The Future of Chinese Growth

Policy Paper

March 1, 2011

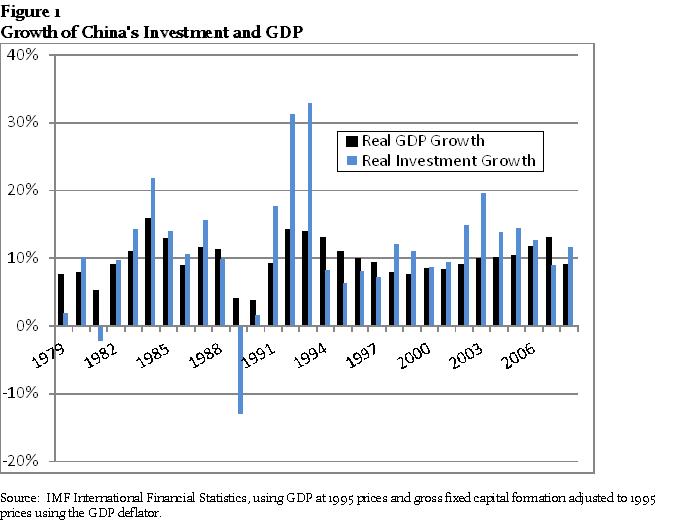

Real GDP in China has grown at an average rate of nearly 10% annually for the 30 years from 1980 to 2010, exceeding the real growth of any other country over this period. This performance has been a source of amazement to academics and business people, and a source of immense pride to the Chinese. Certainly countries have grown rapidly in the past, but such growth has generally abated in time; 30 years is a very long run. As shown in Figure 1, the growth has not been uniform. Rather, it has been concentrated in three bursts of 5-6 years duration, each associated with high growth in capital investment. I shall briefly explore the reasons for each of these high-growth periods.

The first growth phase was caused by the unleashing of Chinese entrepreneurship by Deng Xiao-Ping in the 1980s. In Huang’s (2008) account, Deng put particular emphasis on the countryside via the Township and Village Enterprises (TVEs) which were in fact private enterprises at the village level, and which benefited during the 1980s from significant financial support and political encouragement. This growth program brought benefits that were widely distributed around the country. Notably, it was not export-oriented.

By the early 1990s, the second growth phase, a new dynamic was in place. Political leadership shifted to a group of Shanghai-oriented politicians who emphasized investment in coastal areas that could produce export goods at the lowest possible prices, based on young labor imported from the inland provinces. This was initially based on producing labor-intensive goods such as clothing, shoes and toys. However, it soon evolved into a processing or assembly model that produced more sophisticated goods by importing components and assembling them based on cheap labor imported to the coast from the inland regions. TVEs were de-emphasized and dwindled as a source of growth.

During this period China benefited from another special factor: the offshore Chinese community including Hong Kong. As is well known, people of Chinese background have long dominated the business communities of Southeast Asia, owning a very large proportion of the private businesses in countries such as Thailand and Indonesia. Singapore was and is primarily a Chinese city-state. The offshore Chinese community was able to supply not only capital, but more importantly management skills and market access that China still lacked.

Hong Kong, which was under British rule until 1997, reverted to Chinese control in that year. Anticipation of the handover triggered major new opportunities for the wealthy entrepreneurs of Hong Kong to engage with mainland China. The export processing model was often implemented by a partnership between a factory on the Guangdong mainland and a “front office” in Hong Kong that handled management, marketing and finance.

As the export model matured in the early 2000s, a third factor produced a final growth spurt: for a number of reasons, credit to consumers in the United States and certain countries in Europe (notably the U.K., Ireland, Iceland and Spain) became much more freely available, particularly through mortgage markets. This led to a housing and stock market bubble, and wealth effects stimulated increased consumer spending in those countries. China was a substantial beneficiary of this increased spending, which stimulated the third growth episode illustrated in Figure 1.

Many people take continuation of Chinese growth for granted; after all, China seemed to sustain high growth through the East Asian crisis of 1997-1999 and the financial collapse in the industrialized world in 2007-2009, when many other countries slowed or turned down. Yet growth should never be taken for granted: it does not happen by itself, but results from specific underlying changes and opportunities. Growth, by definition, is change; and change, by definition, is not permanent. It requires constant effort.

The Chinese government seems determined to sustain 8-12% growth for as long as possible. Yet the government itself acknowledges that this may not be feasible. Premier Wen-Jiabao said this at the National People’s Congress press conference in March, 2007: “The biggest problem with China’s economy is that the growth is unstable, unbalanced, uncoordinated and unsustainable”.

Japan offers the closest historical parallel to China’s recent growth. Japan’s real GDP grew at double-digit rates from the mid-1950s through the mid-1970s; many Western observers worried that Japan’s disciplined workforce, work ethic, quality products and careful management would cause it to dominate the world economy, much as many Western observers today worry about China taking over the global economy. But after a spectacular 1973, Japan’s growth began a long, gradual decline, as illustrated in Figure 2. By the 1980s it was in the 5-7% range, but it was being artificially sustained by financial excesses: Japan’s banks were massively over-lending in this era, leading to inflation of equity and real estate prices, much as the subprime bubble artificially boosted U.S. growth in the 2000-2007 era. Japan’s financial bubble burst in 1990, whereupon its GDP growth dropped to nearly zero.

There is ample reason to believe that China’s growth is being artificially sustained by financial excesses at the present time. As will be discussed more fully below, its response to the industrial world recession of 2008-2010 has been over-lending by the Chinese banks, leading to substantial inflation of wages, equity values and real estate prices much as happened in Japan. The longer this continues, the more painful the comedown is likely to be.

The first section of this paper explores investment-driven growth, first in theory and then as it has worked in China. I explore diminishing returns, the efficiency of Chinese investment and particularly the concept that growth by investment can be value-destroying. The second section explores export-driven growth, first in theory and then as it has worked in China. China has enjoyed large-scale Ricardian benefits of trade due to globalization and the debt-driven consumption excesses in the United States and Europe during 2000-2007, but rising price and wage inflation will likely limit the export model’s future.

The third section asks how readily China can shift from investment- and export-driven growth to a more sustainable model based on domestic consumption. This is the express goal of the government, but formidable obstacles stand in its way. Above all, the Chinese people are poor: the returns to capital in China have been high but the returns to labor have been extremely low. The low wages and famously high saving rate of the Chinese people feeds the investment and export models, but must change materially to support domestic consumption as an engine of growth. Indeed, China is now seeing some very large wage increases, and these must be sustained over many years to bring China’s consumption levels closer to the norm in other countries. But the effort to build consumption by raising wages will undermine existing exports. The consequence may be a substantial pause in Chinese growth as one growth model is phased out and the other is phased in.

Investment Driven Growth

Diminishing Returns

China’s fundamental growth strategy over 1980-2010 has been massive investment in physical capital, facilitated by high savings rates both in households and in state-owned enterprises, and by government control over banks. Economists have long observed that a society can choose to defer consuming some of its output and instead invest this amount for the future, which will accelerate the society’s rate of economic growth.

This is formalized in the well-known Solow model.1 In this model capital has diminishing returns to scale: absent innovation, adding more and more physical capital generates growth so long as the economy’s savings exceed the depreciation of the capital stock, but sooner or later depreciation of the growing stock must catch up with savings. As the charge for depreciation grows, returns to invested capital decline and the growth must slow to zero.

Diminishing returns can be offset, however, by technological innovation. This term is understood quite broadly, incorporating not only physical inventions but more importantly management improvements, new products and new markets. When these are incorporated into the model, growth generated by capital investment is augmented by the rate of innovation, and in the long run growth still slows but only to the rate of innovation. The broad definition of technological innovation opens many opportunities to evade or at least postpone declining returns to scale. In particular globalization, by opening borders to a freer flow of goods, services, capital, people and ideas, provides many opportunities for growth to those countries willing and able to take advantage of them. China has been a primary beneficiary of the rise of globalization during the 1990s. It has benefited greatly from Western technology, management, ideas and markets.

The increase of real GDP (or GDP per capita), however, is not a complete economic goal: the quality of growth matters. For example, is the growth sustainable? Is it driven by increasing inputs of capital and labor or by more efficient use of these (productivity growth)? Does it create value or destroy it?

China has grown primarily through heavy investment in capital plant over many decades. In fact, gross fixed capital formation has increased steadily from 29% to 42% of GDP over 1980-2010, and many analysts have expressed concern that some of this rising tide of investment is inefficient. This fear seems particularly plausible since most of the investment is made by state-owned banks lending to state-owned companies. State-owned enterprises everywhere are prone to economic inefficiency because they serve political and social objectives in addition to purely economic ones. China, to its credit, has attempted to distance its state owned enterprises from direct political control, but this is not always successful.

Investment Efficiency

Increased capital investment does not by itself represent GDP growth: capital investment is a use of GDP, but whether it leads to future GDP growth depends entirely on how efficient the investment is. Capital investment only produces growth if it leads to greater production of products that can profitably be sold. Investment in infrastructure, for example, may briefly provide jobs but thereafter lead to no growth at all; Japan invested heavily in bridges, roads, tunnels and similar projects over 1991-2006 but this did not stimulate any significant economic growth.

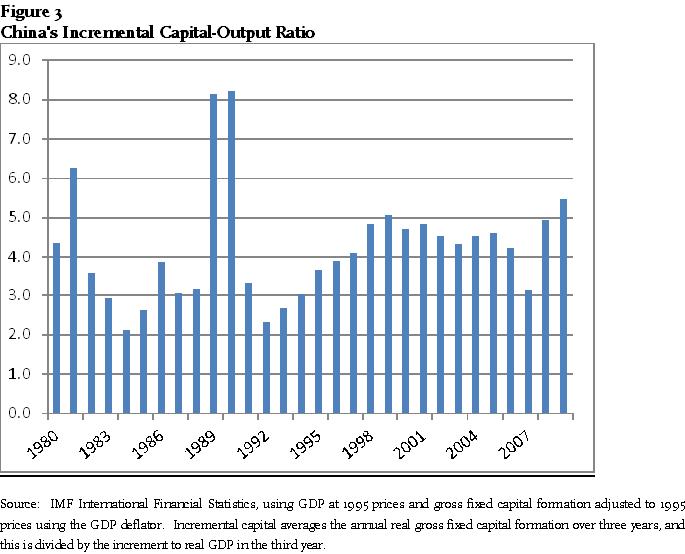

A common measure of investment efficiency is the incremental capital/output ratio (ICOR), the ratio of new capital investment to growth in GDP. This can be computed in a number of ways. Figure 3 shows the ratio of average real capital investment over each year and the two preceding years, divided by the increment to real GDP in the current year. An ICOR of 3 or less is generally considered good, while an ICOR of 4-5 suggests inefficient investment. As shown in Figure 3, China’s ICOR was less than three only twice: in 1983-86 (the first growth phase) and again in 1992-95 (the second growth phase).

That is, one could say that the first and second growth phases were highly efficient, bringing important productivity gains. After 1994, however, growth gradually subsides and ICOR rises, i.e. diminishing returns begins to set in. As will be show below, a substantial portion of investment in the later 1990s proved to be value-destroying, leading to large losses in the banks. Then in 2000-2007, the heyday of the export-driven model and of Western consumption and borrowing excesses, investment rises again, but ICOR remains in the 4-5 region except for the crest year of 2007. When the financial crisis hits and massive lending ensues, inefficient investment reasserts itself as ICOR jumps to over 5.

Academics have examined investment efficiency in China using various methodologies. Based on firm-level data from a sample of 12,400 firms in 120 cities in China, Dollar and Wei (2007) concluded that even after a quarter century of reforms state-owned firms still have significantly lower returns to capital than domestic private or foreign-owned firms. Based on aggregates at the provincial and national levels, He, Zhang and Shek (2007) found that the marginal product of capital has been relatively high for two decades and has not shown clear signs of decline, but this result was stronger in the coastal provinces than in the inland. They also found, however, that the rate of investment in China has consistently exceeded the share of capital income in GDP, implying that the rate of investment is too high and dynamically inefficient.

Value Creation and Destruction

A related question is whether the capital investment creates or destroys value. Value is a financial concept, and finance has only a marginal role in classical macroeconomic models, which focus almost exclusively on the real economy. But value matters. If we could accurately estimate the future cash flows of all the firms in the economy and discount these to present value at an appropriate cost of capital, the result would be the value of the firms in the economy. The rule in corporate finance is that new capital expenditure creates value if its return exceeds the cost of capital, but destroys value if its return is less than the cost of capital.

Value destruction may lie hidden for years and only gradually become apparent. Its eventual price is real, however, and is borne by the suppliers of capital. In a market-based financial system, capital suppliers sensing hidden value destruction first become nervous and yuan risthen may rush for the exit, with prices of stocks, bonds, real estate and/or currencies suddenly falling. The resulting crisis is painful, but the sharp pain signal typically calls attention to the underlying problem and usually brings the value destruction to an end. In some cases, however, the value destroyer is insulated from market signals.

A spectacular example of insulated value-destroying growth is provided by General Motors. From 1965 to 2005 its sales grew from $11b to $474b, a factor of 41 times. But operating income stayed roughly constant and the per share price of its stock declined, adjusted for one stock split. Jensen (1993) estimated the value creation or destruction through capital expenditure and R&D spending by 432 U.S. companies during the 1980s, using a discounting methodology. He concluded that General Motors had destroyed about $100b of economic value over 1980-1990, even though its stock price did not fall. I repeated Jensen’s calculations for the period 1992-2001, an optimistic period when GM’s stock price more than doubled but in which further massive and ultimately unproductive investments in plant and R&D were made. I estimated value destruction in these 10 years to be approximately $200b.

The reason that GM’s value-destroying growth of this magnitude did not trigger a flight by capital suppliers is that the company was insulated by its huge embedded cash flows. These cash flows might have been passed to the capital suppliers, who had opportunities to invest them at market rates of return, but instead were poured into capital investments whose poor quality was not visible for many years. Because embedded cash flows insulated the company from market pressures, GM did not generate investor anxiety for many decades.

The East Asian financial crisis of 1997-98 was as unexpected as was the recent crisis, and puzzled many observers because it was most severe in the countries that had been the most highly regarded and rapidly growing: Korea, Thailand, Indonesia, Malaysia and Philippines. Pomerleano (1998) conducted a study of firm-level accounting data to see if this growth had been value-destroying. Among other measures he examined a simple pre-tax return on capital employed (ROCE), dividing operating income by debt plus equity, and aggregating this year by year at the country level. He then compared his ROCE estimates to the local-currency interest rate year by year. His idea was that cost of capital is elusive, but is bounded below by the cost of debt: if a firm cannot earn at least the local currency interest rate on its total capital, it must be destroying value. Thus ROCE less local interest rate is a rough proxy for whether economic value was likely destroyed.

His results were striking: over 1992-96, the five years leading up to the East Asian crisis, this metric averaged -9% in Indonesia and Philippines, -8% in Thailand and -2% in Korea and was positive elsewhere in East Asia. This implies that firms for which accounting data were available were on average destroying value in four of the five countries that turned out to be the center of the East Asian crisis. This is one of the few metrics that in retrospect might have predicted the crisis.

In the case of China, the main capital suppliers are state-owned banks, which are unlikely to refuse lending to SOEs even if they destroy value. The banks are fully protected by the government and so do not suffer runs. Their patient behavior insulates Chinese firms, especially the SOEs, from capital flight. So China does not experience the pain signals that periodically shock other economies; this is the primary reason China did not appear to participate in either the East Asia crisis or the current financial crisis. But in a sense they did participate. If one has a decaying tooth, for example, the pain signal is unpleasant but forces attention to the underlying decay; the absence of a pain signal is not necessarily a benefit. The East Asia crisis was a form of capital flight from countries whose economies had grown rapidly but which now seemed to have been destroying value. China participated in the value destruction (see next section) but avoided the capital flight.

Chinese Banks and Value Losses

Banks in general are notorious for concealing value destruction. It is only when banks seek to be repaid that they learn whether the borrowers can repay with interest or not; if banks are willing to roll over their loans indefinitely, and lend more to ensure interest payments, losses may be concealed for decades. As a banking quip goes, “A rolling loan gathers no loss.” This often has the collaboration of government regulators. For example, United States regulators of thrift institutions – savings banks and savings and loan associations – permitted the thrifts to engage in massive value-destroying growth after most had failed in the early 1980s, extending the thrift crisis by eight years and causing a $20b problem to grow into a $200b problem. Banking crises are triggered only when either the government or unguaranteed capital suppliers to the banks refuse to go on funding them. Such refusal usually happens abruptly after a change of government or an unanticipated loss of investor confidence.2

I have replicated Pomerleano’s calculation over 2005-2009 for the 387 publicly traded Chinese companies with assets greater than $1 billion whose results are tabulated on Capital IQ. On average the metric is positive, though it declines from 6.2% to 3.4% over this period. However, this averages some very large positives with a number of negatives. Over these five years the fraction of companies for which this metric is negative increases steadily from 26.8% to 38.7%. It appears that more a third of these companies are not currently earning a return on capital employed greater than the local bank lending rate.

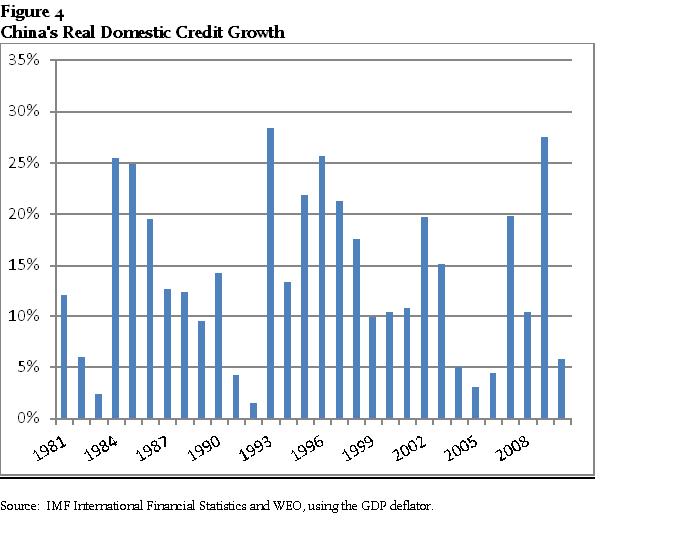

As noted above, China went through three great bursts of double-digit economic growth prior to the financial crisis, each of which was preceded and accompanied by a comparably large burst of capital investment facilitated by increased growth of domestic credit. Figure 4 illustrates the rapid growth of real domestic credit in China throughout the past 30 years. In fact, real domestic credit growth has averaged 14% annually over 1981-2010, i.e. materially faster than the economy.

A close look at Figure 4 shows eight years when real credit growth exceeded 20%. The first of these, 1984-85, coincided with years of high GDP growth, as did 1993. More recently, however, such years follow the crest of real GDP growth, namely 1995-97 and 2009. It appears that the government was alarmed at the decline of the growth rate in 1995-97 and attempted to extend the boom by excessive credit. That was clearly the case in 2009 when China seemed determined not to let its growth rate fall below 10%.

The credit expansion of 1993-99 left a hangover of nonperforming loans (NPLs) that was only gradually acknowledged by the authorities. NPLs are notoriously difficult to estimate in any banking system, but particularly so in China given the non-transparency and government control of the system. The Chinese definition of NPL is substantially looser than equivalents in the U.S. or Europe. The only reliable way to quantify value destruction in the Chinese banking system is to count up the losses retroactively.

In the first years of the new century China determined to reform its banks by opening them to foreign ownership. This in turn required dealing with the hidden losses. The government invested new capital in several stages into the four large banks, which then transferred NPLs to four new asset management companies (AMCs) one for each of the four banks. Dobson and Kashyap (2006) estimated that the total cost to the Chinese government of cleaning up the banks over 2003-2005 was $240-430b or 10-18% of GDP. These losses are best understood as having actually occurred in the credit expansion of the 1990s.

A further credit expansion in 2002-03 very likely led to more NPLs. Only after 2003 did the Chinese authorities exert a determined effort to restrain credit growth. Real credit growth averaged only 4% over 2004-2006, but this restraint was abruptly reversed in 2007 and especially in 2009 after the global economic downturn. Chinese loans outstanding grew by RMB 9.6 trillion in 2009 compared with RMB 4.7 trillion in 2008, and real GDP was up 9.4%.

While banks in almost all other countries grew increasingly risk-averse, the Chinese banks doubled down. Many, both inside and outside of China, expressed anxiety. As the Financial Times reported,3

The chairman of China Construction Bank, the country's second largest by assets, has warned of the perils of rapid economic growth, adding his voice to a growing chorus of economists concerned about overheating. Gross domestic product growth of 9.5 per cent or above would "be very problematic", Guo Shuqing told the Financial Times. "It will mean more duplication of construction, more excess capacity and higher waste of capital."

The Chinese government’s effort to protect the growth rate led to a further loan expansion of RMB 7.95 trillion in 2010, overshooting its target of RMB 7.50 trillion. Growth was at a 9.6% rate in the third quarter and is estimated to have exceeded 10% for all of 2010.

Export-driven Growth

The economic benefits of trade were of course articulated at the dawn of modern economic thought by David Ricardo: a low-wage country can profitably trade with a high-wage country if the former specializes in labor-intensive goods and the latter in capital-intensive goods. A dynamic growth strategy can start with the most labor-intensive goods such as clothing, shoes and toys, then gradually move up the scale of sophistication to consumer electronics and automobiles. This growth path was effectively followed first by Japan in 1960-1990, then by Korea and Taiwan in 1980-2010. It has been China’s preferred path since about 1990.

Export competition brings a number of special benefits. Above all, it forces a country to compete with the best producers in the world, challenging the exporters to improve their products and processes as rapidly as possible. Furthermore, companies in industrialized countries are often interested in producing goods in low-wage economies for their markets, and are willing to invest in the low-wage countries to achieve this. The recipient country can extract a lot of benefits from this partnership including transfer of technology and modern management techniques. China has been particularly adept at extracting such benefits from foreign counterparts.

Chinese Export Experience

Researchers have studied in great detail the role of exports in Chinese growth. Clearly gross Chinese exports are huge, cresting at 37% of GDP in 2008 before falling to 28% by 2010. Net exports are far smaller: they were just 1.3% of GDP in 2001, and then crested at 10.6% in 2007 before falling back to 4.7% in 2010. The contrast in these figures suggests that China’s exports add relatively little value: it reflects the processing approach in which China primarily performs a low-cost, labor-intensive final assembly to imported parts.

Clearly China has directed a large part of its investment at the export sector. IMF staff have estimated that net exports plus the investment linked to building capacity in tradable sectors accounted for 40% of China’s growth in the 1990s and 60% over 2001-2008, larger than comparable figures for the Euro area (30%) and the rest of Asia (35%).4

Koopman, Wang and Wei (2008) developed a new econometric methodology designed to estimate the share of domestic versus foreign value-added when a significant fraction of exports consist of processing or assembly trade. They estimated that the foreign value-added share in Chinese merchandise exports was 47.7% in 1997 and 46.2% in 2006, figures about twice as high as previous estimates. They also found that exports generally considered more sophisticated such as electronic devices have particularly high foreign content (about 80%), contrary to a common assumption.

Economic growth is based importantly on a rise of productivity. If the mix of low-wage labor in GDP increases, the return to capital (as estimated, for example, by either ROCE or ICOR) must improve. One might characterize the Chinese economy as a combination of a highly productive, efficient, value-adding export sector and a less efficient, sometimes value-destroying public sector. This characterization clarifies the importance of exports to Chinese growth: so long as low-wage processing exports increase more rapidly than other output, productivity increases. The coastal export complex maximizes the use of China’s low-cost labor and is a primary reason for China’s productivity gains.

During 2001-2007, as consumer spending in the U.S. and parts of Europe crested, China for the first time developed a significant trade surplus and began to accumulate financial reserves. China’s trade surplus grew at a compounded 40% annual rate from 2001-2007. This quickly became a political issue in Europe and the United States. Import substitution also fueled the greatest rise yet in Chinese GDP, whose real growth rose to 13% in 2007. The European-Chinese trade relationship became particularly strained. The United States has put intense diplomatic pressure on China to raise its exchange rate peg with the U.S. dollar, and under duress China has shown some flexibility and has promised more.

Rising Wages

The export model has caused strains within China. A migrant population estimated at 130-170 million people left the rural Chinese hinterland and settled in burgeoning coastal cities. The rural provinces, which benefited from Chinese growth in the 1980s, fell behind economically, and the migrants were little integrated into urban life. The social stress caused by the migration is a source of concern inside and outside the country. In 2010 a Taiwanese company (Foxconn) operating in Shenzhen experienced a highly-publicized wave of worker suicides, causing considerable agitation over working conditions in the export factories.

The reasons for labor agitation are many: the general unhappiness of displaced workers, the very low wages, the working conditions and, more recently, the inflation in consumer prices. Traditionally China has had little inflation: the CPI rose an average of only 1.4% over 2001-2006. But economic growth driven by credit expansion leads to over-heating. Urban housing prices increased by more than 20% in 2010, according to a Global Times report of January 17, 2011. According to FT.com on December 11, 2010, consumer price inflation was 5.1% in November, 2010, up from 4.4% in October and materially higher than the government’s target of 3.0%. Included particularly in 2010 inflation is a 10% increase in food prices. These add particular urgency to worker demands.

One might characterize the Chinese economy as a combination of a highly productive, efficient, value-adding export sector and a less efficient, sometimes value-destroying public sector.

In the past three years, workers in China have begun demanding higher wages. In 2008, as factory shutdowns multiplied, two new laws established a system of arbitration and courts to handle labor disputes.5 In 2008 the number of labor cases in court jumped 94% to 280,000, and in the first half of 2009 there were 170,000 such cases. In each of 2008 and 2009 nearly 700,000 labor disputes went to arbitration. Numerous prominent companies have raised wages by 30% or more in 2010. In many provinces the minimum wage has been raised 15-25% in 2010.6

Price inflation and wage inflation are closely connected. It was wage demands that made the U.S. price inflation of the 1970s so virulent, and the slack today in the U.S. labor market that holds U.S. price inflation down despite massive injections of liquidity into the system by the Federal Reserve. Similarly, wage demands in China quickly translate into higher prices, particularly in the presence of liquidity injections. In particular, export prices have been steadily rising, reaching 5% growth in 2010.

The Chinese government could use its currency peg to moderate inflation if it had chosen to let the yuan rise more than it has, since a rising currency value would cool the export economy and make imports less expensive. However, this is not the preferred policy of the government, which tends to put growth in production above all other values. This channels the inflationary pressure into export prices directly.

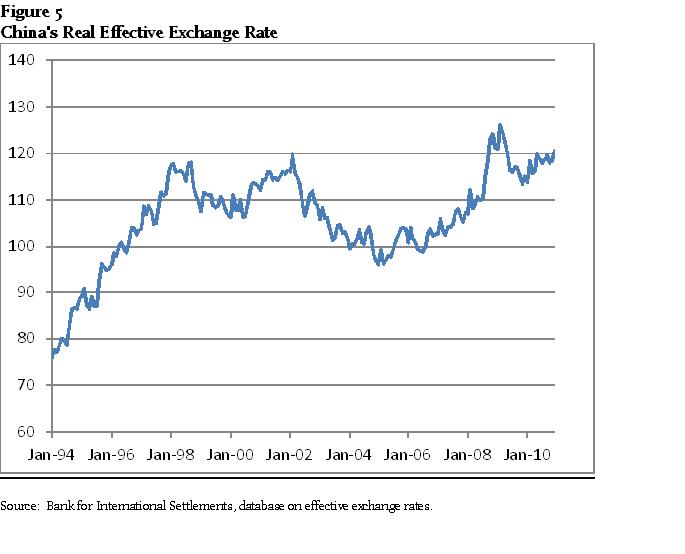

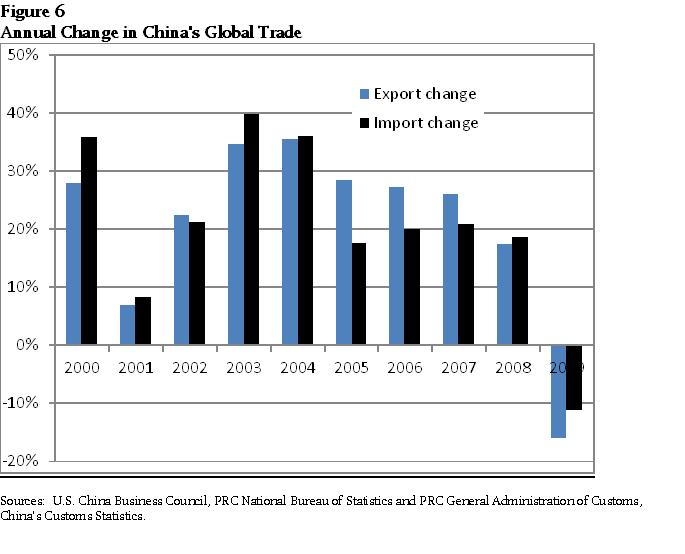

China has in general been losing competitiveness. Figure 5 shows the BIS effective exchange rate for China. As can be seen, China lost competitiveness during the 1990s then regained it during the crest of the export boom in 2002-2007. Since 2006 the currency peg has actually been revised upward by about 20%. Figure 6 shows that China’s export growth crested in 2003 and net export growth crested in 2005. China’s net trade position came under pressure in 2006 and altered materially in 2009. In April 2010 China had its first monthly trade deficit in six years, and China ended 2010 with a 6% decline in its trade surplus.

The fundamental problem China faces is that rising wages will undermine the export model, which is based on being the lowest-cost supplier. Vietnam and others are ready to compete for that space as China’s very success drives its wages higher. The model needs to change.

Could China simply move upscale into higher-end products, respected brands and more value-added? This is the way Japan managed its rising wages in the 1980s without slowing down. But Japan’s success in moving upscale was actually limited to just a few industries, notably automobiles and electronics, where the existing competition was suffering quality and other problems. When Korea attempted to follow Japan’s path a decade later it found the going much harder, primarily because Japanese products had become entrenched. Korea’s automobiles, for example, have had a hard time establishing themselves in part because of Japan’s earlier success in doing so: Korea cannot compete against Toyota as easily as Toyota competed against General Motors. China certainly has ambitions in electronics and automobiles, but only time will tell if they can move beyond cost advantages to compete on quality with the high-performance companies that tend to dominate these fields.

How much scope does China have for taking more low-end export market share away from other countries? The answer depends on what their appropriate longer-term market share ought to be, and how far they are from that optimum. This question was studied in detail by Bussière and Schnatz (2006), who concluded that China’s share of world trade was approximately at its appropriate longer-term level, given its size, location, development level and other factors:

China displays a higher degree of global trade integration than many other industrialized countries or Asian trading partners, However, our measure of global trade integration for China is not higher than that of several developed countries such as the US, Germany or Japan.

The implication is that China has already encroached substantially on the world’s export markets, and trying to raise market share from this point will be an uphill battle. No doubt it will be tried, but there is a limit to the share that any competitor can achieve, so this may be at best a short-term strategy.

Domestic Consumption-driven Growth

China’s mix of entrepreneurial energy, heavy investment and low-wage production for export has proven such a potent formula for economic growth that many people both inside the country and outside cannot imagine a China growing at less than 10% per year. But this is an illusion. The latest burst of capital investment financed by banks during 2009-2010 is almost surely generating another wave of NPLs in the banks.

This is not to say that Chinese growth must slow to a crawl as Japan’s did after its bubble burst at the end of the 1980s, though this is one possible scenario. Unlike Japan, China has an untapped source of future economic growth: its consumers. From a broad perspective, increased domestic consumption seems by far the most attractive source of growth for the future. It would serve to reduce the global financial imbalance, raise living standards in China, facilitate a new development focus on the rural areas and above all be sustainable. Yet this is more easily said than done.

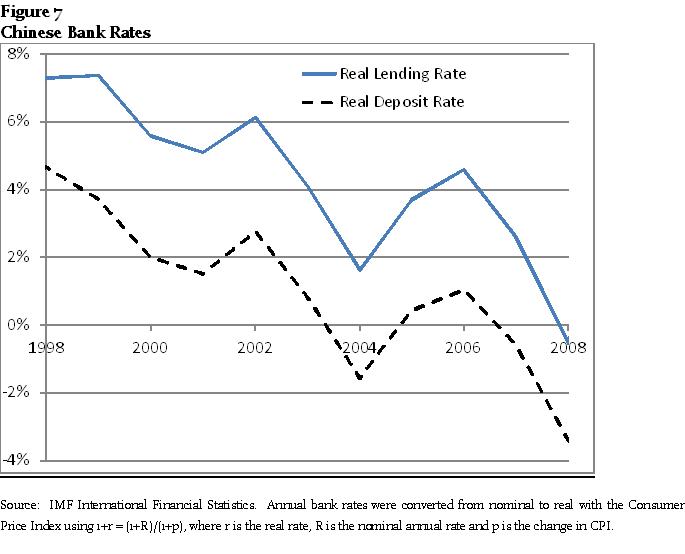

The constraints on Chinese consumers are impressive. Most fundamentally, their incomes are low: China has systematically favored producers over consumers. The returns to capital in China are high but the returns to labor are startlingly low. A recent IMF study uses multiple sources to trace the decline of household income to GDP over 1985-2005 by roughly nine points (9% of GDP).7 Not only are wages suppressed, but China also exploits the vast pool of household savings by keeping bank deposit rates low: real deposit rates averaged 0.2% over 1989-1998, 1.1% over 1999-2004 and 0.1% over 2005-2009 (See Figure 7). With both labor income and capital income low, consumers do not have the resources for expanded purchases of consumer goods, much as they might desire them.

Further constraints on consumers include unaffordable healthcare and an inadequate pension system. Consumer finance is in its infancy: until 2007 the People’s Bank of China did not even show a category for household lending. Since 2007 it has shown Chinese bank lending to individuals for business and for consumption. Consumption loans start at RMB 2.5 trillion at the beginning of 2007, rise to RMB 3.7 trillion by year-end 2008 and then suddenly jump to RMB 5.5 trillion by the end of 2009. However these still represent only 13% of total bank loans of RMB 42.6 trillion.8

Most worrying for advocates of increased local consumption, household saving rates for urban consumers actually increased from 17% to 24% of disposable income from 1995 to 2005. Chaman and Prasad (2007) conducted a detailed study of this phenomenon and found an intriguing pattern:

“We find a U-shaped pattern of savings over the life cycle, wherein the older and younger households have the highest savings rate. This is the opposite of the traditional “hump-shaped” profile of savings over the life cycle in the young workers save very little (in anticipation of rising income), savings rates tend to peak when income is the highest (middle age) and then fall off as workers approach retirement. This relationship between savings and age differs considerably from the norm in other countries.”

Apparently younger Chinese are saving in anticipation of rising educational costs and older Chinese are saving in anticipation of rising health costs.

If Chinese consumers are to absorb a significantly larger fraction of consumer goods produced by Chinese factories, these precautionary savings rates would need to be brought down; this would require better state health care and more affordable education. The entire development philosophy would need to shift away from producers and toward consumers, with businesses raising wages, banks raising deposit rates and increasing consumer loans, government offering expanded health and education services.

While these are not impossible, they imply a major shift in behavior and expectations. The Chinese leadership has often paid lip service to the goal of more internal consumption. Having tilted so strongly toward producers, China needs to begin favoring consumers as a matter of good economics. But there is a timing problem: raising wages will impact export competitiveness immediately, but the benefits of wealthier consumers buying more may take many years to evolve. The old model must be disadvantaged well before the new model can take hold. That suggests an interim period of significantly slower growth.

Summary and Conclusion

In summary, China’s growth over 1980-2010 resulted from a number of well-understood economic effects including acceleration of growth through capital investment and Ricardian benefits of trade. Equally important were a series of unique, transformative events that coincided to China’s benefit during this period: the carefully-managed but decisive policy shift away from Maoism and toward market economy in the 1980s, releasing the remarkable entrepreneurial energy of the Chinese people. Then the advent of globalization and the massive push for exports in the 1990s, culminating with the reunification of Hong Kong with China and the growing linkage of offshore Chinese with the mainland. Third, the burst of financial and consumer excesses in the United States and Europe in the 2000s fueled a consumption boom in both areas and created a rapidly-expanding market for Chinese goods.

One way to characterize China’s growth model is to say that it has favored internal producers and external consumers. Or this could be restated: it has favored internal firms and disfavored internal individuals (consumers, workers). Returns to physical capital have been high but returns to labor and to financial savings have been low. The resultant growth has been high but not sustainable.

China takes pride in not being part of the 1997-98 East Asia crisis or the 2007-2009 financial collapse in the industrialized world. But in a sense they have been part of both. They avoided the impact of the 1997-98 crisis by concealing bank losses and continuing to increase capital investment, some of which was value-destroying and led to a high level of bank losses. The banks did not suffer runs because of total government support, but the price was paid by individual savers, who suffered negative real returns as the firms and banks struggled to rebuild their balance sheets. China has met the 2007-2009 crisis by increasing lending on a larger scale. The consequence has been a debt-driven overheating of the economy and bubble in real estate and stock prices.

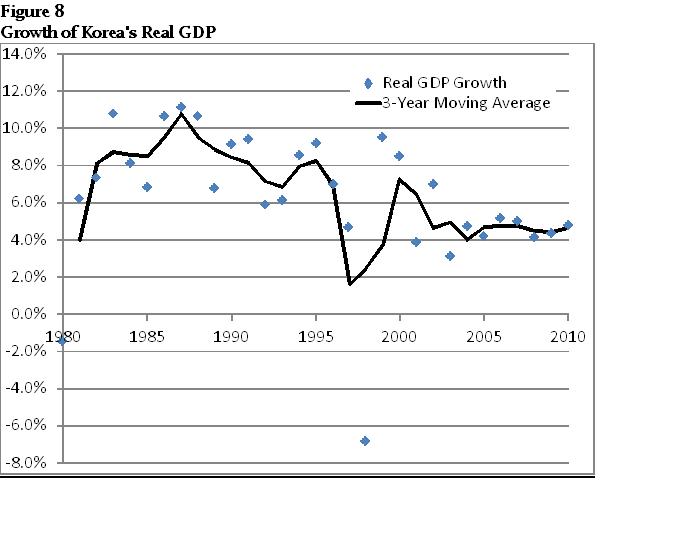

What does the future hold? A sudden stop of growth as happened in Japan in the 1990s seems unlikely; a more probable role model is Korea, whose growth pattern is shown in Figure 8. Korea’s very rapid growth in the 1970s slowed in an irregular pattern to the 4-5% range by the years 2000-10. Growth was broken in 1979-80 by the collapse of a government investment push in heavy and chemical industries, and another burst of overinvestment ended badly in the financial crisis of 1997-98. But much depends on the choices made by the government. A continuing determination to maintain 10% real output growth above all else could end badly.

By far the best course would be to stimulate local consumption. This would imply rapidly rising wages and a return to positive real interest rates on deposits – no other program could stimulate local consumption as well. But the tradeoff would be an immediate reduction in the profits of banks and/or firms, at a time when both are beginning to face a new round of NPLs. Such a departure would surely be resisted by these powerful interests.

The Chinese leadership has a well-established pattern of gradualism, so any change in favor of workers and consumers is likely to move slowly, though it must surely come in due course. In the meantime, it seems more than likely that the golden age of Chinese super-growth is nearing an end. No doubt China has a bright future, given the entrepreneurial energy of its people and the careful, pragmatic path taken by its government in economic policy. But China is at a crossroads. The old growth model has almost run its course, and a new one needs to be developed. The path needs to turn a corner to head in a new direction. Only time will tell how challenging this transition will be.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}