More Scrutiny of Loan to Learn

Blog Post

July 25, 2007

Yesterday, Higher Ed Watch reported that Catherine B. Reynolds' nonprofit company EduCap has marketed private loans -- under the brand name Loan to Learn -- that are as expensive, and in many cases even more expensive, than its for-profit competitors. Today, we take a closer look and find that Loan to Learn is lending to better-risk students; that is those who tend to have higher credit scores than the population of students who are borrowing private loans from EduCap's largest for-profit rivals.

We at Higher Ed Watch believe that the the characteristics of the EduCap's borrowers and the terms and conditions of their loans are key issues to consider at a time when the company's not-for-profit, tax exempt status is coming under scrutiny. On Monday, the Senate Finance Committee demanded that the company turn over a boatload of documents about "its management, structure, and expenses" as part of an effort to determine why it has been allowed to operate as a not-for-profit organization. In a letter to Ms. Reynolds, the Committee's leaders cited an article published in The Washington Post last week that raised "serious questions" about how the company was carrying out "its charitable mission" of "assist[ing] students in meeting the costs of college."

We at Higher Ed Watch believe that the the characteristics of the EduCap's borrowers and the terms and conditions of their loans are key issues to consider at a time when the company's not-for-profit, tax exempt status is coming under scrutiny. On Monday, the Senate Finance Committee demanded that the company turn over a boatload of documents about "its management, structure, and expenses" as part of an effort to determine why it has been allowed to operate as a not-for-profit organization. In a letter to Ms. Reynolds, the Committee's leaders cited an article published in The Washington Post last week that raised "serious questions" about how the company was carrying out "its charitable mission" of "assist[ing] students in meeting the costs of college."

In response to the Post's article and the Senate committee's demands, George Pappas, a spokesman for the company, said that EduCap fulfills its nonprofit mandate by bringing more capital into the student loan marketplace. "As a good and proper nonprofit, we bring more competition and choice to students and families every day."

Those are nice sentiments, but they belie the fact that there is no shortage of loan capital in the private student loan market. Private student loans are the fastest growing form of student aid today. According to the College Board, lenders provided more than $17 billion in private loans in the 2005-06 academic year, and the total volume of private loans has been growing "at an annual average rate of 27 percent" since the 2000-01 school year. If current trends continue, student-aid experts expect that the volume of private loans will eclipse that of the federal student loan programs within a decade.

Nonprofit organizations are given tax-exempt status to serve the public good. As we noted yesterday, most nonprofit lenders are state-affiliated agencies that offer private loans at cheaper rates than banks and other for-profit providers. The Maine Higher Education Loan Authority (MELA) , for example, provides non-federally guaranteed, private loans to undergraduate students who are Maine residents or are from elsewhere but attend colleges in the state an interest rate of 6.35 percent, regardless of their credit histories. Not only are Loan to Learn's private loans more than twice as expensive as its nonprofit counterpart MELA's, as we reported yesterday, despite its nonprofit status, EduCap's loans are no cheaper than its for-profit rivals.

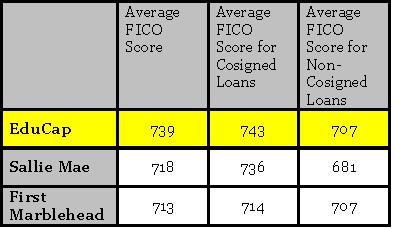

But aside from lower interest rates, another possible charitable purpose for EduCap would be to provide private loans to students who otherwise would not be able to get them because they are too poor or are not credit worthy. But a close examination of non public EduCap documents obtained by Higher Ed Watch reveals that the company tends to lend to students with higher credit scores than either First Marblehead Corporation or Sallie Mae, two of the largest for-profit players in the private-loan marketplace.

Overall, the average FICO score of EduCap's borrowers is 739, which is more than 20 points better than those who obtain private loans from Sallie Mae and First Marblehead, according to the most recent prospectuses for securitization of those two corporations. [FICO scores measure the probability that a borrower will repay his or her debt. FICO scores range from 300 to 850, with 850 being the highest possible score. Scores below 660 are generally considered to be subprime, and borrowers with scores lower than that typically have to pay higher interest rates and fees.]

The results are even more startling when you look at the breakdown of FICO scores among borrowers from the three companies. More than 40 percent of the loans that are taken out by Sallie Mae and First Marblehead borrowers have scores below 700. Comparatively, only about one-quarter of EduCap's loans go to students who have scores within that range.

Conversely, a much higher proportion of EduCap's loans go to students with scores above 800. According to company documents, 12 percent of the Educap's loans go to students with the highest credit scores. In contrast, only about 2 percent of First Marblehead's loans go to such students.

Admittedly, prospectuses for securitization do not provide perfect comparisons. They represent a snapshot of a company's loan portfolio at a given time. But they provide the most complete information available about the makeup and profile of a private loan company's borrowers, and they are widely used within the industry to compare companies, and analyze trends within the marketplace.

At the very least, our data show that EduCap's borrowers are no worse off than those who take out private loans with for-profit companies. Given that reality, and the fact that its loans aren't any cheaper than those offered by its competitors, we are still left with the question of who is really benefiting from the company's nonprofit, tax-exempt status. The answer to that question is still to come. Please continue to stay tuned.