement. This hesitation to purchase land is costly in the long term, as revitalized areas often have higher land costs. In downtown Winston-Salem, for example, land used to be cheaper. However, both city and county officials refused to purchase land for future development. Now that downtown has been revitalized, they have been priced out.

Promote Affordable Housing Development as a Catalyst for Growth: The county should work to promote the development of mixed-income neighborhoods by supporting projects that rehabilitate blighted communities, similar to the Oneida Mills Loft Project in Graham, North Carolina. The affordable housing project was a catalyst for market-rate development in the area. Oneida Mills is now up and running, and the area around it has turned around. The creation of new housing developments has spurred competition for tenants. This has incentivized other property managers to improve their offerings through lower rent prices, or better housing.

Create Neighborhoods of Opportunity: Interviewees emphasized the role that communities of opportunity play in promoting social mobility. Often, affordable housing is situated in neighborhoods that lack access to grocery stores, retail stores, and professional opportunities, making nutrition and employment difficult. Local decision-makers should work to improve the opportunities within these neighborhoods, such as by expanding public transit to link these neighborhoods with grocery stores and employment opportunities. If expanding access to transportation is infeasible, bolstering community farmer’s markets and local employment should be considered. Finding creative solutions to improve the quality of life across the city benefits everyone, as no neighborhood should be left behind.

Conclusion

We began this research in 2019 to examine housing loss across the United States, and at a localized scale in Forsyth County. We could have never predicted that we would release our report in the midst of an unprecedented crisis, with tens of millions of Americans at risk for eviction and foreclosure as a result of the economic fallout of a global pandemic.

We have seen firsthand in the last few months how policy measures can help keep people in their homes. These policies, including nationwide moratorium on evictions, foreclosures, and utility shut-offs, deferments on mortgages, rapid expansion of federal housing voucher programs, and direct rent relief through local public housing authorities, have helped to delay a wave of housing loss that we believe is coming as programs begin to expire.

However, these policies must be targeted to communities most in need, and so we need to know who those communities are, and where they live. While the economic shocks resulting from COVID-19 are unique, we do believe that past housing loss provides an indication of future housing loss, even in these unprecedented times. As such, we hope this granular examination of where exactly evictions and foreclosures are most acute, and which communities are traditionally most impacted, will help municipal leaders and advocates direct outreach and resources in this time of crisis.

The COVID-19 pandemic may have elevated the urgency of eviction and foreclosure, but housing loss is a scourge even in times of relative calm. We must develop long-term policies to combat this systemic ill. Policy recommendations that we believe should be considered across the entire country are included in the national policy recommendations section of this report, and include policies to improve housing loss data, prevent housing loss, expand affordable housing options, and improve tenants' legal rights.

We also acknowledge that, in Forsyth County, the work is not done. We need more research to understand, for example, housing loss among low-income rural residents in the county. We must also better understand informal evictions, which do not leave a legal trace and are therefore difficult to track. And, we must understand why and where lower-income households move, when not forced out of their homes through eviction and foreclosure.

Citations

- From an interview with the authors.

- From an interview with the authors.

- While these rates are at or below the county average, it is critical to note that numerous tracts express mortgage foreclosure rates two to three times the national average.

- In order to generate an indicator of housing loss based on the total number of evictions and mortgage foreclosures, we created two new variables: housing loss rate and housing loss index. The housing loss rate reports the total number of evictions and mortgage foreclosures as a proportion of the total number of renters and homeowners with a mortgage in a given geography (here, Census tract). The housing loss index reports the housing loss rate by Census tract as a proportion of the mean (average) housing loss rate across the entire county. As a benchmark for interpretation, a housing loss index of 1 indicates that the Census tract under consideration has a housing loss rate equal to that of the county average, while an index of 3 indicates that the Census tract has a housing loss rate that is three times the county average.

- This finding is supported by national research which shows higher rates of eviction among families with children and single-parent households.

- From an interview with the authors.

- This problem is not unique to Forsyth County. Nationally, only one in five renter households who qualify for the housing choice voucher program—commonly known as Section 8—actually receives it. Many cities have waiting lists for up to 10 years or more; or have closed their lists down altogether.