Design Principles for Financial Aid Offers

Abstract

In 2018, New America partnered with uAspire, a nonprofit focused on college access and affordability, to review thousands of financial aid offers from over 500 colleges and universities. The resulting report, Decoding the Cost of College: The Case for Transparent Financial Aid Award Letters, recommended several minimum bars financial aid offers must pass including listing price, separating loans from grants, and standardizing terms and formatting. But those recommendations were just a start.

This report reviews findings from the Decoding the Cost of College report, presents each stage of our efforts to redesign financial aid offers, and discusses our recommendations for design principles. We offer an example of how financial aid offers should be structured, and the role of policy in improving financial aid offers.

Acknowledgments

This work would not have been possible without the generous support of the Kresge Foundation, Lumina Foundation, and the Bill & Melinda Gates Foundation. The views expressed in this paper are of the authors alone. New America would like to thank the numerous researchers, experts, and practitioners who graciously shared their insights, knowledge, and experiences, especially our Financial Aid Offerpalooza participants. The authors would like to thank Stephen Burd for editing, Sabrina Detlef for her copyediting support, and Riker Pasterkiewicz, Julie Brosnan, Fabio Murgia, Joe Wilkes, and Naomi Mourduch Toubman for their communications and data visualization support.

Downloads

Introduction and Context

How to pay for college has long been a top concern for students and families. While the federal government, states, and institutions provide financial aid, there are many hoops that students have to go through before being able to access aid. Even when students are finally accepted to colleges of their choice and receive financial aid offers—also known as financial aid award letters or packages—the process does not get any easier: the jargon, the vague fine print, the inconsistent breakdown of cost calculations all make it harder for students and families to understand the bottom line of the offer.

While the problems with financial aid offers have been acknowledged for a long time and some efforts have been made by the U.S. Department of Education,1 the National Association of Student Financial Aid Administrators,2 and the institutions themselves to improve their clarity,3 a survey released by Sallie Mae in April 2020 shows that students and families still struggle with comprehending the price of college and the availability of aid. Only a quarter of families find all components of a financial aid offer easy to understand, and 43 percent of families find at least one component difficult to understand.4

We partnered with uAspire, a nonprofit focused on college access and affordability, in 2018 in order to review thousands of financial aid offers from over 500 colleges and universities. We found alarming issues in current financial aid offers, such as the inconsistent use of terminology and the misleading inclusion of Parent PLUS loans.5 In fact, the 500 offers used more than 136 different terms to describe the Federal Direct Unsubsidized Loan, including 24 that did not even use the word loan. In our report, Decoding the Cost of College: The Case for Transparent Financial Aid Award Letters, we recommended several minimum bars financial aid offers must pass including listing price, separating loans from grants, and standardizing terms and formatting.

But our recommendations are just a start. We believe it is important that students and families be involved in deciding what formatting, terms, and elements matter most to them. For this reason, we kicked off a yearlong project in summer 2019 to design a financial aid offer that ensures students and families can successfully navigate and understand how much a college will cost and what types of financial aid they will receive. The project started with a convening of stakeholders to create financial aid offer prototypes and continued with two rounds of consumer testing that included interviews with students (both traditionally aged and non-traditionally aged) and parents. This research and the principles of design it yielded can inform the process of improving financial aid offers that is happening at institutions, states, and at the federal level.

This report will review findings from the 2018’s Decoding the Cost of College report, present each stage of our efforts to redesign financial aid offers that include the Financial Aid Offerpalooza and the interviews, and showcase the development of financial aid offers through each stage. Finally, we will discuss our recommendations for design principles, offering an example of how financial aid offers should be structured, and the role of policy in improving financial aid offers.

Citations

- U.S. Department of Education (website), “The College Financing Plan,” source

- NASFAA (National Association of Student Financial Aid Administrators, website), “Improving Financial Aid Offers,” source

- Elissa Nadworny, “Confused by Your College Financial Aid Letter? You’re Not Alone,” NPR, April 10, 2019, source

- Sallie Mae, How America Pays for College (Newark, DE: Sallie Mae, 2020), source

- Stephen Burd, Rachel Fishman, Laura Keane, and Julie Habbert, Decoding the Cost of College: The Case of Transparent Financial Aid Award Letters (Washington, DC: New America, June 2018), source

Decoding the Cost of College

In Decoding the Cost of College, we took a close look at financial aid offers from 500 schools that were predominantly four-year public and nonprofit colleges and universities. Each of the financial aid offers we reviewed included a Pell Grant so that we could make consistent comparisons. This research revealed just how challenging it is for students and families to understand a financial aid offer from a college, let alone compare it to offers from other colleges.

Many of the offers described financial aid using jargon and inconsistent terminology, making them difficult to understand and compare. We found that over a third of institutions did not include any information on the actual price that the college was charging. Grants, loans, and Federal Work-Study were often grouped and totaled together even though they have very different terms and conditions. Some financial aid offers inappropriately included federal Parent PLUS loans in the package even though parents can access these only after passing a credit check, making it seem that the college was being more generous than it actually was. Few offers provided any sort of calculation about the remaining cost that students and their families were responsible for paying. And only half of the institutions provided information about what next steps students should take to accept or decline their grants, scholarships, and loans.

Based on these findings, we suggested that state and federal policymakers create a standardized template for financial aid offers through legislation. In the interim, colleges, when designing their own offers, should:

- Require a written financial aid offer to all qualified students and employ standardized terms with student-friendly definitions

- Include full cost of attendance with a breakdown of direct costs and indirect expenses

- List grants/scholarships and loans separately

- Separate Parent PLUS loans and Federal Work-Study from scholarships, grants, and student loans

- Calculate the student’s net cost and estimated bill

- Identify critical next steps

The Financial Aid Offerpalooza

After publishing our report, we wanted to better understand just how terminology and formatting could be standardized and presented more clearly. We knew that a clear, accurate, and consumer-friendly offer cannot be accomplished if designers do not understand their users. For this reason, we invited the users (students and parents) and the designers (financial aid and enrollment officers at colleges and universities) to a daylong design workshop called Financial Aid Offerpalooza.1 Our goal was to facilitate conversations among the groups and have them work together to create a concrete financial aid offer prototype. The workshop also included other stakeholders, such as college access and guidance counselors, financial aid software developers, and policy experts. With diverse expertise and different levels of experience with financial aid offers, each participant brought to the discussion a distinct perspective on how a financial aid offer should look and what information it should include.

New America

In advance of our Financial Aid Offerpalooza, we convened three focus groups conducted by FDR Research Group: one of traditionally aged students, one of non-traditionally aged students, and one of parents of college students.2 Through the focus groups, we grew to understand which components of the offer are confusing to students and parents, how the technical terminology falls short, and what students and parents would like to see in the offer letters. The results of those focus groups were used to help frame and shape our Financial Aid Offerpalooza and were shared publicly and with the participants of the event.3

Under the facilitation of Stephanie Nguyen, a user-experience (UX) design expert, participants in the event learned about the challenges that students and families go through when it comes to navigating financial aid offers and the resources students and families rely on to overcome those difficulties. Colleges and organizations presented the changes they have made to their financial aid offers, and how these changes have worked for their students. The needs of both institutions and students that might have been overlooked came to the surface, driving thoughtful debate about how important information such as college prices and loans should be presented and how to simplify jargon and terminology and not mislead students and parents.

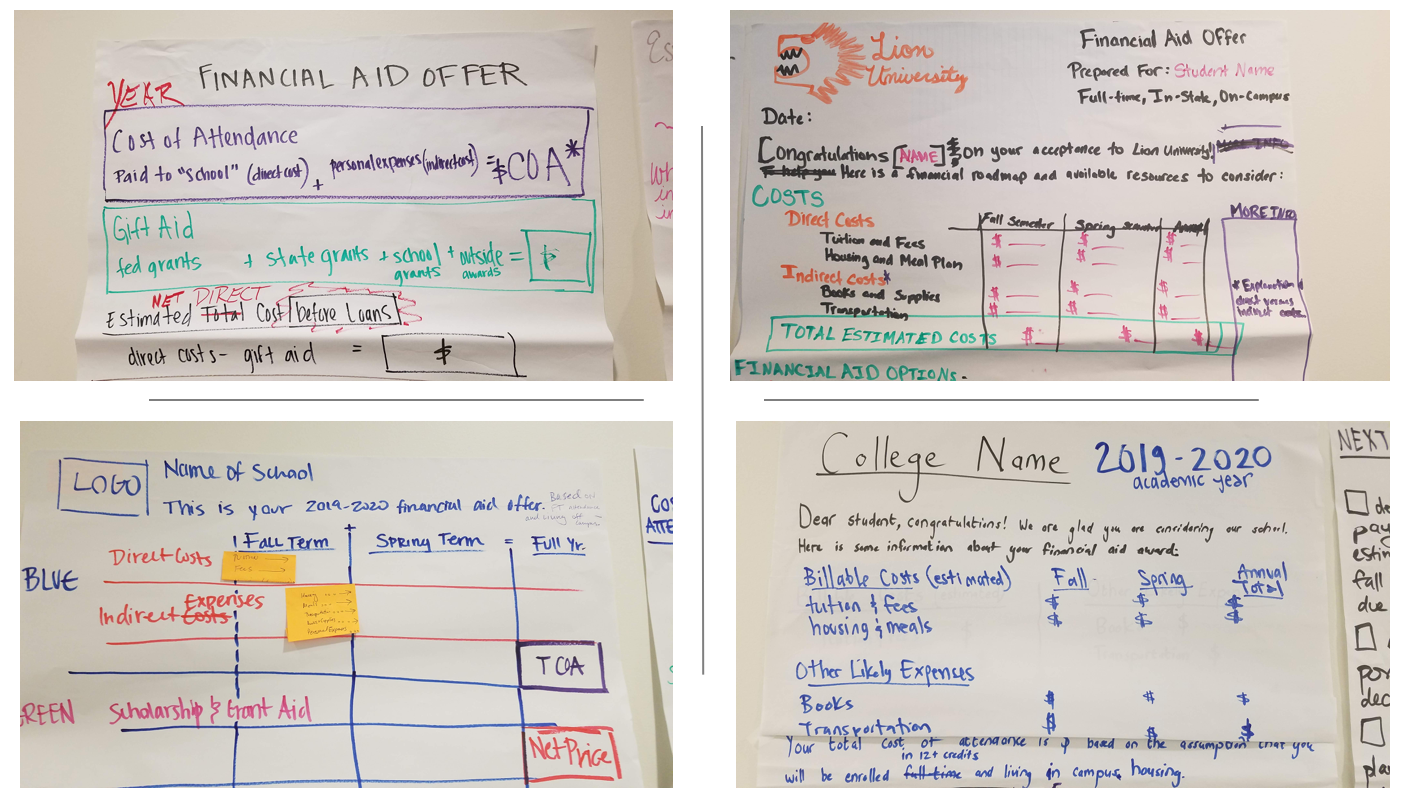

Following the discussion, participants were divided into teams to design financial aid offer prototypes. Nine prototypes were created, with many inventive features. Most prototypes followed the recommendations from our report, Decoding Cost of College, such as separating loans from grants, calculating remaining cost after financial aid, listing other financing options, and next steps. These prototypes creatively made the terminology more self-explanatory and accessible, either by using plain language instead of financial aid jargon, or by providing concise yet accurate definitions for terms students and families had struggled to understand. All prototypes placed cost information first, and then the other elements of the financial aid offers.

New America

New America

New America

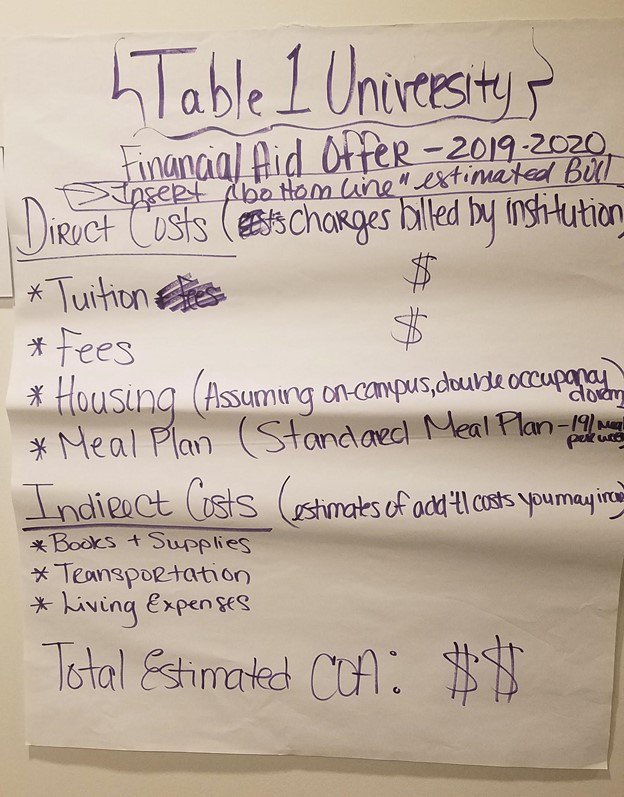

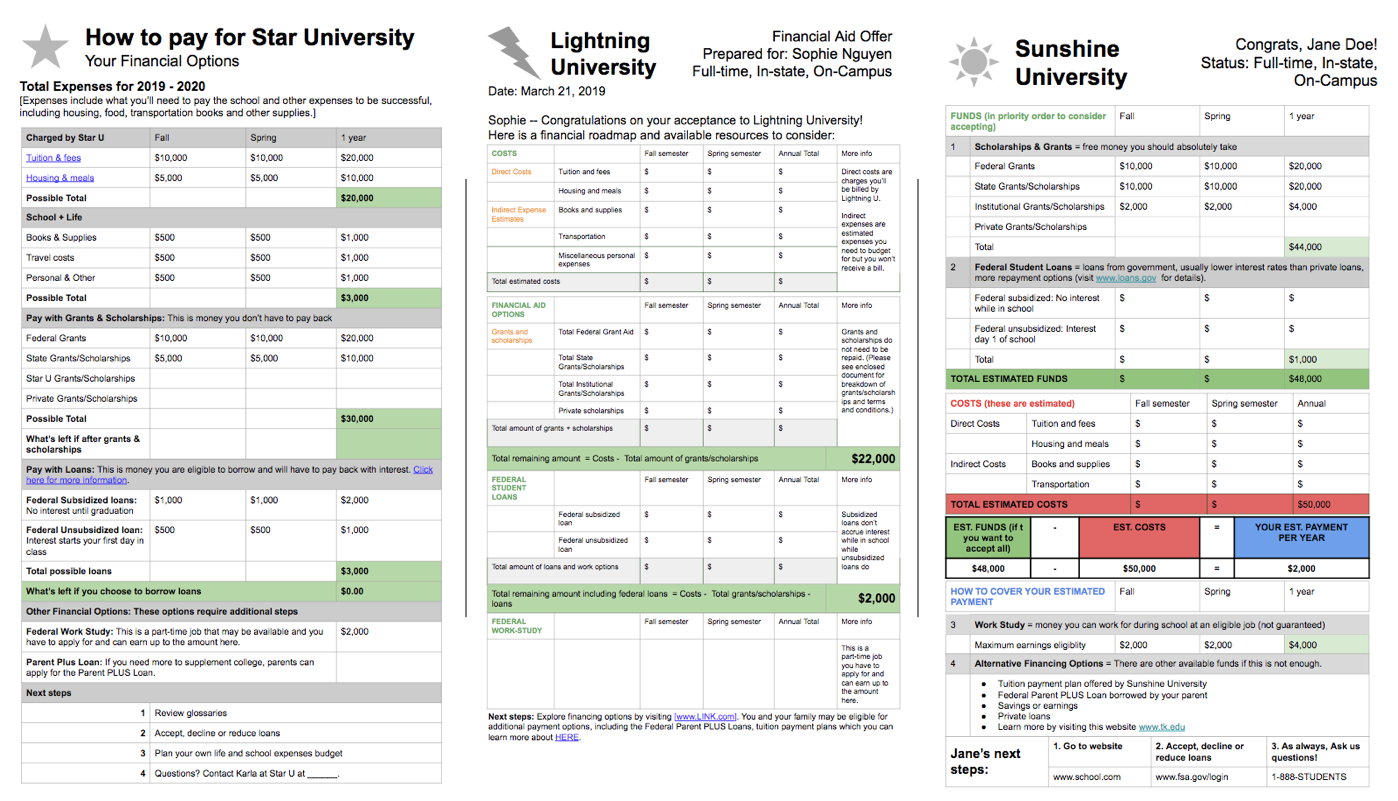

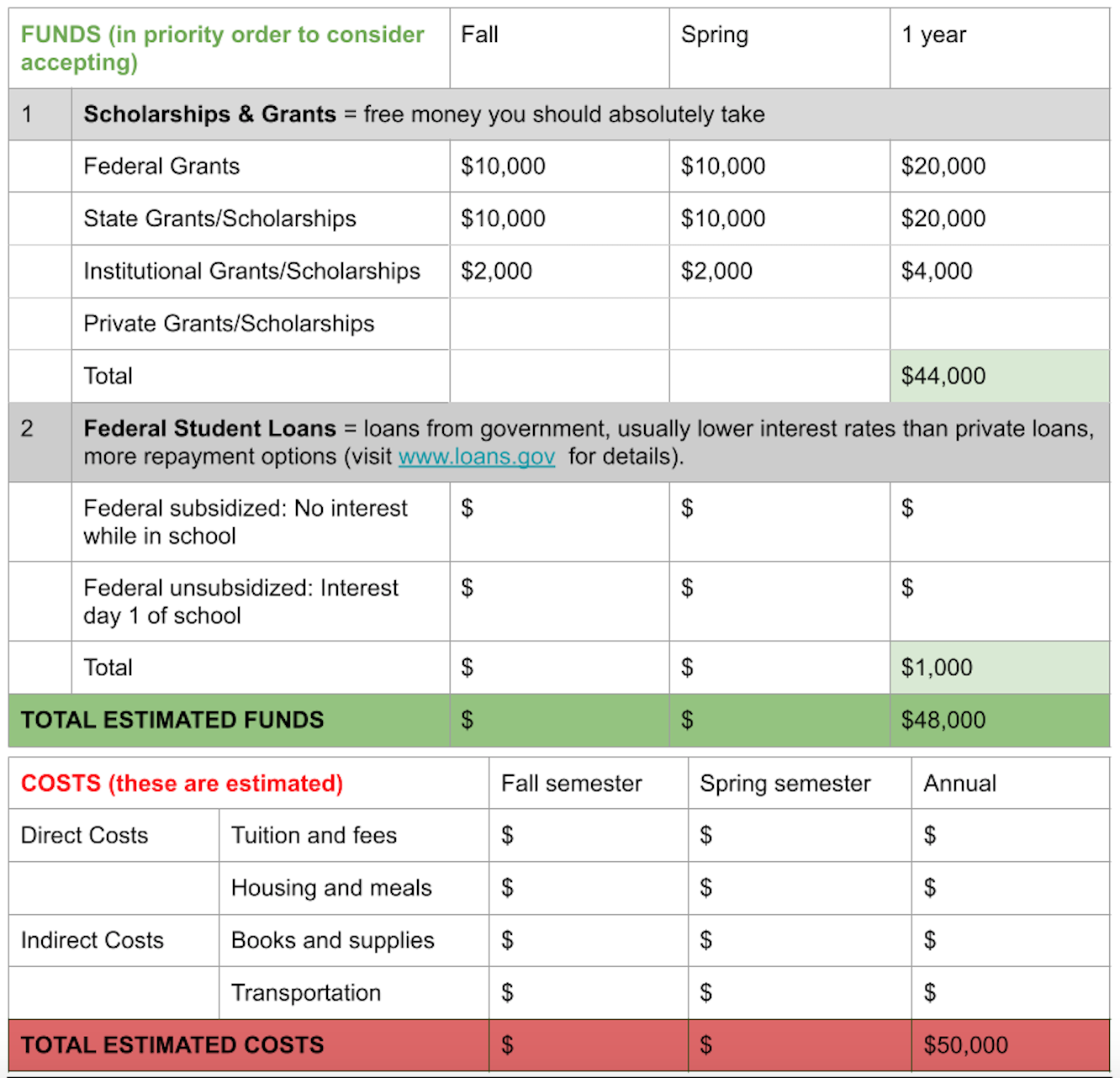

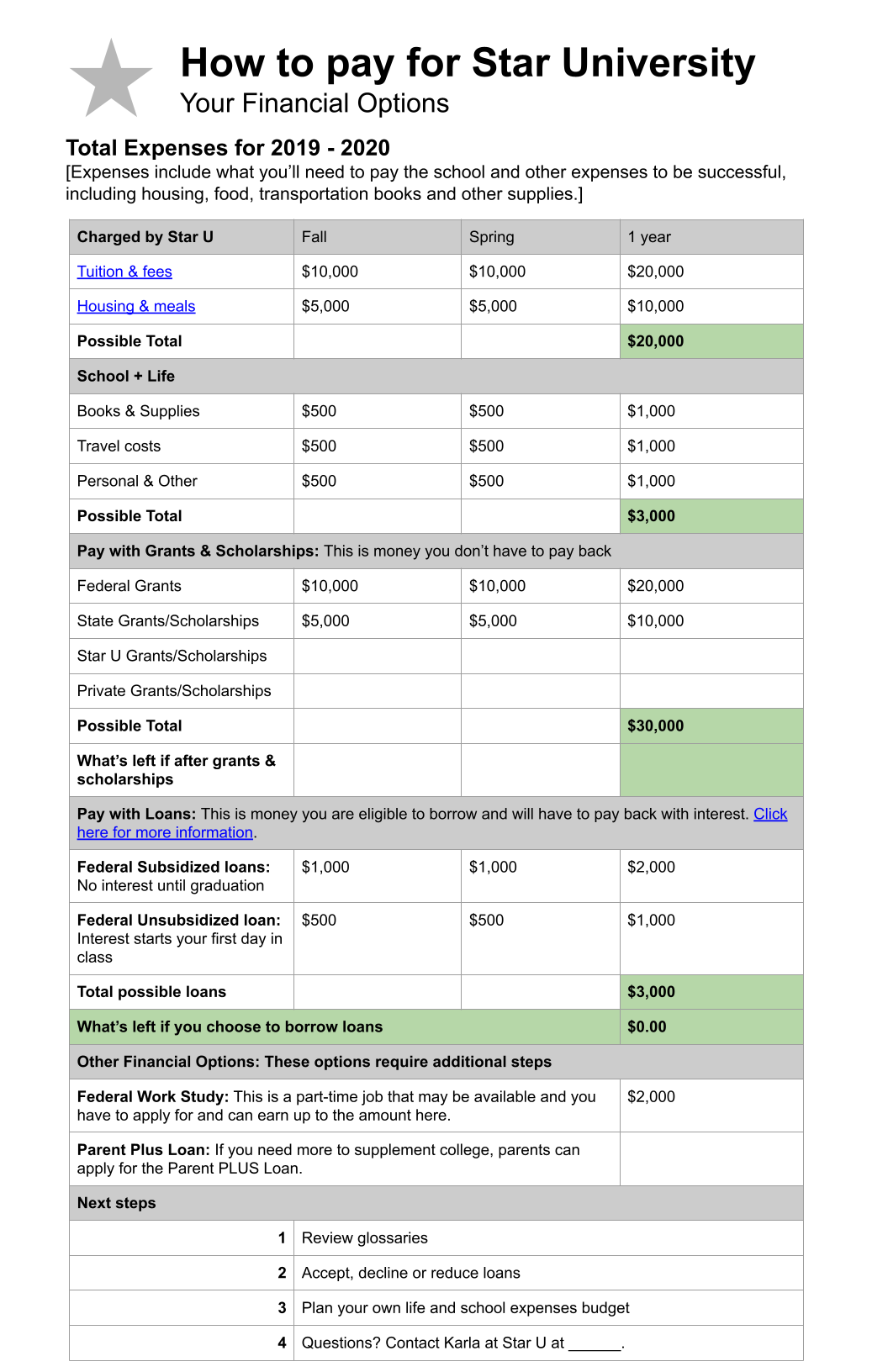

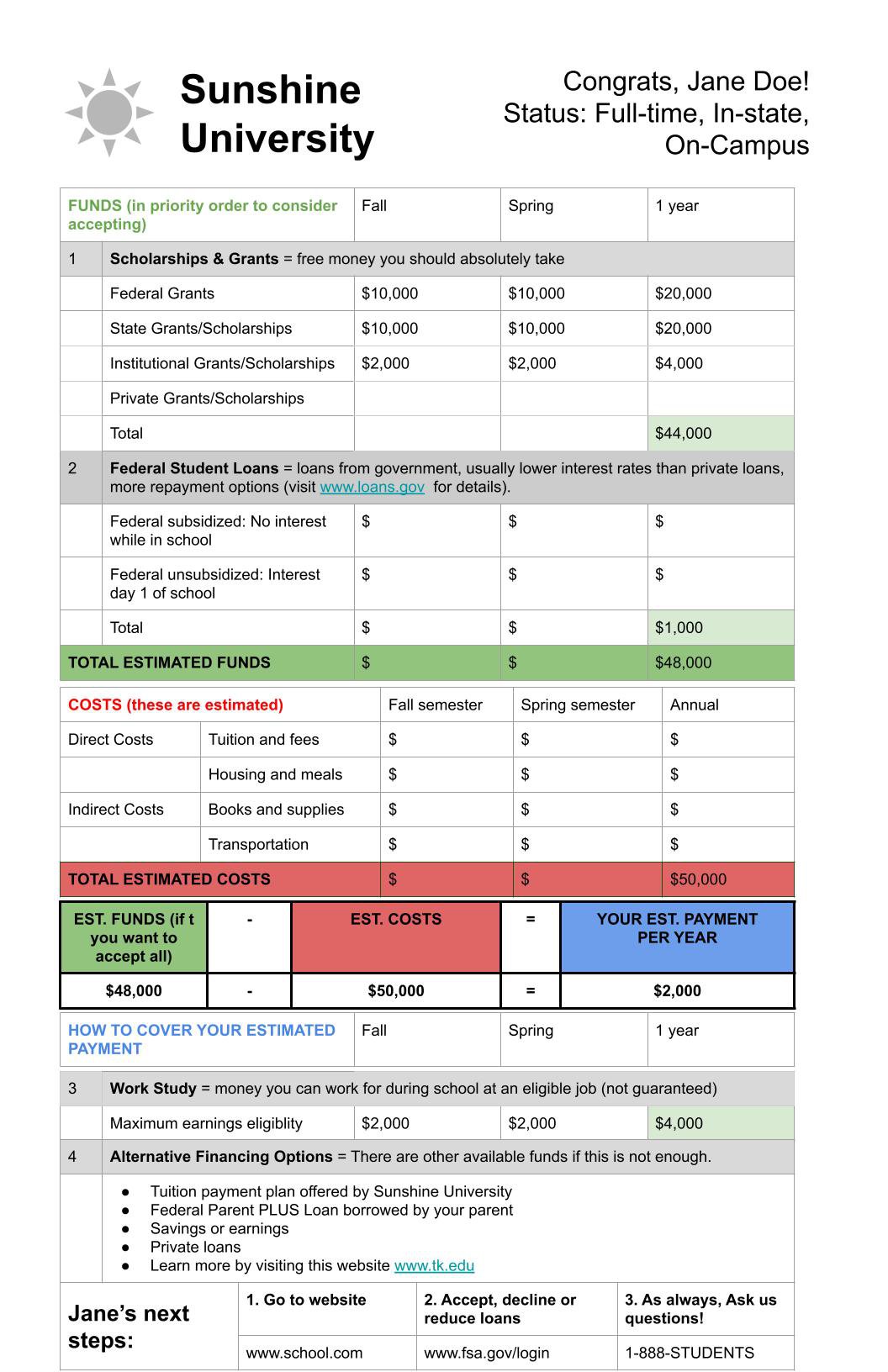

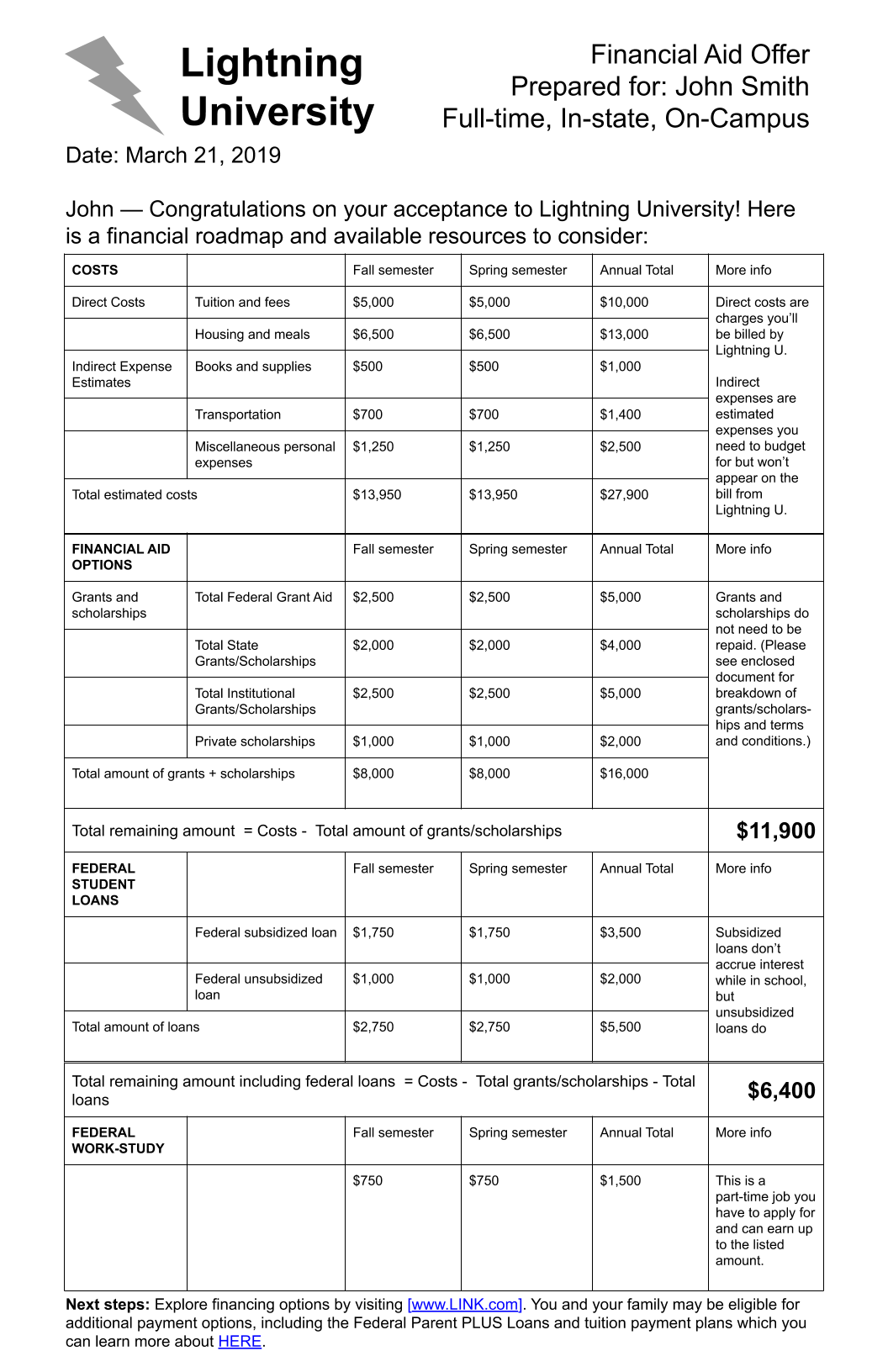

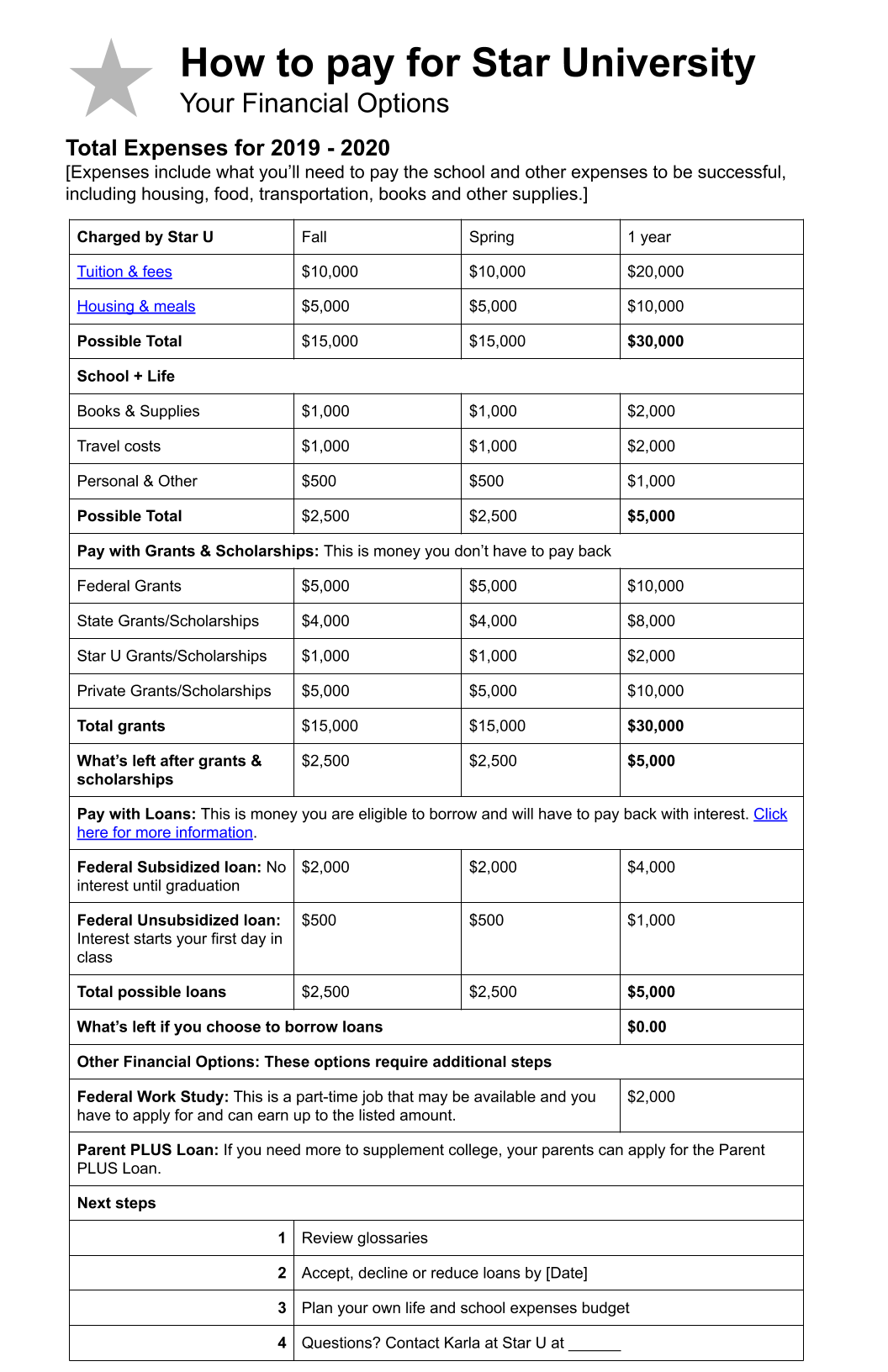

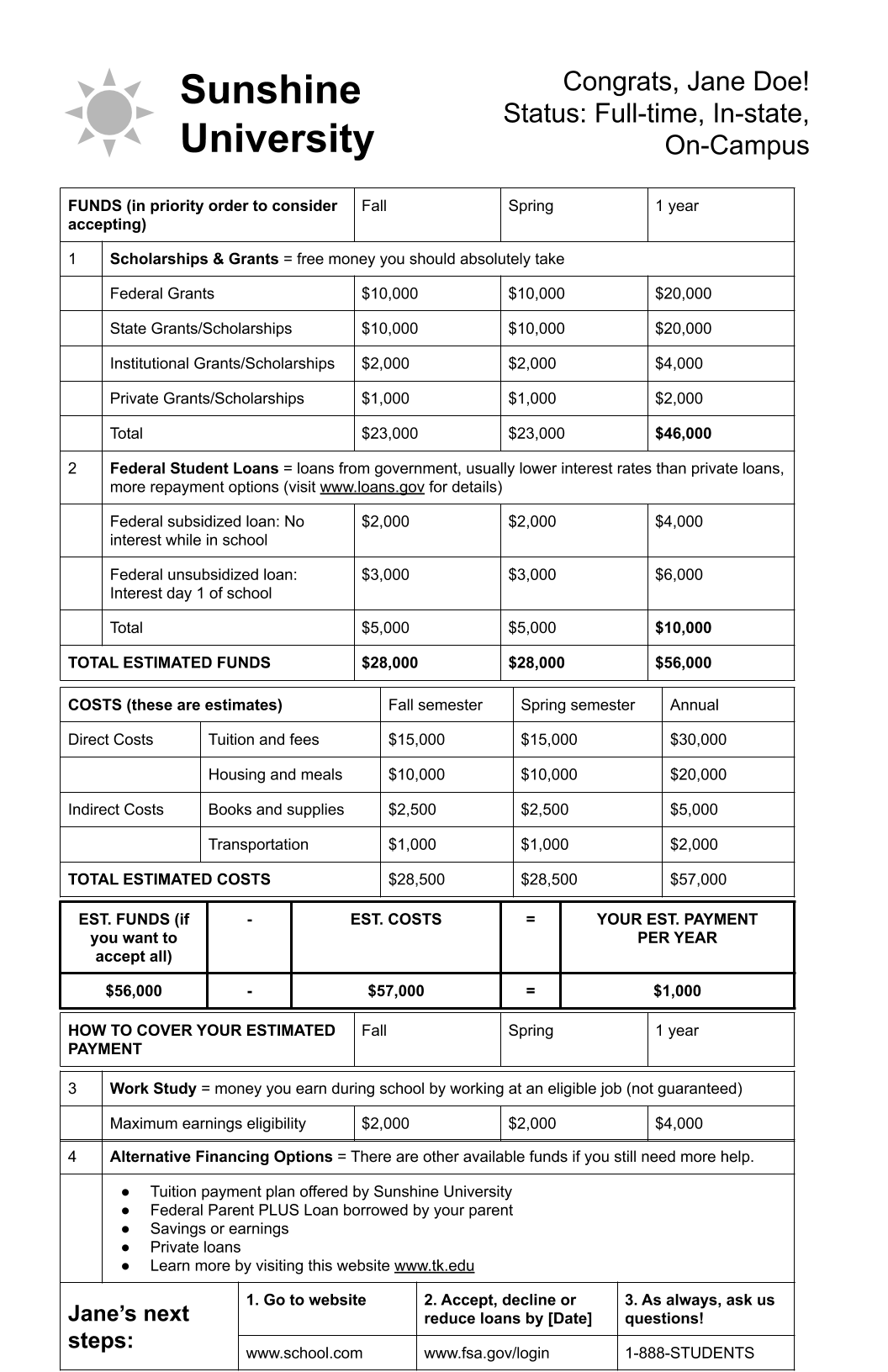

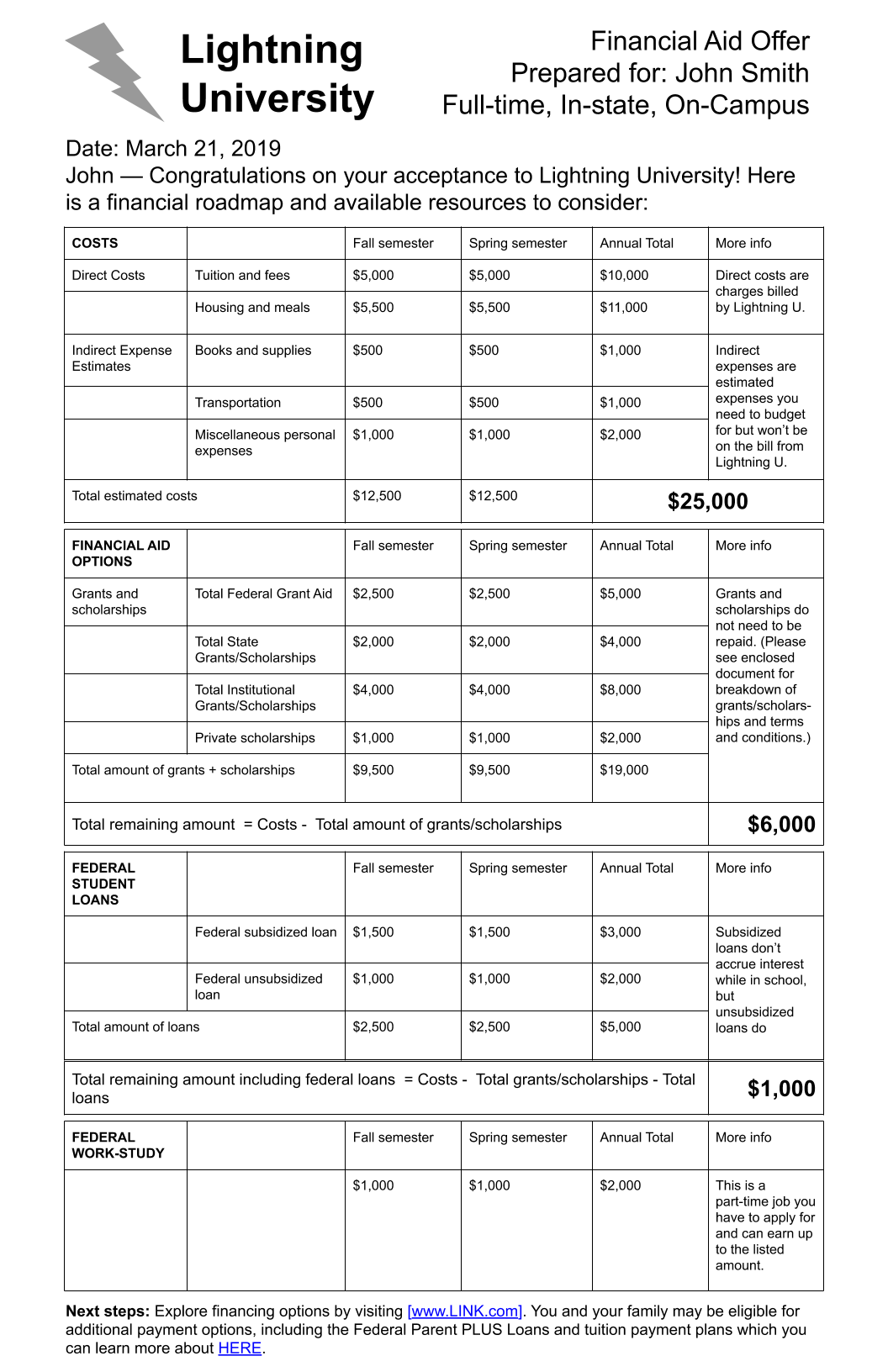

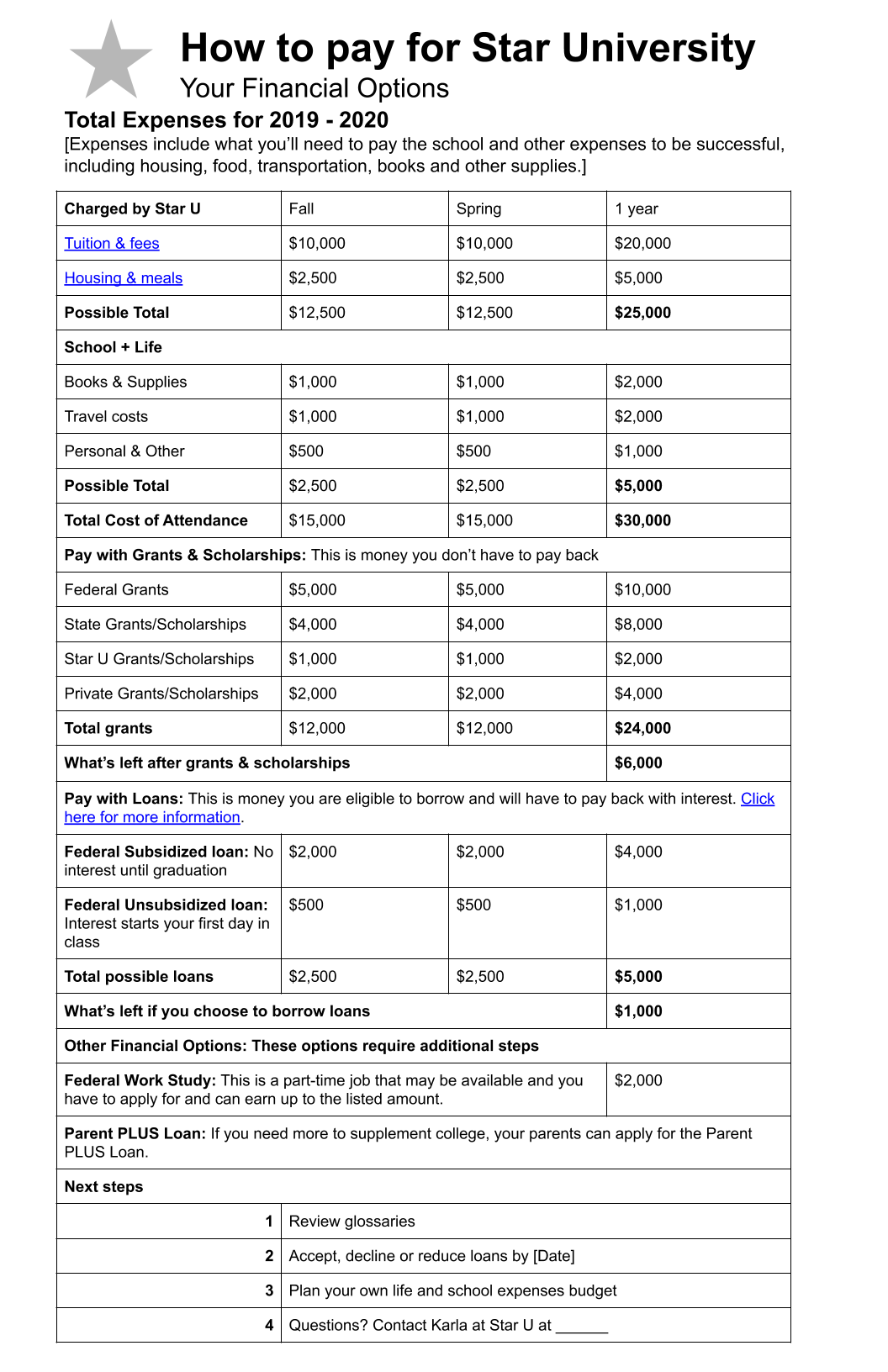

Guided by these ideas from the participants, Nguyen, our UX design expert, designed three prototypes for the made-up Star, Sunshine, and Lightning Universities. Each of the three prototypes had five components: college costs, financial aid (including grants and loans), net price (full cost of attendance subtracting grants and scholarships), remaining cost to the student after loans are included, alternative financing options, and the next steps a student must take to accept the award. Each prototype listed the student’s name and enrollment status, provided some definitions of the terminology used, and listed Parent PLUS loans and work study as alternative financing options, rather than misleadingly packaging them into the aid offer. However, each of the three prototypes also had some distinct features.

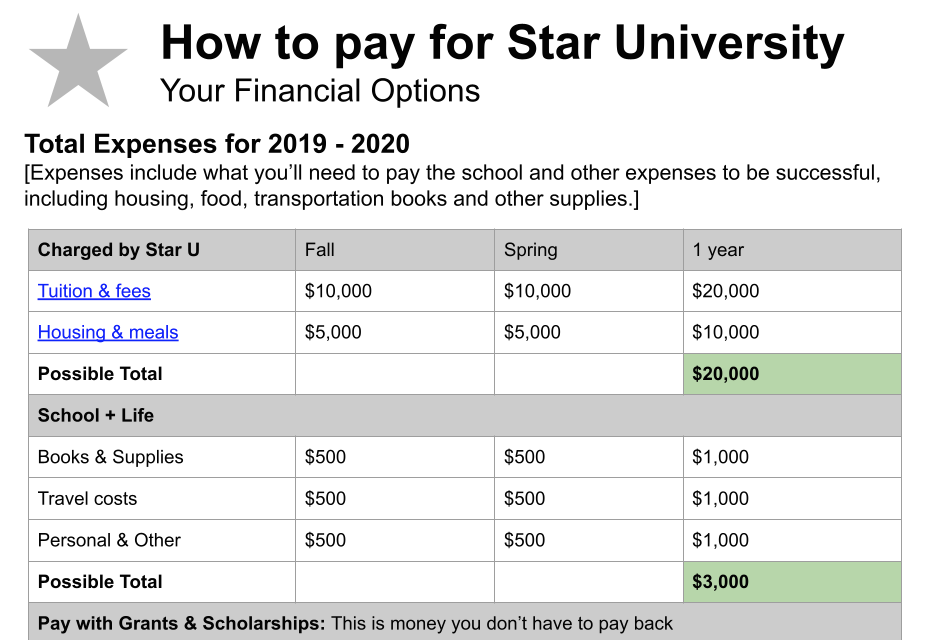

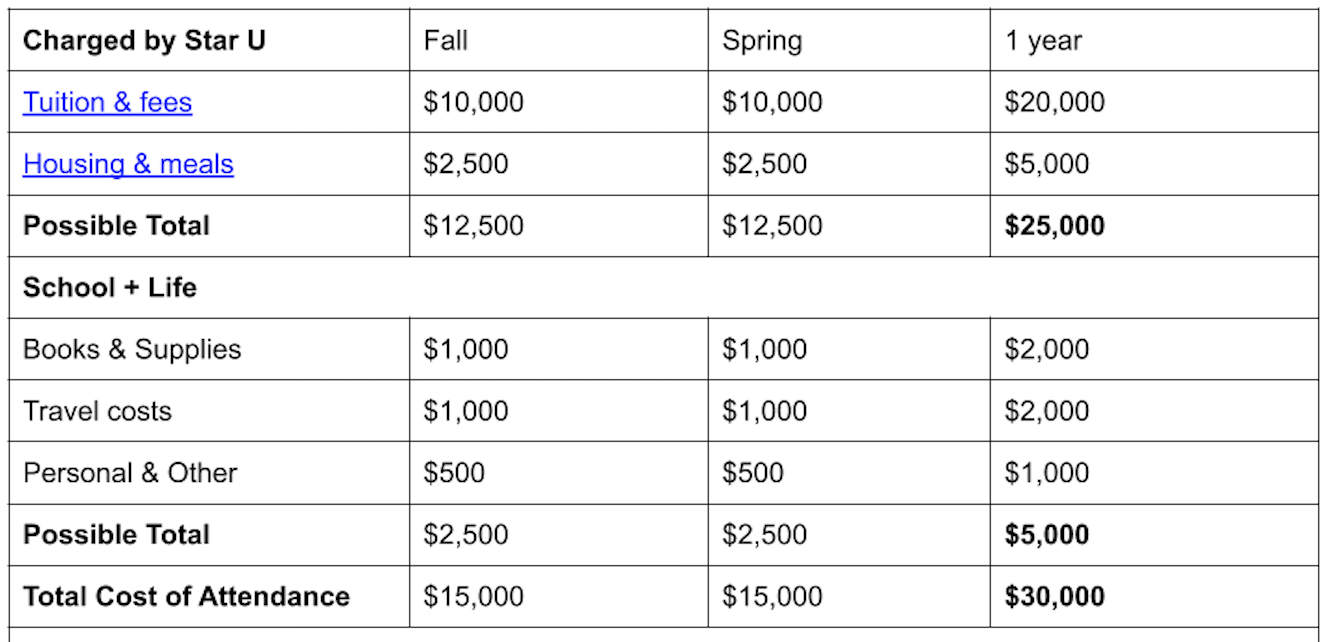

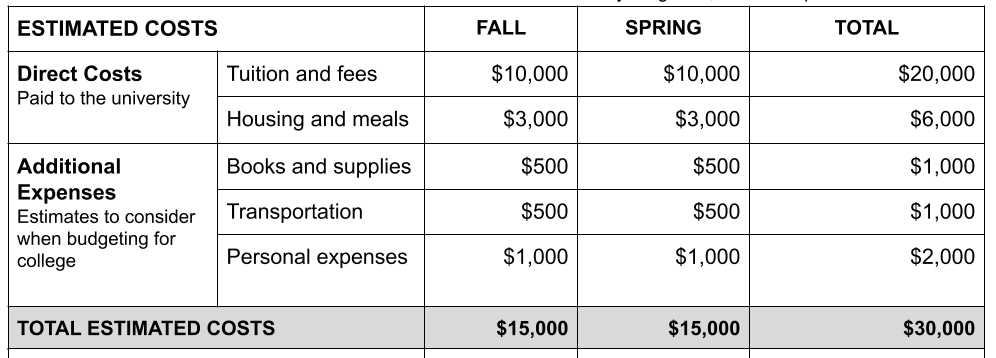

Star University used the most plain language to describe financial aid terms. For example, it titled the offer “How to Pay for Star University” instead of “Financial Aid Offer.” It used “charged by Star U” instead of “direct costs,” and “school + life” instead of “indirect expenses.” Star placed costs first, followed by grants and loans, and then calculated the net price right after presenting the grant information. It presented the estimated bill right after the loan information.

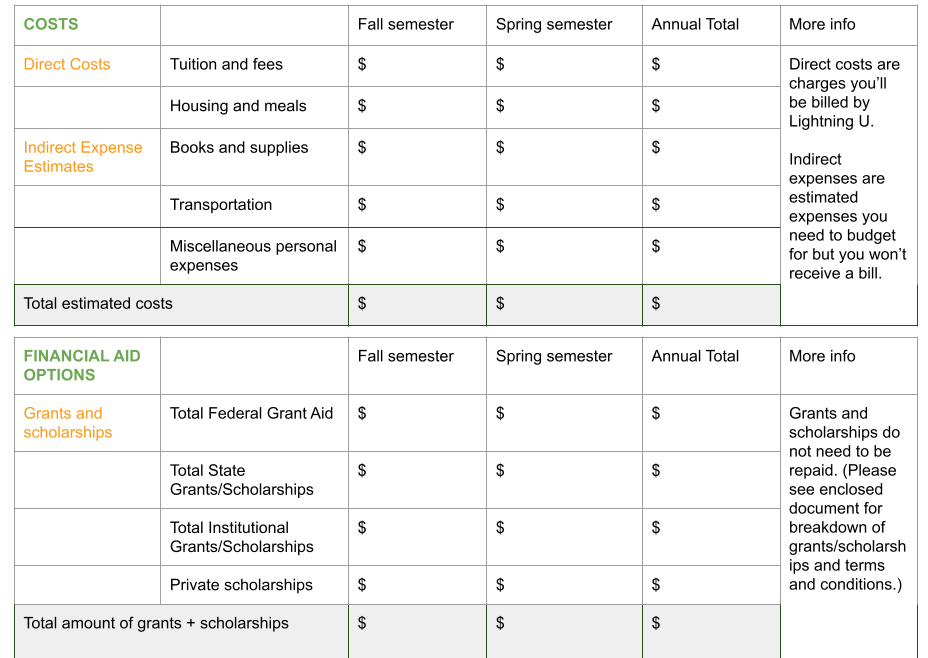

Lightning University took a similar approach in terms of the order in which it presented the information. However, Lightning kept most of the technical terms as used by colleges and universities. But it added an explanation column to provide definitions of the terms.

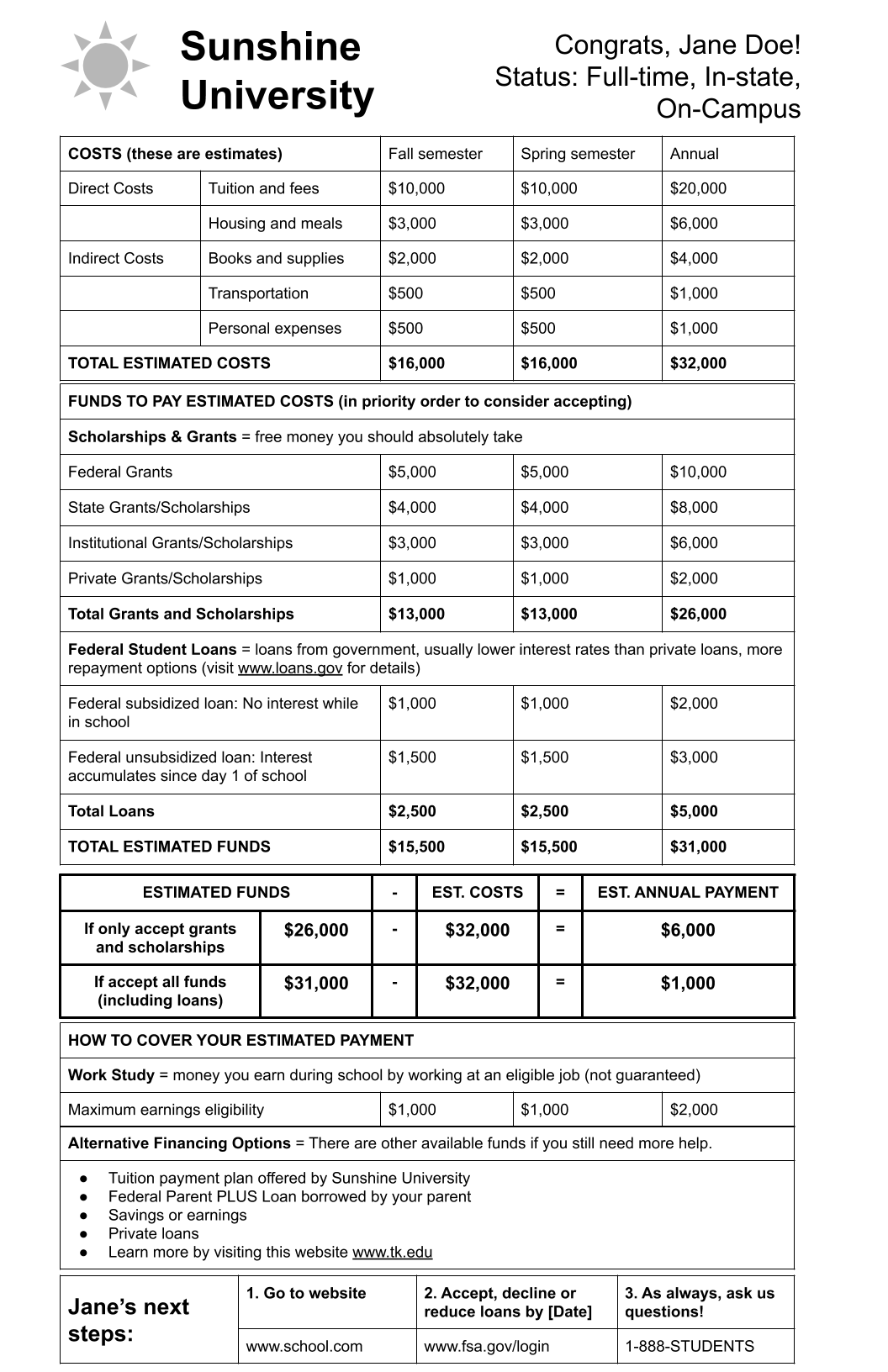

Sunshine University tried a different approach, displaying the grant and loan offers first, before breaking down the costs. Sunshine also featured a highlighted box which spells out the calculation of the remaining cost.

Once we had the three prototypes, we moved into usability testing. We conducted the user-research in order to understand the shortcomings of the prototypes and how to improve them so they could be used by all types of users, from high school students, to parents, to non-traditionally aged students.

Citations

- Rachel Fishman and Sophie Nguyen, “Financial Aid Offerpalooza,” EdCentral (blog), New America, August 5, 2019, source

- Fishman and Nguyen, “Financial Aid Offerpalooza.”

- Fishman and Nguyen, “Financial Aid Offerpalooza.”

Usability Testing

People tend to be very opinionated about the design of financial aid offers. Certain design choices, like font size, type, and color, can completely distract from the contents of the package and derail conversations about what works when formatting and designing offers. To avoid these issues during the usability testing, we created prototypes that all used the same font and only two colors, black and white.

This is also the reason why we created a set of criteria—known as “success criteria”—to determine whether students and parents could navigate and understand the offers during our usability testing.

The Success Criteria

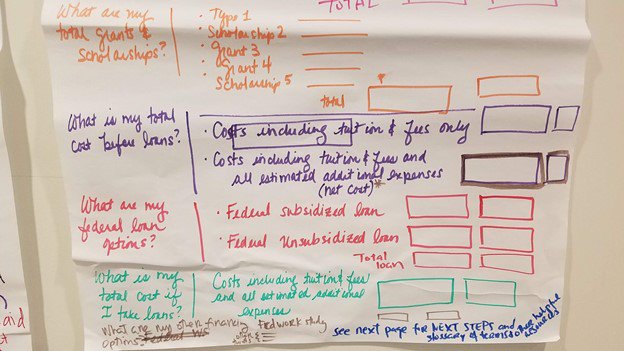

Our success criteria are rooted in our findings from Decoding the Cost of College and our focus groups. In order to successfully navigate financial aid offers, students and parents must be able to:

- Understand the differences in financial aid packages, including:

a. Grants and scholarships they will receive

b. The amount of federal student loans they can borrow

c. How much Federal Work-Study they are eligible to receive - Understand the full cost of attendance, including:

a. Direct costs such as tuition and fees

b. Indirect estimated expenses such as off-campus living and books and supplies - Understand the concept of “net price” or the cost after grants and scholarships are taken into account, and successfully apply loans to the remainder

- Understand the availability of other financial resources and alternative payment schedules (such as wages, savings, tuition payment plans, federal Parent PLUS loans) that they can use to pay remaining balances

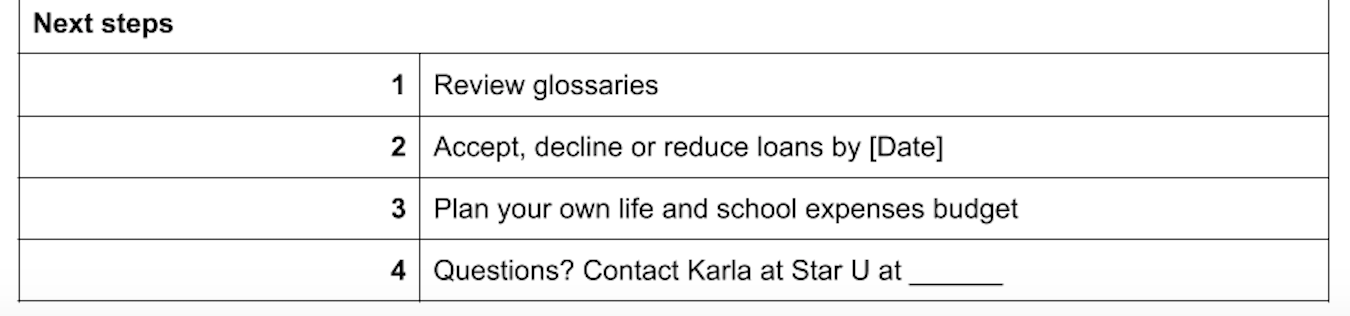

- Understand next steps for accepting, reducing, or declining any types of aid, and how to contact the school for more information or clarification

To compare the three prototypes, we hired an expert, Ann Duffet from FDR Research, to conduct interviews with students (both traditionally aged, and non-traditionally aged) and parents of traditionally aged students.

Duffet conducted one-hour interviews starting in November 2019, with two testing sessions conducted in Atlanta and Boston, comparing New America’s prototypes within the interviews. Thirteen people were interviewed: six parents, five traditionally aged students, and two non-traditionally aged students. (Please see methodology in Appendix A.)

Results of Phase One Interviews

First, the good news: most of the participants were able to make accurate calculations about price. They were able to identify and correctly sum scholarships and grants, how much they could borrow in federal student loans since they were already separated from grants and scholarships on our offers, and any work study money they were eligible to earn. They were able to, for the most part, distinguish the differences in these types of aid, although some still needed more prompts from the facilitator to arrive at the right answer, and it is important to recognize that many students and families have to navigate the financial aid offer process on their own with little to no outside help.

Participants valued cost information the most and wanted to see it first. Although they identified which costs were direct and indirect, based on the information given on the offers, they disagreed on what cost items should be included (especially for indirect costs). Many cared more about the direct costs and did not want to see indirect costs because, they argued, those are the costs that would occur anyway and are not as meaningful. One participant objected to Star University’s use of the phrase “possible total,” saying, “I would just say total…they can do an asterisk next to housing and meals, because these are choices people make. Possible sounds ridiculous.”

Although some participants did not think including indirect costs was necessary, they agreed that having the estimates on the offer was helpful. Some participants did not like the terms “direct” and “indirect” cost. One suggested calling it “mandatory” and “additional costs.” Some liked the way the Star University prototype, calling them “Charged by Star U” and “School + Life.”

None of the participants seemed to have any trouble with having two cost calculations: one that just applies grants, and another that applies both grants and loans.

Participants were able to tell which financing options were available to them. They seemed to understand what work study was, although it was unclear whether they knew it from their own experience or learned of it from the explanatory text provided.

Participants were also able to tell us what they needed to do next. One caveat is that participants who seemed experienced with the financial aid process tended to answer the next step question using their previous knowledge, not necessarily the information provided on the offer. When asked again to look at the next steps section, they agreed that the information was sufficient. Most preferred how Star and Sunshine presented next steps, both of which listed necessary actions that students and parents should take.

During the conversations, participants also told us the features they liked and did not like about each prototype that went beyond our success criteria. Although most were personal and different for each participant, one thing that most participants seemed to agree on was the order in which the different categories in the letter were listed. Our participants liked to see cost first, followed by grants and scholarships, and then student loans, alternative financing options, and finally next steps. Many liked having the net price calculation in a bold box like the Sunshine prototype, but a handful wanted to see an additional remaining cost calculation after grants/scholarships and loans were applied to the total cost of attendance.

After two testing sessions, most participants voted Sunshine as the financial aid offer that was easiest for them to navigate (6 votes), followed by Lightning (4 votes), and finally Star (3 votes). Most who voted for Sunshine highlighted the remaining cost calculation box and the layout of next steps at the bottom of the page as being particularly helpful. For those who voted for Lightning, they liked how the offer broke down cost and aid in detail, presenting them in a consistent format throughout the letter. For those who voted for Star, the reasons varied: most notably, one participant liked how it separated the total of direct and indirect costs.

Interestingly, at the interview sessions in Atlanta, Sunshine seemed to receive the most negative feedback. Participants did not like that Sunshine’s offer started with grants and scholarships, and that the different boxes on Sunshine did not align with each other, making it confusing to read. For that reason, we moved the cost section up and fixed the column misalignment after the Atlanta testing. As a result, Sunshine really stood out among participants in Boston. One participant remarked, “this one…by far, blows everything away.” Many participants especially liked the cost calculation box, which put two cost calculations in a bold box on the offer.1

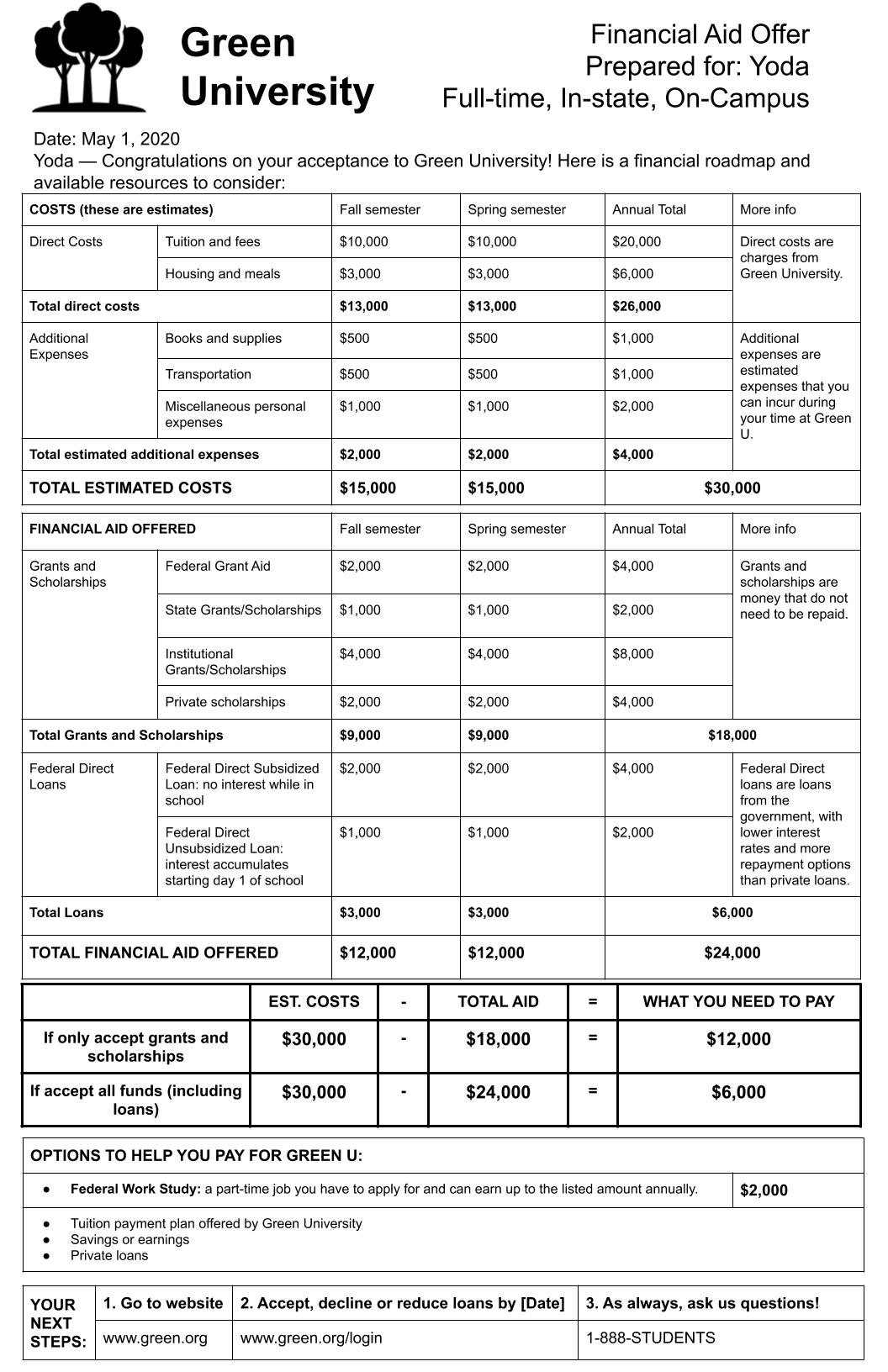

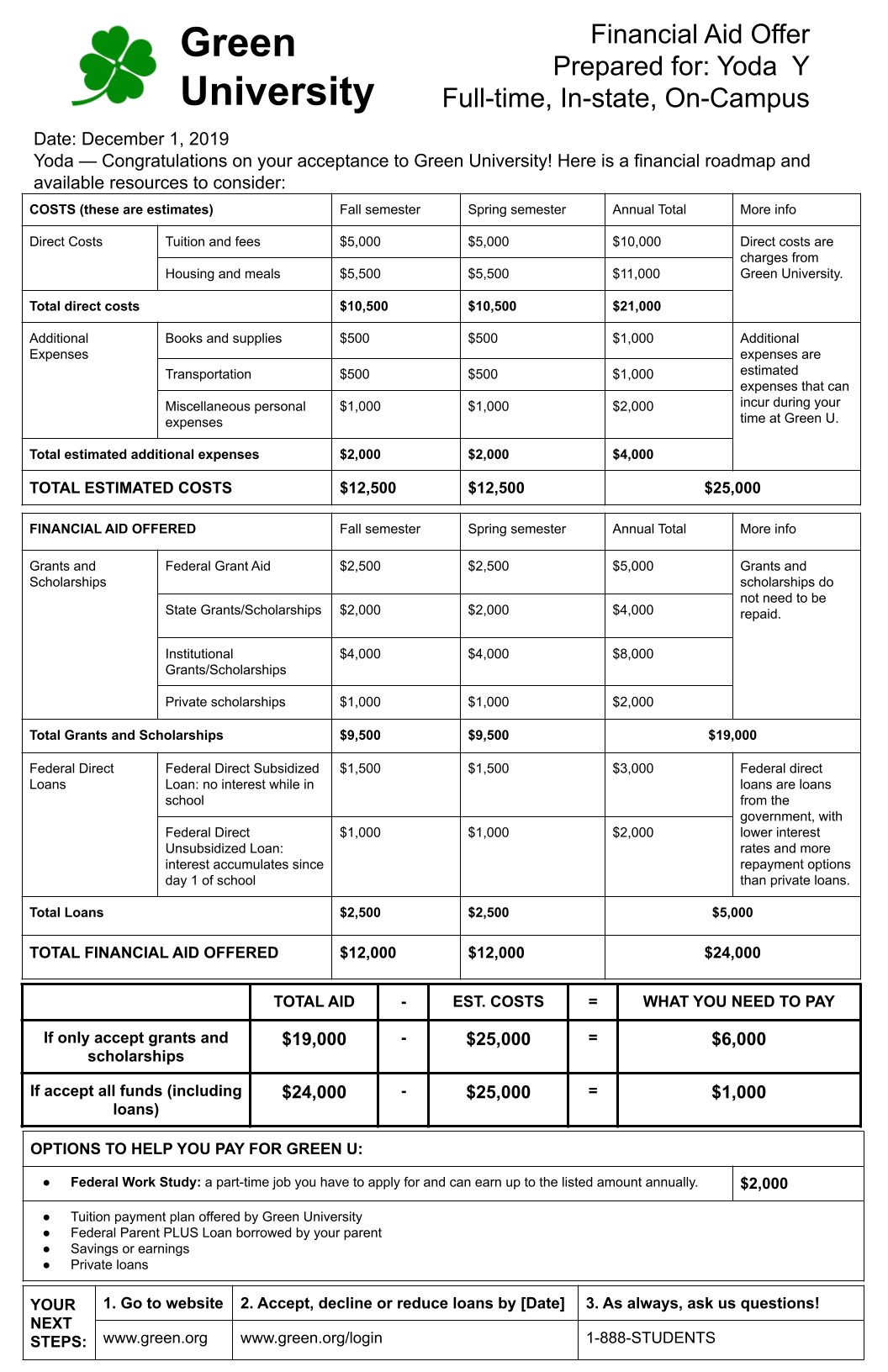

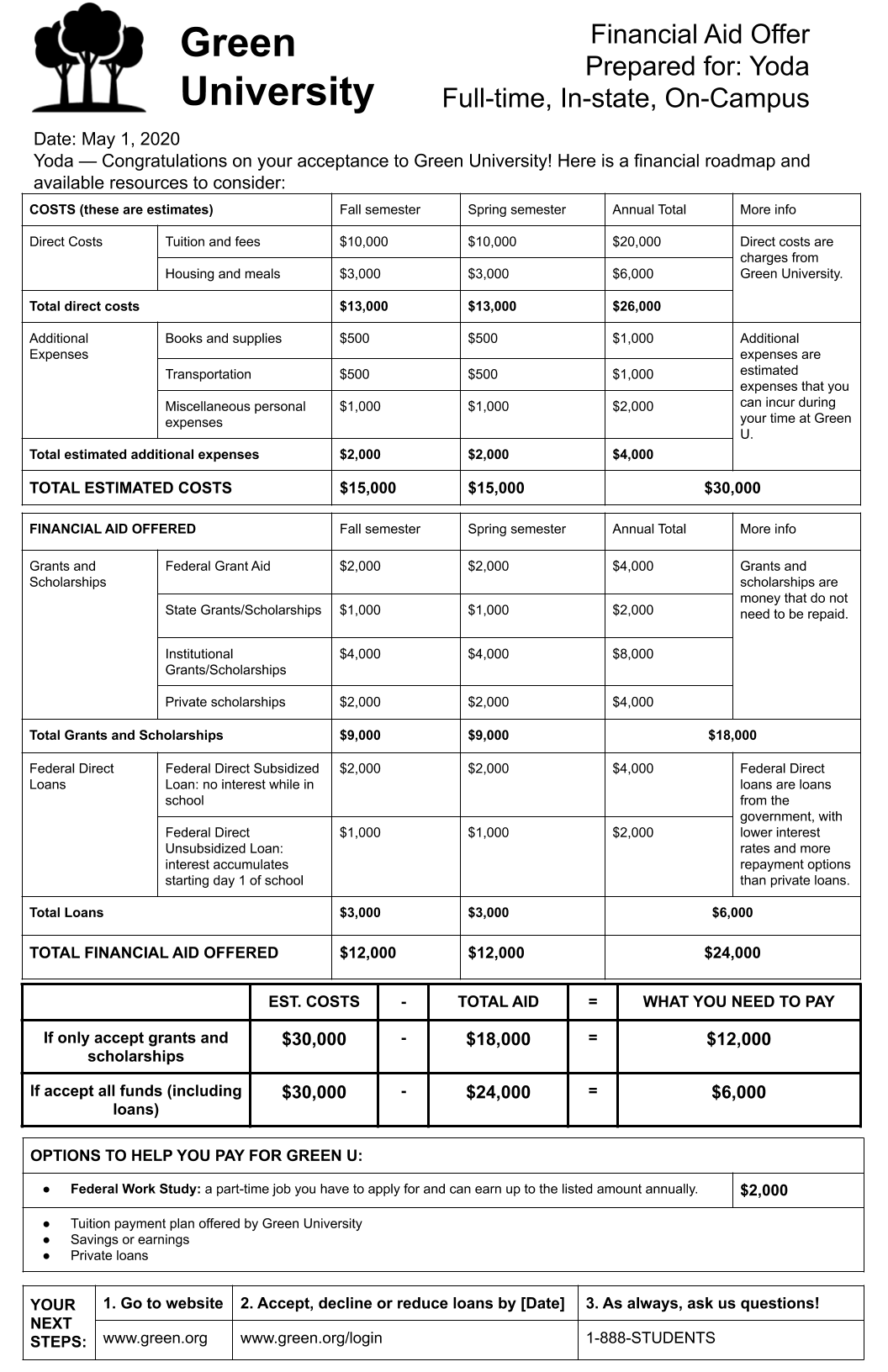

Based on feedback from our participants, we combined elements of participants’ favorite parts of Lightning and Sunshine. This prototype, which we named Green University, starts with cost information, followed by grants/scholarships, and then loans. This first section resembles the first half of Lightning. The next section—the remaining cost calculation, alternative options, and next steps—are taken from Sunshine.

Phase Two: Honing What Works

After completing our phase one research, we embarked on a second round of consumer testing to tease out what really worked well with our Green prototype, and what still fell flat. This time, we wanted to focus on “uninitiated” users, those who have likely never seen a financial aid offer before. In our phase one testing it was clear that some participants were relying on information and knowledge from their own memory. This time, we wanted to get feedback from high school sophomores and juniors, their parents, and non-traditionally aged students on the cusp of enrolling in college.

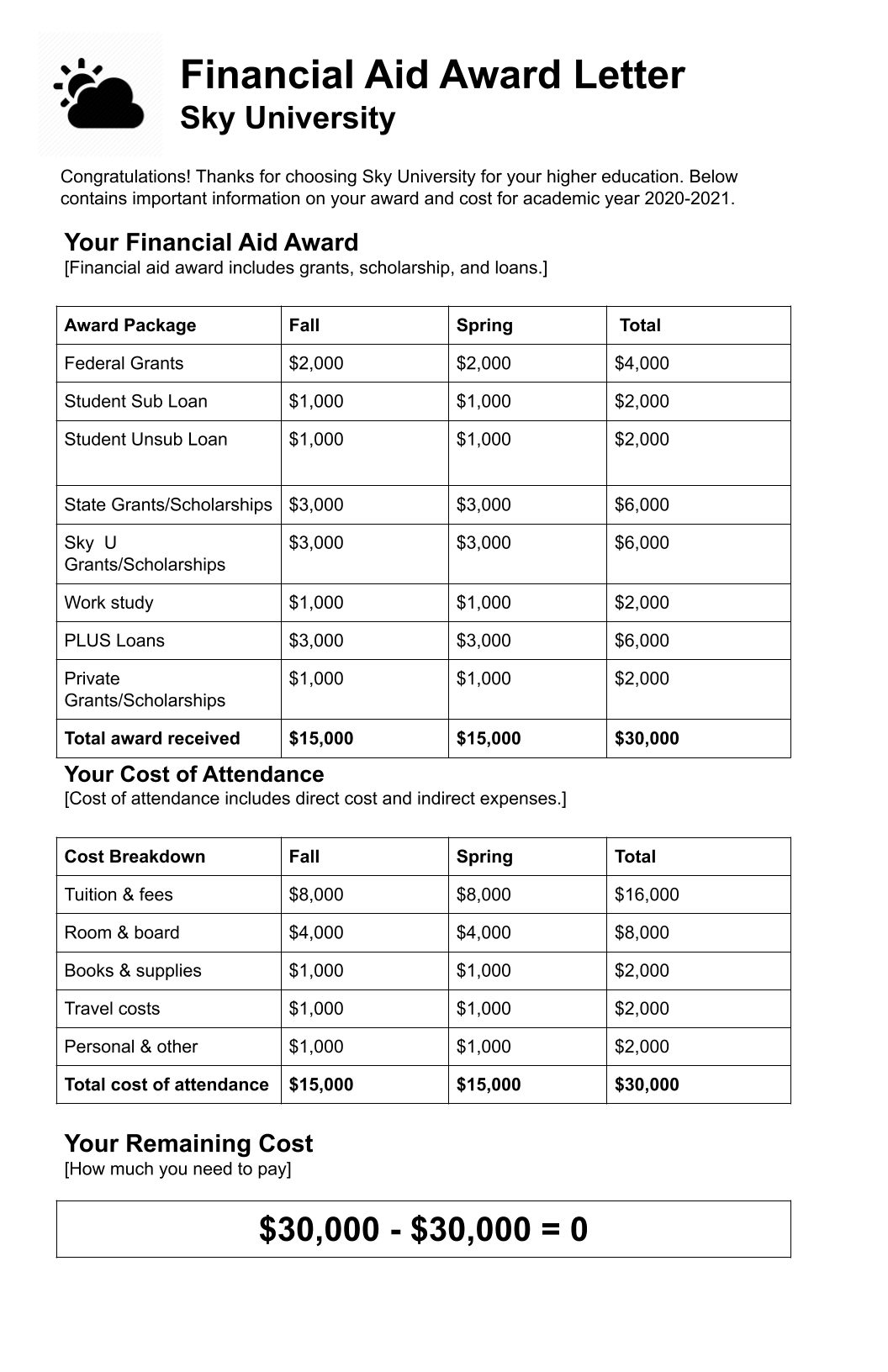

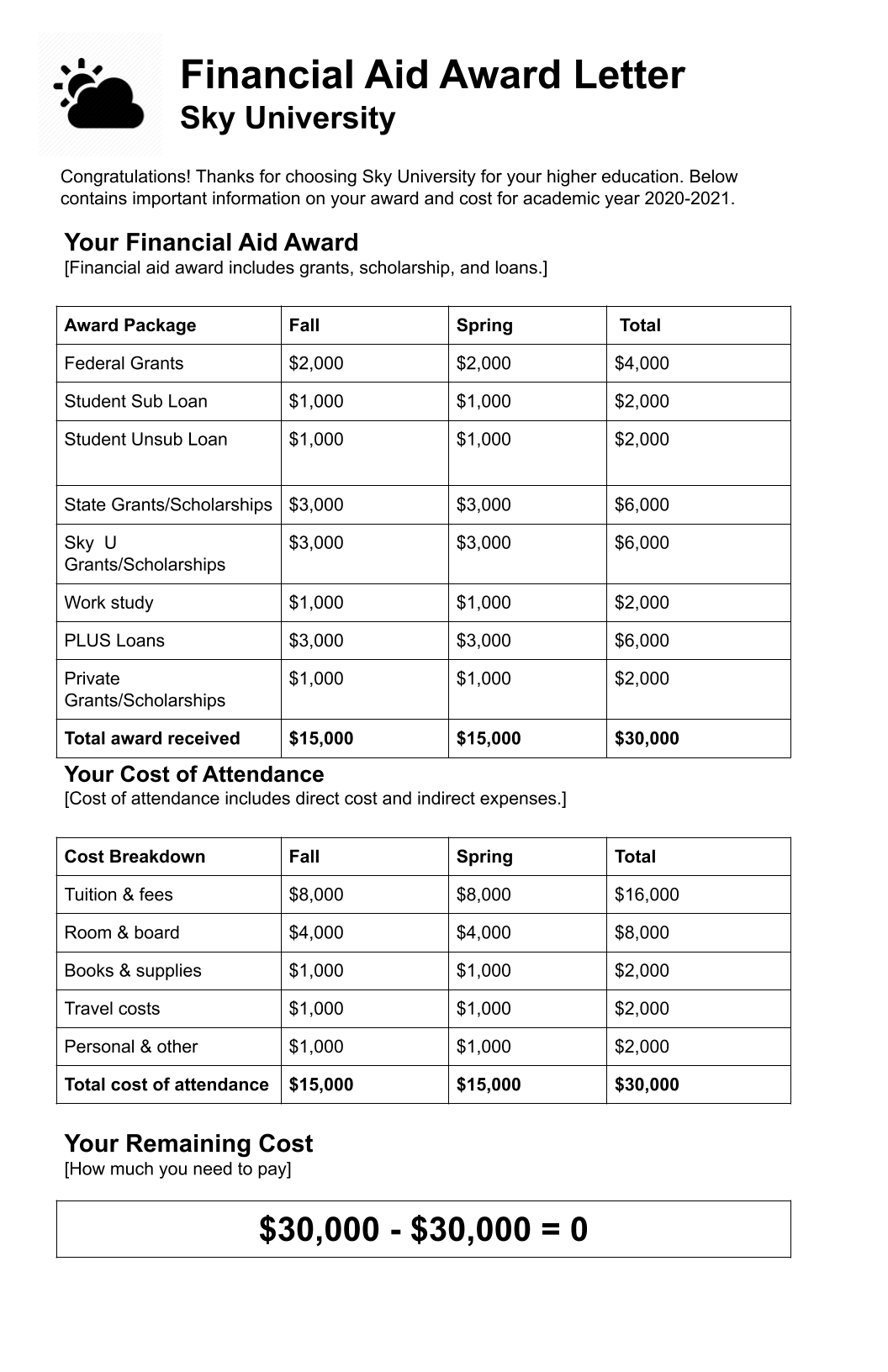

We also created a new prototype—Sky University—that combined many elements of a middling financial aid offer from our Decoding the Cost of College report. This was done in an effort to tease out what set our redesigned offer apart. Because all of the prototypes in our first phase met the success criteria, we wanted to understand how our redesign performed against an offer a student might receive currently.

Like everything about 2020, the second phase of our research was upended due to the COVID-19 pandemic. Initially, we had hoped to conduct in-person interviews over the summer. As it became clearer that the pandemic would make it unsafe to meet in person, we explored virtual options. Ultimately, we conducted 22 interviews via Zoom with our facilitator and New America representatives observing. (Please see Appendix B for methodology.)

We started by showing two prototypes in random succession: Sky (our middling offer) and Green (our “best practices” prototype). In effect, the comparison to Sky allowed participants to discuss the benefits of Green as they worked to answer our questions and do the math. Most participants struggled to navigate Sky, finding the offer disorganized and missing key information. In comparison, the details on Green resulted in everyone being able to meet the success criteria. “If you like things broken down, [Green] is a great document because it has got the direct costs, what additional expenses are,” one adult prospective student said. “This is very detailed.”

Notably, participants continued to struggle, as they did in phase one, with the concept of “additional expenses” or indirect costs. While participants understood that these costs were estimates from the institution, they were unclear how representative these estimates would be for their own personal situation. Some were not sure that including them was even necessary. One parent said, “I don’t even need money for these indirect expenses. I’m looking at it as $30,000, but there’s things on there that they always include that aren’t technically expenses; they are not fixed expenses, I should say.” This parent figured, “so it’s $30,000, but there’s $12,000 that could be adjusted like room and board if [my son] decides not to stay on campus.”

While participants understood the differences between loans and grants, some expressed appreciation for the explanatory text in the “More info” box. When it came to loans, participants struggled, especially with Sky University, to articulate the difference between subsidized and unsubsidized loans. For this reason, it will be important when designing a standardized letter to keep some sort of brief explanation, as seen with Green University.

With Sky University, Parent PLUS loans and work study were combined with grants and scholarships as part of the aid package. Once participants navigated both Sky and Green, they preferred Green’s presentation with work study and Parent PLUS loan being placed under “Options to help you pay for Green U” since they are not guaranteed aid. A parent has to apply and be approved for a PLUS loan and a student has to find a work study-eligible job and work a specified number of hours each week in order to receive the funding.

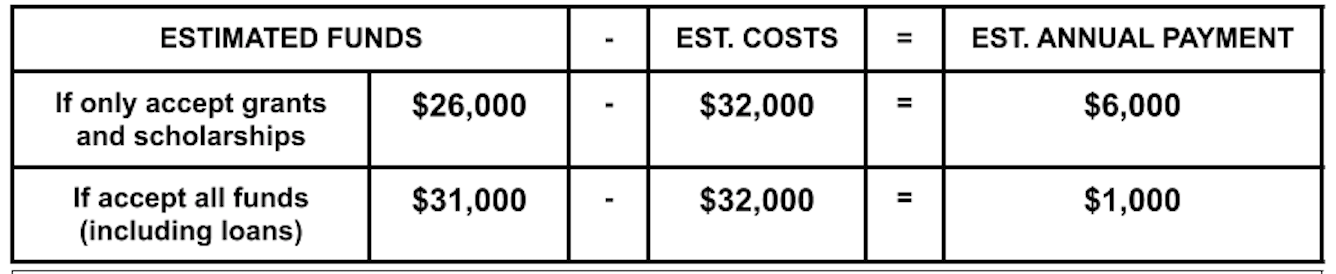

One of the biggest criticisms from participants about Sky came over how the offer “did the math” compared with Green. Sky’s offer lumped all aid together (including grants, student loans, work study, and PLUS loans) and subtracted the total from the cost of attendance, indicating that the student had $0 left to pay. Several participants said that this calculation made the offer misleading. “There probably is a subcategory of people who would more quickly gravitate toward Sky because [the $0] makes them feel confident in their ability to afford the school,” said one participant, “whereas Green is going to give them a more accurate presentation and is more ethically responsible than Sky.”

In the end, when it came to Sky University, the participants initially liked the simplicity but when they reflected on both offers side by side, believed that the extra information provided on Green gave it a sense of legitimacy and gravitas. “It looks more professional,” commented one high school student. Said another adult prospective student, “I can already tell Green is going to be more of a distinguished school by the layout of their document.”

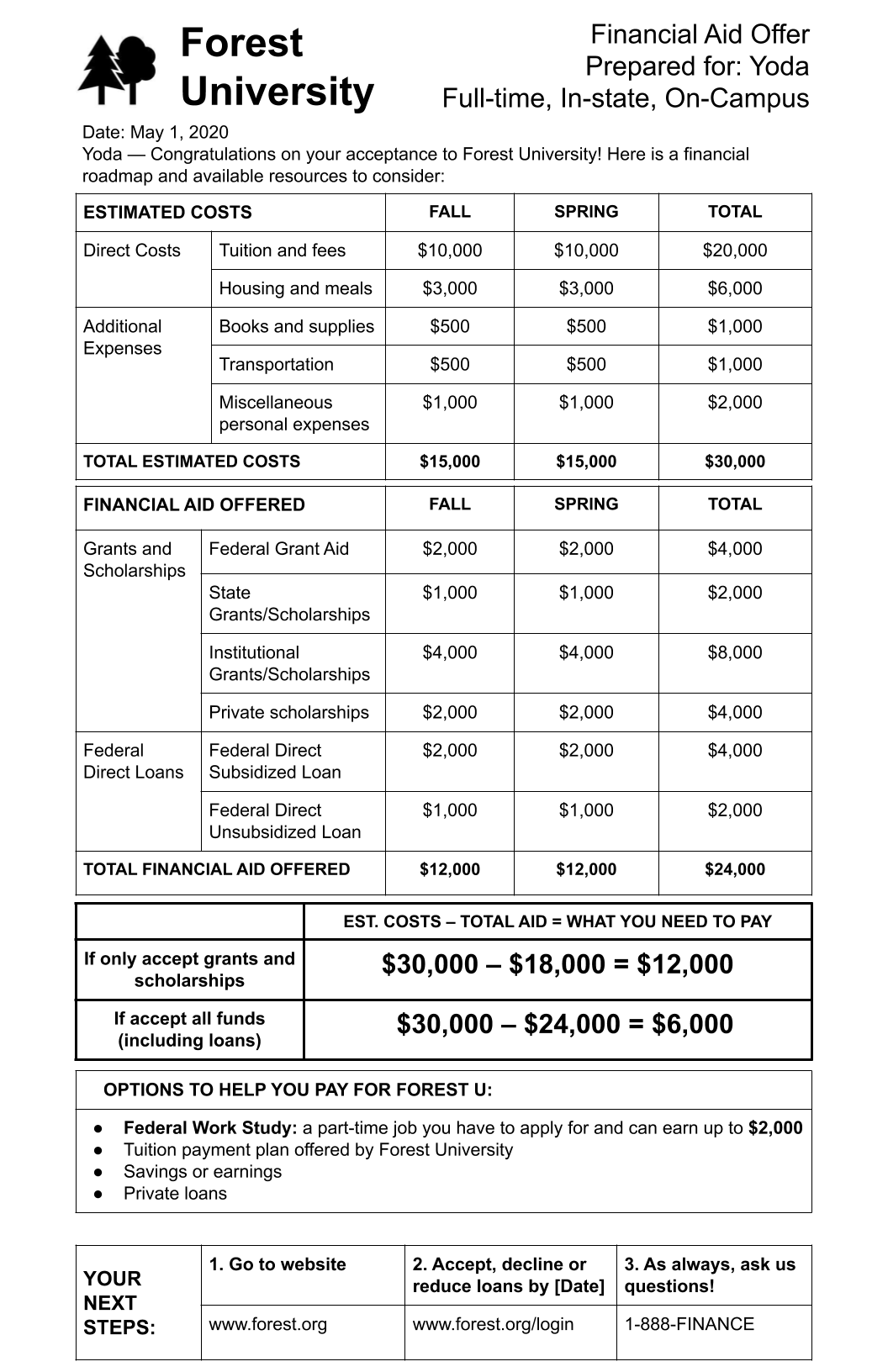

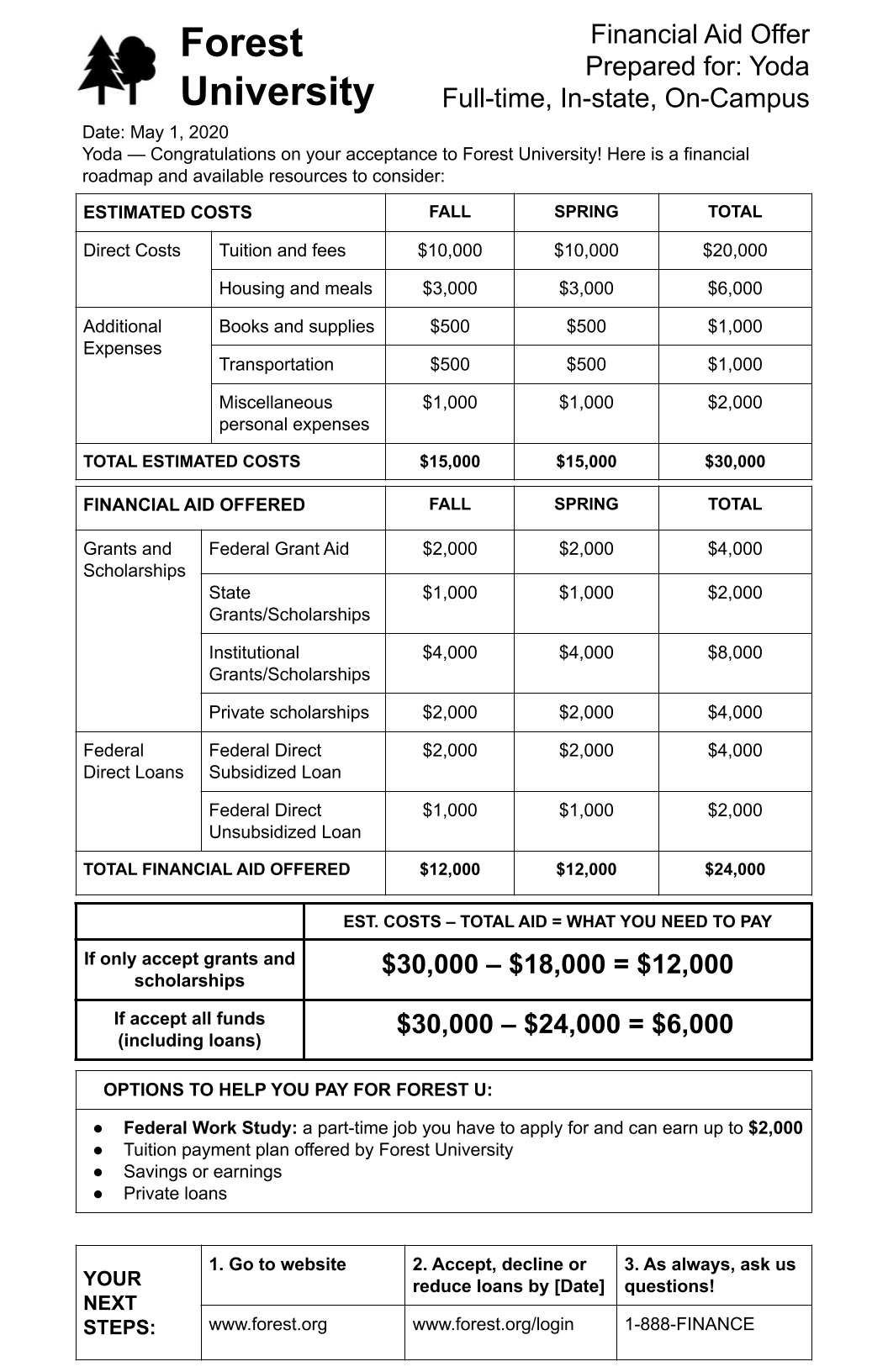

At the halfway point (after the 11th interview) it became clear that while Green was the preferred version in terms of order and clarity of information, it was perceived as “cluttered,” “busy,” and “overwhelming.” Participants almost unanimously wanted more white space and a larger font. “I don’t like this setup because it is not straightforward to me,” said one parent participant, since “I want to glance at it and see what’s what.”

In response to these complaints, we created a third prototype, Forest University, which was a simpler version of Green. In 9 of the remaining 11 interviews, all three prototypes were shown. Green continued to be the preferred version, mainly because it was the only one that included the “More Info” column, explaining the various elements that make up the offer. It was evident that although many participants said they did not carefully read the explanations in the “More Info” section, they wanted to keep the explanations. Said one high school student, “I just liked how everything’s categorized [on Green]. And they had explanations on the side, which I noticed the other two don’t. So it’s a little bit more helpful, easier to navigate, not just for me, but for lots of people.”

Citations

- The evolution of the documents, including summary notes about how the offers changed throughout the user testing, is shown in Appendix C.

Discussion and Recommendations

For years, New America has advocated for better and more transparent financial aid offers so students and families understand how much financial aid they will receive, how much they will have to pay right now, and how much they will have to pay back through loans. Now, with a serious and long-lasting economic downturn due to the coronavirus pandemic, these communications will be even more crucial for understanding which college is the best financial fit for a family.

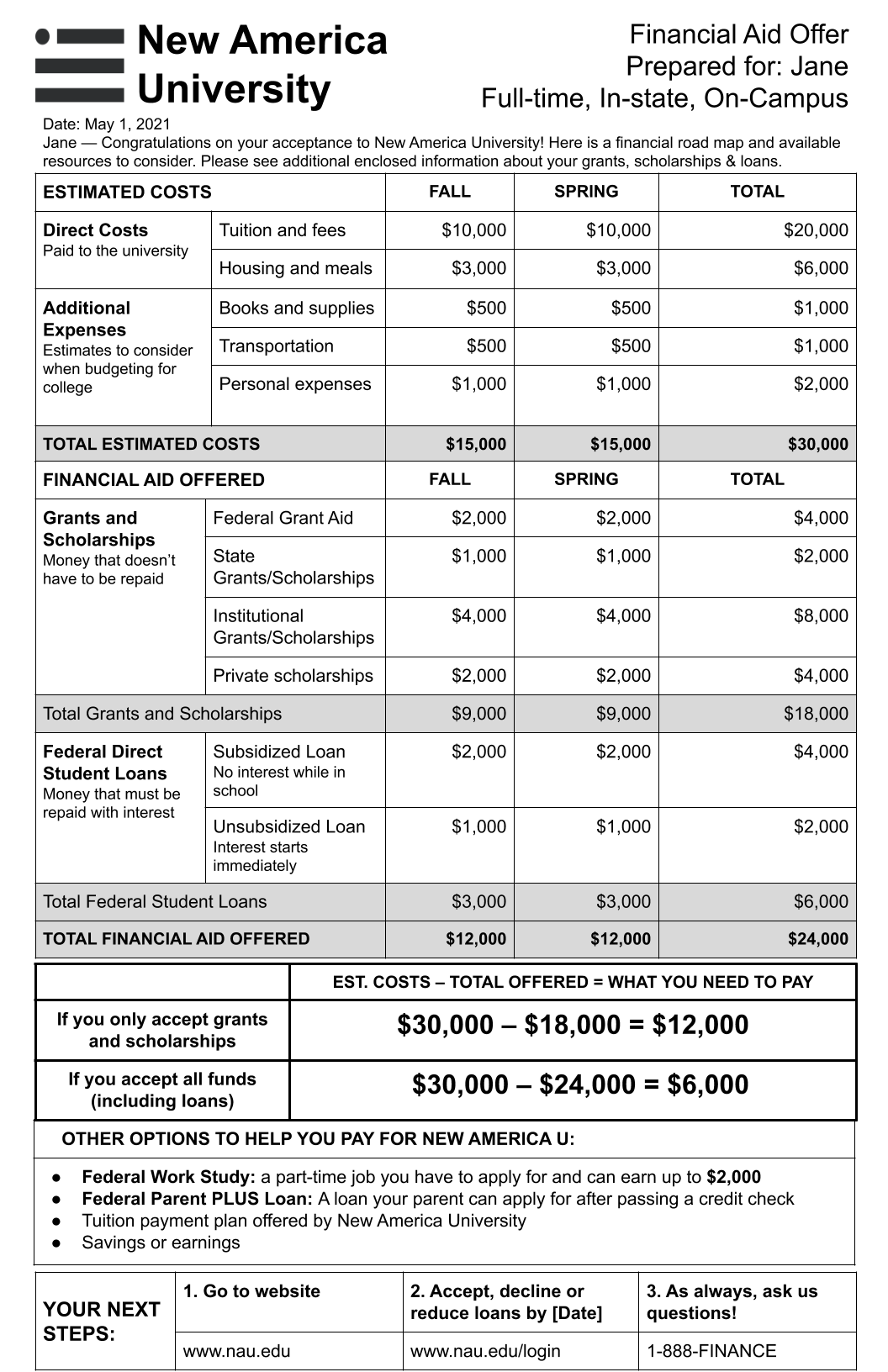

In concert with Decoding the Cost of College, this user research on financial aid offers can help determine some of the best methods and formats for communicating price and financial aid. Based on the research, we created one final prototype, New America University, which reflects all that we learned from our initial focus groups, our Financial Aid Offerpalooza, and the two rounds of consumer testing. This prototype is meant to be an example of how information can be clearly communicated so that students and families can understand the information correctly on their own.

A financial aid offer must contain all the following information:

- Price, including indirect expense estimates

- Financial aid offered, with distinctions made between grants/scholarships and federal student loans

- Mathematical calculations that present what students and their families will ultimately need to pay

- Other financing options to help students and families pay off any remainder

- Next steps they have to take to receive, reduce, or decline the aid

The offer should also indicate who the financial aid is for, since we found that students and parents liked the personalization, and whether the package was calculated based on the student being full- or part-time, in-state or out-of-state for public schools, and living on or off campus.

Information on full cost of attendance should come first. Our research revealed that students are most interested in seeing price information first, and then aid. Although there was some confusion among participants about indirect costs and whether they should be included in the offer, it will still be important to present this information since it is part of the federally defined cost of attendance. Instead, we believe indirect costs should be renamed “additional expenses,” with a simple explanation such as “estimates to consider when budgeting for college” beneath. We also think it is important to rename “room and board” because “housing and meals” will be more clear.

After presenting the full cost of attendance, grant and scholarship aid should be listed and totaled, and then federal student loans should be listed and totaled. We believe it is important to include a simple explanation of what grants and scholarships are, such as “money that does not need to be repaid.” There also needs to be a brief explanation of what loans are, and that explanation must also make clear the difference between subsidized and unsubsidized loans. Once loans and grants are totaled within their own respective sections, they should be added together to give students and families an idea of the overall financing available to them.

Financial aid offers must include a net price calculation and should also provide a calculation that includes both grants and loans. The federal definition of net price is the total cost of attendance, subtracting grants and scholarships. Since the net price calculation is not commonly known among students and parents, the offer must describe and present the calculation in very simple terms, taking the total presented in the first part of the letter, and subtracting grants and scholarships. Then a separate equation should clearly explain the subtraction of loans.

Once students and families understand the costs they have left to cover, it is important to provide them general information about other options they have for covering the remaining costs. This section of the offer is where information on Federal Work-Study and the federal Parent PLUS loan should be located. This section can also include other options such as savings and earnings, private loans, and tuition payment plans. Several participants in our phase two research particularly liked the idea of tuition payment plans, so institutions that offer them should communicate these plans in financial aid offers, if possible.

Every offer must include the next steps students and their families have to take and contact information if they have questions. What students must do to accept, decline, or reduce aid included in the offer must be spelled out, as well as the relevant dates by which they have to take these actions. Participants also liked having a phone number or email address so they knew who to call if they had any questions.

In designing financial aid offers, there is a tension between simplicity and the provision of more information. New America undertook this design process assuming the financial aid offer would be like a cover sheet. For this reason, the offer is presented to the student, Jane in this case, as a “road map” and includes the most salient information to meet our stated success criteria, with enough white space to make it legible. Our assumption is that more information will be provided to the student on the back of this sheet, through other documents accompanying the offer, or electronically through hyperlinks. For example, while the offer indicates the size of the institutional grant award, further information would have to be included to show the breakdown of institutional scholarships and their terms and conditions. Similarly, more information on federal student loans would be needed, including the interest rate that will be charged and repayment options.

Limitations and further research

Our research recreated how financial aid offers have been typically designed over the years: something that can be printed on a regular sheet of copier paper in black and white. Increasingly, however, these communications are delivered electronically via email, PDF, through student information systems (portals), or highly personalized software. One participant in our research mentioned he had received an electronic financial aid offer that had illustrated confetti pop out when he opened it. We still believe, and our focus groups backed this up, that families want to have both electronic and paper options. Though at a minimum, any financial aid offer should be optimized for mobile devices so that students and families can access it and read it anywhere and from any device.

In addition, we focused exclusively on financial aid offers for first-time undergraduate students. More research is needed on ways to present price and financial aid information to graduate students given the particularities of graduate school education financing (such as the federal Graduate PLUS loan and research/teaching assistantship stipends). More research is also needed on how offers should be designed for returning students. Another group of students that might require a different financial aid offer consists of returning students; they will already have familiarity with offers and might find data on their total indebtedness to date useful.

The role of state and federal policy in financial aid offers

Students who apply to multiple colleges and universities are not able to compare financial aid offers from different institutions effectively. Every institution currently designs its own financial aid offer and there are no standardized terms or formatting, so students and families cannot make apples to apples comparisons. This means that families often operate under misguided assumptions about which school is the best financial fit for them.

During phase two of our research, we asked prospective students and parents whether it would be helpful if financial aid offers were standardized or if colleges should have full control over how they present the information. Participants agreed that they want offers to follow a similar format to make comparison easier among schools but still allow some flexibility for a college to add its personality. One participant noted that the introduction at the top of a letter, for example, “gives you a little insight as to the culture of each individual school.” A few also pointed out that a similar format is important to prevent colleges and universities from making it seem like families would owe nothing, “just to make sure that colleges aren’t producing false information or misleading like Sky University,” as one participant cautioned.

To prevent misleading pricing information, some federal and state policymakers have been pushing to standardize financial aid offers so that all colleges and universities have to present their information within the same template. The State University of New York system, for example, is required to provide a standardized financial aid offer template—known as Smart Track—to all students at its 64 campuses.1 The U.S. Department of Education has also encouraged institutions to voluntarily adopt its College Financing Plan (formerly known as the Financial Aid Shopping Sheet, developed by the Obama administration) which is another standard template.2

Voluntary efforts only go so far, however. In order to ensure all students receive common financial aid offers, Congress should pass the bipartisan, bicameral Understanding the True Cost of College Act, which was first introduced in 2012 and was most recently re-introduced in 2019 by Senators Grassley (R-IA), Ernst (R-IA), and Smith (D-MN) and Representative Van Drew (R-NJ). This bill would require colleges and universities to provide a common financial aid offer to every accepted student who applies for financial aid. The measure would not preclude colleges from providing more information, as long as any additional information uses standard financial aid terminology. The common financial aid offer would be developed by stakeholders and would be rooted in user-centered design, similar to the user research we conducted for this report.

Students and parents should not need a Rosetta stone when navigating financial aid offers. Our research shows the information and formatting needed to successfully interpret a college’s price, the contents of its financial aid package, and what remains to be paid or repaid in the future. Being able to easily understand this information from one school, let alone compare that information between schools, would empower students and families to have conversations about what college or university is the right social, academic, and financial fit for their family.

Appendix A

The FDR Group convened a series of in-depth interviews (IDIs) with 13 people who had applied for financial aid. The IDIs took place in November 2019—7 in Atlanta (11/12/19) and 6 in Boston (11/16/19)—in professional focus group facilities.

Recruiting

Participants were carefully screened to verify their student or parent status and ensure that they had experience applying for financial aid. The IDIs included 5 traditionally aged students, 6 parents of traditionally aged students, and 2 non-traditionally aged students. The participants were mixed demographically: by race and ethnicity (4 African American, 2 Hispanic, 7 white); household income (2 less than $35,000, 2 more than $115,000, 9 in between); and gender (7 female, 6 male).

- Traditionally aged students (n=5): current students who entered college/technical school immediately after high school (4), or high school seniors who plan to attend college/ technical school in fall 2020 (1). Both groups had to have applied for financial aid.

- Parents of traditionally aged students (n=6): parents of young adults who are currently enrolled in a two-year or four-year college or a technical school and who have received financial aid (4). Also included were parents of high school seniors who have applied for financial aid for next year (2).

- Non-traditionally aged students (n=2): adults between 24 and 40 years old who are currently enrolled in a two-year or four-year college or a technical school, and who have received financial aid. This category of student did not go immediately to higher education after high school.

The IDIs were recruited by a professional organization and held in professional facilities. The potential participants were recruited using opt-in databases that include thousands of people who have signed up to participate in qualitative research projects (e.g., focus groups, IDIs). The databases grow by word of mouth, community outreach, and advertising.

Interviewing

The purpose of the IDIs were to get a better understanding of how potential recipients of financial aid offer letters responded to the prototypes; the intent was to use information culled from the IDIs to help design an offer letter that would ensure the best possible experience for end users.

Each interview consisted of a participant, an interviewer, and a note-taker. Participants were provided information about the purpose of the research and were assured of confidentiality. Then they were given three prototypes of financial aid offer letters in succession and asked a series of questions about each. Some questions were empirical and had right or wrong answers; others were subjective.

Changes were made to the prototypes prior to the Boston IDIs based on feedback from the interviews in Atlanta. The interviews were audio-recorded and averaged 45 minutes in length (range 38–55 minutes). All interviews were moderated by Ann M. Duffett, of the FDR Group in New York, NY.

Appendix B

The FDR Group conducted 22 virtual IDIs between August 13 and September 4, 2020. All IDIs took place via Zoom video call. The interviews were recorded and averaged 49 minutes in length (ranging from 38–60 minutes).

Recruiting

Participants were screened to verify their status in these categories:

- High school students (n=8): students starting 11th grade or 12th grade in the 2020–21 school year who are considering going on for higher education after high school.

- Parents of high school students (n=7): those whose oldest child is a high school sophomore, junior, or senior in the 2020–21 school year.

- Adults who are considering higher education (n=7): those between 20 and 45 years old who do not have a degree or certificate beyond high school but are open to going back to school. These are NOT the parents of any college-age students.

To the extent possible, we tried to include people who had little or no experience with financial aid offer letters. The participants were mixed demographically: by race and ethnicity (9 African American; 2 Asian; 2 Hispanic; 10 white); household income (5 less than $35K; 4 more than $115K; 13 in between); and gender (15 female; 7 male).

The participants were recruited by Schlesinger Associates, a recruiting firm with a national database of potential research subjects. The facility recruits potential participants using its own opt-in databases that include thousands of people who have signed up to participate in qualitative research projects (e.g., focus groups, interviews, product testing). The databases grow by word of mouth, community outreach, and advertising.

Interviewing

The IDIs were structured to focus on the user experience of reviewing a financial aid offer letter. Each participant was shown either two or three prototypes of financial aid offer letters, in succession; asked a series of questions about each; and then shown the prototypes side by side and asked to compare them. Some questions were empirical and had right or wrong answers; others were subjective. All interviews were moderated by Ann M. Duffett, of the FDR Group.

Interruptions were common—children and pets appeared on camera, telephones rang, technology glitches occurred. We accepted this as an unintended benefit of the virtual interview; it allowed for real-life interruptions in a way that an interview taking place in a focus group facility could not. In all cases, participants were able to turn their attention back to the document and re-focus.

There were some unintended negative consequences of the virtual interview approach as well. For example, participants using Chromebooks were unable to accept control of the mouse, so the interviewer had to do the scrolling and magnifying for them. Some were less comfortable using a device to view the prototypes than they would have been seeing them on paper. In some instances, participants were unable to view the full document due to small screen size. But people were mostly able to view the entirety of the documents via scrolling, if not always at one glance.

Appendix C

Prototypes as of 8/27/19 (after the convening)

Note: the grants/scholarships section in all prototypes presents the aggregated amounts of grants and scholarships based on their sources. Institutions can break down the specific grants/scholarships from each source, together with their own terms and conditions, on a separate document.

Prototypes as of 11/11/19 (for use in Atlanta Usability testing)

Summary of changes:

- Turned colored text into black and white

- Added dollar amounts for cost, grants and scholarships, loans, etc.

- Fixed typos, edited explanatory texts

Prototypes as of 11/14/19 (for use in Boston usability testing)

Summary of changes:

- Fixed the dollar amounts on each prototype so that each has $5,000 in loans and $1,000 in remaining cost

- Sunshine University: moved cost section up, before grants and scholarships; added personal expenses to direct costs; added net cost calculation.

Prototypes as of 12/01/19 (after consolidating feedback from usability testing)

Summary of changes:

- Cost and financial aid package sections taken from Lightning University

- Remaining cost calculation, other financing options, and next steps taken from Sunshine University

- Make explanatory text more precise

Prototypes as of 8/2020 (for use in the second round of in-depth interviews)

Summary of changes:

- Create prototypes of Sky University and Forest University to compare with that of Green University

More About the Authors

Rachel Fishman

Director, Higher Education

Sophie Nguyen

Senior Policy Manager, Higher Education