Table of Contents

Orange County, Florida

"At $15 an hour, there isn't a single apartment in the city of Orlando that you could live in." – Leader of Philanthropic Foundation in Florida1

Orange County is located in central Florida and is home to Orlando. Approximately 1.3 million residents live in Orange County. The presence of Disney World and Universal Studios makes Orange County a world-renowned tourist destination.

Approximately 40 percent of Orange County residents are non-Latinx, white and 33 percent are Latinx. Black residents account for 23 percent of the population of Orange County, followed by Asians, who make up 6 percent.

Since the start of the COVID-19 pandemic, Orange County has experienced roughly 88,700 cases and 804 deaths. Adding to the public health toll, the unemployment rate in Orange County was 8.1 percent as of November 2020, more than triple the 2.8 percent unemployment rate during the same time in the previous year. Housing insecurity was also acute; the Census Bureau’s Household Pulse Survey shows that 37 percent of residents surveyed in Florida expect to be evicted or foreclosed upon in the next two months.

When and Where Are People Losing Their Homes?

Overall Housing Loss: Residents in Orange County experienced housing loss at a rate of 2.1 percent between 2017 and 2019, meaning that each year one out of every 50 renters and homeowners with a mortgage lost their home. This rate was the lowest of all the counties we studied, however the average masks pockets of Orange County that experience acute housing insecurity.

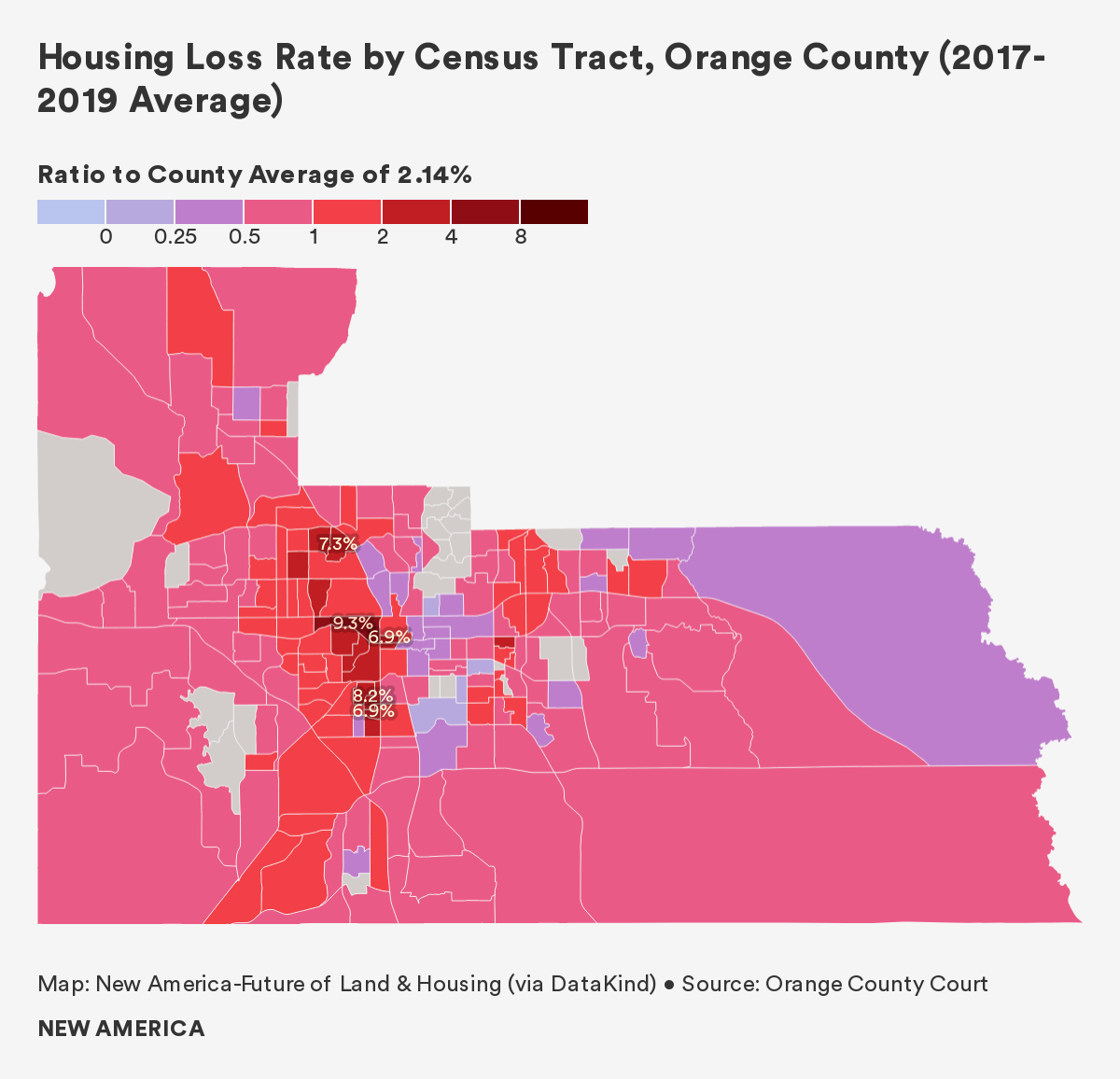

Housing loss in Orange County is most acute in census tracts in west-central Orlando, particularly in and around the Parramore neighborhood where rates were three times the county average. Parramore was developed as a segregated Black community, and the legacy of segregation and racist housing policies that excluded Black residents from white neighborhoods are clear today.

Parramore was developed as a segregated Black community, and the legacy of racist housing policies and urban development that excluded Black residents from white neighborhoods is clear today.

Evictions: Forty-five percent of residents in Orange County rent their homes, but evictions accounted for 66 percent of housing loss from 2017 to 2019. Nearly 16,000 households were evicted in Orange County over our study period, resulting in an eviction rate of 2.6 percent. This is a significantly lower eviction rate relative to the other Sun Belt counties.

Eviction rates were most acute in census tracts to the west of downtown Orlando, around Parramore, Lake Sunset, Rio Grande Park and in the neighborhoods between Hiawassee and route 441. The tracts with relatively high eviction rates ranged from 5 percent to 7 percent, with one tract that included the neighborhoods Haralson Estates, Rock Lake, and Lorna Doone reaching as high as 14 percent.

The Seasonality of Evictions in Orange County: Bucking the Trend?

Average evictions in Orange County were high in January and fell steadily until April, falling on average 34 percent over these four months. From April to August, evictions rose steadily, until September when they fell sharply again. Average evictions spiked back up in October, only to decline again during the last couple of months of the year.

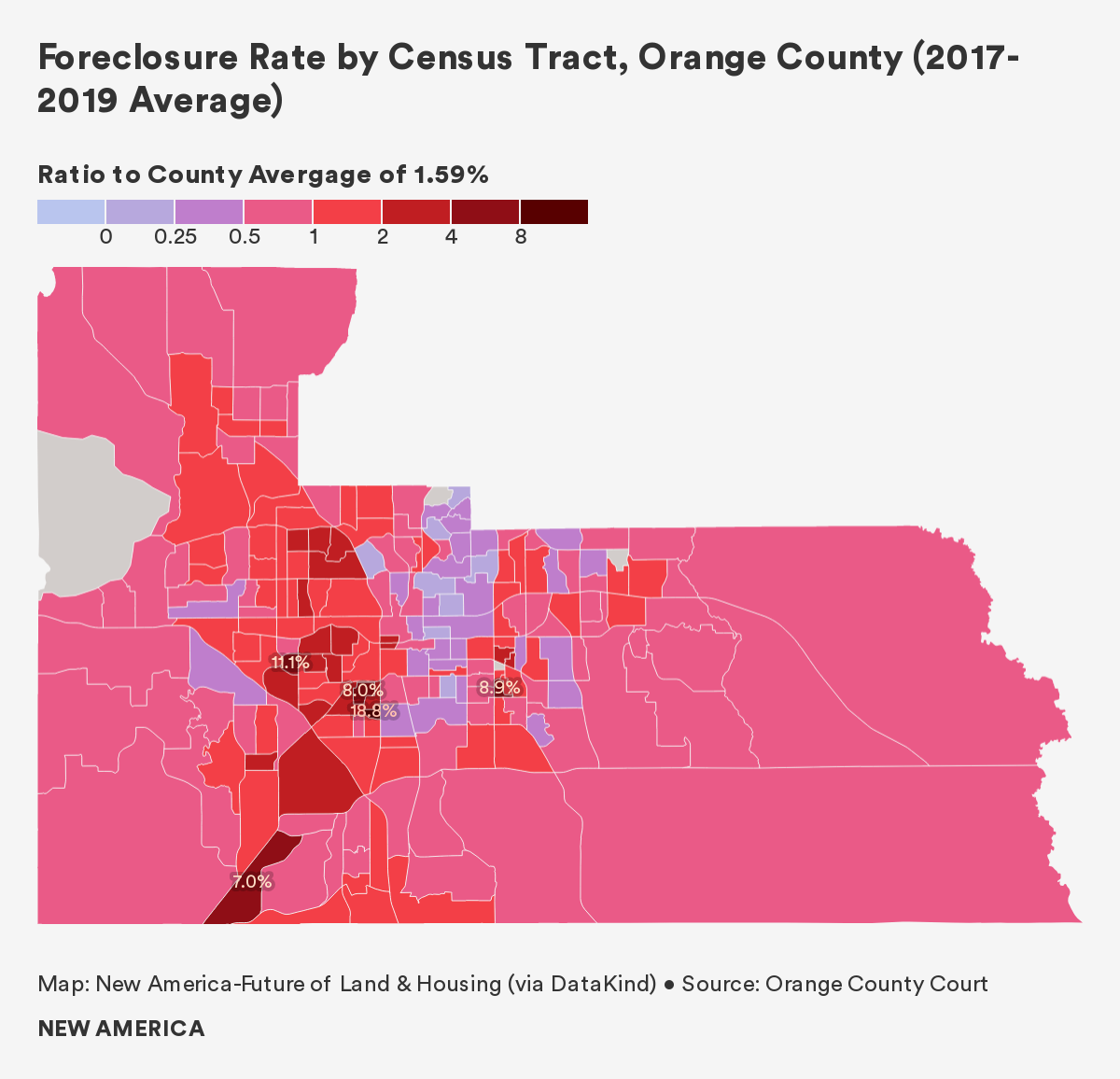

Mortgage Foreclosures: Homeowners are less at risk of housing loss than renters. While fifty-five percent of residents in Orange County own their home, mortgage foreclosure accounted for 34 percent of housing loss from 2017 to 2019. Just over eight thousand households were foreclosed upon in Orange County during our study period, resulting in a foreclosure rate of 1.6 percent.

While foreclosure rates in Orange County were consistently higher than average in the neighborhoods to the west of downtown Orlando, these tracts also had fewer homeowners with mortgages than other parts of the county. These tracts had foreclosure rates ranging from 2 percent to 4 percent, with the exception of two tracts in Park Central, which had foreclosure rates of 8 and 19 percent, and another tract by Valencia College, which had a foreclosure rate of 11 percent. Though there are very few of them, tracts with foreclosure rates of 9 percent or above had less than 50 homeowners with mortgages, and are not typical of county dynamics overall. Relative to other counties, foreclosure rates in Orange County were relatively steady, with fewer fluctuations and fewer hotspots.

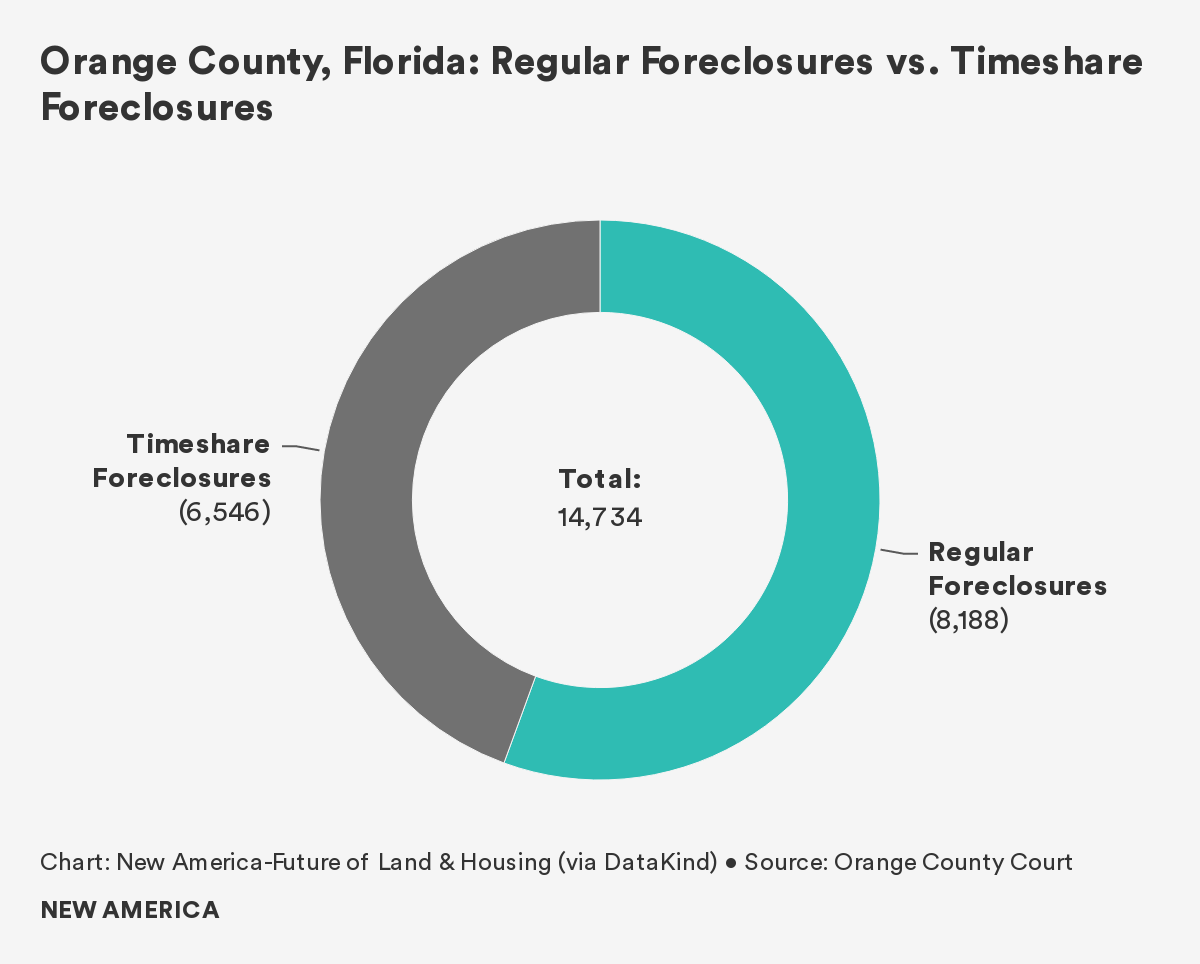

Timeshares and Foreclosures in Orange County

As our partners at DataKind cleaned and analyzed the foreclosure dataset they had received from the Orange County Court, they noticed a fascinating trend that we did not see in any of our other case study locations: approximately 6,500 of the county's 14,000 foreclosures were timeshares.

Perhaps unintuitively, it is possible for a timeshare to go into foreclosure. If a timeshare owner takes out a mortgage on their timeshare purchase, that mortgage is subject to delinquency and foreclosure just like a traditional home mortgage.

However, while a timeshare foreclosure certainly results in negative credit impacts, it is unlikely to lead to housing instability or homelessness as would the foreclosure of a primary residence. Since this report focuses on housing instability and loss, we decided to omit this data from our analysis. If we were to include "timeshare foreclosures" in our calculations, Orange County's foreclosure rates would nearly double.

Who Is Losing Their Home?

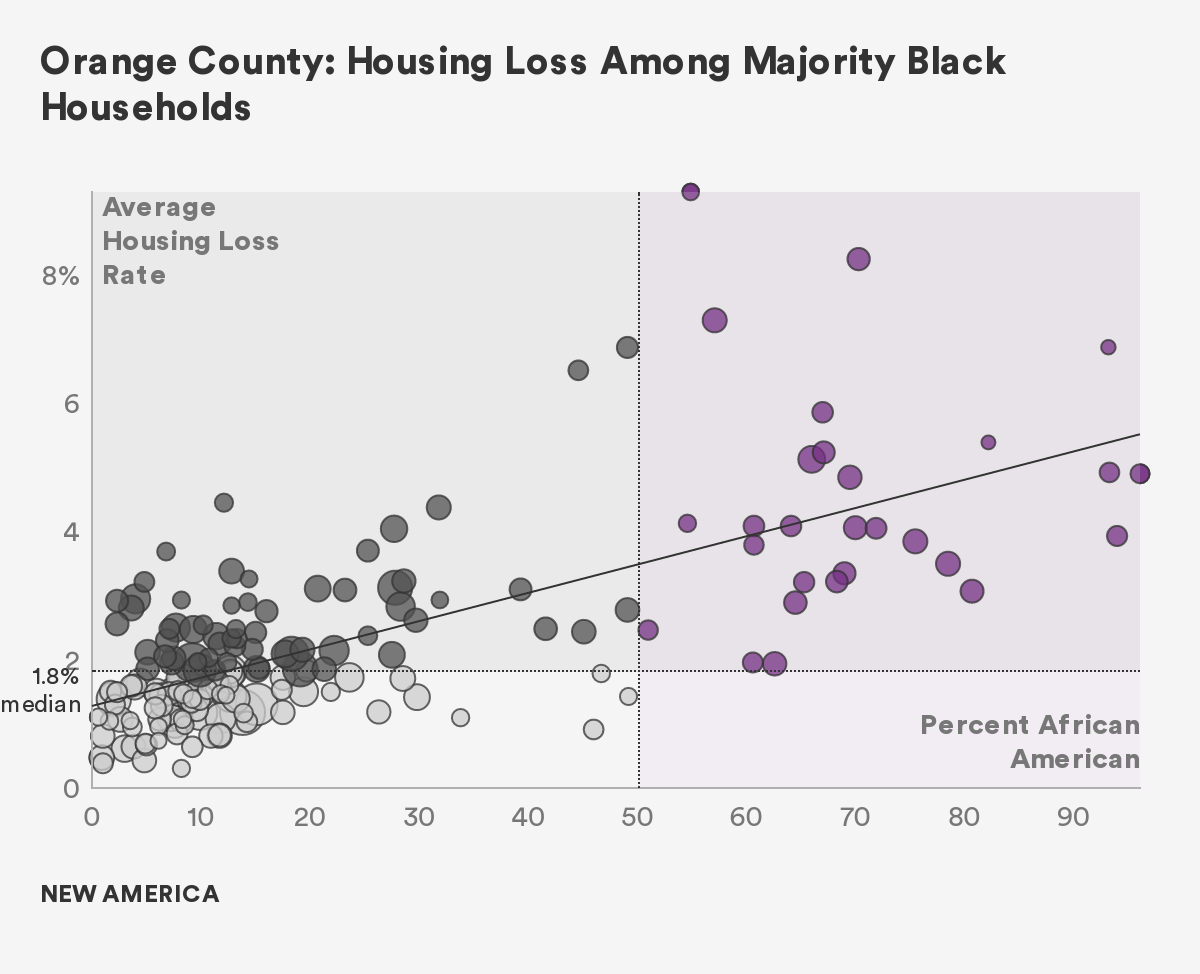

Orange County exhibited a strong relationship between home loss and race. Evictions, foreclosures, and overall housing loss was substantially higher in census tracts with a larger share of Black households. Tracts with a higher percent of households that rely on public transportation to get to work, and tracts with more households without health insurance, also showed higher housing loss rates.

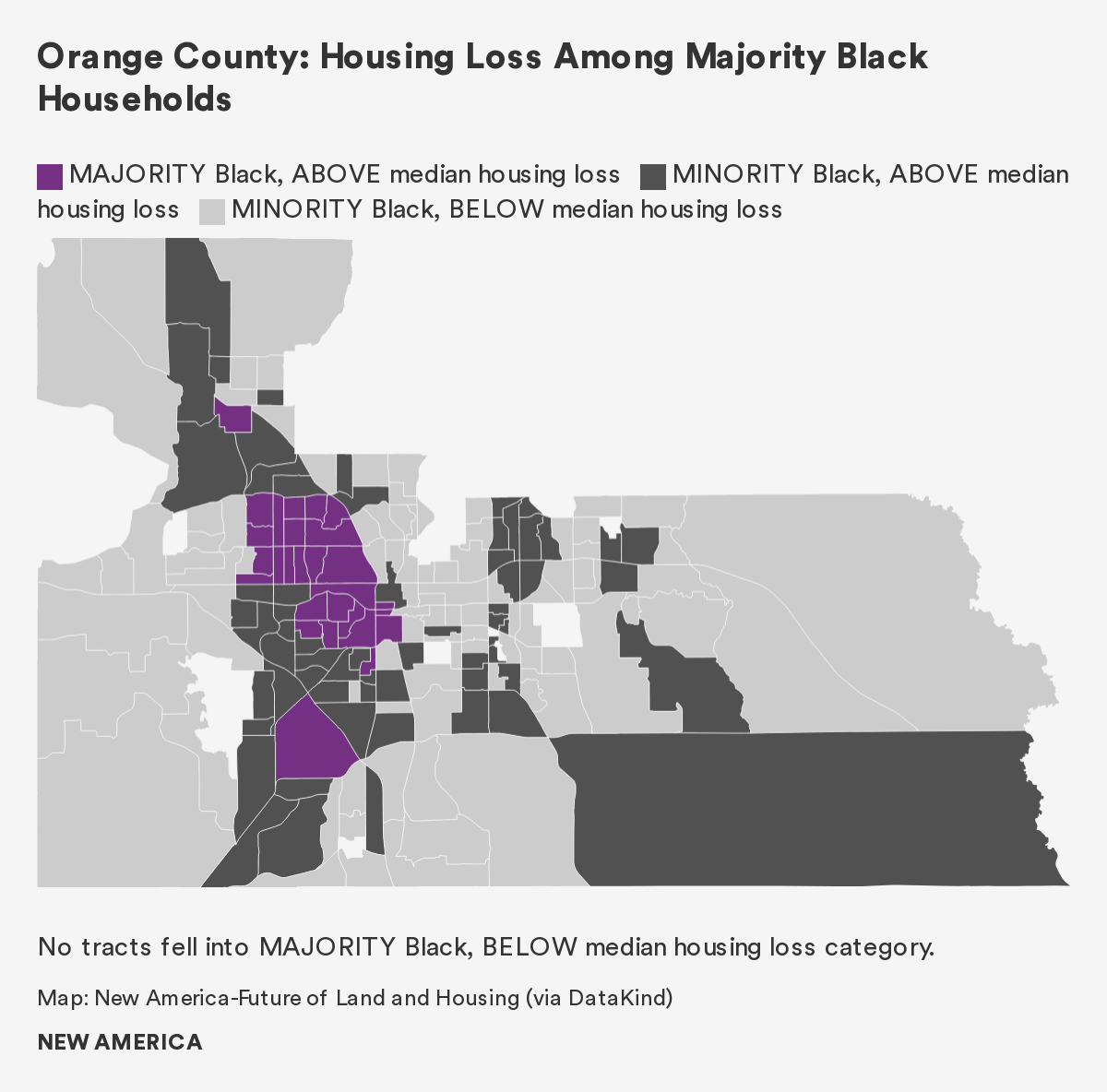

To understand the relationship between housing loss and Black households better, we categorized census tracts such that they fell into one of four categories: by whether they were majority or minority Black (in other words, whether the percent of Black households fell above or below 50 percent) and by whether the housing loss rate was above or below the county median of 1.8 percent. In the scatter plot, we see that all majority Black census tracts in Orange County had housing loss rates above the median.

To better understand where in Orange County the relationship between race and housing loss is most prominent, we mapped this relationship. Census tracts with higher concentrations of Black households and above average housing loss rates are clustered in west-central Orlando from the Rosemont neighborhood south to Rio Grande Park.

Housing Loss and COVID-19

Prior to the pandemic, access to affordable housing was impeded by several factors. First and foremost, decades of population growth and yearly tourist traffic have resulted in increased rents in Central Florida that have outpaced wage growth throughout the region, particularly in Orange County. As a result, many residents live in areas outside Orlando where rent is more affordable and commute to Orlando.

Further, local affordable housing stock is limited by a widespread practice wherein developers convert available low-cost real estate into timeshare or rental properties. As a result, “naturally occurring” affordable housing has become increasingly unaffordable over time. According to one interviewee, state and federal business incentives, such as tax credits and funding available to developers, are not sufficiently lucrative to facilitate private development of affordable housing.

The county’s limited supply of affordable housing is in high demand, contributing to competition for what little affordable housing is made available. This may constitute a roadblock to rehousing families once they have been evicted. As such, many renters are displaced to older hotels and motels, like the ones along the route 192 corridor in Osceola County.

According to interviewees, COVID-19 has acutely impacted Orange County. Home to Disney World and Universal Studios, leisure and hospitality jobs account for 16 percent of the workforce in Orlando. This sector has seen a 31 percent drop in employment from the same time last year. The service workers facing eviction or economic hardship as a result of the pandemic were already vulnerable to housing loss because their low wages did not cover the rising cost of housing. This insecurity is now severely exacerbated in the wake of mass layoffs at Disneyworld and elsewhere. Interviewees expect evictions to dramatically increase after moratoriums end. Outside evictions, there has been an uptick in lease non-renewals, potentially indicating that people are being priced out as unemployment increases.

Orange County used its CARES funding to institute an eviction diversion program that circumvents civil court mediation and relies instead on mutual agreements between landlords and tenants. The program makes available up to $4,000 per rental property to cover housing debt. Some stakeholders noted that recruiting landlords, notably larger landlords, to participate in the program has been difficult. While the eviction diversion program expires at the end of January 2021, the program will continue in some form with funding from the recent federal relief package. The new program will increase the dollar amount of assistance available per household and cover a longer time span. As eviction moratoriums are extended, applications to the eviction diversion program are increasing.

The distribution of relief funds related to the pandemic has been hampered by several factors. The county deployed relief funding through existing channels, which already had numerous documentation requirements for residents. Further, existing aid distribution organizations lack the staffing capacity to handle misapplications and other issues. While Orlando distributed its $2.5 million allocation to residents before the end of the year, it is unclear whether Orange County utilized all of its allocated CARES Act funding before the spending deadline.

The modified loans that banks have offered homeowners to avoid foreclosure typically constitute brief forbearances followed by balloon payments. This could contribute to an even higher number of foreclosures once forbearances end.

Policy Solutions

Our policy recommendations to mitigate housing loss amid COVID-19 can be found in the report section: “Housing Loss in the U.S. Sun Belt.”

Citations

- From an interview with contributing author Jack Portman.