Insights for Better Loan Offerings

During the last two design sessions, participants spent time writing down and then talking about where they would go first to find money for one of two scenarios. This allowed people to first share their thoughts with us, without external influence, and then to work through different options as a group. The two scenarios were:

- Scenario A: A big bill is always due one week before your paycheck. You need $200–$250 every month, knowing you will be able to pay it off soon.

- Scenario B: An unexpected emergency costs you $1,000–$2,000 and you will need to pay it off over time.

In the first session, people also discussed where they had learned about loans in the past and designed their own loans for similar scenarios. These discussions showed us who borrowers trust for loan information, who is considered a trusted lender, and what loan features may be most appealing.

Meegan Dugan Adell/New America

Trusted Messengers and Lenders

With many payday and auto title lenders closing their brick-and-mortar locations in Illinois because they are unwilling to abide by the PLPA’s 36 percent APR cap, it is more important than ever for households to be steered toward safe, affordable lending alternatives. However, it can be difficult for consumers, particularly those from Black or other communities of color, to trust financial institutions that have been discriminatory in the past. We wanted to better understand where consumers go for information they can trust about small dollar loans. With a better understanding of what sources they trust, resources and financial information can be more effectively shared with these consumers. The points below outline issues and differences that lenders serving these communities should be aware of.

Lack of Trust in Financial Institutions

Several people in our groups mentioned that many in their communities feel safer keeping their money at home than in banks. This was particularly true among the Latina participants in our Logan Square design session. There was also significant fear in that community around taking out a loan and being trapped in a cycle of debt. Among Black participants in our groups, several mentioned a distrust of both banks and online apps. Several felt they are likely to be taken advantage of and that they lack power in the relationship. Some didn’t like the fact that lenders can sell their information to other companies. Participants in general were also worried about the risk of giving an app or lender direct access to their accounts, as they may not be able to manage when different payments are deducted. Others were concerned about or had experienced fraud on online apps, including scams that clean out a person’s bank account. Across races, multiple participants felt frustrated that lenders held borrowers accountable for their part of the original agreement but can change interest rates or make other changes that borrowers might not have agreed to.

Lack of Common Trusted Messengers

Residents didn’t identify one common source of trusted information about borrowing. People from all neighborhoods seemed to be unsure about where to go, particularly for higher amounts, and had a variety of different trusted messengers. Most residents said that family members, friends, credit unions, and online resources like Google searches, Credit Karma, Trustpilot, and the Better Business Bureau are the best way to learn about a loan or check out a lender. A handful of people trusted the banks they had accounts with. Several people said they would trust a local nonprofit if it offered help. A few people mentioned low- or no-interest options from their employers. At the end of each session, multiple people asked the facilitators if there was some trustworthy place where they could find information.

Differences between Generations

Respondents indicated that different generations seemed to trust different types of messengers, with younger people using social media sources such as Instagram, Reddit, TikTok, YouTube, or X (formerly Twitter). Middle-aged people mentioned relying on Google searches; websites like Credit Karma, NerdWallet, or WalletHub; Facebook groups and other social media; or online reviews of companies. Much older people trusted television shows or news programs, such as Univision in the Latino community. Some participants were worried that young people might be getting bad information on social media, while several Latina participants were impressed by how helpful these sources had been for teaching their teen or young adult children about money management.

Cultural Differences for Larger Loans

For larger expenses, like an emergency requiring $2,000, talking to family and friends was the first choice, with some variation. People in the Latino community expressed a strong cultural aversion to taking loans from financial institutions and strongly preferred to ask family and friends. Most didn’t even suggest taking out a loan as an option and would rather sell or possibly pawn something if they couldn’t receive help from family or friends. People in the third group of primarily Black residents considered a variety of options but were slightly more likely to mention taking out an online or loan-store loan as an option. Asking family or friends was a close second. Gig work was a popular choice as well. Only one person mentioned using a credit card.

Preference for Asking Family and Friends for Small Loans

For a smaller loan, like for a bill that comes before payday, there was not one common answer across groups, although asking family and friends was one of the most common answers. This was slightly more popular with people in the predominantly Black South Side design session. For people in the entirely Latina Northwest Side session, the answers varied more, including online loan options, saving money, and asking for an extension, in addition to support from family and friends.

Confusion about Credit Unions

In our two design sessions hosted within Black and Latino communities, several people seemed to be confused about how credit unions work, whether they qualified to use a credit union, or whether they had to be employed in a specific place to use one. Just a few people in each group had had a good experience taking out car, home, or other loans with credit unions, but they spoke of them in glowing terms, which interested others in the option. Our first group, recruited from multiple neighborhoods, seemed to be more familiar with and trusting of credit unions.

“Even nowadays, some people still don’t trust banks. Banks are not very friendly towards people with ITINs. It took me years to build credit, for example.” —Michelle, 44, Logan Square

“The best way [to find out about a loan] is a family member or friend. They’ve already gone through the experience, and they can help guide you.” —James, age unknown, South Chicago

Desirable Loan Features

Some literature has shown that even with the closure of payday loan stores, people still do not tend to switch to more traditional credit instruments like credit cards or small personal loans from banks, finance companies, and retail stores.1 Additionally, it has been found that most current payday borrowers prefer higher-priced but less restrictive standard payday loans over lower-priced but more restrictive alternatives offered by institutions like credit unions.2 Only a handful of participants in each design session thought of banks or credit unions as a source for short-term, small dollar loans, so understanding what residents were looking for could help these institutions better meet community lending needs in their service areas. The following are some of the features in small dollar loans that consumers in our groups were looking for but perceived were not available in existing products.

Clear, Simple Process with a Rapid Turnaround

Participants had made calculated choices to take on higher APR loans in part because they knew how much they would receive and that they would receive the loan within one-to-two business days. Consistent with other research, we know that loans with clear processes—just a handful of steps, quick turnaround, and simple parameters that determine who is eligible for how much money—are crucial for consumers, especially in times of emergency.3

Options for Eligibility

Across all of our groups, having different ways of getting approved for loans was important. Some had good payment history or income but were self-employed, had poor credit, or had an online bank account that wasn’t part of the data transfer network used by many banks. Many participants felt that loans should be granted based on pay history or proof of income rather than credit score.

Options for Online Access

Having an online application and multiple online options (for example, an easy-to-use website or app) was a must-have for most people. However, there were limitations. Many people were concerned about online fraud and identity theft, so some weren’t open to loans from apps rather than a brick-and-mortar location they could visit in case there was an issue. Many people were also concerned about giving online apps full access to their checking accounts.

Ability to Manage Monthly Costs

People want more flexibility with loan payments, dates, and options for how many payments are expected per month.

Credit and Wealth-Building Features

Many participants would welcome elements that help build their financial security and wealth, although this doesn’t surpass ease of use on the wish list. Consumers wanted rewards for early repayment and credit-building features, and they appreciated wealth-building features like earning shares in the lending institution.

Just-in-Time Financial Coaching

Financial literacy coaching to answer questions when they arise, as well as individualized support throughout the loan process, would help borrowers know about the options available to them and the best path toward financial security. This is consistent with substantial research that suggests that financial literacy education has a limited impact on behavior, in part because people don’t retain the information as early as six months later.4

“I lost a car going through a title loan. They didn’t call me or tell me anything; $300 for a $10,000 car. I lost it. This was not too long ago. It’s ridiculous, the sacrifices people make.” —Barbara, 56, Belmont Cragin

Designing Simple Loans

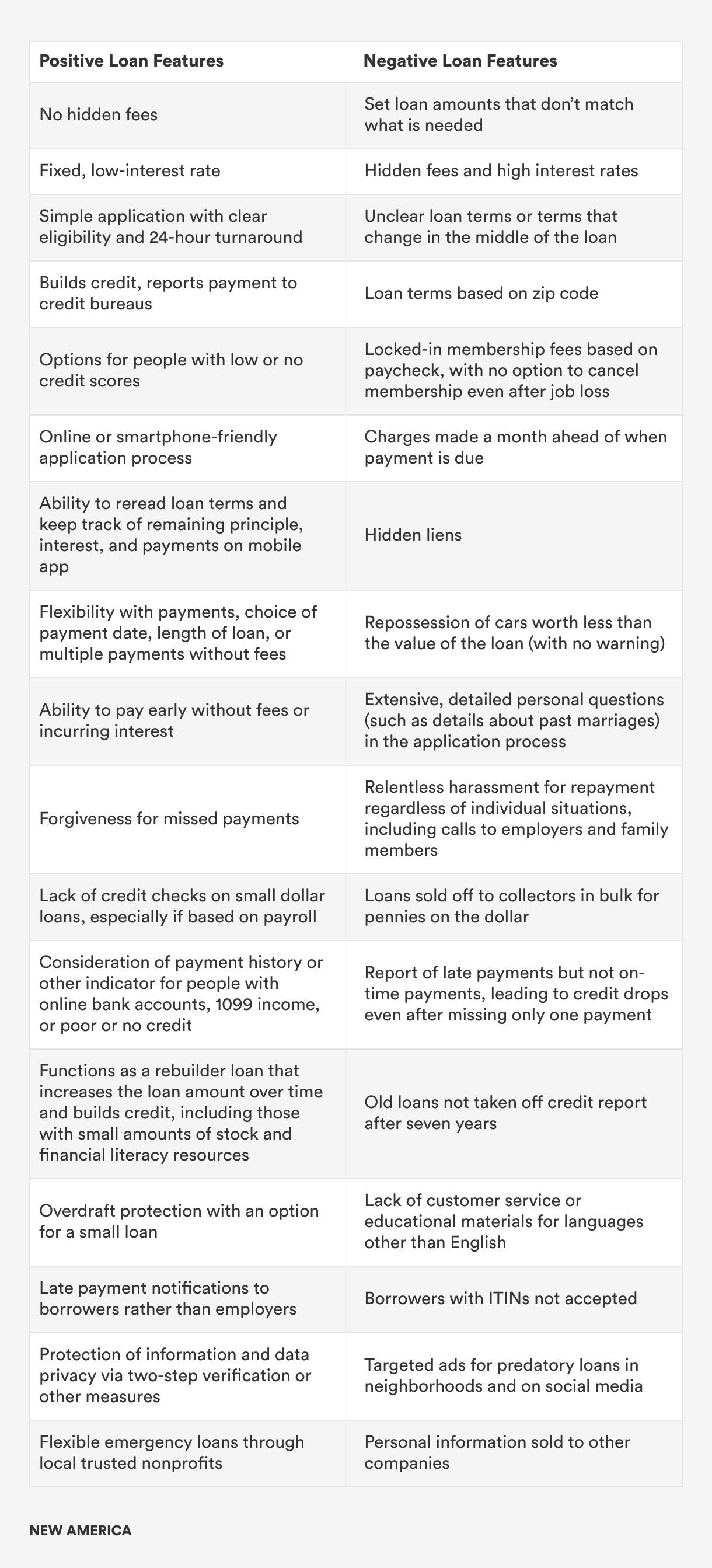

During our group activities, participants contributed to a list of the best and worst loan features from their experiences borrowing or needing small dollar loans.

At the end of the first event, participants were asked to design their own ideal loan and vote on each other’s designs to uncover the most popular features. Participants were split into two groups: one group designed a $200 loan that a borrower would need consistently each month, and the other group designed a $1,000 loan for a one-time emergency. From the lists of features they generated, participants picked two “positive” features and one “negative” feature to form a loan that would be useful to them and identify trade-offs they were willing to make.

The most popular loan for consistent access to a smaller sum included one that had no credit check and a low interest rate with no increase if it is paid on time, with the downside that borrowers get approved through their current debt status rather than their paycheck. For the $1,000 one-time infusion loan, the most popular loan was one that had no fees and helps borrowers build or rebuild their credit, with the downside of harassment for late payments. Residents defined harassment for late payments as incessant phone calls and email reminders about payment status.

The least popular loan option for consistently borrowing a smaller sum offered forgiveness for a missed payment and no fees, but also included a membership that borrowers were not able to opt out of even if they no longer needed the loan option. For the larger emergency loan amount, the least popular featured design was a loan that had a flexible payment plan with an accessible mobile app but offered no customer service.

Vanessa Rangel/New America

Consumer Responses to Currently Available Loans

Updated at 2:19 p.m. on April 3, 2024: This section has been changed to clarify the use of the term “credit union” as it pertains to the research methodology. The term was also removed from both tables.

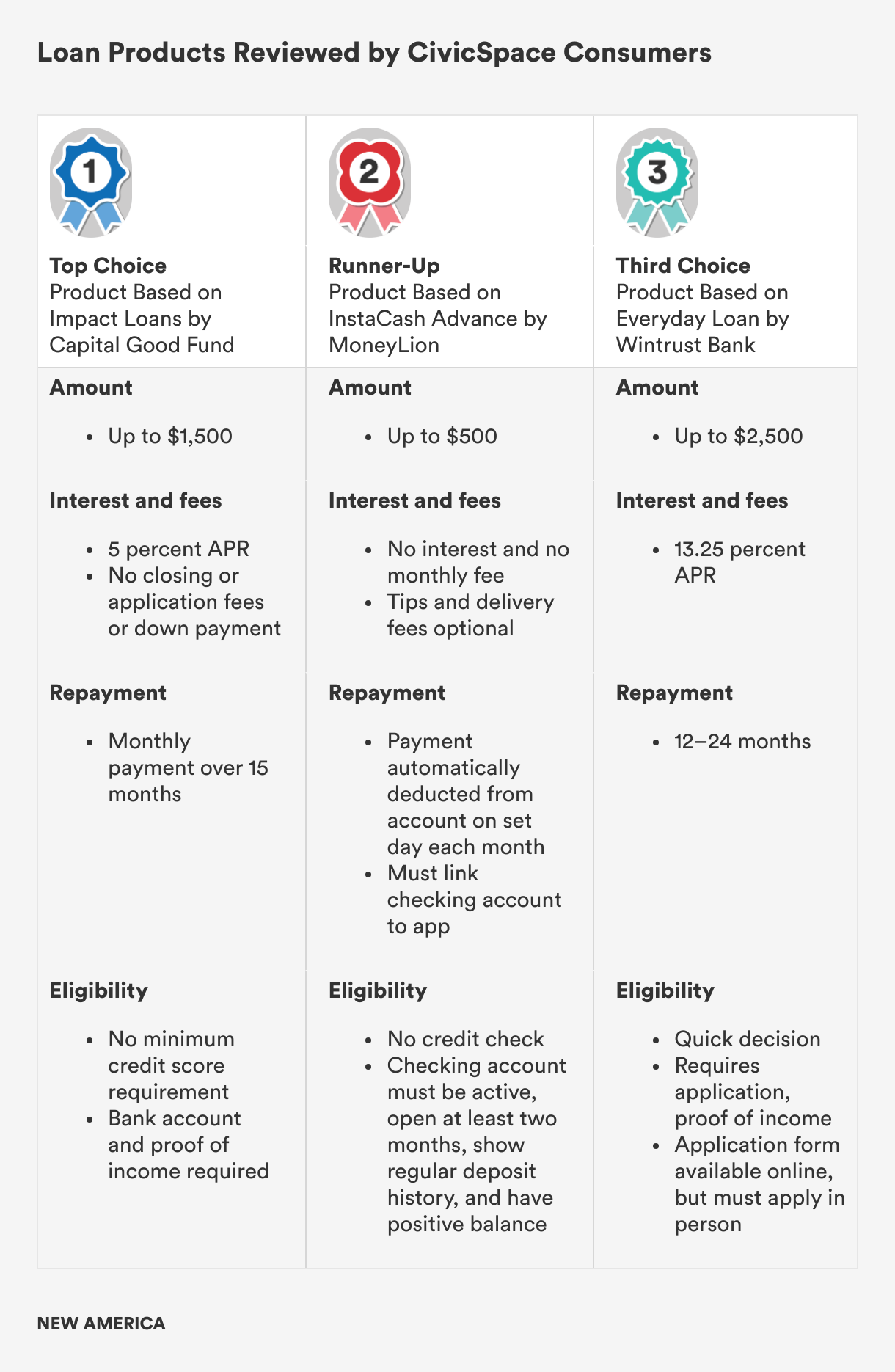

In the last two groups, we again split participants into two scenarios and asked them to respond to three real loan products with the two scenarios in mind: a regular $250 loan for an ill-timed bill or a one-time emergency loan of $2,000. We increased the loan amounts for each scenario in the last two design sessions to reflect the higher cost of living in 2023. We also concealed the sources of these loan products and only shared a description of the products and key features.

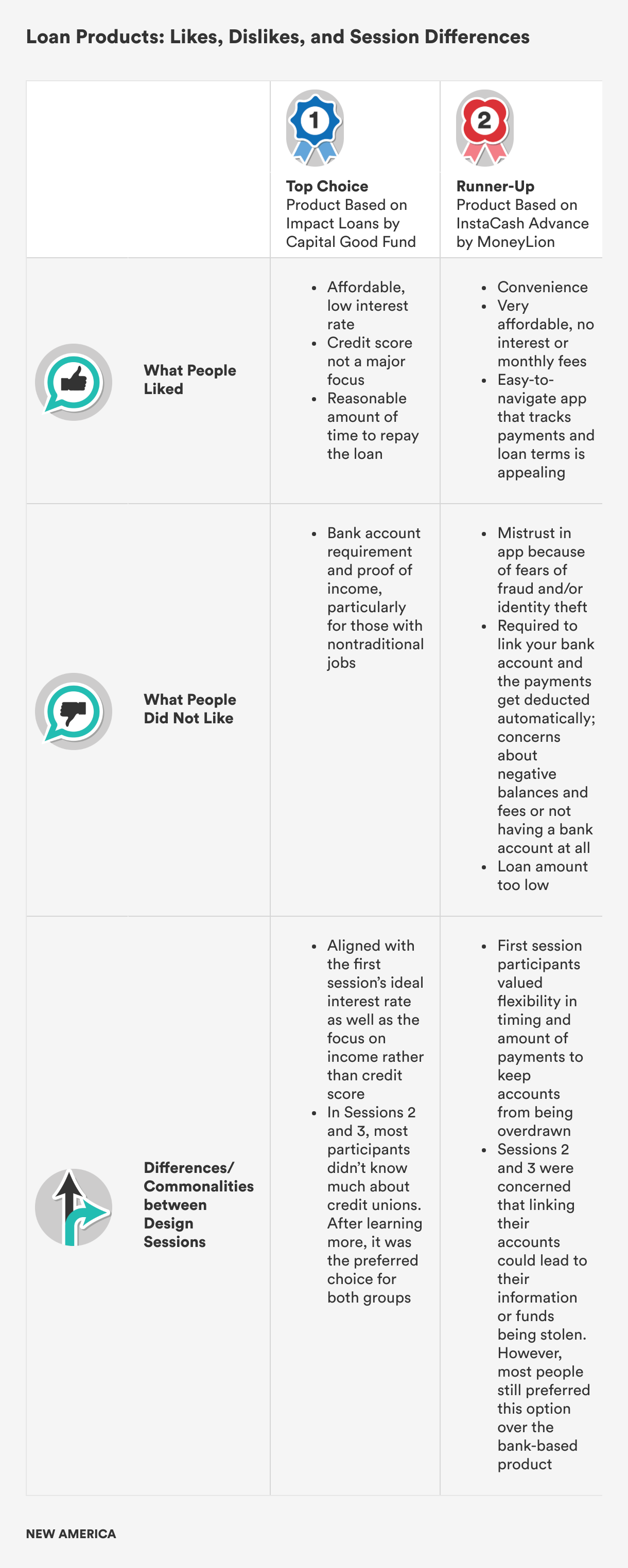

The credit union loan was the most popular choice for both scenarios. (Note: Capital Good Fund is a community development financial institution. However, in order to understand people’s reactions to online, credit union, and bank products, we left out the lender names and used the word credit union to describe this product.) In both groups, once residents learned more about how credit unions worked from their peers, the credit union loan product was the top choice due to its fair and affordable loan terms.

The least favorite loan product among the two groups was the bank branch product. Many participants from the predominantly Latina and Black groups were concerned about whether they would even be approved for a traditional bank loan and felt that it would be a waste of their time to apply in person. They assumed there would be requirements for eligibility that are not listed and that they likely would not meet. Both groups also thought the 13.25 percent interest rate was high compared to the other products and questioned how quick the approval process would actually be.

The online app-based loan fell in the middle. Some participants loved the idea; others hated it, especially those who had had experiences with identity theft. Participants really appreciated the convenience and affordability of the product, but it was difficult for most to overcome the fact that it was a completely online product not attached to a physical institution and that the loan was directly linked to a personal checking account. It gave the lender too much power over their finances without enough online security to reassure participants that their checking accounts were protected. The risk did not feel worth the $500 loan amount; however, this design shows promise, particularly if the security concerns are addressed.

Citations

- For example, see Neil Bhutta, Jacob Goldin, and Tatiana Homonoff, “Consumer Borrowing after Payday Loan Bans,” Journal of Law and Economics 59, no. 1 (February 2016): 225–59, source.

- See Victor Stango, “Some New Evidence on Competition in Payday Lending Markets,” Contemporary Economic Policy 30, no. 2 (April 2012): 149–61, source.

- See Caetano et al., Increasing Applications for Small Dollar Loans, source.

- For example, see Daniel Fernandes, John G. Lynch, and Richard G. Netemeyer, “Financial Literacy, Financial Education, and Downstream Financial Behaviors,” Management Science 60, no. 8 (August 2014): 1861–83, source.