Table of Contents

Miami-Dade County, Florida

“The people who need stability the most are the people who are least able to lock in a stable housing cost.” – Housing Researcher, University of Florida1

Situated on the Atlantic Coast in the southernmost tip of Florida, Miami-Dade County is home to the cities of Miami and Miami Beach, an international airport, and PortMiami, known as the “cruise capital of the world.” With 2.7 million residents, Miami-Dade is the most populous county in Florida.

Miami-Dade County has a multicultural, multilingual population. Sixty-six percent of the population speaks Spanish at home and over half the county’s residents are born outside of the U.S. The Latinx community makes up nearly 70 percent of the population and the Black community makes up 17.7 percent, while the non-Latinx, white residents account for 12.9 percent of the population.

Since the start of the COVID-19 pandemic, Miami-Dade County has experienced roughly 331,000 cases and 4,450 deaths. Adding to the public health toll, the unemployment rate in Miami-Dade County was 7.4 percent as of November 2020, which is over three times the level of unemployment during the same time in 2019. Housing insecurity was also acute: the Census Bureau’s Household Pulse Survey shows that 22.2 percent of residents surveyed in the Miami-Fort Lauderdale-Pompano Beach metropolitan area expect to be evicted or foreclosed upon in the next two months.

When and Where Are People Losing Their Homes?

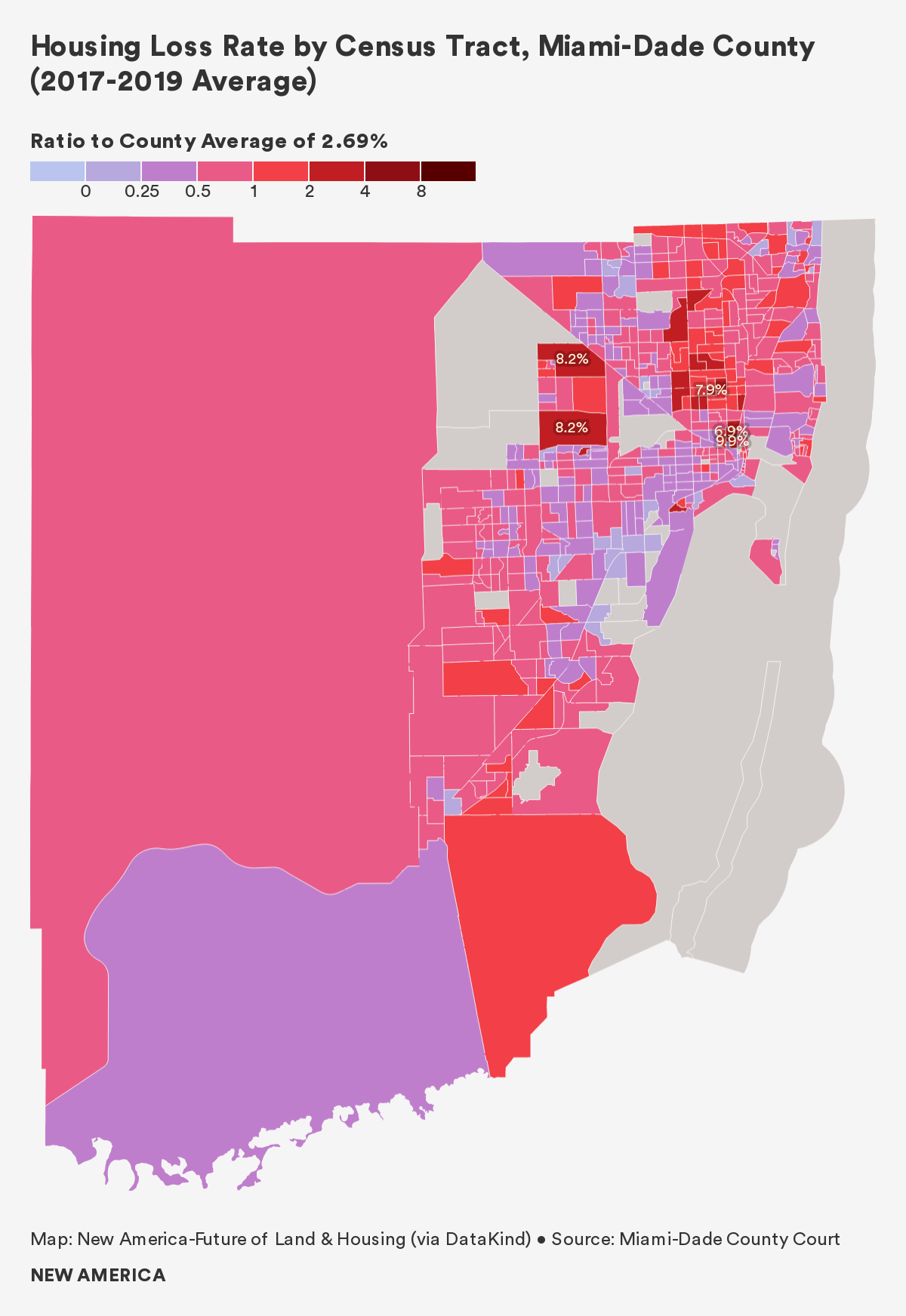

Overall Housing Loss: More than 150,000 people lost their homes through eviction and foreclosure between 2017 and 2019, a rate of 2.7 percent per year. This rate of housing loss is below average for the Sun Belt counties examined in this report.

Housing loss was most acute in tracts to the west of the Miami International airport and in the neighborhoods Opa-Locka, Westview, West Little River, Gladeview, and Brownsville. In these tracts, we saw housing loss rates two or three times higher than the rest of the county.

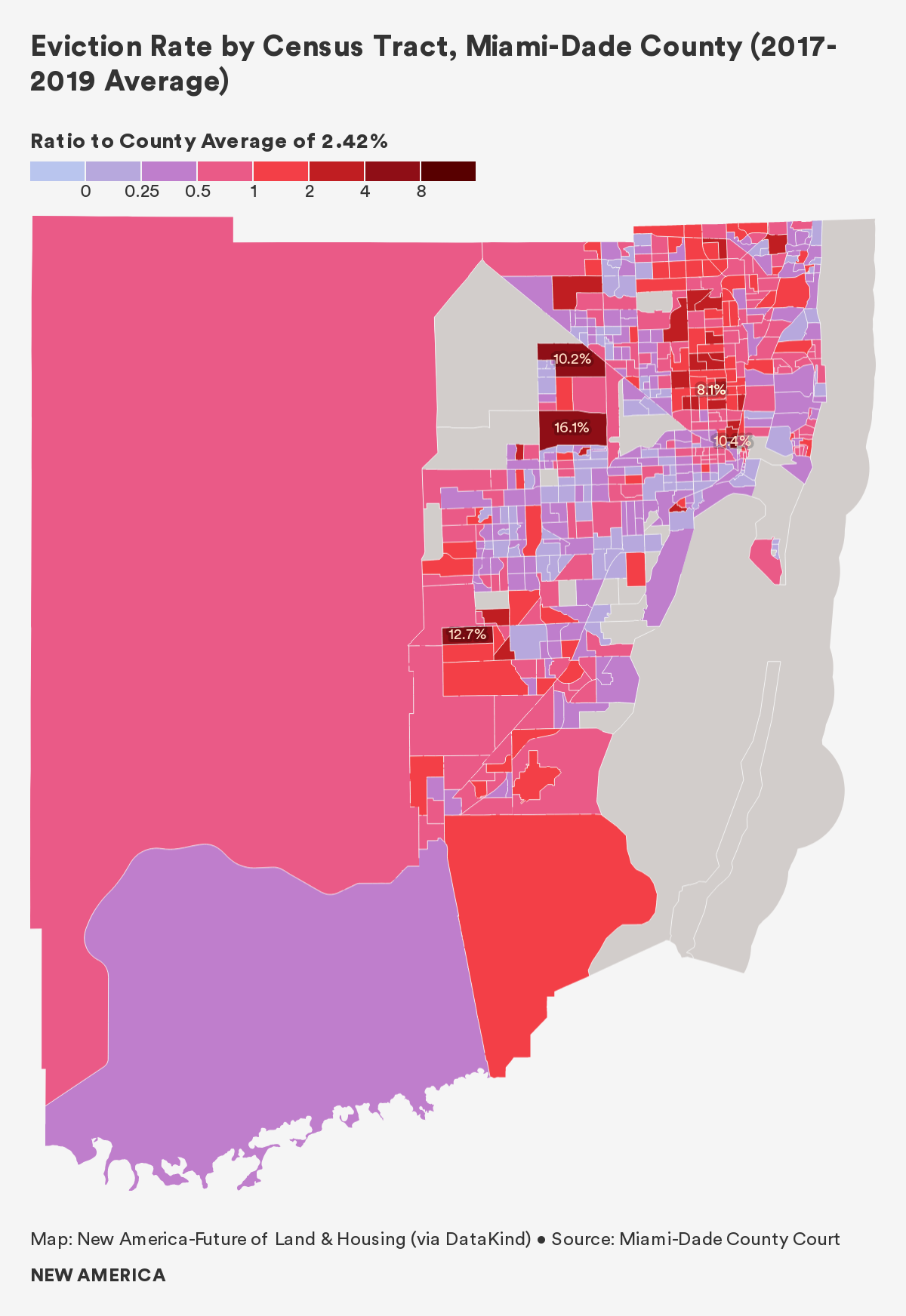

Evictions: In most of the counties we studied, evictions accounted for a disproportionate proportion of housing loss. By contrast, in Miami-Dade County evictions accounted for 53 percent of overall housing loss, closely aligning with the percent of residents in Miami-Dade who rent their homes, 49 percent. Roughly 29,000 households were evicted in Miami-Dade County, resulting in an eviction rate of 2.4 percent. This eviction rate is the lowest of the Sun Belt counties we studied, and fell by 10 percent over the course of the study period.

The highest eviction rates were in tracts west of the Miami International Airport, near Sweetwater and north of Doral. Two tracts in this area had eviction rates of 10.2 percent and 16.1 percent. A cluster of tracts around Opa-Locka and West Little River had high eviction rates, ranging from 4 percent to 8 percent. Close to downtown Miami, in Overtown, a historically Black neighborhood, the eviction rate is over 10 percent.

A Spotlight on Summer Evictions

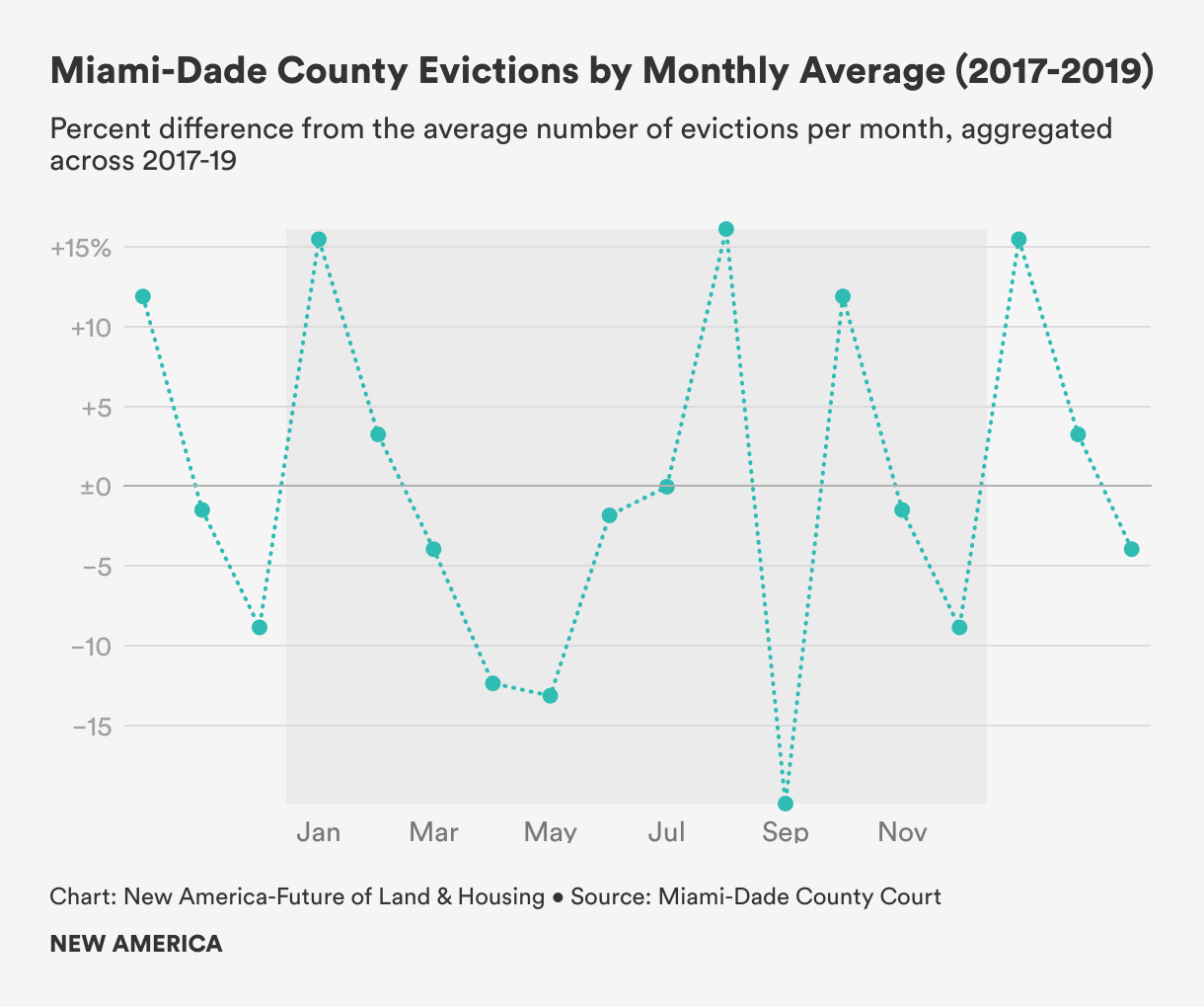

Similar to trends in other parts of the country and across the Sun Belt, evictions in Miami-Dade County drop steadily over the winter months and rise steadily from late spring until the end of summer. August had the highest average number of evictions at 971, followed by a 30 percent drop-off in September, which saw the lowest average number of evictions at 679.

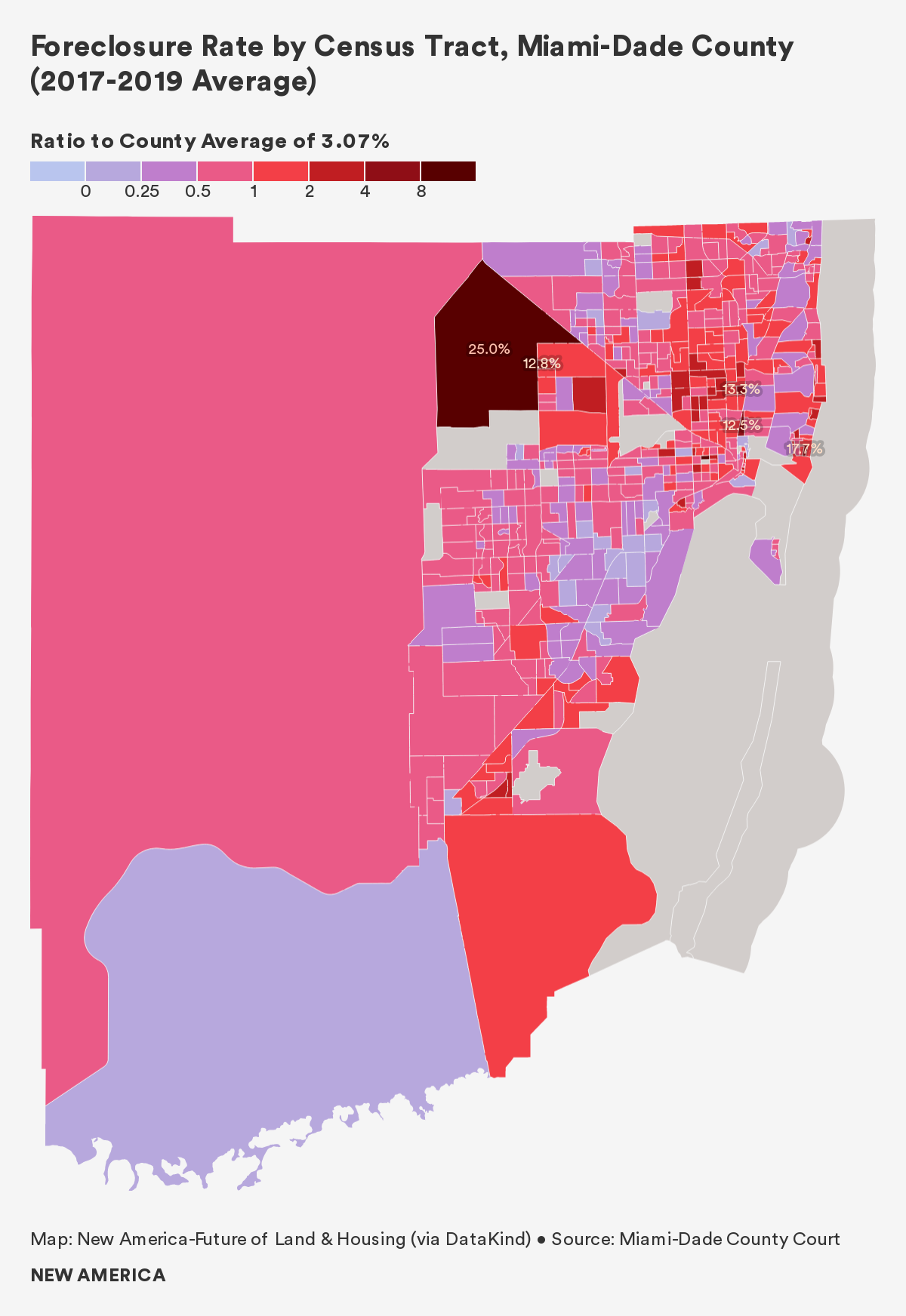

Mortgage Foreclosure: The foreclosure rate for Miami-Dade is the highest of the seven Sun Belt counties included in this report. More than 26,000 households were foreclosed upon in Miami-Dade County over this three-year period, a foreclosure rate of 3.1 percent.

High foreclosure rates in Miami-Dade are clustered in two main areas: inland and to the northeast of the Miami International Airport in neighborhoods such as Brownsville, Gladeview, and West Little River; and along the coast in Mid-Beach and North Beach. The high foreclosure rates in these tracts range from 5 percent to 13 percent. There is a small tract in South Beach and a large tract to the west of Hialeah with foreclosure rates of 17.1 percent and 25 percent, respectively, but both have relatively few homeowners with mortgages.

Who Is Losing Their Home?

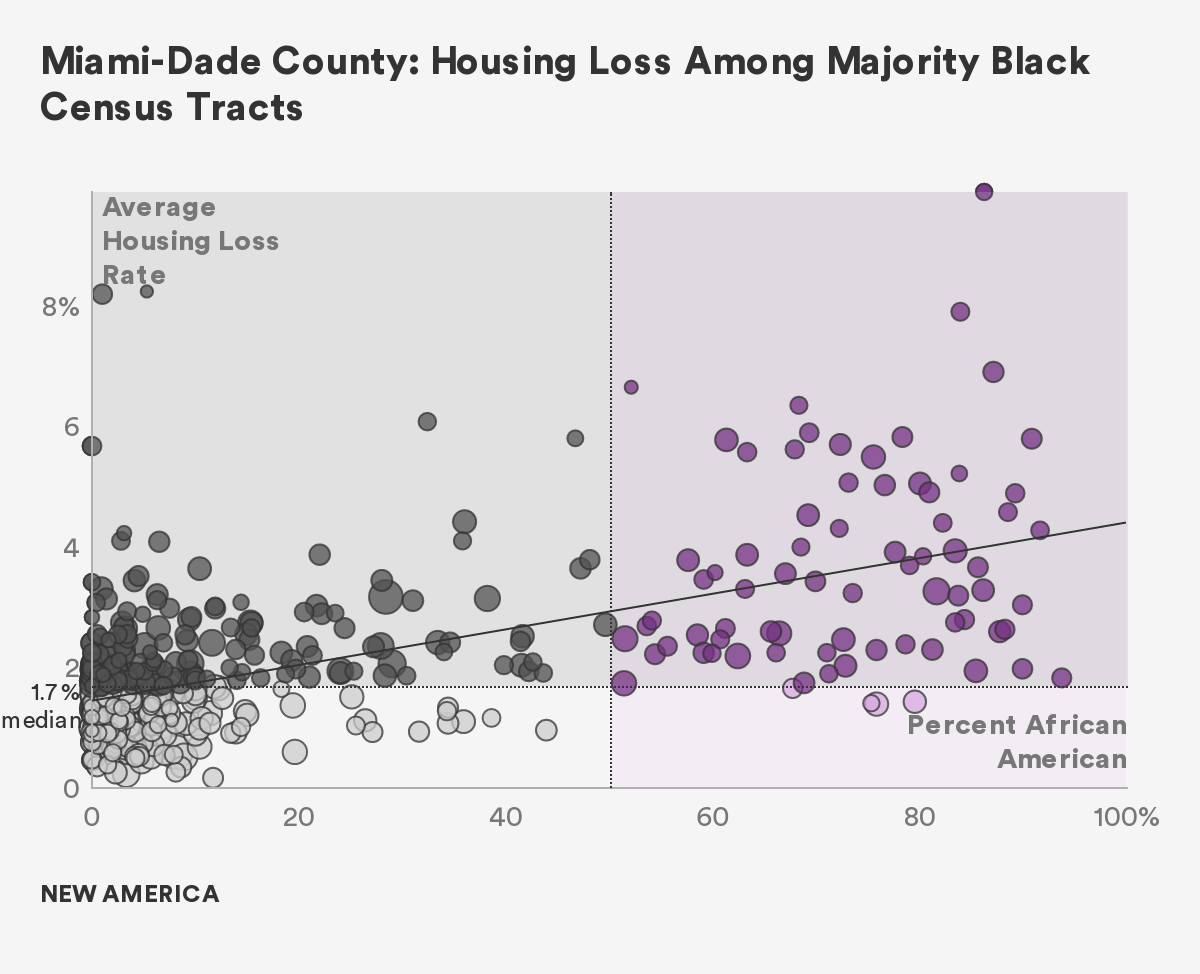

We found a strong relationship between home loss and racial composition in Miami-Dade County. We see that census tracts with a larger share of Black households are likely to experience higher rates of home loss than census tracts with fewer Black households. In other words, census tracts with more Black households are most at-risk of loss, notably via evictions, in comparison to all other races. Census tracts with higher percentages of Latinx households displayed a moderately negative relationship with evictions and housing loss.

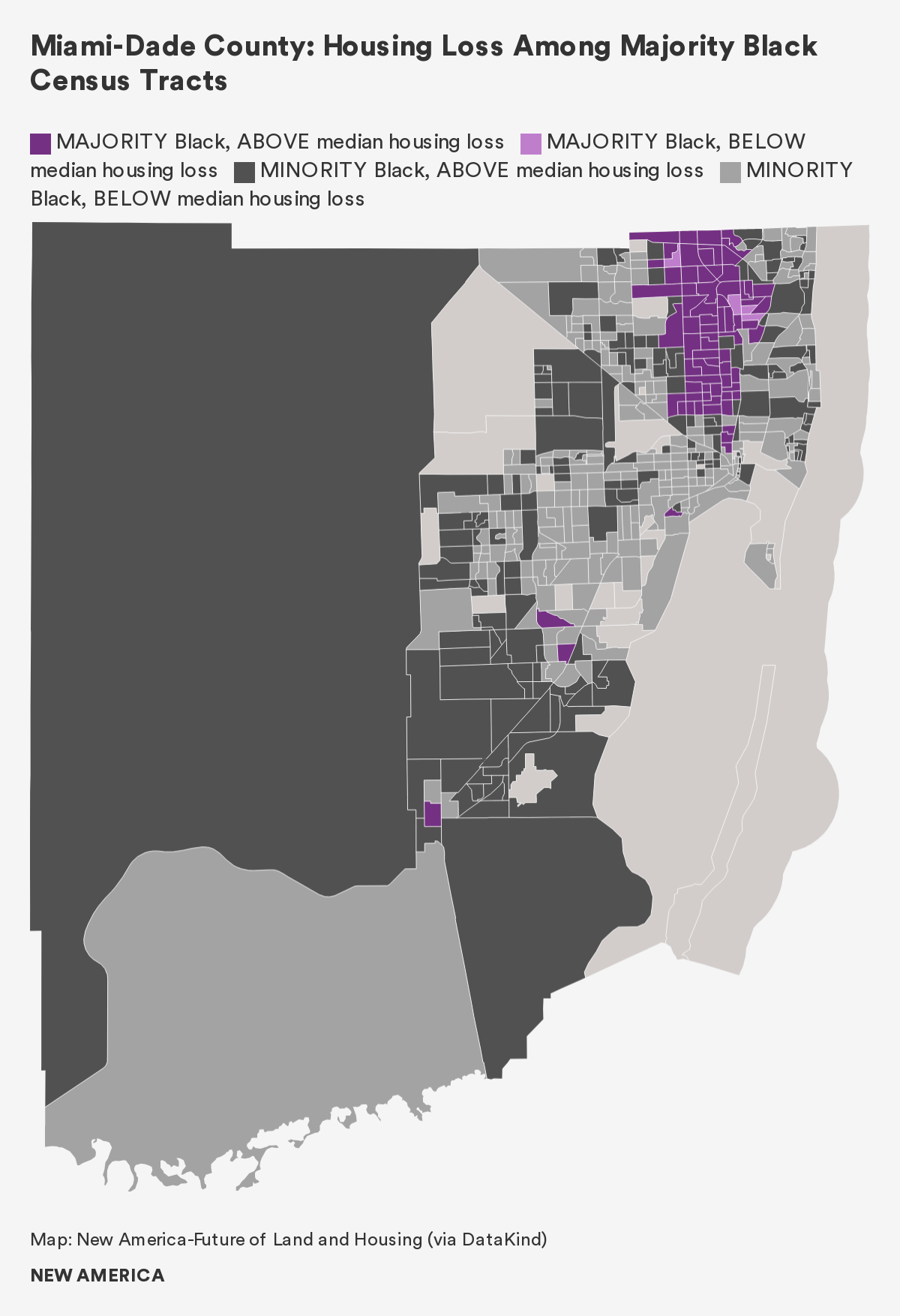

To better understand the relationship between housing loss and Black households, we categorized census tracts by whether they were majority Black (or whether the percent of Black households fell above or below 50 percent) and by whether the housing loss rate was above or below the county median of 1.8 percent. Categorized this way, census tracts fell into one of four categories. In the scatter plot, we can see that ninety-five percent of majority Black census tracts have housing loss rates above the median. We see there are only a few tracts that are majority Black and have below median housing loss rates, and these tracts do not fall too far below the median.

We mapped this data to better understand where in Miami-Dade County the relationship between Black households and housing loss is the most prominent. We see that majority Black tracts are nearly all clustered to the east of Hialeah, from Miami Gardens south to Model City, and almost 100 percent of these tracts have higher than median housing loss rates.

Notably, Miami-Dade County did not exhibit many of the relationships between social factors and housing loss that we saw in other Sun Belt counties. For example, we did not see noticeable correlations between high eviction and foreclosure rates and lack of health insurance or high percentages of single-parent households.

Housing Loss and COVID-19

Prior to the pandemic, housing experts identified two big sources of housing instability in Miami-Dade: the lack of quality affordable housing and the prevalence of outside investment in expensive housing. These forces made it difficult for even middle-income renters to afford homes, as they were often pitted against investors who paid in all cash. Interviewees discussed how incomes that were once high enough to support housing costs in Miami-Dade are no longer sufficient, and middle-income residents are increasingly cost-burdened. One example of this is in the historically Black Miami neighborhood of Liberty City, which is on higher ground than the surrounding neighborhoods, and where residents are seeing increasing in-migration from higher-income residents as part of “climate gentrification.”

COVID-19 has exacerbated existing challenges and increased housing instability across the county. Local stakeholders confirmed that residents in Miami-Dade who were “treading water” and “living on the edge” before the pandemic are the most vulnerable to housing loss. This includes seniors, undocumented immigrants, and low-income residents who mostly work in the informal economy, such as Lyft and Uber drivers, as well as those that are typically paid in cash (e.g., house painters, dog walkers, house cleaners, etc.).

One stakeholder said that the “scope and scale of need is so enormous” in Miami-Dade that COVID-19 relief funds will only go so far in alleviating housing instability. Local stakeholders explained that housing-specific COVID relief funds were split into three pots: one small and two big. The small pot was to fund specialized needs gaps, such as supportive housing for people with special needs or for existing organizations to make operational changes to how they house people. The two bigger pots went to a pre-existing collection of organizations that are part of the State Housing Initiatives Partnership (SHIP), specifically designed to distribute aid in crises, and to the Florida Housing Finance Corporation, which created a program for participating owners of state-sponsored affordable housing.

In describing housing-related aid, one stakeholder explained that Miami-Dade “got off to a late start and the implementation has been bumpy.” Several interviewees described significant variation in how funds have been distributed locally, from how much documentation organizations were requiring from applicants to whether organizations had the administrative capacity to process applications and distribute money. A local expert explained that while some organizations had preexisting processes in place to move money quickly, other organizations did not, and this created an access and equity issue in terms of who was able to receive assistance expeditiously.

Miami-Dade “got off to a late start and the implementation has been bumpy.”

Lastly, stakeholders described how critical the eviction moratoriums have been, especially for those living in housing that is not subsidized and whose rents do not fluctuate as their incomes fluctuate. One local stakeholder discussed the importance of robust advocacy on the changing status of tenant protections and eviction moratoriums as tenants that do not know their rights are more vulnerable to eviction.

Policy Solutions

Our policy recommendations to mitigate housing loss amid the pandemic can be found in the report section: “Housing Loss in the U.S. Sun Belt.”

Citations

- From an interview with contributing author Abbey Chambers.