An Enrollment Management Scandal

The sexual assault catastrophe was not the only scandal at Baylor under Starr’s watch. A separate scandal, news of which did not break until long after the former independent counsel had left campus, received far less attention than the first but threatened to do great financial harm to vulnerable students and their families. And it too showed how the university had, in its quest for greater status and glory, “lost its moral compass.”1

In October 2021, The Wall Street Journal revealed that Baylor had been steering low- and lower-middle income families to take out “no limit” Parent PLUS loans as part of the university’s efforts to help pay for the costs associated with its ambitions “to transform itself from a regionally known Baptist college into a national brand.”2 By pushing low-income parents to take out PLUS loans, Baylor would receive the money up front from the government, without having to worry whether the families would be capable of paying the debt back.

The article cited U.S. Department of Education College Scorecard data showing that about 47 percent of PLUS loan borrowers with kids who graduated from Baylor in 2018 and 2019 were the parents of Pell Grant recipients.3 They incurred a median of $43,500 in PLUS debt while their children were in college. Meanwhile, the Scorecard data showed that “only about a quarter of Baylor parents paid down any of what they originally borrowed after two years,” the article stated.4

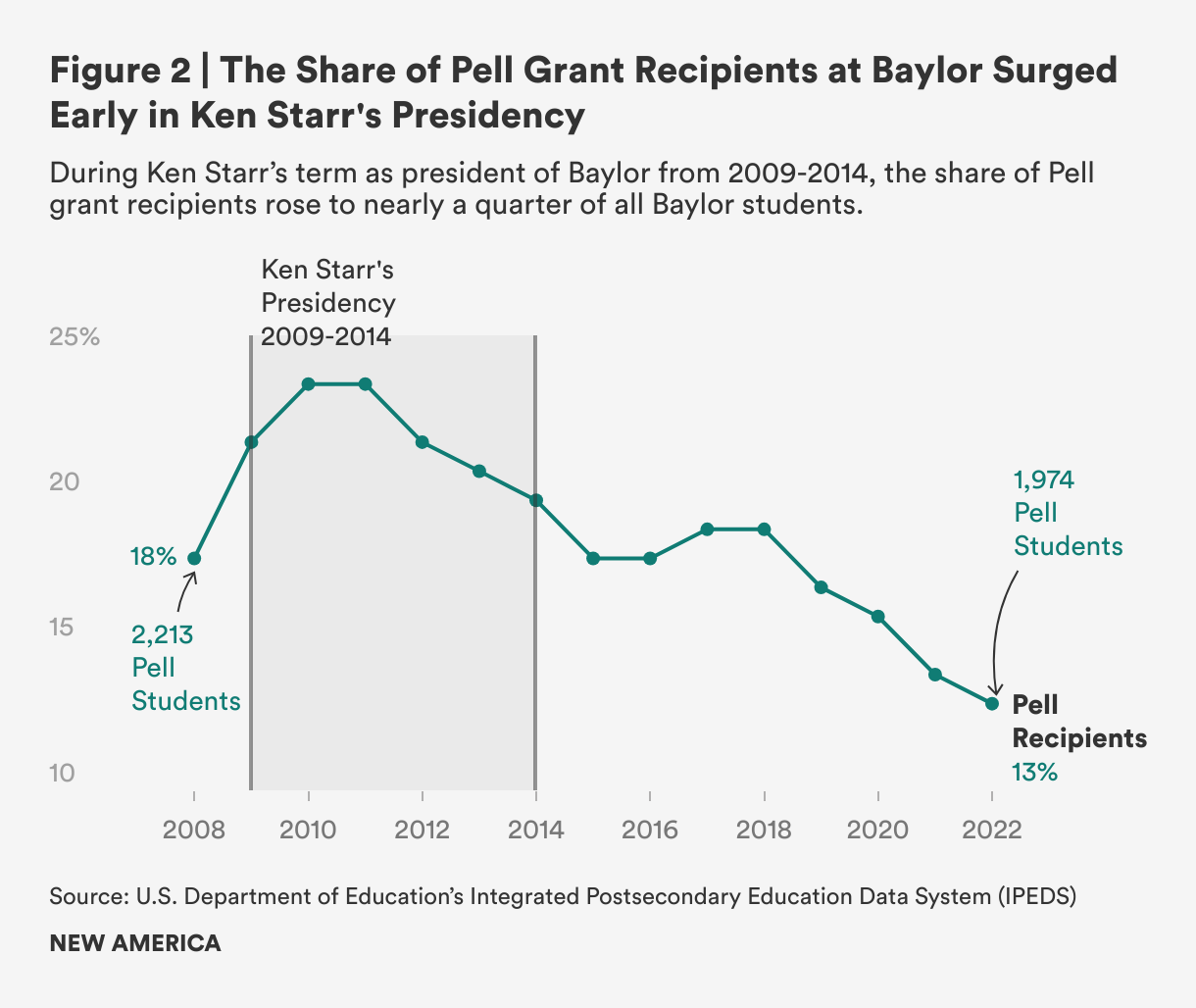

This situation likely started before Starr arrived at Baylor, as university officials were desperate to make payments on the $250 million bonds the university had issued when Sloan was president.5 However, it accelerated under Starr, as the university became more aggressive in recruiting low-income students. From 2009–10 through 2014–15, recipients of Pell Grants, the federal government’s primary source of funding for low-income students, made up 20 percent or more of the university’s students (see Figure 2). In two of those years, 2010–11 and 2011–12, they made up nearly one-quarter of the student body.6

The Wall Street Journal reporters revealed that some of the university’s recruiters had serious reservations about the institution’s aggressive pursuit of low- and lower-middle-income students:

Annabeth Mohon, a former Baylor admissions counselor and 2014 graduate, felt so conflicted about visiting poor neighborhoods in Texas to sell prospective students on a college they couldn’t afford that she left after a year on the job in 2015. “I felt like a real jerk,” said Ms. Mohon.7

Normally college access advocates would applaud a school for enrolling so many low-income students. It is important to remember, however, that Baylor did not make available the resources to adequately support them. During the Starr years, the university regularly met less than 70 percent of the financial need of student aid recipients at the university, far less than many other wealthy private colleges and universities covered at the time.8

It is also important to remember that under the financial aid leveraging programs that private enrollment management firms aggressively market to colleges, institutional aid is not used to meet financial need. With enrollment managers primarily focused on increasing colleges’ net revenue and rankings, covering low-income students’ financial need is considered inefficient and wasteful. Instead, enrollment managers are concerned with using aid to reel in the students they most desire, without spending a dollar more than necessary.9 By 2016, Baylor awarded about $92 million in non-need-based aid. About two-fifths of freshmen received a non-need-based aid award of nearly $18,000 each.10

“Aid leveraging is an analytical tool that enables admissions and financial aid administrators to estimate the amount of financial aid (regardless of formal need formulas) that would be necessary to increase the probability that a student with a specified set of characteristics would enroll,” Donald Hossler wrote in 2000, when he was Indiana University at Bloomington’s vice chancellor of enrollment services. “This approach raises tuition and uses large portions of the increase to provide financial aid to prospective colleges students to induce them to matriculate,” he explained. “Although these financial aid inducements might be used to meet student financial need, the intent behind the strategy is to use the award as a merit award that will help individual campuses more effectively ‘court’ or recruit students with higher grades, with more talent, or with lower levels of financial need.”11

Ever since the introduction of the “Baylor 2012” plan in 2002, the financial aid funding gaps (the yearly cost of attendance minus the amount of grants and scholarships offered) that the lowest-income students faced grew steadily because the university had become so much more expensive. “Though Baylor still charges less than many other wealthy [private] colleges, its tuition grew the most among wealthy schools in the Journal’s analysis of available federal data,” The Wall Street Journal article stated. “Baylor charges about 2.6 times as much as it did two decades ago, accounting for inflation.”12 During Starr’s presidency, students from families making $30,000 or less paid an average net price of about $32,000, after adjusting for inflation—which was more than they earned in a year.13 As a result, these families had little choice but to borrow PLUS loans if they wanted to send their children to Baylor.

In their quest for institutional greatness, Baylor’s leaders turned a blind eye to the collateral damage their policies caused. Just as they tried to bury the complaints of women who had been sexually assaulted, they did not give a second thought about the possibility of putting families who were already struggling economically into severe financial distress.

But it is hard to see how encouraging low-income parents to take on debt they most likely won’t be able to repay will end in anything but disaster for these families.

Citations

- Watkins, “Under Starr’s Presidency, Baylor Watched Golden Age Turn Sour,” source.

- Hobbs and Fuller, “How Baylor Steered Lower-Income Parents,” source.

- The PLUS loan borrowing data are produced for rolling two-year pooled cohorts for the U.S. Department of Education’s College Scorecard. In this case, the cohort consists of PLUS loan borrowers who are the families of Pell Grant recipients who graduated in 2017–18 and 2018–19.

- The PLUS loan borrowing data are produced for rolling two-year pooled cohorts for the U.S. Department of Education’s College Scorecard. In this case, the cohort consists of PLUS loan borrowers who are the families of Pell Grant recipients who graduated in 2017–18 and 2018–19.

- Luther, “How Baylor Happened,” source.

- Colleges and universities report annual data on the share of Pell Grant recipients in their student bodies to the U.S. Department of Education’s Integrated Postsecondary Education Data System (IPEDS).

- Hobbs and Fuller, “How Baylor Steered Lower-Income Parents,” source.

- Hobbs and Fuller, “How Baylor Steered Lower-Income Parents,” source.

- Burd, “The Dangerous Game of Financial Aid Leveraging.”

- Peterson’s, “Undergraduate Financial Aid and Undergraduate Databases.”

- Donald Hossler, “The Role of Financial Aid in Enrollment Management” in The Role Student Aid Plays in Enrollment Management, ed. Michael D. Coomes (Jossey-Bass Publishers, 2000), 83.

- Hobbs and Fuller, “How Baylor Steered Lower-Income Parents,” source.

- Colleges report the average net-price-by-income data annually the U.S. Department of Education’s Integrated Postsecondary Education Data System (IPEDS), which displays the school-by-school data on its College Navigator site. Baylor’s data can be found at source.