Table of Contents

I. Learning: Awareness and Exploration

The first breakdown often happens before someone even considers claiming credits on their tax return: Many people either don’t know tax credits exist or don’t believe it’s worth going through the intensive filing process when they aren’t required to file based on their income.

Awareness Gaps Keep Eligible People from Accessing Credits

While filing taxes is an obligation for some, it is an opportunity for many others. For low-income households—especially those below the filing threshold—not filing is often not about apathy or avoidance. It is a genuine belief that they don’t need to or are not allowed to file.

“I only work side jobs, so I don’t have enough money to file.”

—Survey respondent, living in a household with one child under six years; $10,000–$25,999 annual household income; hadn’t filed taxes in three years

“I have yet to reach an income that requires [me] to file for taxes.”

—Survey respondent, employed with multiple employers; <$10,000 annual household income; hadn’t filed taxes in three years

People repeatedly told us, “I don’t make enough to file.” While this is often legally true, it can come at a real financial cost—many were still likely eligible for tax credits even if they weren’t required to file.

Among low-income households earning under $26,000 that hadn’t filed taxes in the past three years, one-third (33 percent) said they didn’t file because they believed their income was too low. Yet within this group, 20 percent had earned income from work (including jobs with one or more employers, gig or freelance work, or self-employment), and 37 percent had at least one child in their household—factors that likely would have made many of them eligible for tax credits had they filed.

“I’ve never heard of tax credit[s].”

—Survey respondent, living in a multigenerational household with one child; <$10,000 annual household income; hadn’t filed taxes in three years

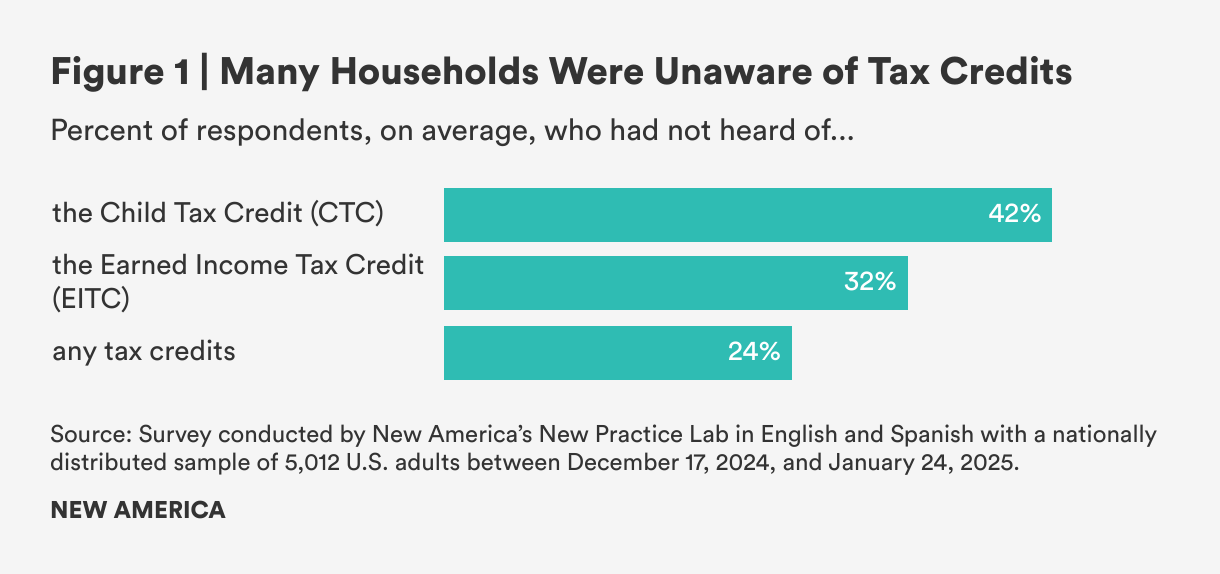

When asked about their awareness of tax credits, on average, 42 percent of households had not heard of the Child Tax Credit (CTC); 32 percent had not heard of the Earned Income Tax Credit (EITC); and 24 percent had not heard of any tax credits.

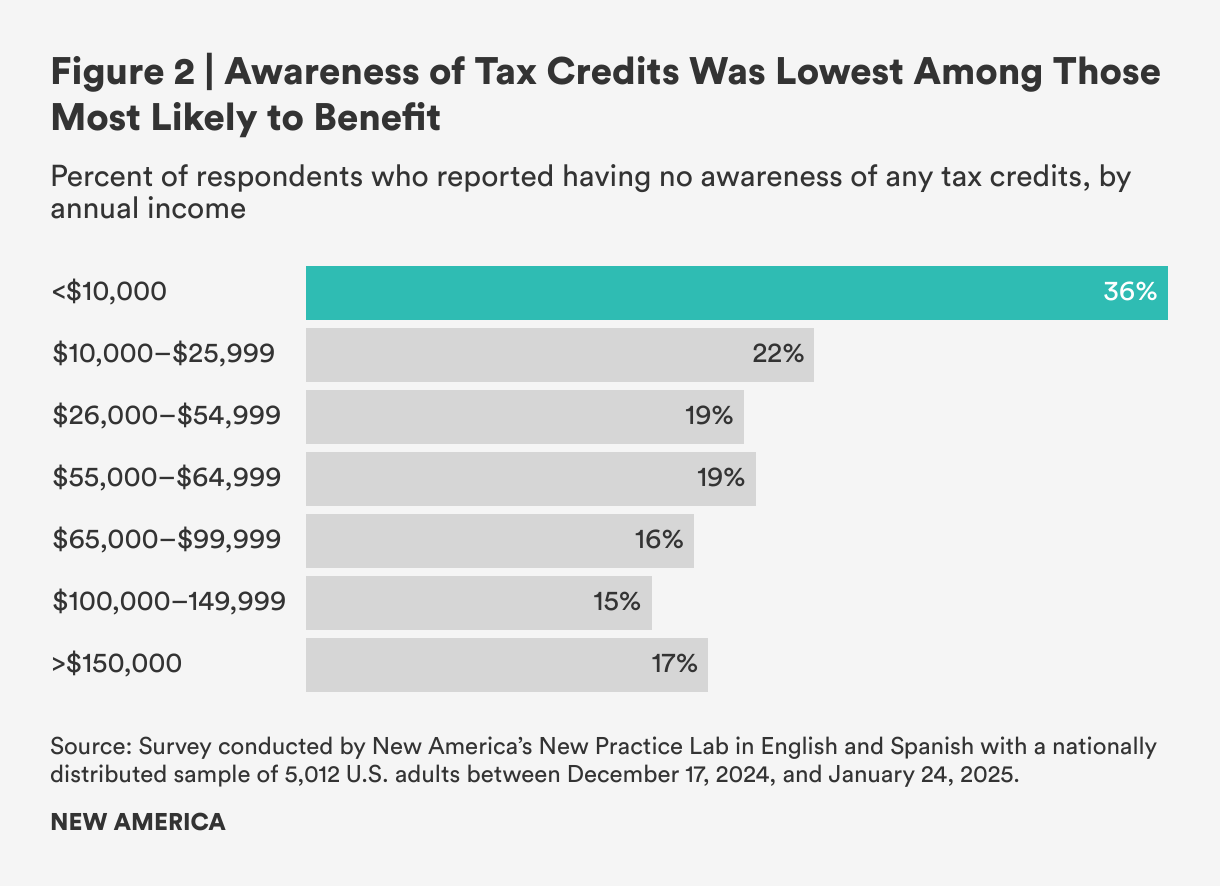

Awareness was lowest among those most likely to benefit. Among households earning under $10,000 annually, 36 percent were unaware of any tax credits, more than double the rate among households earning over $150,000 (17 percent). Within this lowest-income group in our survey, 40 percent of employed households hadn’t heard of the EITC, and 47 percent of households with children hadn’t heard of the CTC.

When asked why they had not claimed credits, low-income non-filing households cited overlapping concerns: 40 percent believed their incomes were too low to qualify, 24 percent found it challenging to understand which credits they were eligible for, 16 percent were worried that claiming credits might affect other benefits like Medicaid or the Supplemental Nutrition Assistance Program (SNAP), 16 percent didn’t know how to claim credits, and 12 percent said they couldn’t find the help they needed. A few more shared “other” reasons but did not mention the specific reasons or restated previous reasons worded differently.

Some people, like those receiving Social Security Disability Insurance (SSDI), were especially confused about their tax eligibility, particularly when they were simultaneously employed. Twenty-five percent of SSDI recipients in our sample reported employment, but 55 percent of these employed SSDI recipients had not filed taxes at all, and another 14 percent had filed inconsistently. While SSDI alone doesn’t qualify someone for the EITC, many of these individuals may still have been eligible based on their earned income.

“I don’t have to file because I never make enough.”

—Survey respondent, employed with one employer and receiving SSDI payments; $10,000–$25,999 annual household income; hadn’t filed taxes in three years

“I find knowing how to start challenging. I have questions like who do I connect with, and how will my income be affected? It’s a lot of steps that don’t always appear coherent.”

—Illinois study participant, receiving SSDI payments

Some simply assumed they were doing everything right, until asked more directly. Their filing habits had become routine, shaped by early experiences or advice that hadn’t changed over time, even as their life circumstances did. This kind of path dependency, or “status quo bias” (repeating what’s familiar without re-evaluating), can prevent people from realizing that tax credits might help in new ways. When awareness of credits was low—especially during major life changes like becoming a caregiver or taking on new forms of work—it was easy to overlook that tax filing could offer meaningful support.

“I never thought about [tax credits]…I just filed my taxes the same way I have been doing since I was 17 years old.”

—Survey respondent, 35–44 year old legal guardian/foster parent to two children; <$55,000 annual household income; had filed taxes every year for the past three years but had never claimed tax credits

In our Illinois interviews, several participants were surprised to learn that they were eligible for credits, especially after we clarified that different types of labor, like gig work, caregiving, or selling goods online, could count toward income. Slightly different eligibility rules across federal and state programs added to the confusion.

“Oh, so I can file taxes if I was an Uber driver? I didn’t know that!”

“That’s awesome that I can include income from driving and selling goods online…I did not know that.”

“I didn’t even know you can get an income credit on state taxes…I didn’t use to file state because I didn’t want the state to take it from me. Maybe had I known, it might have boosted me up to pay off those tickets, and I still would have gotten a portion back.”

Tax credit programs are designed to reward work and caregiving by providing financial or family support, but the impact of these incentives is limited when people don’t know they exist.

Diverse Motivations and Multiple Sources of Information Shape Credit Uptake

Across our survey and qualitative research in Illinois, one theme stood out: Families don’t think about taxes in one uniform way. While some file annually, others file occasionally or not at all—often based on whether the refund feels “worth it,” and whether they trust the process or fear it will interfere with other benefits.

Their motivations, filing behaviors, and barriers are shaped by life experiences, financial pressures, and personal networks.

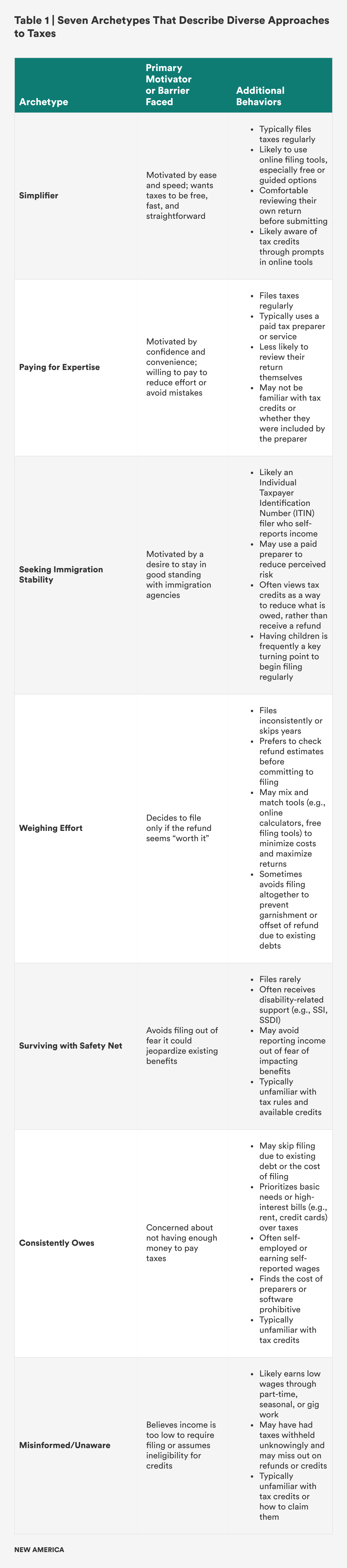

Within the families we spoke to in Illinois, we identified seven behavioral archetypes that help explain these patterns:

- Simplifier: wants taxes to be free and fast; avoids unnecessary steps

- Paying for Expertise: will pay for filing to reduce risk or effort

- Seeking Immigration Stability: wants to remain in good standing with immigration agencies

- Weighing Effort: will file only if the refund feels “worth it”

- Surviving with Safety Net: worries that filing could jeopardize benefits

- Consistently Owes: may have other debts that are a higher priority to pay than taxes

- Misinformed/Unaware: believes income is too low to file or assumes they’re ineligible for credits

Table 1 below outlines each behavioral archetype along with their primary motivations or barriers to filing, and highlights behavioral patterns that may shape how they approach taxes and tax credits.

Simplifiers may respond to language about ease and speed: “File in 10 minutes, for free.” Those worried about benefit loss might appreciate reassurances: “Filing won’t impact your SNAP or housing.” Those misinformed or unaware may need help understanding why they should file or that they were eligible for credits.

This variety matters. Standard messages about “filing for tax credits” can miss the mark, especially for those who don’t plan to file or who don’t associate taxes with benefits. In fact, families we interviewed in Illinois said that language about “missing money” or “extra income” resonated far more than tax-specific terms like “credits” or “returns.” This is consistent with findings from quantitative studies in behavioral science that emphasize amounts lost.

The qualitative study in Illinois explored how behaviors, motivations, and barriers around taxes and government benefits could influence which introductory messages an individual prefers when learning about a new state tax service. The findings suggest that “one-size-fits-all” messaging was generally less effective than more tailored approaches. Given a range of sample text messages, nearly every participant selected at least one message that corresponded with an archetype reflective of their screening responses and many also chose messages that spoke to secondary motivations, highlighting the value of segmentation in communication design.

Participants in our Illinois study reflected on how the test messages they received seemed to cater to their unique needs:

“They were direct and used the right tone. It’s like they are helping me out instead of just giving the message.”

“[The message] felt relevant to me considering I pay to get help with my taxes, so I’m definitely interested in learning about the easier way that is free.”

Timing mattered, too. Many people in our interviews said they wanted to learn about tax-related opportunities early in the fall—before commercial tax preparers start calling, and to give them plenty of time to learn about the program ahead of the next tax season. They also suggested syncing with tax season to provide actionable reminders, which could be especially helpful for those less familiar with the system and have also previously been shown to make a difference in increasing filing.

In addition to motivations and timing, our survey highlights the central role played by trusted messengers. The survey revealed that people turn to a range of sources when learning about government benefits and tax credits, and, on average, the most utilized channels for gathering information were:

- Friends, neighbors, or family (49 percent)

- Google or other online searches (48 percent)

- IRS website (42 percent)

- In-person preparers (38 percent)

- Online tax software (25 percent)

Importantly, people reported turning to multiple sources: On average, people named at least three trusted sources, underscoring the importance of multi-channel outreach. As one survey respondent put it:

“I decipher information from a combination of places before making a decision.”

For most, trusted messengers are personal—a friend who’s done their taxes before, a daughter who keeps up with tax rules, or a family member who works as a preparer. Participants in the nationwide survey valued these sources for their trustworthiness, accessibility, and shared lived experience:

“My son helps me, and I trust him.”

“My friend does them for me because I can’t afford a preparer.”

“The answers I seek come from trusted friends and people in the community…because I see them regularly, and they know what’s most helpful for me.”

“My friends and family would not lie to me. So I trust their recommendation.”

Even among those who used official or professional services, trust was closely tied to experience and relationships. In-person tax preparers were valued for their qualifications, personal reputations, and the sense of being in safe hands:

“I’ve known the woman for most of my life. She’s a CPA.”

“They are nonprofit organizations, so I trust them.”

“I trust the tax people [unions, worker advocacy groups, and local tax prep support] more than the ones online.”

“Tax preparers are a good legal source…I like the online options, but I just don’t feel confident doing it myself.”

Tax software and online platforms also earned trust—particularly among regular filers—because of their ease of use, error detection capabilities, and clear language:

“It flags my errors.”

“They know what they are doing, and I trust them.”

“They are a legit business, and their information is easy to read.”

“They are all accredited companies.”

Many saw official sources like mail or flyers from the government as reliable simply because they were official:

“I like to go directly to the source.”

“It’s my government, and I trust them highly.”

“They’re not trying to sell me something.”

“Because it’s the only place to get this information.”

While mail and flyers from the government were less commonly cited overall (12 percent), those who did receive them were more likely to have claimed tax credits (nearly 70 percent said they had claimed credits).

Some families in the Illinois study highlighted barriers to receiving physical mail and wanted reminders through email or text, especially if they had moved or lacked stable housing. Survey data reflected these preferences: 57 percent of respondents preferred communication by email, 47 percent by mail (primarily those 44 and older), 35 percent by text message (more common among those under 44), and 24 percent by phone call. On average, people selected 1.6 communication preferences, suggesting that most wanted to receive information through more than one channel.

“Mail and email, in case something gets lost.”

“It’s tricky because sometimes I don’t get the mail. If I don’t get the mail, I didn’t get that redetermination in time. Then, I have a breach in my food stamps…it might be double trips to the food pantry. They don’t send you email reminders…I like text reminders…or even if they just post it on the website.”

Some in the Illinois study also noted a lack of faith in being given flyers in person at local state offices.

“I feel like if the flyer’s not right there on their desk, they might not give it to you. I’ve been in the office and seen really valuable information just sitting on someone’s desk, or posted on a bulletin board where no one notices it. If you don’t happen to see it or it’s not handed to you, it’s just good information going to waste.”

Through our Illinois study, we also heard that many families were learning about government benefits more broadly from schools, early intervention specialists, medical providers, libraries, or local community organizations. Of the survey respondents, 14 percent mentioned local community centers, libraries, or local events as trusted sources of information.

“I tend to do it alone because I don’t want to pay that $400 or $500 tax preparer fee. But usually, I get help from the library or something like that. Or use a free website. Or try to call as much as I can when I’m not understanding something.”

Ultimately, people don’t absorb tax information in isolation. They interpret it through trusted messengers, layered sources, and personal thresholds for effort and risk.

Recommendations for Implementation

Tailor Messages to Real-Life Motivations

Effective messaging must reflect how people actually seek information and make decisions.

To improve credit uptake, outreach must feel relevant, trusted, and empowering. That means moving away from one-size-fits-all campaigns. Notably, no one in our interviews said they were overwhelmed by too much information; more and well-placed outreach is not only helpful but welcome.

Outreach strategies should reflect how people learn and validate information—through a mix of formal and informal, personal and institutional sources. Within these message delivery channels, the content should also be relevant to varying barriers and motivations. Taxpayers and credit-eligible families benefit from hearing messages in multiple places and from multiple messengers.

Effective outreach looks like:

- Partnering with trusted messengers. Tailored, culturally relevant messages resonate more than one-size-fits-all campaigns. Collaborate with local organizations, tax preparers, and accountants in under-filing ZIP codes; use Google Ads; leverage state Department of Revenue (DOR) websites; and partner with non-DOR benefits agencies to reach people where they already are. Messaging should be simple, repeatable, and ideally reinforced by sources families already trust.

- Tailoring messaging to behavioral archetypes. Filing and claiming behaviors are governed by distinct fears and motivations. Outreach efforts should either (1) cover a range of concerns in a single campaign to reach multiple archetypes at once, or (2) tailor specific messages to match the audience you are speaking to. For example, an outreach campaign through human services agencies might prioritize alleviating fears about losing benefits, while outreach through workforce development centers could emphasize financial gain.

- Using more than mail. Many families miss or never receive physical mail, or prefer more than one mode of communication. Supplement mailed communications with email or text reminders, and post updates directly on agency websites and benefits portals.

- Reaching out early and often. Government communication should be simple, timely, and consistent. Start sharing tax credit opportunities in the fall, ahead of the next tax season, and before commercial tax preparers begin heavy marketing, to give families time to understand all their options.

If we want more people to file and claim the support they’re eligible for, tax outreach needs to be more than a one-time message or announcement. It should be part of an ongoing relationship built on consistent timing and consistent messaging.