Coastal Risk is Rising: How Will We Respond?

Introduction

With 95,439 miles of shoreline, U.S. coastal areas were home to 29.1 percent of the U.S. population (over 94 million people) in 2017. The coastal population grew steadily in recent decades, increasing 15.3 percent since 2000.1 This has brought economic growth; if the coastal counties were a country, they would rank third, after the United States and China in gross domestic product.2 Annually they produce more than $9.5 trillion in goods and services, employ 58.3 million people, and pay $3.8 trillion in wages.

At the same time, the risk to the people, buildings, and economies of the coast is growing. Sea level rise and more frequent and perhaps more severe storms are increasingly no longer a future threat but a current one.

“Managed retreat,” the purposeful and planned relocation of people, infrastructure, and buildings away from vulnerable areas, such as the coasts and riverine flood plains, is one response to this risk. At present, there is no consensus on where and how managed retreat would be implemented and who would be affected.

Despite the lack of formal policies, at either the national or local level, communities are increasingly discussing, or in some cases implementing, managed retreat. They are grappling with many questions, including who will cover the cost to stay and who benefits or loses from the decision to pull back. Which homeowners will be most affected? Will those with greater economic resources have different choices than poor or middle-income households?

This report examines the increased threat of climate change to coastal communities, the weaknesses of current local and federal policies to manage this heightened risk, and the recent introduction of eminent domain as a policy tool for involuntary managed retreat.

Floods and Storms: Increasing Coastal Risk

Population growth is exploding in parts of the country that are most susceptible to hurricanes and coastal flooding. These areas will become even more vulnerable in the coming years due to the impacts of climate change.

The Gulf of Mexico and Atlantic coasts, home to 60.2 million people, are also the most vulnerable to hurricanes. And their populations continue to increase. In the Gulf of Mexico region, the population increased by 26.1 percent in recent decades, nearly double the national growth rate. This added 3 million people to vulnerable areas that experienced 13 major storms, each causing more than $10 billion in damage, between 2000 and 2017.3 In 2018 one storm alone, Hurricane Michael, the first Category 5 hurricane to make landfall in the United States since Hurricane Andrew in 1992, caused $25 billion in damage. Coming ashore in the Florida panhandle Hurricane Michael destroyed the community of Mexico Beach, and was responsible for 16 deaths.4

Climate change is predicted to intensify the strength of tropical storms in the coming decades. In addition, sea level rise is causing higher levels of flooding when these hurricanes hit. As hurricanes move, high winds around the eye of the hurricane blow on the ocean, creating a vertical circulation, pushing the water down towards the ocean floor. As the storm moves onshore into shallow water, the water can no longer be pushed downward; instead, it moves up and inland, creating a “storm surge.” This fast-moving “wall of water”5 can be the most damaging part of the storm, causing wide-scale property loss and death by drowning. Storm surge from Hurricane Katrina reached 19 feet, overwhelming the levees designed to protect the low-lying city. In Hurricane Sandy, the arrival of the storm coincided with a high tide, creating a “storm tide” of 20 feet.

Even smaller surges can cause widespread beach erosion and damage key infrastructure such as roads, railroads, and bridges. North Carolina Highway 12, which connects the barrier island communities of the Outer Banks to the mainland, is often damaged or closed by storms. Sea level rise here is twice that found further south on the coast, and even strong winds blow waves over the road. Since 1851, this vulnerable area has been hit by 156 hurricanes or tropical storms.6

Coastal communities construct extensive (and expensive) structures to protect buildings and beaches from erosion, wave action, and other ocean effects. This “hardening” is done with concrete fortifications such as sea walls or other concrete barriers. In 2015, NOAA estimated that 14 percent of the U.S. shoreline was coated in concrete, with hardening especially noticeable in the Atlantic and Gulf regions. Though designed to reduce the threat of property damage, these structures actually increase long-term risk. These protective barriers redirect the wave energy back towards the ocean, where the “water can scour beaches and destroy tidal marshes that are not protected by concrete, ultimately making coastal areas more vulnerable to storms.”7

In 2015, NOAA estimated that 14 percent of the U.S. shoreline was coated in concrete, with hardening especially noticeable in the Atlantic and Gulf regions.

Even in the absence of extreme weather events, coastal communities are already managing flooding associated with rising sea levels. In 2019 NASA documented over 600 “sunny day floods” caused by high tides in conjunction with lunar activity amplifying the impact of sea-level rise.8 Such events are common in Miami, where the sea level has risen 2.8 inches since 1992, and in the Florida Keys, which had 90 days of sunny day flooding in 2019.9

The Cost to Stay

How much are we willing to pay to stay on the coasts?

The cost to adapt infrastructure for climate change is high, typically well beyond what can be covered through the normal tax revenue of towns and cities. Increasingly, communities are grappling with questions of what should be done to stay and how to pay for it. At times, these questions lead to an existential one: should we stay?

In the Outer Banks, homeowners in the community of Avon need to raise $11 million to save their beachfronts and protect the roads. But who should pay to dredge a million cubic yards of sand and widen 2.5 miles of beach? Will some members of the community benefit more than others? And if so, should they shoulder a greater burden of the cost? Avon, and Dare County, ultimately decided that homeowners closer to the ocean did benefit more and should pay a greater share.

In response, Dare County approved two distinct property tax districts.10 Those owners closest to the beach, where home values can be in the millions of dollars, face a 62 percent property tax increase. Those further from the ocean will have a much smaller increase. This will raise an additional $750,000 each year and cover about half of the project’s cost. The remainder will be covered through occupancy taxes collected from visitors to the area’s hotels.

In Miami, a new stormwater management plan calls for $3.8 billion in infrastructure improvements between now and 2060. The city faces an anticipated sea level rise of 18–30 inches in the coming decades. To meet this threat, the plan calls for 90 miles of upgraded sea walls, an additional 93 giant stormwater pumps, backflow preventers, and a network of drainage pipes. Funding for the plan has been identified; indeed, the plan acknowledges it may be necessary to allocate funding initially to a few areas of the city. Even then, it will take several years to see results. Even with full funding, not all of the city can be saved, as available engineering solutions aren’t adequate to protect some of the city’s most vulnerable areas.11

Communities in the Florida Keys also face hard choices. It will take over $2.6 billion to raise roads and protect homes and commercial structures in Monroe County. Here, too, political leaders have acknowledged not everything can be saved. According to County Administrator Roman Gastesi, “It doesn’t mean that we are going to spend $20 million dollars to go down a small road to get to two or three houses. It just doesn’t make sense.”12 It is unclear, too, how this project, which focuses on protecting the Keys’ main road, U.S. 1, will be funded.

A Failing Federal Flood Insurance Program

Meanwhile, there is growing concern about the financial viability of another major safeguard that has allowed communities to keep living on the coasts: the nation’s heavily indebted flood insurance program.

Created by Congress in 1968 and managed by the Federal Emergency Management Agency (FEMA), the National Flood Insurance Program (NFIP) provides flood insurance to homeowners belonging to participating communities in flood-prone areas. Participating communities are required to implement practices to reduce future flood risk. Under the Community Rating System (CRS), communities are rated based on their voluntary flood mitigation activities, and communities with more activities receive greater discounts on flood insurance rates. The program also restricts development in floodplains, thereby reducing overall national flood risk. As of December 2020, over 22,000 communities in 56 states and jurisdictions participated in the NFIP.13

However, the program is not currently solvent, and its future is uncertain.

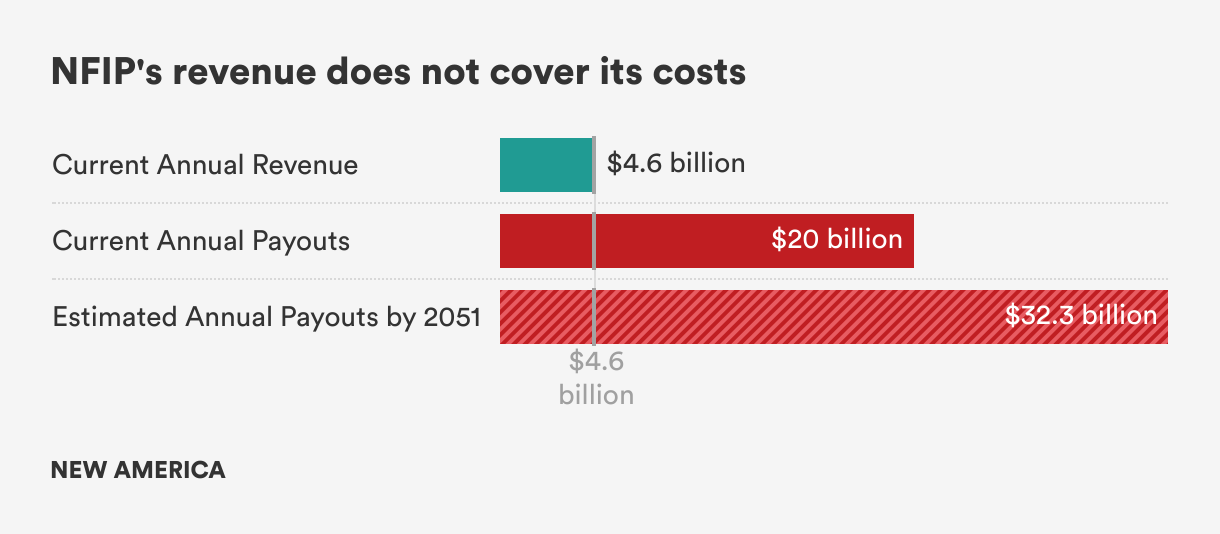

NFIP pays out more than it takes in, a situation that is likely to become more severe as climate change leads to increased flooding. NFIP brings in approximately $4.6 billion in annual revenue primarily through premiums, fees, and surcharges on insurance policies.14 This is clearly not enough to cover the claims inflicted by a single large storm, let alone multiple storms in one year. Even small storms, such as Hurricane Irene that hit the Outer Banks as a Category 1 in 2011, can inflict more than $15 billion in damage.15 First Street Foundation, a nonprofit organization that focuses on quantifying climate risk, calculated the average annual loss for 4.3 million properties in the United States with substantial flood risk to be $20 billion, or $4,694 per property. By 2051, due to the impacts of climate change, this is projected to rise by 61 percent to $32.3 billion, or $7,563 per property. 16

NFIP pays out more than it takes in, a situation that is likely to become more severe as climate change leads to increased flooding.

NFIP was rendered insolvent for the first time in 2005, overwhelmed by payouts for Hurricanes Katrina and Rita; since then, it has remained viable only through congressional intervention. In recent years NFIP has borrowed extensively from the U.S. Treasury to cover payments on claims. By law, the NFIP can borrow no more than $30.425 billion. By September 2017, the program had reached its borrowing limit. Faced with claims for damages from hurricanes Harvey, Irma, and Maria, Congress cancelled $16 billion of this debt in October 2017, enabling the NFIP to borrow again. Today the NFIP owes $20.5 billion.17 Since then, Congress has repeatedly reauthorized NFIP only on a short-term basis—the current authorization expires September 30, 2021.

Stalled Reform Efforts

Efforts to reform the program have focused on increasing premiums to reflect the true risk of living on the coast or other flood-prone areas, eliminating what many consider a government subsidy, especially for wealthy coastal residents. The First Street Foundation study, The Cost of Climate: America’s Growing Flood Risk, estimated an average annual loss of $4,419, while the average NFIP premium is $981.18

However, assessing higher premiums has proven difficult, with concerns that low- and moderate-income homeowners, especially those with mortgages, will be left without affordable insurance.

In 2012, Congress introduced the Biggert-Waters Flood Insurance Reform Act authorizing an increase in premiums over a five-year period to bring them in line with the true risk of flooding. Implementing this rightsizing would mean those living in areas of highest risk, based on their FEMA rate maps, could see the cost of flood insurance skyrocket. For example, the annual payment of a homeowner in Staten Island, New York was estimated to increase from $400 to $9,000.19 In the extreme, some Florida homeowners could have been assessed premiums of $20,000 to $30,000 by the end of the five-year period.20

Amid concerns that low- to moderate-income homeowners would be unable to afford these increases, and such rates would make it impossible to sell their homes, Congress amended Biggert-Waters. The Homeowner Flood Insurance Affordability Act, which came into effect in 2014, capped the amount insurance premiums could be increased annually by no more than 18 percent for a primary residence.21

Flood Risk 2.0

In October 2021, NFIP will introduce its most extensive changes ever since the program was created. The new Risk Rating 2.0 system fundamentally alters the way true risk is calculated for property and, for the first time, factors in future climate change. The rates go into effect on October 1, 2021, for new NFIP policies, and rate changes to existing policies take effect April 1, 2022.22

Previously, the risk to property was determined by its flood zone according to the FEMA national Flood Insurance Rate Maps (FIRM), occupancy type, and base flood elevation.

Under Risk Rating 2.0, risk is determined based on characteristics of the specific property, including foundation type, the height of the lowest floor of the structure relative to base flood elevation, and the replacement cost value of the structure. The property’s location, including distance to flooding sources, the type of flooding sources (coastal, riverine, and rainfall), and the property’s elevation relative to the flooding source, will all be factored into the risk calculation.23 This more comprehensive approach captures additional environmental variables, including those associated with climate change.

FEMA has not shared how individual premiums under the Risk Rating 2.0 plan will change, but projects that 23 percent of policyholders will see their premiums decrease, and that the vast majority (66 percent) will see increases of $10 or less a month ($120 annually). Seven percent will see monthly increases between $10-$20. Only 4 percent of policyholders will see increases of $20 or more ($240 annually). While it is not known which homeowners will be most affected, FEMA has explicitly highlighted the equity aspects of the new system, pointing out that, “Currently, policyholders with lower-valued homes are paying more than their share of the risk while policyholders with higher-valued homes are paying less than their share of the risk.”24

The First Street Foundation also expects that the majority of policyholders will not see significant changes. But for approximately 265,000 properties, annual premiums may need to reach $10,000 or more to match actual risk. In the historic waterfront city of Charleston, South Carolina, for example, nearly four in 10 flood-prone homes would need to pay an average premium of $18,211 to cover the anticipated costs of flooding, compared to the current average NFIP rate of $2,264.25 Florida, with over 900,000 at risk properties, illustrates the challenge facing NFIP. If all the eligible Florida homes participated in the NFIP, the program would collect $43.65 billion in revenue in the face of an expected payout risk of $307.31 billion, creating a deficit of $263.67 billion over 30 years.26

However, First Street cautions that while the estimates are based on the best available information about FEMA’s approach, all modeling is subject to error. Actual premium adjustments will not be known until Risk Rating 2.0 is implemented. The lack of detailed information on future premiums has created unease among policyholders. It is important to note, however, that per the program’s rules, premiums can rise no more than 18 percent a year.

Equity, Affordability, and Viability

Even with Risk Rating 2.0, concerns remain about both the affordability of individual policies and the financial viability of the program overall. Policy affordability is not a requirement under the NFIP, indeed “FEMA does not have the authority to implement an affordability program, nor does FEMA’s current rate structure provide the funding required to support an affordability program.” This leaves low- and middle-income homeowners in a tough spot: they are required to maintain flood insurance that may rapidly become unaffordable, and that they did not budget for when they purchased their home.

If an affordability program were to be funded from NFIP funds, this would require either raising flood insurance rates for NFIP policyholders or diverting resources from another existing use. Alternatively, an affordability program could be funded fully or partially by congressional appropriation.”27 Legislation proposed by Sens. Bob Menendez (D-N.J.) and John Kennedy (R-La.) attempts to address the affordability issue by limiting annual premium increases to 9 percent. The legislation also calls for flood insurance vouchers for low- and middle-income homeowners and renters for whom flood insurance causes their housing costs to exceed 30 percent of their adjusted gross income.28

As the policy rate changes themselves will not bring NFIP into financial solvency, the proposed legislation calls for a freeze on the NFIP debt interest payments and reinvestment of these savings into flood mitigation efforts.29

Deciding to Go: Managed Retreat Has Begun

Faced with increasing risks and the rising costs of staying on the coasts, some communities are already turning towards managed retreat. In 2012 Hurricane Sandy sped up the East Coast, wreaking havoc across many states before making landfall in New Jersey. The storm inflicted extensive damage on New York’s coastal areas, including Staten Island. In the aftermath, residents of Staten Island’s Oakwood Beach community decided not to rebuild some damaged properties, instead choosing to move away and return the area to wetlands.

For years residents of this low-lying area had been noticing that flooding was becoming progressively worse. During Sandy, however, the storm surge reached 10 feet, destroying nearly 100 homes and damaging many more. Soon after the storm, residents began to discuss the possibility of leaving the homes many had owned for decades or generations.

The slow pace of post-Sandy insurance payouts and low payout amounts is also thought to have contributed to the community’s decision to move away.30

To fund their relocation, residents turned to the federal Hazard Mitigation Grant Program (HMGP),31 which provides buyouts for homeowners who choose to relocate after a storm rather than rebuild. Created in 1988, the program provides homeowners with the fair market value of their property prior to the disaster event. All property sales are voluntary, and communities, not individuals, must apply for this funding.32 Residents of Oakwood Beach also took advantage of State of New York relocation programs that encouraged residents living in very high-risk areas to relocate elsewhere within the city’s five boroughs. In the end, 180 homeowners participated in the buyout program, and the land where their houses once stood reverted to wetlands.

In New Jersey, the new state Climate Change Resiliency strategy also calls for more buyouts of flood-prone areas, allowing their conversion to wetlands to provide a flood buffer and coastal protection.33 The state’s Blue Acres program, created after Hurricane Sandy, has used $300 million in federal disaster recovery funds to purchase 1,300 properties in low-lying areas affected by Sandy or in other flood-prone towns. After demolition, the land will be permanently preserved as public open space for recreational or conservation use.34

Despite its benefits, the HMGP has a major flaw: it only funds property acquisition after storm damage, making it a reactive measure. Some communities are planning for climate resilience before the next big storm hits, and must find other ways to fund relocation and other adaptation measures.

In Punta Gorda, Florida, which was badly damaged by Hurricane Charley, a managed retreat is part of the Climate Adaptation Plan adopted in 2008. “Planned relocation” through mapping vulnerable areas and developing buyout programs for properties that have repeatedly experienced flood loss are part of a multifaceted, comprehensive plan. The relocation of critical infrastructure, such as the Emergency Management Center, to higher ground, imposition of new construction standards, limitations on future development, and the restrictions on further coastal hardening are further elements of the plan.35 Punta Gorda also benefited from earlier decisions in the 1990s to acquire as much shorefront as possible and convert it to parks and preservation areas, instead of homes and other structures.36

Voluntary Buyouts

Voluntary buyouts are a long-established federal policy mechanism to manage flood-prone properties, especially in riverine areas. FEMA or the Department of Housing and Urban Development typically provides three-quarters of the buyout funding, and municipal and county governments administer the programs and fund the remainder.

The first national level analysis of FEMA aid raises questions about the efficacy of the program.

A research team from the University of Miami led by Katharine Mach evaluated data on 43,633 funded buyouts between 1989 and 2017. Buyouts took place in 49 states and three U.S. territories. The number of properties bought out in each of the 1148 counties varied widely, from 1 to 2,190, with a median of 11. Counties that bought out more than 500 properties were located in Texas, Missouri, Alabama, and North Carolina. Harris County, Texas, home to Houston, had the highest number of bought out properties in the country.37

Overall, the study found that wealthier counties, such as those in coastal New England, were more likely to receive funding for buyouts than less well-off areas. The top three states for flood damage—Florida, Louisiana, and Mississippi—ranked 23, 18, and 21 in deployment of buyouts.38 One reason for this trend is that small towns often lack the planning capacity and other resources to apply for and administer the federal funds. Among the major buyout beneficiaries are larger cities such as New York, Houston, and Charlotte.

The study further found that within counties that implemented buyout programs, the specific properties that accepted buyouts were concentrated in areas of greater social vulnerability than the county overall.39 Residents in these areas tended to have lower incomes, education levels, and lower English language proficiency than other areas in the county. They also exhibited greater racial diversity.40

However, due to missing data in the FEMA database, very little is actually known about the individual homeowners who receive voluntary buyouts. The database lacks critical information about the type of home that received a buyout (e.g., single-family residences or rental units) as well as information on how much money was offered to those eligible for buyouts.41

Without information on the socio-demographic characteristics of buyout recipients, it is hard to assess the equity impacts of the FEMA buyout program. But a neighborhood analysis by National Public Radio suggests that the program exacerbates inequality. NPR found that most buyouts were in neighborhoods that were more than 85 percent white and non-Hispanic. This is well above the national level of 62 percent white/non-Hispanic.42

Forced Retreat—The Federal Use of Eminent Domain

Traditionally, buyout programs for coastal communities have been voluntary, with homeowners proactively deciding to sell their homes. But this practice appears to have quietly changed—opening the way for the use of eminent domain to mitigate climate risk.

The practice of eminent domain allows the government to expropriate private property, with compensation, for public use. The U.S. government has often used its powers of eminent domain to acquire land for key infrastructure, such as a road or bridge.

At the end of 2015, the U.S. Army Corps of Engineers (USACE) published a revised Planning Bulletin with the subject line: Clarification of Existing Policy for USACE Participation in Nonstructural Flood Risk Management and Coastal Storm Damage Reduction Measures. This bulletin opened the way for the Army Corps to use eminent domain to relocate residents in flood-prone areas who do not want to leave on their own. In it, the USACE stated (emphasis added):

“In order to have a complete plan, the ability to use eminent domain must be retained and a condition of an implementable project. A 100-percent voluntary acquisition, plan for acquisition relocation, and permanent evacuation is not considered a complete plan and is not acceptable for USACE participation. All future acquisition, relocation and permanent evacuation recommendations for USACE must include the option to use eminent domain where warranted.”43

This quiet yet remarkable policy shift links access to federal funds for disaster recovery and climate change mitigation to the local government’s willingness to use eminent domain. Indeed, despite typically stringent Republican resistance to the use of eminent domain, the Trump Administration promoted this approach.

In Nashville, Tennessee, 44 homeowners whose properties abut a creek were informed in 2019 that they were eligible for a buyout program. However, the city told residents that if they chose not to participate, the city could acquire the homes through eminent domain. Some of the residents do not want to sell, including a 98- and 99-year-old couple, and the City of Nashville is now in a difficult position of needing to remove these residents in order to fulfill their obligation to the federal government.44

Deeply entwined in this issue are feelings, among both the public and elected officials, about individual property rights and the historical legacy of the use of eminent domain, especially in marginalized communities. In the face of controversy, the attempt to force local governments to use eminent domain may be discouraging local governments from pursuing buyouts at all, thereby failing to reduce flood risk.

Flood-prone Charleston, which had already purchased dozens of homes in voluntary buyout programs, has ruled out the use of compulsory buyouts in current projects.45 Similarly, the State of New Jersey, which has extensively leveraged the voluntary buyout program in the past to purchase over 700 properties, has resisted the inclusion of eminent domain.46

In the Florida Keys, Monroe County has also decided against the use of eminent domain. In 2018 the county embarked on a three-year multi-million-dollar study in partnership with the U.S. Army Corps of Engineers to study storm risk and develop a mitigation plan. The study examined means to stabilize critical infrastructure threatened by storms, especially U.S. 1, the only road that connects the keys to the mainland, and assessed the risk to over 4,000 residential properties.

An initial draft of the plan, presented in February 2020 to the Board of County Commissioners, included the potential forced acquisition of vulnerable homes.47 But county leadership pushed back on the requirement to include eminent domain in the plan, and requested “a formal waiver related to mandatory land acquisition” from USACE in April 2020, hoping to make any land acquisition voluntary.

In its letter, the county questioned the statutory requirement that acquisitions be mandatory.

“Where is the citation in rule or statute that requires acquisition be mandatory?” the letter read, “And that a homeowner cannot choose elevation over acquisition?”48

The number of homes designated for buyout ranged from approximately 225 to 286,49 a very small number of the total structures under consideration in the plan. No written response to this request is included in the plan’s final documents. However, the Monroe County website states:

“USACE removed all acquisitions from the plan after additional analysis determined it was less cost-effective compared to the elevation of homes.”50

The final recommended plan, which needs congressional authorization and funding approval, calls for elevating 4,687 structures, stabilizing U.S. Route 1, and flood-proofing 1,130 structures and 48 pieces of critical infrastructure.51 If approved, the federal government will pay 65 percent ($1.7 billion) of the plan’s overall $2.6 billion cost, and non-federal sources, such as the county and municipalities, will cover 35 percent ($893 million). An estimated $1.2 billion is needed for Key West alone, where 43 percent of the houses to be elevated are located.52 It is not clear yet where the remainder will come from, but sources could include state resources and property owners themselves. However, participation in the mitigation plans, such as elevating and floodproofing, is voluntary.53

Conclusion

Coastal communities have begun to respond to the rising threat of sea level rise and increased storm damage. Their approaches range from full retreat to staying in place but increasing resilience, and are often a combination of the two. The Federal government has no comprehensive plan, nor policy toolkit, for how to meet a threat that potentially affects over 29% of the US population, more than 94 million people. Instead, Congress and different agencies are left to enact small fixes that fail to holistically mitigate the threat.

Though Risk Rating 2.0 will increase premiums for some property owners, overall the program is likely to experience continued financial crises as the rate of payouts exceeds premiums collected. In the short term, at least, many people will continue to live in homes and communities at risk of substantial flood damage.

In requiring the use of eminent domain, the Army Corps of Engineers ostensibly created the federal government’s first compulsory managed retreat policy by linking its usage to federal aid eligibility. No public documentation exists on what led to this decision, but it raises an important, though uncomfortable, issue – are there properties that cannot or should not be saved from sea-level rise? If so, what are the criteria for selecting these properties and through what process should ‘retreat’ occur? What is the danger that coastal retreat will disproportionately impact low to moderate income homeowners?

In the eight months since President Biden took office there have been two major storms resulting in Major Disaster Declarations in five states. Guidance is needed at the federal level, beyond current FEMA policies that are focused primarily on post-disaster relief, to help communities meet the rising risk on our coasts.

Downloads

Citations

- Cohen, Darryl, “94.7M Americans Live in Coastline Regions: About 60.2 M Live in Areas Most Vulnerable to Hurricanes”, U.S. Census Bureau, July 15, 2019. Last modified 08/18/2020 source

- “Fast Facts: Economics and Demographics”, National Ocean and Atmospheric Administration, Office of Coastal Management. Last modified 09/01/2021, source

- Cohen, “94.7M Americans Live in Coastline Regions: About 60.2 M Live in Areas Most Vulnerable to Hurricanes”.

- Wamsley, Laurel “Hurricane Michael Was A Category 5, NOAA Finds — The First Since Andrew In 1992”, National Public Radio, April 19, 2019; Last modified, April 22, 2021. source

- “Introduction to Storm Surge”, NOAA, National Hurricane Center, no date, source

- Wagner, Adam “Will Climate Change and a Rising Ocean Mean the End of the Road for NC Highway 12?”, The News and Observer, August 9, 2021, source

- Popkin, Gabriel “Fourteen Percent of U.S. Coastline is Covered in Concrete”, Science, August 18, 2015, source

- Rasmussen, Carol “Study Projects a Surge in Coastal Flooding, Starting in 2030s”, NASA, July 7, 2021 source

- Raim, Laura. “Florida’s Flooded Future: Retreat While There’s Still Time”, The Nation, June 8, 2020 source

- Hampton, Jeff “Avon beachfront property owners facing 62% property tax hike ot pay for beach widening”, The Virginian-Pilot, March 16, 2021source

- Harris, Alex,“Miami’s sea level rise bill is $4 billion by 2060. It won’t keep every neighborhood dry”. The Miami Herald, April 23, 2021. source

- “‘The Keys Are Not Going To Save Everybody’: Officials Could Let Roads, Homes Be Swallowed Up Rising Sea”, CBS Miami, December 4, 2019 source

- Introduction to the National Flood Insurance Program NFIP, Congressional Research Service, January 5, 2021. source

- Kyle Bagenstose, Dinah Voyles Pulver and Kevin Crowe, “Flood-prone homeowners could see major rate hikes in FEMA flood insurance changes, new study finds”, USA Today, February 21, 2021. source

- Berkowitz, Ben“Irene send floundering flood insurance program further underwater”. NBC News, August 30, 2011, source

- Highlights From "The Cost of Climate: America’s Growing Flood Risk", First Street Foundation, February 21, 2021 source

- Introduction to the National Flood Insurance Program NFIP, Congressional Research Service, January 5, 2021. source

- Highlights From "The Cost of Climate: America’s Growing Flood Risk", First Street Foundation, February 21, 2021, source

- Rush, Elizabeth, “ Leaving the Sea: Staten Islanders Experiment with Managed Retreat”, Urban Omnibus, February 11, 2015. source

- Harrington, Jeff “Flood Rate Relief In Sight for Manatee Homeowners”, Bradenton Herald, November 11,2013, source

- Homeowner Flood Insurance Affordability Act of 2014, Public Law 113-89, source

- “Risk Rating 2.0: Equity in Action” FEMA, source

- source 99/5

- “Risk Rating 2.0 – National Rate Analysis”, FEMA source

- source,

- First Street Foundation, “The Cost of Climate: America’s Growing Flood Risk”, February 2021, source

- Congressional Research Service, “Introduction to the National Flood Insurance Program”

- source

- source

- Rush, Elizabeth “Leaving the Sea: Staten Islanders Experiment With Managed Retreat”, Urban Omnibus, February 11, 2015 source

- “Hazard Mitigation Assistance Grants”, FEMA, source

- source

- Oglesby, Amanda “Shore climate change: NJ plans more buyouts in frequent flood areas”, Asbury Park Press, April 23, 2021 source

- “Blue Acres Buyout Program”, reNew Jersey Stronger, no date, source

- Adaptation Plan Update source

- Weissman, Jack Marcus, “How to Prevent a Flood Disaster: Using Law and Policy to Systematically Reduce Risk”, Columbia Climate School, August 20, 2021 source

- K. J. Mach, C. M. Kraan, M. Hino, A. R. Siders, E. M. Johnston, C. B. Field, Managed retreat through voluntary buyouts of flood-prone properties. Sci. Adv. 5, eaax8995 (2019).

- Niler, Eric “Wealthy Counties Benefited Most From a Flood Relief Program”, Wired, October 9, 2019 source

- K. J. Mach, C. M. Kraan, M. Hino, A. R. Siders, E. M. Johnston, C. B. Field, Managed retreat through voluntary buyouts of flood-prone properties. Sci. Adv. 5, eaax8995 (2019).

- K. J. Mach, C. M. Kraan, M. Hino, A. R. Siders, E. M. Johnston, C. B. Field, Managed retreat through voluntary buyouts of flood-prone properties. Sci. Adv. 5, eaax8995 (2019

- K. J. Mach, C. M. Kraan, M. Hino, A. R. Siders, E. M. Johnston, C. B. Field, Managed retreat through voluntary buyouts of flood-prone properties. Sci. Adv. 5, eaax8995 (2019).

- Hershey, Rebecca and Robert Benincasa “How Federal Disaster Money Favors the Rich”, National Public Radio, March 5, 2019 source

- “Planning Bulletin PB 2016-01” U.S. Army Corps of Engineers, December 22, 2015 source

- Flavelle, Christopher “Trump administration presses cities to evict homeowners from flood zones”, The New York Times, March 11, 2020; source

- Army Corps Plan for Charleston Flooding Won’t Include Buyouts

- source

- source">Army Corps of Engineers plans for storm resilience

- “Florida Keys Coastal Storm Risk Management Feasibility Study, Monroe County Florida, Draft Integrated Feasibility Report and Environmental Impact Statement, Appendix X, Correspondence with Non Federal Sponsor”, June 2020 source

- USACE planning documents mention approximately 225, Monroe County Board of County Commissioners minutes say 286.

- “Monroe County: Sustainability” source

- Haug, Rachel, “Florida Keys Coastal Storm Risk Management Feasibility Study, Final Recommended Plan Briefing”, February 2021 source

- Klingener, Nancy “The $2.8 Billion plan to protect keys from flooding now includes raising homes, floodproofing – but no buyouts”,WLRN, May 5, 2021 source

- Klingener, Nancy “The $2.8 Billion plan to protect keys from flooding now includes raising homes, floodproofing – but no buyouts”,WLRN, May 5, 2021 source

More About the Authors

Dona Stewart

Fellow, Future of Land and Housing

Issues

Programs/Projects/Initiatives

Related

Climate Change, Housing, and Homeowners Insurance in Florida: Lessons for California